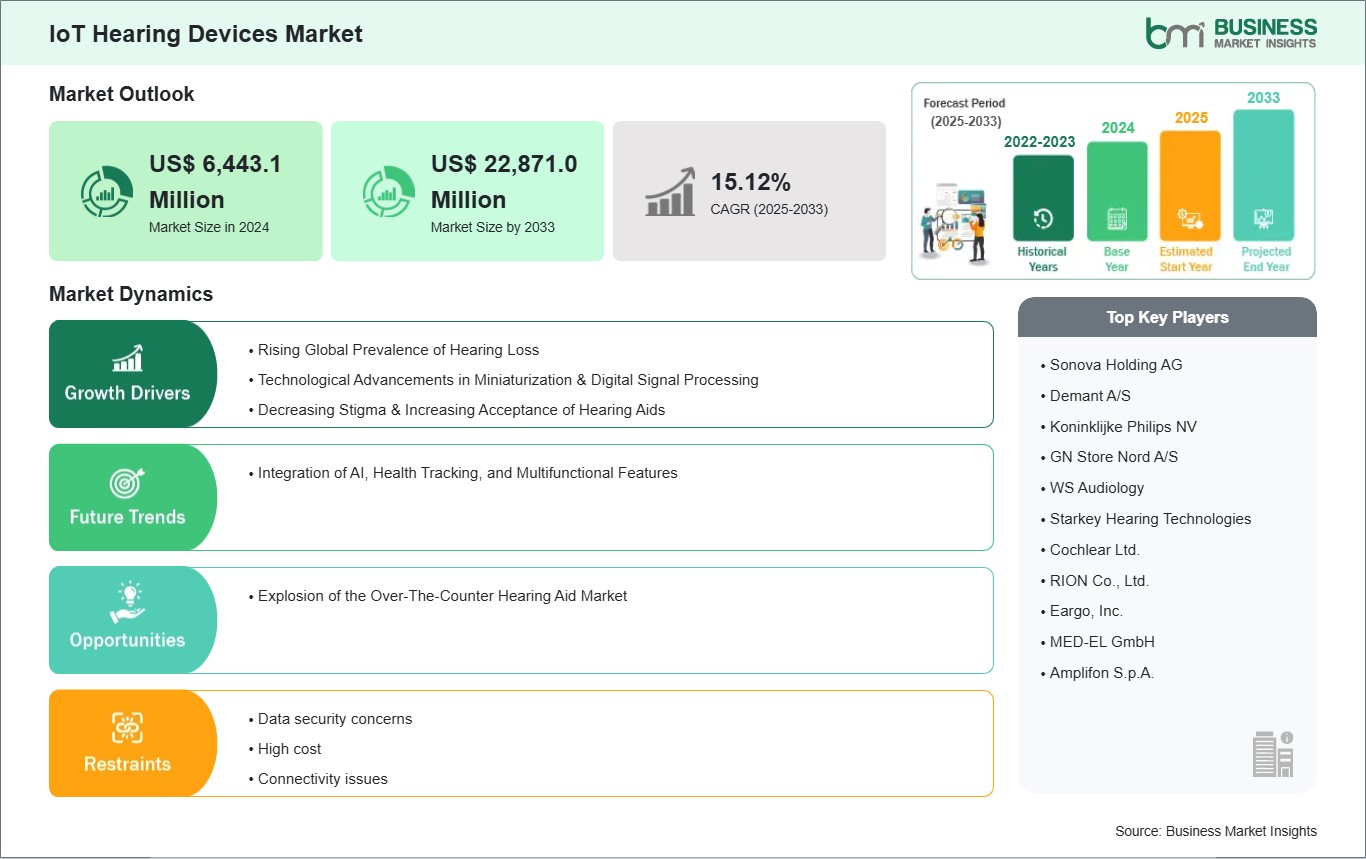

The IoT Hearing Devices Market size is expected to reach US$ 22,871.0 Million by 2033 from US$ 6,443.1 Million in 2024. The market is estimated to record a CAGR of 15.12% from 2025 to 2033.

