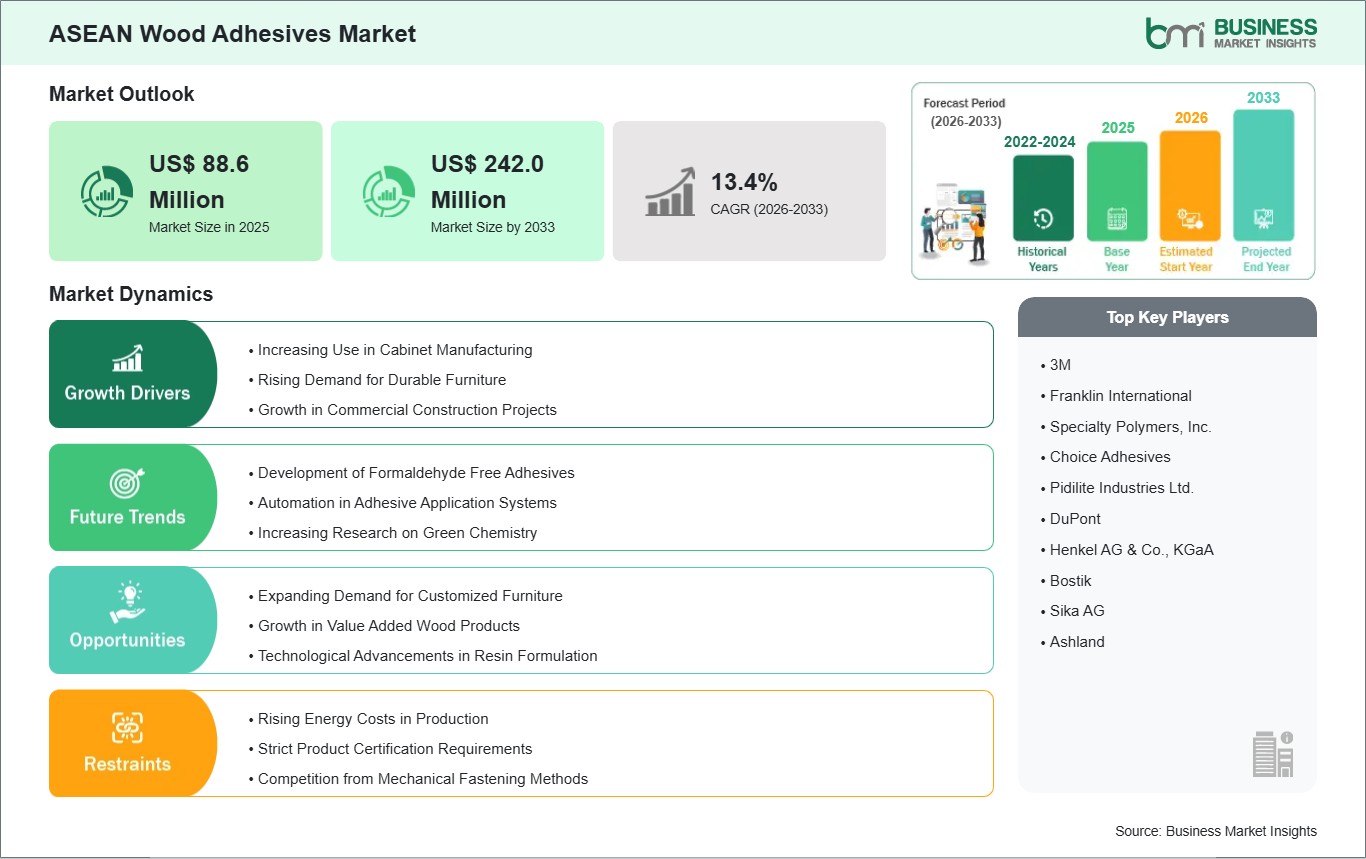

The ASEAN wood adhesives market size is expected to reach US$ 1,135.7 million by 2033 from US$ 627.4 million in 2025. The market is estimated to register a CAGR of 7.7% from 2026 to 2033.

