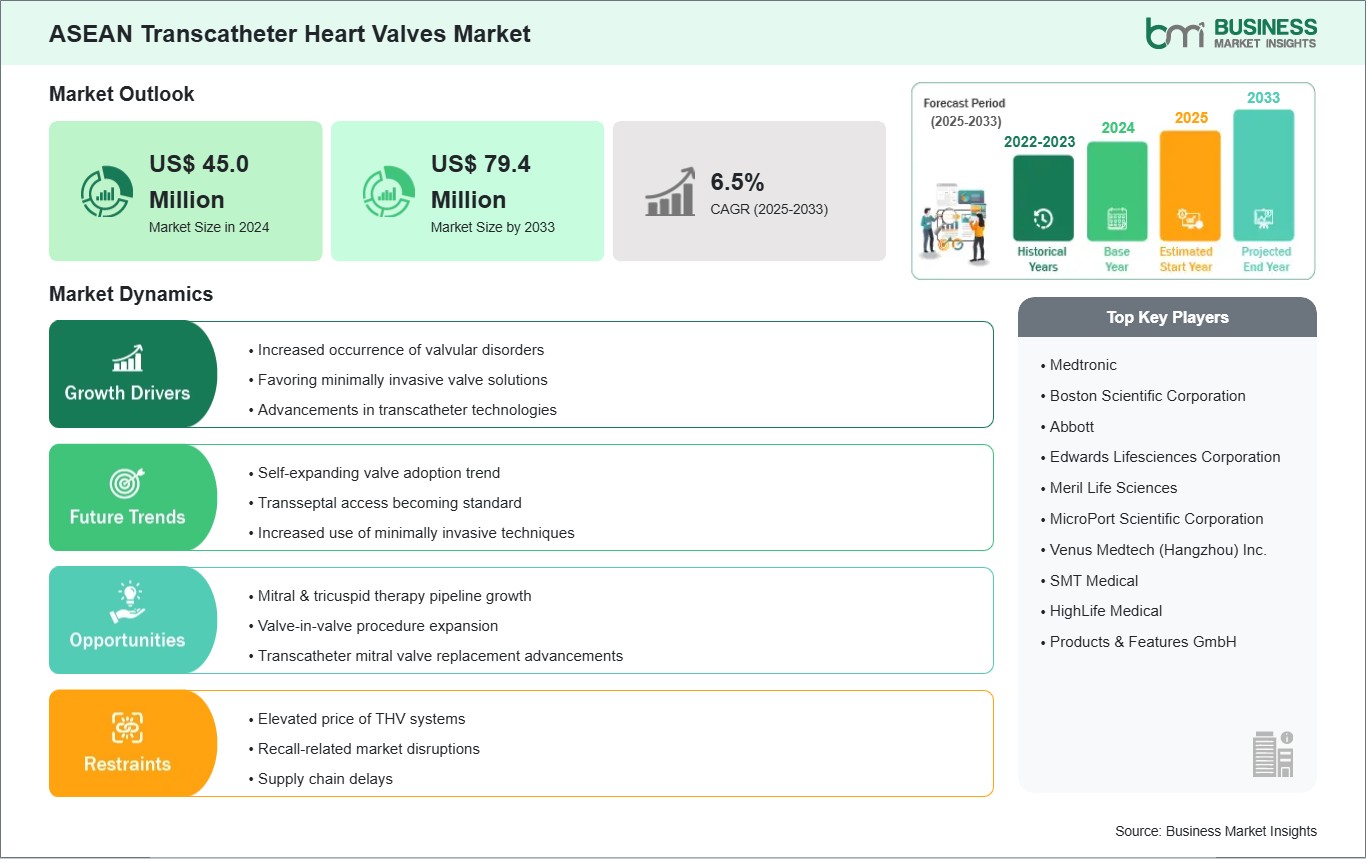

Increased occurrence of valvular disorders

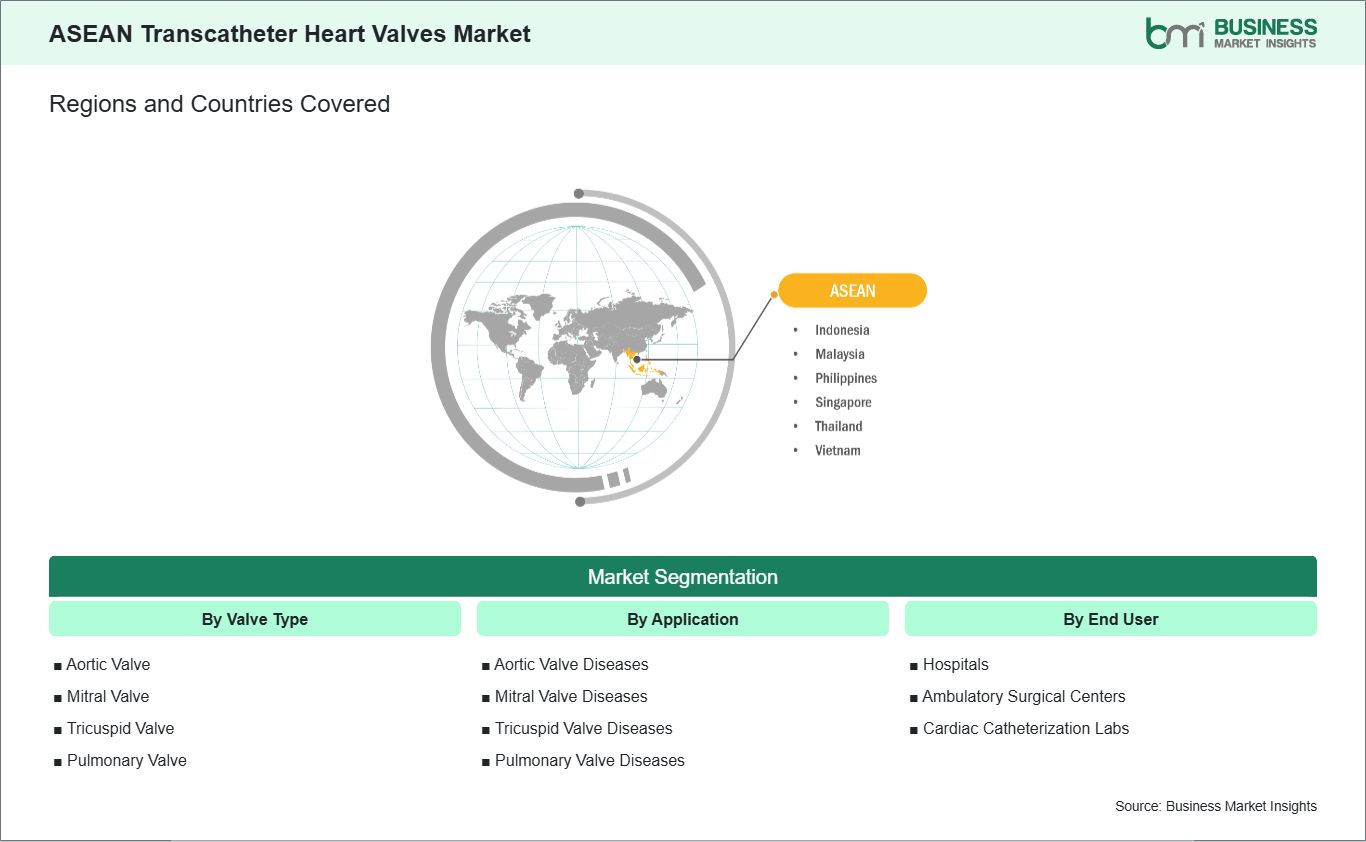

In ASEAN, valvular heart diseases are recognized as a pressing health concern. Rapid urbanization, lifestyle shifts, and aging populations are contributing to more cases of aortic and other valve dysfunctions. Many patients are living longer with chronic conditions, which raises the likelihood of developing issues that require medical intervention. As diagnosis rates improve through better access to clinics and imaging tools, healthcare providers across ASEAN are encountering more patients with moderate to severe valve problems that need advanced treatment options.

Traditional open-heart surgery remains common in the region, but it poses challenges such as lengthy recovery times, higher risk for older adults, and reliance on large tertiary care centers. Many patients in ASEAN countries seek alternatives that reduce hospital stay and procedural risk. This environment makes transcatheter heart valve therapies more attractive, especially for patients who are at greater surgical risk. Cardiologists and cardiac centers in urban hubs such as Singapore, Kuala Lumpur, and Bangkok are reporting a steady increase in referrals for transcatheter procedures, driven by patient demand and clinical evidence of better outcomes for selected cases.

Governments and private healthcare systems are also beginning to prioritize minimally invasive cardiac care. Several ASEAN health ministries are supporting training programs and investing in catheterization labs, which help expand the availability of transcatheter interventions. As physician expertise, diagnostic infrastructure, and patient awareness continue to grow, the rising prevalence of valvular disease serves as a major driver for transcatheter heart valve adoption in the ASEAN market.

