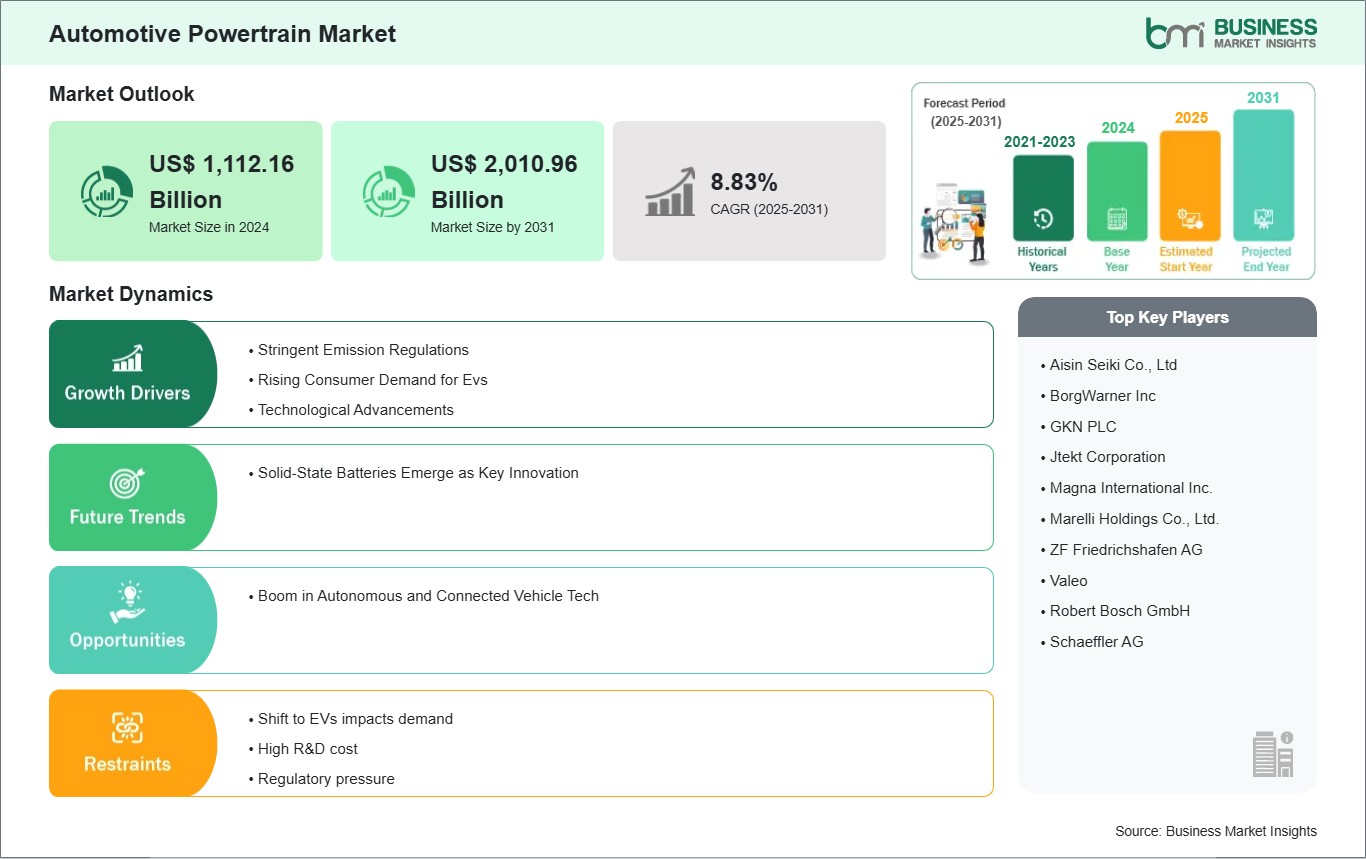

The Automotive Powertrain Market size is expected to reach US$ 2,010.96 Billion by 2031 from US$ 1,112.16 Billion in 2024. The market is estimated to record a CAGR of 8.83% from 2025 to 2031.