Executive Summary and ASEAN Wood Adhesives Market Analysis:

Wood adhesives in the ASEAN region function as essential bonding agents across furniture manufacturing, construction paneling, flooring systems, and engineered wood production, supporting structural integrity and design versatility. The market is experiencing steady industrial integration as manufacturing hubs in Southeast Asia expand their output of value-added wood products for both domestic consumption and export markets. Rising urbanization across the region is encouraging higher utilization of wood-based interior materials, particularly in residential housing and commercial fit-out projects. Manufacturers are increasingly focusing on water-based, low-emission, and formaldehyde-reduced adhesive formulations to align with tightening environmental and workplace safety expectations. Additionally, the expansion of organized furniture manufacturing clusters in countries such as Vietnam, Thailand, and Indonesia is strengthening demand consistency. Supply chain localization and cost-competitive production capabilities are improving regional competitiveness against global suppliers. Technological upgrades in lamination, veneer bonding, and engineered board production are further enhancing adhesive consumption intensity. The competitive environment remains moderately fragmented, with both multinational chemical suppliers and regional producers competing on pricing efficiency, product reliability, and distribution reach. Growing export-oriented furniture production continues to reinforce long-term consumption stability across ASEAN economies.

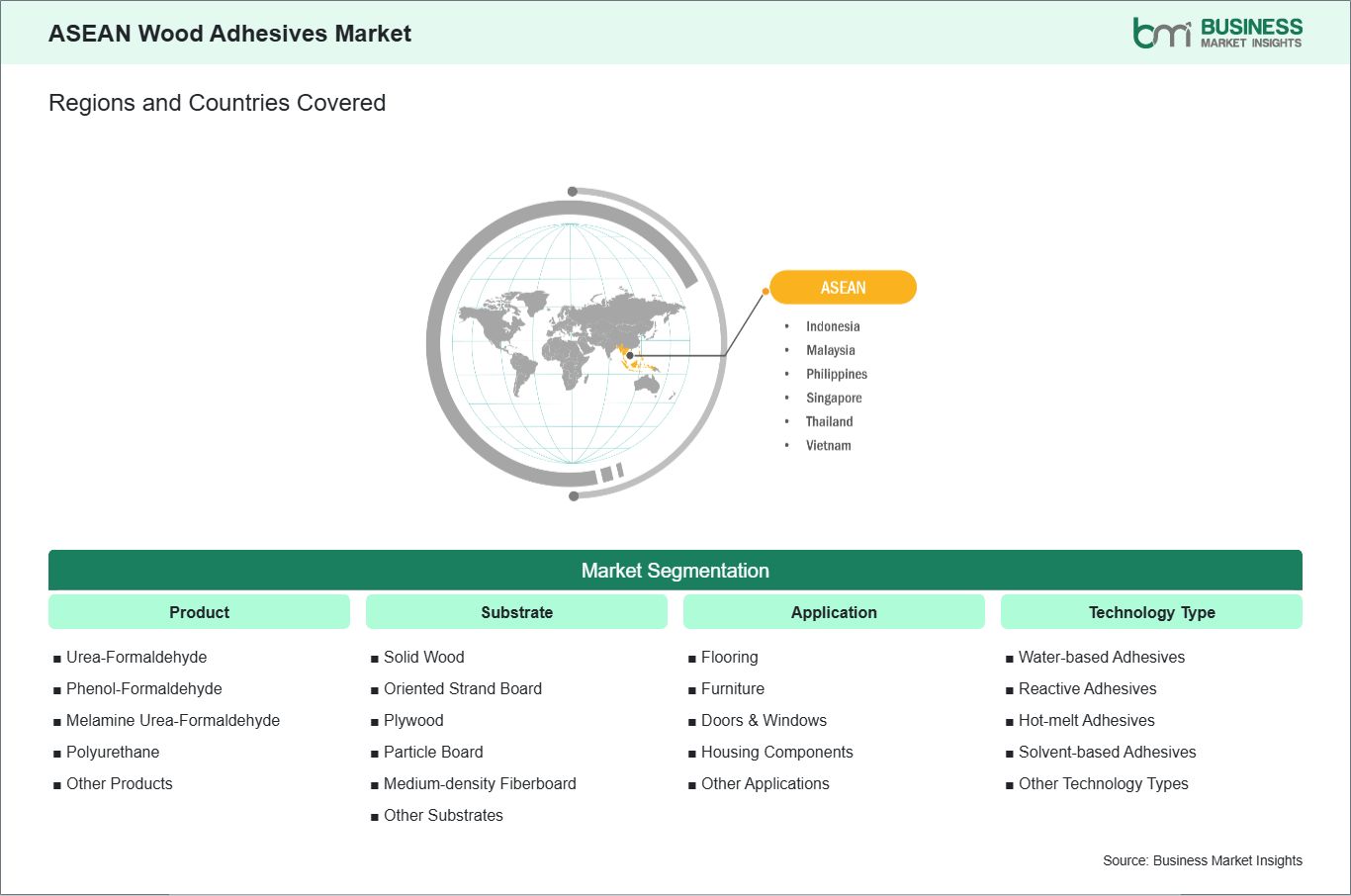

Key segments that contributed to the derivation of the ASEAN wood adhesives market analysis are product, substrate, application, and technology type.

