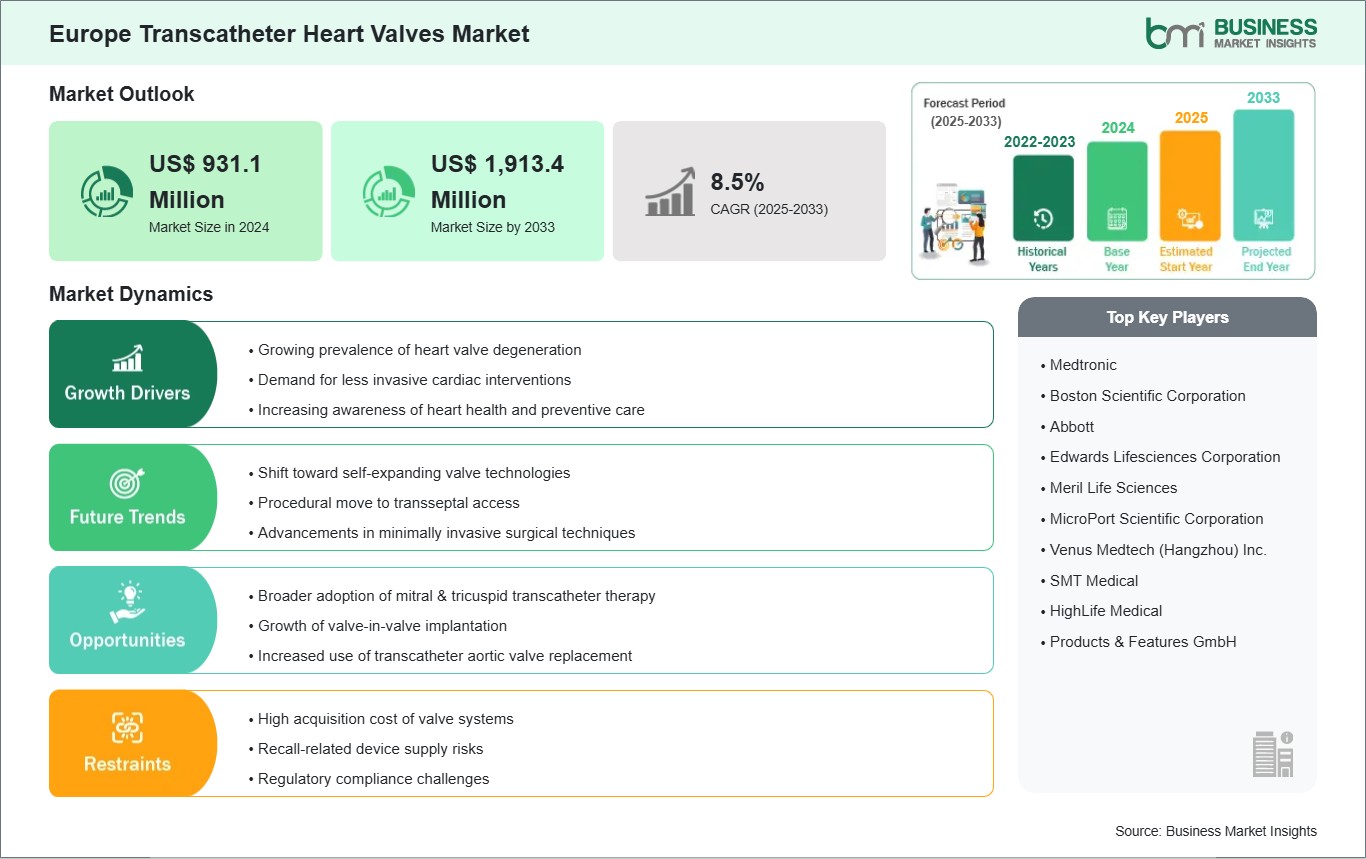

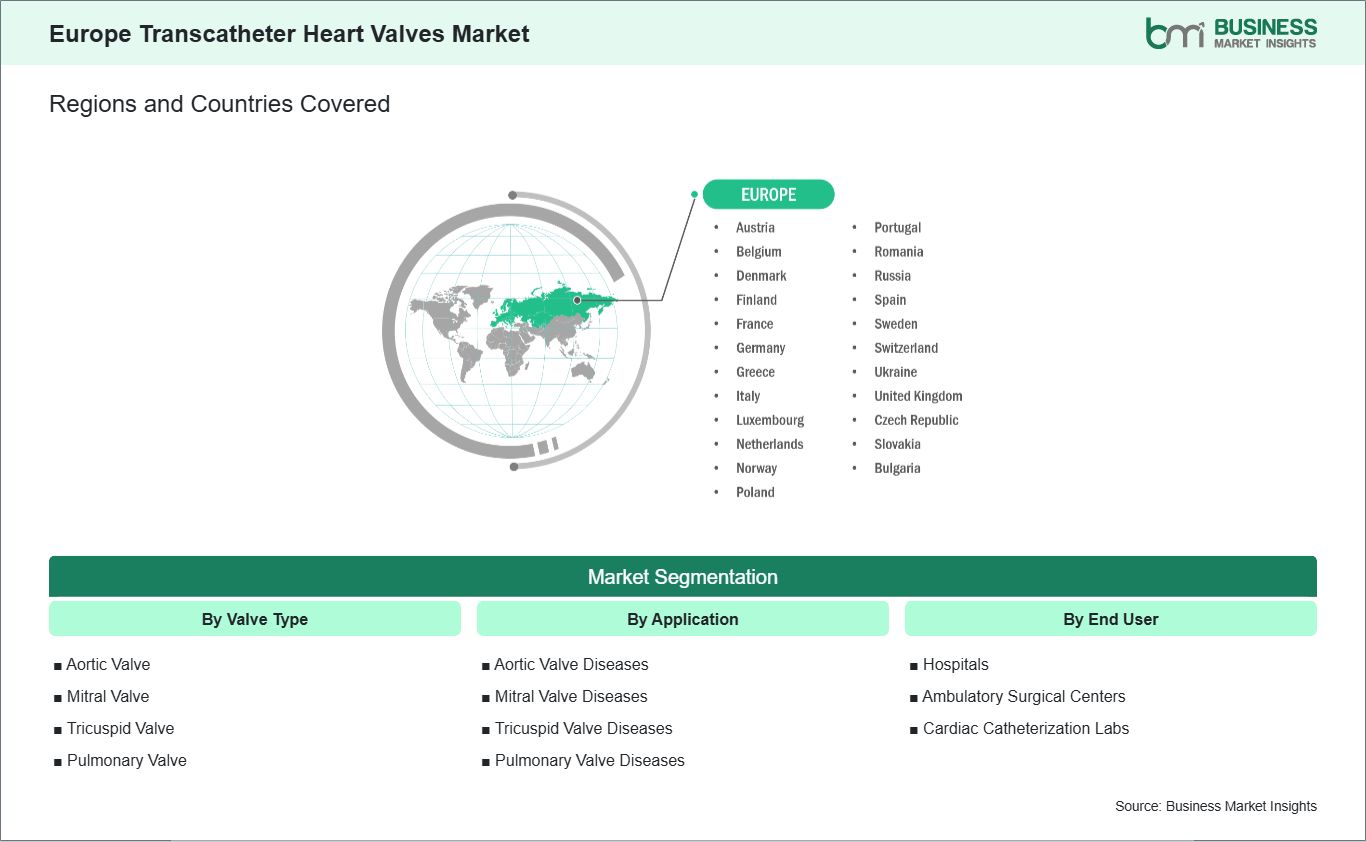

The geographical scope of the Europe Transcatheter Heart Valves market report is divided into: Germany, Italy, France, the UK, Spain, Belgium, the Netherlands, Luxembourg, Norway, Finland, Denmark, Sweden, Austria, Switzerland, Russia, Romania, Greece, the Czech Republic, Portugal, Ukraine, Poland, Slovakia, and Bulgaria. Germany held the largest share in 2024.

Germany represents the dominant country in the Europe transcatheter heart valves market, driven by its advanced healthcare infrastructure, strong clinical expertise, and long-standing leadership in cardiovascular medicine. The country is recognized for its early adoption of innovative medical technologies and its strong emphasis on minimally invasive treatment modalities, particularly in the field of interventional cardiology. German hospitals are equipped with state-of-the-art catheterization laboratories and hybrid operating rooms, enabling efficient and safe performance of transcatheter heart valve procedures. A well-structured referral system and the presence of multidisciplinary heart teams support accurate patient selection and consistent procedural outcomes, reinforcing physician and patient confidence in transcatheter therapies.

Germany's healthcare reimbursement environment plays a crucial role in facilitating access to these procedures, allowing hospitals to integrate transcatheter valve interventions into routine clinical practice. Furthermore, the country's active participation in clinical research, registries, and post-market surveillance initiatives contributes to continuous evaluation and optimization of treatment protocols. At the same time, the German market is influenced by increasing focus on long-term clinical outcomes, device durability, and cost-effectiveness, particularly as transcatheter therapies are considered for broader patient populations. Despite these considerations, Germany continues to set clinical and procedural benchmarks for transcatheter heart valve adoption across Europe.