Executive Summary and Global Market Analysis:

The global automotive powertrain market is experiencing significant growth driven by stringent emission norms, rising consumer demand for EVs, and technological advancements. Automotive powertrain market on the basis of vehicle type encompasses passenger cars, light commercial vehicles, and heavy commercial vehicles. Passenger vehicles significantly influence the automotive powertrain industry, with market dynamics shaped by shifting user demands, environmental regulations, and innovative technologies. The passenger vehicle sector demonstrated continued expansion in 2024, propelled by heightened demand from developing markets, urban growth, and enhanced consumer purchasing power. The automotive powertrain industry, comprising traditional combustion engines (ICE) and electric vehicles (EVs), is experiencing fundamental changes

Governments are intensifying regulatory pressure on vehicle emissions through increasingly stringent environmental policies and compliance standards, driving the automotive powertrain market toward the adoption of cleaner, more sustainable technologies. The EU’s 95 g/km CO2 target for 2025 and the UK’s ZEV mandate, requiring 28% zero-emission vehicles, force automakers to swap low fuel-efficient vehicles for electric and hybrid powertrains. California’s aim for 68% EV sales by 2030 sets a global approach, while China’s NEV policies demand higher EV quotas. Non-compliance would invite steep fines, like €95 per g/km over the limit per vehicle in the EU. Countries like Norway are heading toward 100% EV sales by 2025, and cities such as London and Paris are banning ICE vehicles from urban zones. This pressure has encouraged automakers to invest heavily in EV and hybrid R&D. The transition extends beyond mere regulatory compliance; it represents a strategic imperative in an increasingly stringent regulatory environment where policymakers are intensifying enforcement and tightening industry standards.

Key segments that contributed to the derivation of the automotive powertrain market analysis are product, application, and end user.

By Vehicle Type, the automotive powertrain market is segmented into Passenger Cars, Light Commercial Vehicles (LCVs), Heavy Commercial Vehicles (HCVs. The passenger cars segment dominated the segment in 2024

By Drive Type, the automotive powertrain market is segmented into Front-Wheel Drive, Rear-Wheel Drive, All-Wheel Drive)

By Propulsion Type, the automotive powertrain market is segmented into ICE and Electric. The ICE segment dominated the market in 2024

By ICE Propulsion Type, the automotive powertrain market is segmented into Engine, Transmission Systems, Driveshafts, Differentials, Axles. Engine segment dominated the market in 2024

By Electric Propulsion Type, the automotive powertrain market is segmented into Motors, Battery Packs, Transmissions, Differentials, Axles. The battery segment dominated the market in 2024

By Sales Channel, the automotive powertrain market is segmented into OEM and Aftermarket. The OEM segment dominated the market in 2024

Automotive Powertrain Market Drivers and Opportunities:

Rising Consumer Demand for EVs

With fuel prices skyrocketing and climate change making the headlines, battery-electric vehicles (BEVs) and hybrids are picking up pace—global EV sales are set to reach 17 million in 2025, up by 20% from 2024. Better battery chemistries now offer 300-mile ranges, and costs are dropping, making EVs more affordable. Tax breaks, like US$ 7,500 in the US or subsidies in China and Europe, catalyze a paradigm shift toward mass acceptance of EVs. Over 3 million public chargers were online in 2024, easing range anxiety. New models such as Tesla’s Model Y and BYD’s Han indicate a clear market shift with customers increasingly prioritizing performance coupled with environmentally sustainable design. Cities charging congestion fees and banning gas cars compel drivers toward EVs. However, high upfront costs and the absence of charging networks in some areas slow down the transition rate, especially in poorer markets. Automakers are pushing to introduce over 200 BEV models planned for 2026, ranging from budget to luxury.

Technological Advancements

Emerging technologies are redefining the powertrain landscape, enabling vehicles to achieve superior acceleration, enhanced environmental sustainability, and greater cost efficiency. Solid-state batteries and lithium-iron-phosphate cells are improving EV ranges and slashing charge times, with companies such as CATL and Samsung SDI leading the market. Lightweight materials—carbon fiber, aluminum—reduce vehicle weight significantly, thereby boosting range and fuel economy. Electric motors deliver more power with less energy. Battery costs have dropped by 20% since 2020, making EVs closer to ICE vehicles in price. Modular platforms, such as Volkswagen’s MEB, streamline production and cut costs. However, raw material shortages and pricey R&D are hindering the market. Nevertheless, technology breakthroughs help automakers build versatile vehicle portfolios that cater to diverse customer segments while simultaneously ensuring compliance with increasingly stringent emissions regulations.