By product, the wood adhesives market is segmented into urea-formaldehyde (UF), phenol-formaldehyde (PF), melamine urea-formaldehyde (MUF), polyurethane (PU), and other products. The urea-formaldehyde (UF) segment dominated the market in 2025.

Based on substrate, the wood adhesives market is segmented into solid wood, oriented strand board (OSB), plywood, particle board (PB), medium-density fiberboard (MDF), and other substrates. The particle board (PB) segment dominated the market in 2025.

On the basis of application, the wood adhesives market is classified as flooring, furniture, doors & windows, housing components, and other applications. The furniture segment dominated the market in 2025.

In terms of technology type, the wood adhesives market is segmented into water-based adhesives, reactive adhesives, hot-melt adhesives, solvent-based adhesives, and other technology types. The water-based adhesives segment dominated the market in 2025.

ASEAN Wood Adhesives Market Drivers and Opportunities:

Growing Demand for Lightweight Panels

The ASEAN wood adhesives market is experiencing strong growth due to increasing adoption of lightweight panel materials in construction and interior applications. Urbanization is rapidly taking place in developing nations such as Indonesia, Vietnam, Thailand, Malaysia, and Philippines. As such, there is increased demand for engineered wood products such as plywood, medium density fiberboard (MDF), and particle boards because of their cost effectiveness and convenience when used for construction in dense urban environments.

The production of furniture has also played an important role in this trend, especially with regard to countries like Vietnam and Malaysia, which are prominent exporters of wooden furniture products. In order to cope with global design specifications and cut costs on transportation, manufacturers have resorted to using light composite panels. This has made there be a need for adhesives like polyurethane, melamine urea formaldehyde, and PVAC.

Environmental concerns and raw material optimization are further accelerating the shift toward engineered wood panels. Countries like Thailand and Indonesia are promoting sustainable forestry practices and value-added wood processing industries. This has led to higher utilization of plantation timber and wood residues, which require advanced bonding solutions for structural stability. The expanding use of lightweight panels across residential and commercial applications continues to strengthen adhesive demand across the ASEAN region.

Growth in Prefabricated Building Solutions

The ASEAN region is witnessing rapid expansion in prefabricated and modular construction methods, significantly boosting the wood adhesives market. Governments in Singapore, Malaysia, and Indonesia are encouraging modern construction technologies to address urban housing shortages and reduce project timelines. Prefabricated wooden housing units, wall panels, and modular interior systems rely heavily on high-performance adhesives for structural integrity and assembly efficiency.

Urban housing demand is particularly strong in fast-growing cities such as Jakarta, Ho Chi Minh City, and Manila, where population density is high and land availability is limited. Prefabricated solutions offer faster construction cycles and cost advantages, increasing their adoption in both public housing projects and private residential developments. This shift is directly increasing consumption of structural adhesives used in panel bonding and lamination processes.

Industrial development and construction innovation are also supporting market expansion. Countries like Vietnam and Thailand are developing smart industrial parks and export-oriented construction hubs, where prefabricated building components are increasingly used. These facilities rely on consistent adhesive performance for mass production of standardized components. As prefabrication gains momentum across ASEAN’s construction sector, demand for durable, high-efficiency wood adhesives is expected to grow steadily.

ASEAN Wood Adhesives Market Size and Share Analysis:

The wood adhesives market in ASEAN is experiencing steady growth, with market size and share analysis reflecting evolving treatment preferences and competitive dynamics among key players. The report evaluates important subsegments categorized within product, substrate, application, and technology, highlighting their respective contributions to market performance.

By product, the urea-formaldehyde (UF) segment dominated the market in 2025, driven by strong penetration in cost-sensitive plywood and particleboard production supported by expanding construction and furniture manufacturing.

Based on substrate, the particle board (PB) segment dominated the market in 2025, driven by increasing adoption in budget furniture and modular interiors fueled by rapid urban housing development.

On the basis of application, the furniture segment dominated the market in 2025, driven by rising middle-class income levels and fast-growing demand for ready-to-assemble and space-efficient home solutions.

In terms of technology, the water-based adhesives segment dominated the market in 2025, driven by tightening environmental regulations and the shift toward low-emission, worker-safe adhesive technologies in wood processing.

