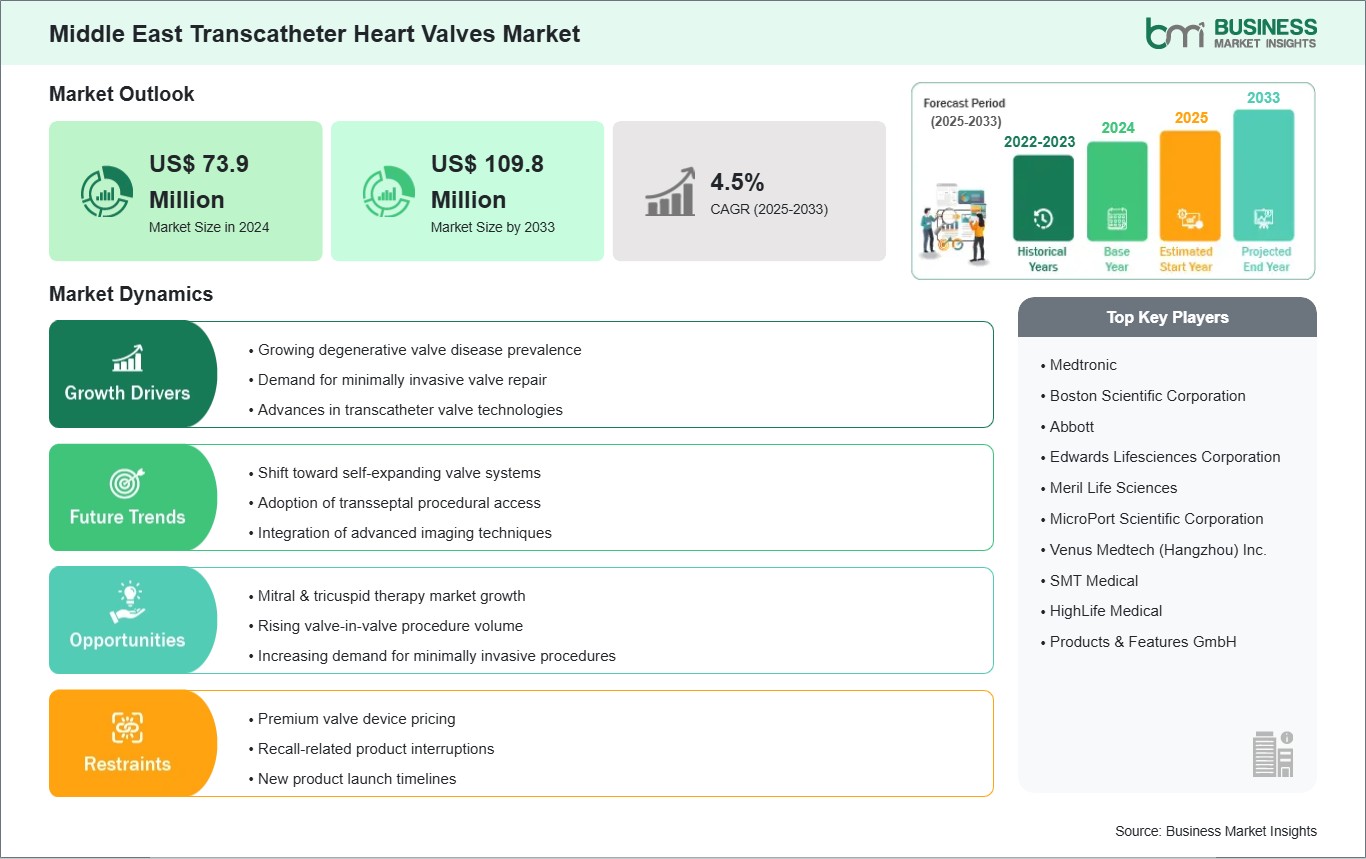

Growing degenerative valve disease prevalence

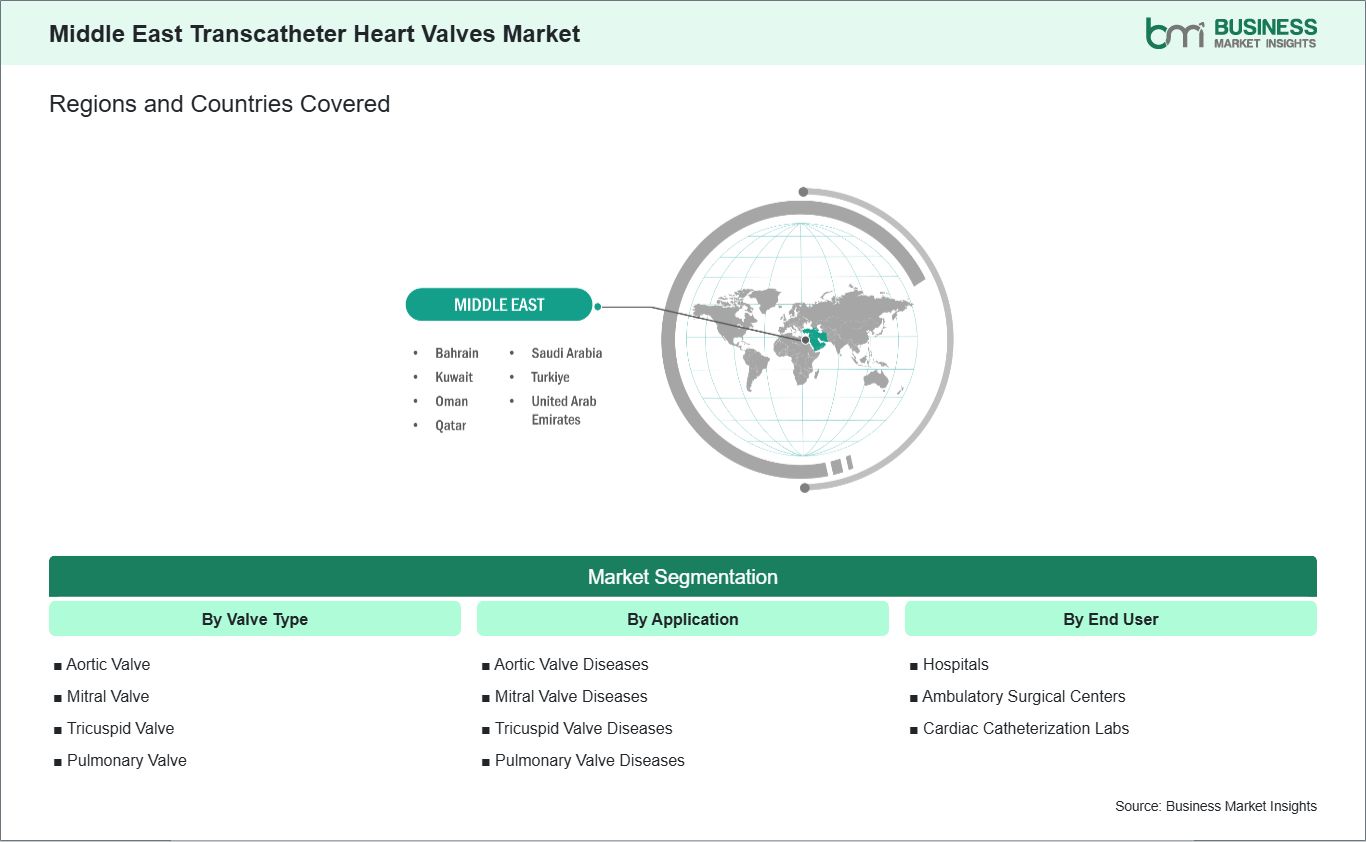

In the Middle East, valvular heart diseases are emerging as a growing health concern, particularly in aging populations and individuals with lifestyle-related cardiovascular risk factors such as obesity, hypertension, and diabetes. Countries such as Saudi Arabia, the UAE, and Qatar are observing an increase in degenerative valve conditions such as aortic stenosis and mitral regurgitation, alongside residual cases of rheumatic heart disease in some areas. Widespread use of echocardiography and other diagnostic technologies in urban hospitals is helping identify these conditions earlier, increasing the number of patients eligible for intervention.

While advanced cardiac surgery is available in major urban centers, many patients still face challenges such as procedural risk or extended recovery times. Transcatheter heart valve therapies offer a minimally invasive alternative, allowing high-risk and elderly patients to receive effective treatment with reduced hospitalization. Cardiac centers in cities such as Riyadh, Dubai, and Doha are increasingly adopting these procedures as part of their structural heart disease programs, making them more accessible to patients who would otherwise be limited to surgical options.

Government health initiatives and private sector investments are also supporting the adoption of minimally invasive cardiac care. Programs to expand cardiac infrastructure, train interventional cardiologists, and improve patient referral systems are helping to address the rising burden of valvular disease. As awareness among physicians and patients grows, the increasing prevalence of valvular heart disease is a major driver for transcatheter heart valve adoption in the Middle East.

Mitral & tricuspid therapy market growth

Historically, transcatheter interventions in the Middle East focused on the aortic valve, but clinical interest is shifting toward mitral and tricuspid valve disorders. Improved imaging, growing expertise among interventional cardiologists, and the availability of specialized devices are allowing physicians to diagnose and treat these complex valve conditions more effectively. Leading hospitals in Dubai, Abu Dhabi, Riyadh, and Doha are expanding their procedural offerings to include these valves, creating a significant market opportunity.

Patients with mitral or tricuspid valve dysfunction are often elderly or have multiple health complications that make conventional surgery risky. Minimally invasive transcatheter therapies provide a safer alternative, with shorter recovery times and fewer complications. Referral networks from smaller hospitals to urban cardiac centers are also helping more patients access these therapies, increasing overall awareness and adoption.

For device manufacturers and healthcare providers, this growth represents a clear opportunity. By offering training, procedural support, and clinical education, companies can help build physician confidence in performing these interventions. As expertise spreads and patient acceptance grows, mitral and tricuspid valve applications are expected to become a key growth segment in the Middle East transcatheter heart valve market.