Boom in Autonomous and Connected Vehicle Tech

Autonomous vehicles require robust electric powertrains to support sophisticated AI computing systems, as illustrated by Nvidia's Drive platform managing pedestrian detection. While Tesla leads with its full self-driving capability, traditional manufacturers, e.g., BMW, are integrating electric powertrains with advanced sensor systems. Connected vehicles utilize 5G technology and software-driven powertrains for continuous data transmission and processing. Market adoption shows strong momentum, with projections indicating 60% of vehicles will feature connectivity by 2026. While Waymo establishes success with autonomous taxis in San Francisco, GM's Cruise faces challenges following safety incidents, highlighting tough market dynamics. These advanced systems require higher-cost components, including batteries and processors, and market forecasts suggest autonomous-capable premium electric vehicles could generate US$ 100 billion in additional market value by 2030. OEMs who successfully implement these technologies will establish market leadership in this transformative sector.

Automotive Powertrain Market Size and Share Analysis

The automotive powertrain market is classified according to vehicle into passenger cars, light commercial vehicles, and heavy commercial vehicles. The passenger car powertrain segment led the market in 2024 and beyond. Electric vehicles are showing remarkable momentum, with worldwide purchases expected to represent over 10% of car sales by 2025, driven by strict emission controls, state subsidies, and improved charging networks. European nations and China dominate electric vehicle uptake, while American markets show consistent expansion. Despite maintaining market leadership, traditional combustion engines face declining shares, especially in advanced economies, as automotive companies focus resources on electric technologies. Hybrid and plug-in vehicles provide transitional solutions, delivering improved fuel consumption and lower emissions, particularly attractive in areas with limited electric charging facilities. The powertrain sector benefits from innovations in lightweight components, turbocharging systems, and power-efficient solutions, enhancing combustion engine capabilities to satisfy emission requirements. Simultaneously, the declining cost of electric powertrains through production scaling and battery advancements enhances BEV competitiveness. However, the industry faces challenges due to supply network disruptions, battery material scarcity, and substantial initial EV costs. The Asia Pacific market leads in vehicle sales and powertrain manufacturing, with Chinese and Indian markets driving growth. As manufacturers pursue carbon neutrality targets, research in hydrogen fuel systems and eco-friendly production represents emerging trends, steering the powertrain industry toward an active transformation aligned with automotive electrification and sustainability objectives.

In terms of drive type, the market is segmented into front-wheel drive, rear-wheel drive, and all-wheel drive. The front-wheel drive (FWD) configuration continues to hold a substantial position in the worldwide automotive powertrain sector, especially for consumer vehicles and small commercial units, owing to its economical design, optimal space usage, and reduced fuel consumption. As of 2024, FWD layouts lead the small- and medium-sized vehicle categories, notably in city-focused regions such as Europe and Asia Pacific, propelled by the need for economical, productive transportation. The vehicle powertrain industry, including conventional engines (ICE), hybrid models (HEVs/PHEVs), and electric vehicles (BEVs), witnesses widespread FWD implementation across these propulsion types.

By propulsion type, the market is segmented into ICE and electric. The ICE powertrain segment held the largest share of the market in 2024. The internal combustion engine (ICE) powertrain remains the leading force in the global automotive powertrain sector through 2025, supported by its proven performance, cost-effectiveness, and established fuelling network, specifically for passenger vehicles, light commercial vehicles (LCVs), and heavy commercial vehicles (HCVs). While electric vehicles (BEVs) and hybrids (HEVs/PHEVs) gain momentum, ICE powertrains, both gasoline and diesel variants, hold substantial market dominance, notably in developing regions such as Asia Pacific, Latin America, and Africa, where fuel accessibility and economic benefits supersede electric vehicle advantages.

In terms of sales channel, the market is bifurcated into OEM and Aftermarket. The OEM segment emerged as the dominant sale channel in 2024. The Original Equipment Manufacturer (OEM) sales channel dominated the global automotive powertrain market in 2024, holding an estimated 68% share of the USD 1,112.16 billion market valued in 2024. This dominance is driven by robust vehicle production, particularly in China, which recorded 25 million vehicle sales in 2024, and India, with a 10.3% CAGR from 2019-2023. The OEM segment benefits from strong demand for internal combustion engine (ICE) powertrains, commanding an 88% share in 2024, alongside a surge in electric vehicle (EV) production, with global EV sales reaching 14 million units in 2023, up 35% YoY.