ASEAN Wood Adhesives Market Report Highlights:

Report Attribute

Details

Market size in 2025

US$ 627.4 Million

Market Size by 2033

US$ 1,135.7 Million

CAGR (2026 - 2033)

7.7%

Historical Data

2022-2024

Forecast period

2026-2033

Segments Covered

By Product

Urea-Formaldehyde

Phenol-Formaldehyde

Melamine Urea-Formaldehyde

Polyurethane

Other Products

By Substrate

Solid Wood

Oriented Strand Board

Plywood

Particle Board

Medium-density Fiberboard

Other Substrates

By Application

Flooring

Furniture

Doors & Windows

Housing Components

Other Applications

By Technology Type

Water-based Adhesives

Reactive Adhesives

Hot-melt Adhesives

Solvent-based Adhesives

Other Technology Types

Regions and Countries Covered

ASEAN

Indonesia, Malaysia, the Philippines, Singapore, Thailand, Vietnam

Market leaders and key company profiles

3M

Franklin International

Specialty Polymers, Inc.

Choice Adhesives

Pidilite Industries Ltd.

DuPont

Henkel AG & Co., KGaA

Bostik

Sika AG

Ashland

Get more information on this report

ASEAN Wood Adhesives Market Report Coverage and Deliverables:

The "ASEAN Wood Adhesives Market Size and Forecast (2022–2033)" report provides a detailed analysis of the market covering below areas:

Market size and forecast at the regional and country levels for segments covered under the scope

Market trends, as well as drivers, restraints, and opportunities

Market analysis, covering key trends, regional framework, major players, regulations, and recent developments

Market concentration, heat map analysis, prominent players, and recent developments for the Market

Detailed company profiles, including SWOT analysis

ASEAN Wood Adhesives Market Geographic Insights:

The geographical scope of the ASEAN wood adhesives market report is divided into Indonesia, Malaysia, the Philippines, Singapore, Thailand, Vietnam. Indonesia held the largest share in 2025.

Indonesia emerges as the dominant market within ASEAN, supported by its large-scale raw material availability, expanding furniture manufacturing sector, and growing domestic construction activity. The country benefits from strong integration of upstream wood processing industries with downstream furniture and panel production, enabling consistent adhesive demand across multiple value chains. Increasing investments in residential housing and commercial infrastructure projects are further strengthening consumption of engineered wood products and related adhesive systems. Vietnam represents a major export-oriented hub, driven by its strong participation in global furniture supply chains and rapid expansion of plywood and MDF production facilities. Thailand maintains a stable industrial base supported by established woodworking clusters and growing demand for interior construction materials across urban development projects. Malaysia demonstrates a technology-driven market with emphasis on high-value engineered wood products and advanced manufacturing processes, particularly in export-oriented industrial zones. Other ASEAN economies, including the Philippines and emerging smaller markets, are experiencing gradual growth supported by infrastructure expansion, urban housing demand, and increasing adoption of wood-based interior materials. Across the region, foreign investment inflows, manufacturing relocation trends, and evolving sustainability standards are shaping procurement patterns, with increasing preference for environmentally compliant adhesive formulations in industrial applications.

Get more information on this report

ASEAN Wood Adhesives Market Research Report Guidance:

The report includes qualitative and quantitative data in the ASEAN wood adhesives market product, substrate, application, technology, and geography.

The report starts with the key takeaways (chapter 2), highlighting the key trends and outlook of the ASEAN wood adhesives market.

Chapter 3 focuses on the research methodology of the study.

Chapter 4 includes ecosystem analysis.

Chapter 5 highlights the major industry dynamics in the ASEAN wood adhesives market, including factors that are driving the market, prevailing deterrents, potential opportunities, as well as future trends. Impact analysis of these drivers and restraints is also covered in this section.

Chapter 6 discusses the ASEAN wood adhesives market scenario, in terms of historical market revenues, and forecast till the year 2033.

Chapters 7 to 11 cover the ASEAN wood adhesives market segments by product, substrate, application, technology, and geography across Indonesia, Malaysia, the Philippines, Singapore, Thailand, Vietnam. They cover the market revenue, forecast, and factors driving the market.

Chapter 12 describes the competitive analysis along with the heat map analysis for the key players operating in the market.

Chapter 13 describes the industry landscape analysis. It provides detailed descriptions of business activities such as market initiatives, new developments, mergers, and joint ventures globally, along with a competitive landscape.