Executive Summary and Global Market Analysis:

The global IoT hearing devices market is experiencing significant growth driven by rising global prevalence of hearing loss, technological advancements in miniaturization & digital signal processing, decreasing stigma & increasing acceptance of hearing aids. However, the lack of standardization and associated security and privacy concerns are slowing market evolution. Geographically, the largest market share was in North America due to a strong healthcare infrastructure, increased public awareness and acceptance of newer technology related to medical needs, large manufacturers in the region, and a pro-regulatory environment, with the passing and approval of over-the-counter (OTC) hearing aids recently. The fastest-growing region is the Asia-Pacific (APAC) region, due to a rapidly changing healthcare infrastructure, a massive aging population, increasing disposable incomes, and a growing awareness of health and well-being campaigns. The leading companies in this space are Sonova Holding AG, GN Store Nord A/S, Demant A/S, WS Audiology, Starkey Hearing Technologies, and Cochlear Ltd., with all of these companies looking to innovate and work with new technologies in order to expand their market and global reach as a company.

IoT Hearing Devices Market Strategic Insights

Key segments that contributed to the derivation of the IoT Hearing Devices market analysis are product, technology, application, and end user.

- By product, IoT hearing devices market is segmented into smart hearing aids, IoT cochlear implants, bone anchored hearing devices, tinnitus maskers, and others. The smart hearing aids segment dominated the market in 2024.

- By technology, IoT hearing devices market is segmented into Wi-Fi, Bluetooth, and others. The Bluetooth segment dominated the market in 2024.

- In terms of application, the market is segmented into hearing loss treatment, audio streaming, tinnitus therapy, and others. The hearing loss treatment segment held the largest share of the market in 2024.

- By end user, the market is segmented into ENT hospitals, audiology clinics, and others. The audiology clinics segment held the largest share of the market in 2024.

IoT Hearing Devices Market Drivers and Opportunities:

Increasing Prevalence of Hearing Loss Driving IoT Hearing Devices Market

The increasing prevalence of hearing loss globally is a foundational and powerful driver for the expansion of the IoT hearing devices market. Current statistics estimate that a significant number of the world's population has some form of hearing impairment and predicted forecasts show the number of people who will need some form of hearing rehabilitation is expected to grow substantially over the next decades. This growing and widespread burden of health represents a persistent and growing demand for effective solutions. Hearing loss impacts communication, social interaction, cognition, and quality of life, and it has never been more urgent to provide high quality, accessible, and user-friendly hearing solutions. One of the main contributors to the rising prevalence of hearing loss is the rapidly growing elderly population in the world. Age-related hearing loss, called presbycusis, is one of the most prevalent sensory deficits in the elderly population and the prevalence rises significantly with age. Age is not the only factor related to the increase in hearing loss, as exposure to loud noise is more prevalent than ever (e.g. personal audio technology, occupational exposure), chronic diseases, and ototoxic drugs are also contributions to the numbers rising across all ages. As more people are aware of the impact of their hearing impairment and adopt solutions, the potential for IoT hearing devices to provide users with more than just basic amplification should be a constant trend in the progress of IoT hearing devices.

Explosion of the Over-The-Counter Hearing Aid Market

The enormous growth of the over-the-counter (OTC) hearing aid category is a major opportunity for the IoT hearing devices industry. Until recently, the common experience of purchasing hearing aid involved a lengthy process that cost thousands of dollars and potentially carried a social stigma of "needing a hearing aid", as it required professional consultation, testing, and fitting by a certified audiologist. This process acted as a roadblock for the millions of people with mild to moderate hearing loss. However, due to changes in regulations, particularly the FDA's announcement that it would create an OTC category for hearing aids in the US, the process of accessing the benefits of hearing aids has been dramatically simplified, placing these devices in consumers' hands without them requiring a prescription or a visit to a hearing professional. Tying this increased access and ease of purchasing with significantly lower price points being offered against traditional prescription hearing aids, this category of devices is now becoming accessible by massive populations who would not have otherwise sought treatment.

IoT Hearing Devices Market Size and Share Analysis

The IoT hearing devices market is classified according to products into smart hearing aids, IoT cochlear implants, bone anchored hearing devices, tinnitus maskers, and others. The smart hearing devices segment led the market in 2024 and beyond. Smart hearing devices are the largest product segment because they will meet the complete needs of people with hearing loss, particularly those with a mild to moderate loss, which constitutes the vast majority of hearing losses. Smart hearing aids simply augment hearing health by combining with sophisticated digital sound processing with IoT features – Bluetooth connectivity on smart hearing aids allows audio streaming and hands-free calling, smartphone applications for personal settings, and even AI-driven sound environments. Considering all of the benefits and ease of use it is easy to see how smart hearing aids vastly improve an existing hearing aid process by not only offering better hearing but convenience and connectedness to our routines and lifestyles. Their non-invasive continued technological advancements in miniaturization and development in the over-the-counter (OTC) market offer more selection and a barrier to finding and using a hearing aid accessible.