Mitral & tricuspid therapy pipeline growth

In many ASEAN countries, clinical focus in the past has been heavily weighted toward aortic valve disease, but there is a growing interest in treatments for mitral and tricuspid valve disorders. Improvements in cardiac imaging and specialist training are helping physicians identify and understand these conditions more effectively. As a result, doctors in the region are beginning to evaluate patients for transcatheter mitral and tricuspid procedures earlier, creating an opportunity to broaden the scope of valve therapies offered beyond aortic interventions.

Patients with mitral and tricuspid valve dysfunction often face significant symptom burden and limited treatment options, particularly in settings where surgical resources are stretched. Transcatheter therapies provide a less invasive pathway for those who are older or have other health issues that make surgery risky or less desirable. ASEAN cardiac centers are investing in the tools and training needed to perform these procedures. This trend is supported by rising referrals for structural heart disease management and collaborative efforts with global device developers to bring next-generation solutions into the region.

Medical device companies and healthcare leaders can play a role in accelerating this shift by facilitating education, procedural support, and outcome tracking specific to mitral and tricuspid interventions. These build confidence among physicians who may be early in their learning curve. As clinical expertise spreads and more patients become eligible and aware of these treatment options, growth in mitral and tricuspid valve applications stands out as a key opportunity to expand the transcatheter heart valve market across ASEAN.