Chapter 14 provides detailed profiles of the major companies operating in the ASEAN wood adhesives market. Companies have been profiled on the basis of their key facts, business descriptions, products, financial overview, SWOT analysis, and key developments.

Chapter 15, i.e., the appendix, is inclusive of a brief overview of the company, list of abbreviations, and disclaimer.

ASEAN Wood Adhesives Market News and Key Development:

The ASEAN wood adhesives market is evaluated by gathering qualitative and quantitative data post primary and secondary research, which includes important corporate publications, association data, and databases. A few of the key developments in the ASEAN wood adhesives market are:

In September 2025, Henkel AG & Co. KGaA introduced new micro-emission hot-melt adhesive technologies at LIGNA 2025, targeting furniture and engineered wood manufacturing, with rollout extended to ASEAN markets including Malaysia, Indonesia, and Thailand via its regional supply chain.

In January 2025, Sika AG opened a new high-capacity manufacturing plant in Singapore focused on mortars and construction adhesives, strengthening regional supply for Southeast Asia markets including wood panel, flooring, and interior construction applications.

Key Sources Referred:

Food and Agriculture Organization (FAO)United Nations Industrial Development Organization (UNIDO)World BankInternational Trade Centre (ITC)Organization for Economic Co-operation and Development (OECD)European Chemicals Agency (ECHA)S. Environmental Protection Agency (EPA)International Organization for Standardization (ISO)United Nations Environment Programme (UNEP)World Trade Organization (WTO)

Identical Market Reports with other Region/Countries

Suraj Sajeev is a market research and consulting professional with nearly 10 years of experience across Life Sciences, Consumer Goods, Food & Beverages, Materials & Chemicals, and Automotive industries. Throughout his career, he has successfully managed and delivered custom market research and consulting engagements, enabling clients to make informed strategic decisions through actionable market intelligence.

Suraj has extensive expertise in end-to-end project management, including proposal development, market assessment, competitive intelligence, opportunity analysis, market sizing and forecasting, strategic recommendation..

Show More

Frequently Asked Questions

How big is the ASEAN Wood Adhesives Market?

The ASEAN Wood Adhesives Market is valued at US$ 627.4 Million in 2025, it is projected to reach US$ 1,135.7 Million by 2033.

What is the CAGR for ASEAN Wood Adhesives Market by (2026 - 2033)?

As per our report ASEAN Wood Adhesives Market, the market size is valued at US$ 627.4 Million in 2025, projecting it to reach US$ 1,135.7 Million by 2033. This translates to a CAGR of approximately 7.7% during the forecast period.

What segments are covered in this report?

The ASEAN Wood Adhesives Market report typically cover these key segments-

Application (Flooring, Furniture, Doors & Windows, Housing Components, Other Applications)

Technology Type (Water-based Adhesives, Reactive Adhesives, Hot-melt Adhesives, Solvent-based Adhesives, Other Technology Types)

What is the historic period, base year, and forecast period taken for ASEAN Wood Adhesives Market?

The historic period, base year, and forecast period can vary slightly depending on the specific market research report. However, for the ASEAN Wood Adhesives Market report:

Historic Period : 2022-2024

Base Year : 2025

Forecast Period : 2026-2033

Who are the major players in ASEAN Wood Adhesives Market?

The ASEAN Wood Adhesives Market is populated by several key players, each contributing to its growth and innovation. Some of the major players include:

3M

Franklin International

Specialty Polymers, Inc.

Choice Adhesives

Pidilite Industries Ltd.

DuPont

Henkel AG & Co., KGaA

Bostik

Sika AG

Ashland

Who should buy this report?

The ASEAN Wood Adhesives Market report is valuable for diverse stakeholders, including:

Investors: Provides insights for investment decisions pertaining to market growth, companies, or industry insights. Helps assess market attractiveness and potential returns.

Industry Players: Offers competitive intelligence, market sizing, and trend analysis to inform strategic planning, product development, and sales strategies.

Suppliers and Manufacturers: Helps understand market demand for components, materials, and services related to concerned industry.

Researchers and Consultants: Provides data and analysis for academic research, consulting projects, and market studies.

Financial Institutions: Helps assess risks and opportunities associated with financing or investing in the concerned market.

Essentially, anyone involved in or considering involvement in the ASEAN Wood Adhesives Market value chain can benefit from the information contained in a comprehensive market report.

Get Free Sample For ASEAN Wood Adhesives Market

Get Free Sample For ASEAN Wood Adhesives Market