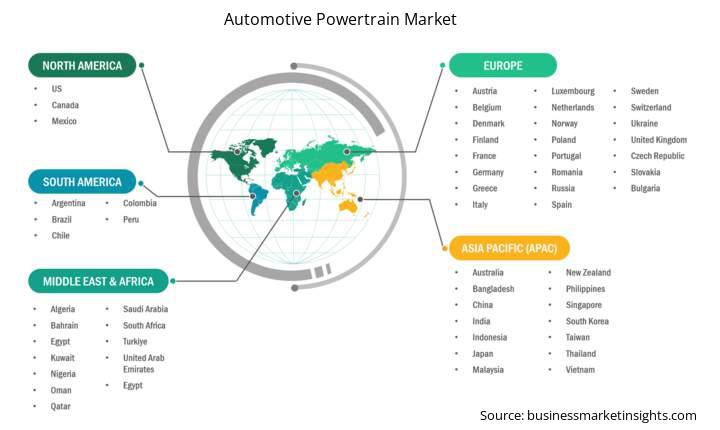

China, Japan, South Korea, India, Australia, New Zealand, Indonesia, Malaysia, Philippines, Singapore, Thailand, Vietnam, Taiwan, Bangladesh

South and Central America

Brazil, Argentina, Chile, Colombia, Peru

Middle East and Africa

Saudi Arabia, United Arab Emirates, Kuwait, Bahrain, Qatar, Oman, Turkiye, South Africa, Egypt, Nigeria, Algeria

Market leaders and key company profiles

Aisin Seiki Co., Ltd

BorgWarner Inc

GKN PLC

Jtekt Corporation

Magna International Inc.

Marelli Holdings Co., Ltd.

ZF Friedrichshafen AG

Valeo

Robert Bosch GmbH

Schaeffler AG

Get more information on this report

Automotive Powertrain Market Report Coverage and Deliverables

The "Automotive powertrain Market Size and Forecast (2021–2031)" report provides a detailed analysis of the market covering below areas:

Automotive powertrain market size and forecast at global, regional, and country levels for all the key market segments covered under the scope

Automotive powertrain market trends, as well as market dynamics such as drivers, restraints, and key opportunities

Detailed SWOT analysis

Automotive powertrain market analysis covering key market trends, global and regional framework, major players, regulations, and recent market developments

Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments for the automotive powertrain market

Detailed company profiles

Automotive Powertrain Market Country and Regional Insights

Get more information on this report

The geographical scope of the automotive powertrain market report is divided into five regions: North America, Asia Pacific, Europe, Middle East & Africa, and South & Central America. The automotive powertrain market in Asia Pacific is expected to grow significantly during the forecast period.

The Asia Pacific automotive powertrain sector, with key nations including China, Japan, India, South Korea, and neighboring countries, represents the world's biggest market, propelled by industrial growth, urban expansion, and increasing customer needs. At US$ 476.10 billion in 2024, it captured 42% of the worldwide market share, with projections indicating growth to US$ 890.86 billion by 2034, growing at 9.36% CAGR.

China leads the region with its strong automotive industry, representing over 60% of regional EV sales in 2024, supported by initiatives like the New Energy Vehicle (NEV) program. The passenger vehicle segment dominated with a 68% market share in 2024, driven by higher household incomes and metropolitan growth, especially in India and China. Traditional combustion engines maintained a 84% share in 2024, though gasoline powertrains face competition from hybrid and electric alternatives amid tighter emission controls and breakthroughs such as BYD's hybrid system, delivering 2,000+ km range.

Automotive Powertrain Market Research Report Guidance

The report includes qualitative and quantitative data in the automotive powertrain market across product, application, and end user, and geography.

The report starts with the key takeaways (chapter 2), highlighting the key trends and outlook of the automotive powertrain market.

Chapter 3 includes the research methodology of the study.

Chapter 4 further includes ecosystem analysis along with PEST analysis.

Chapter 5 highlights the major industry dynamics in the automotive powertrain market, including factors that are driving the market, prevailing deterrents, potential opportunities and future trends. Impact analysis of these drivers and restraints is also covered in this section.

Chapter 6 discusses the automotive powertrain market scenario, in terms of historical market revenues, and forecast till the year 2031.

Chapters 7 to 11 cover automotive powertrain market segments by vehicle type, drive type, propulsion type, sales channel, and geography across North America, Europe, APAC, Middle East and Africa, South and Central America. They cover market volume revenue forecast and factors driving the market.

Chapter 12 describes the competitive analysis along with the heat map analysis for the key players operating in the market.

Chapter 13 describes the industry landscape analysis. It provides detailed description of various business activities such as market initiatives, new developments, mergers, and joint ventures globally, along with a competitive landscape.

Chapter 14 provides a detailed profile of the major companies operating in the automotive powertrain market. The companies have been profiled on the basis of their key facts, business description, products and services, financial overview, SWOT analysis, and key developments.

Chapter 15, i.e., the appendix, is inclusive of a brief overview of the company, list of abbreviations, and disclaimer section.

Automotive Powertrain Market News and Key Development:

The automotive powertrain market is evaluated by gathering qualitative and quantitative data post primary and secondary research, which includes important corporate publications, association data, and databases. A few of the key developments in the automotive powertrain market are:

BMW: Committed ZAR 4.2 billion during 2023 to modernize its Rosslyn facility in South Africa, preparing for electric vehicle manufacturing by 2026, with initial focus on X3 production to support the nation's Just Energy Transition initiative.

BYD: Strengthened its Thai market position, driving a 639% year-over-year increase in BEV purchases in 2023, while launching the ATTO 3 model in South Africa, accelerating electric vehicle adoption across developing regions.

Bosch: Secured controlling interest in Seeo Inc. during February 2023, enhancing its ECU development capabilities for electric and hybrid powertrains through innovative battery solutions.

Key Sources Referred:

ACEA

International Organization of Motor Vehicle Manufacturers (OICA)

China Association of Automobile Manufacturers(CAAM)

Japan Automobile Manufacturers Association, Inc (JAMA)

International Energy Association (IEA)

American Automobile Association (AAA)

The List of Companies - Automotive Powertrain Market

Aisin Seiki Co., Ltd BorgWarner Inc, GKN PLC Jtekt Corporation Magna International Inc. Marelli Holdings Co., Ltd. ZF Friedrichshafen AG Valeo Robert Bosch GmbH Schaeffler AG

About Author— Automotive and Transportation Research Team

Dhananjay is a market research and consulting professional with over 5 years of experience in syndicated reports, consulting assignments, and custom research projects. He holds a Bachelor's degree in Pharmacy and an MBA in Marketing, combining technical domain knowledge with strong business acumen and analytical rigor.

Currently supporting end-to-end research engagements and delivering actionable, data-driven insights across multiple industries, Dhananjay is skilled in market forecasting, market sizing, competitive benchmarking, and trend analysis, with a strong focus on delivering high-quality, decision-ready insights for strategic..

Show More

Frequently Asked Questions

How big is the Automotive Powertrain Market?

The Automotive Powertrain Market is valued at US$ 1,112.16 Billion in 2024, it is projected to reach US$ 2,010.96 Billion by 2031.

What is the CAGR for Automotive Powertrain Market by (2025 - 2031)?

As per our report Automotive Powertrain Market, the market size is valued at US$ 1,112.16 Billion in 2024, projecting it to reach US$ 2,010.96 Billion by 2031. This translates to a CAGR of approximately 8.83% during the forecast period.

What segments are covered in this report?

The Automotive Powertrain Market report typically cover these key segments-

Vehicle Type (Passenger Cars, Light Commercial Vehicles, Heavy Commercial Vehicles)

Drive Type (Front-Wheel Drive, Rear-Wheel Drive, All-Wheel Drive)

Propulsion Type (ICE, Electric)

Sales Channel (OEM, Aftermarket)

What is the historic period, base year, and forecast period taken for Automotive Powertrain Market?

The historic period, base year, and forecast period can vary slightly depending on the specific market research report. However, for the Automotive Powertrain Market report:

Historic Period : 2021-2023

Base Year : 2024

Forecast Period : 2025-2031

Who are the major players in Automotive Powertrain Market?

The Automotive Powertrain Market is populated by several key players, each contributing to its growth and innovation. Some of the major players include:

Aisin Seiki Co., Ltd

BorgWarner Inc,

GKN PLC

Jtekt Corporation

Magna International Inc.

Marelli Holdings Co., Ltd.

ZF Friedrichshafen AG

Valeo

Robert Bosch GmbH

Schaeffler AG

Who should buy this report?

The Automotive Powertrain Market report is valuable for diverse stakeholders, including:

Investors: Provides insights for investment decisions pertaining to market growth, companies, or industry insights. Helps assess market attractiveness and potential returns.

Industry Players: Offers competitive intelligence, market sizing, and trend analysis to inform strategic planning, product development, and sales strategies.

Suppliers and Manufacturers: Helps understand market demand for components, materials, and services related to concerned industry.

Researchers and Consultants: Provides data and analysis for academic research, consulting projects, and market studies.

Financial Institutions: Helps assess risks and opportunities associated with financing or investing in the concerned market.

Essentially, anyone involved in or considering involvement in the Automotive Powertrain Market value chain can benefit from the information contained in a comprehensive market report.

Get Free Sample For Automotive Powertrain Market

Get Free Sample For Automotive Powertrain Market