By technology, the market is segmented into Wi-Fi, Bluetooth, and others. The Bluetooth segment held the largest share of the market in 2024. Bluetooth, notably Bluetooth Low Energy (BLE) is the leading technology in IoT hearing devices for its most optimal utilization of low energy usage, short-range wireless communication, and compatibility with all of the other connected personal devices. For small devices that use small batteries like hearing aids and are designed to work all day and need constant charging BLE range is critical to maximizing battery life. BLE also allows users to connect directly to their personal smart devices like smartphones, tablets, and smart TVs.

In terms of applications, the market is segmented into hearing loss treatment, audio streaming, tinnitus therapy, and others. The hearing loss treatment segment had the largest market share in 2024. Hearing loss treatment is the primary and biggest application segment for IoT hearing devices because their central purpose is to compensate for hearing loss and enhance auditory performance. All other applications, including audio streaming and tinnitus treatment, are merely supporting features of this main purpose. The number of people globally with hearing loss is growing rapidly from aging and noise, so the majority of people who buy them to hear and understand speech better in all environments. The IoT features can help with that treatment, personalization, and usability, but their purpose is still to manage hearing loss.

By end user, the market is segmented into ENT hospitals, audiology clinics, and others. The audiology clinics segment held the largest share of the market in 2024. Audiology clinics continue to have the largest end-user market for IoT hearing devices. Hearing healthcare is specialized and personalized, and while other over-the-counter options are available, the service and expertise available from audiologists in audiology clinics is invaluable for the accurate identification of a hearing loss, selection, fitting, and programming of complex IoT hearing aids to individual needs and the process of rehabilitation and providing support. In audiology clinics, the initial evaluation, making custom molds (for some styles), and programing of complex digital features and settings.

IoT Hearing Devices Market Report Highlights| Report Attribute | Details |

| Market size in 2024 | US$ 6,443.1 Million |

| Market Size by 2033 | US$ 22,871.0 Million |

| Global CAGR (2025 - 2033) | 15.12% |

| Historical Data | 2022-2023 |

| Forecast period | 2025-2033 |

| Segments Covered |

By Product

|

|

Regions and Countries Covered

|

|

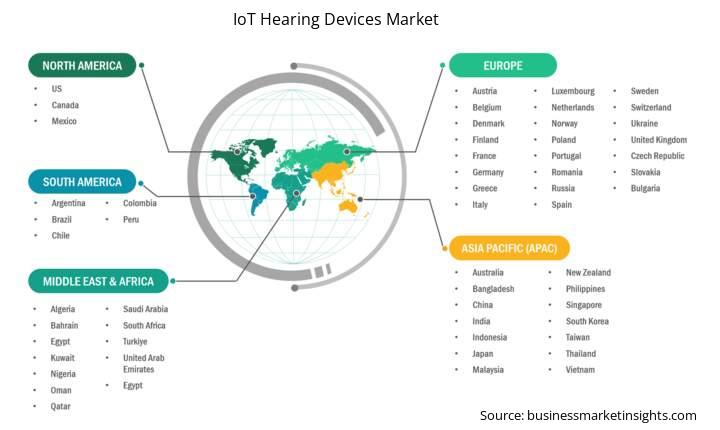

| North America | US, Canada, Mexico |

| Europe | Germany, Italy, France, U.K., Spain, Belgium, Netherlands, Luxembourg, Norway, Finland, Denmark, Sweden, Switzerland, Austria, Greece, Portugal, Russia, Poland, Romania, Czech Republic, Ukraine, Slovakia, Bulgaria |

| Asia-Pacific | China, Japan, South Korea, India, Australia, New Zealand, Indonesia, Malaysia, Philippines, Singapore, Thailand, Vietnam, Taiwan, Bangladesh |

| South and Central America | Brazil, Argentina, Chile, Colombia, Peru |

| Middle East and Africa | Saudi Arabia, United Arab Emirates, Kuwait, Bahrain, Qatar, Oman, Turkiye, South Africa, Egypt, Nigeria, Algeria |

| Market leaders and key company profiles |

|

IoT Hearing Devices Market Report Coverage and Deliverables

The "IoT Hearing Devices Market Size and Forecast (2022–2033)" report provides a detailed analysis of the market covering below areas:

- IoT hearing devices market size and forecast at global, regional, and country levels for all the key market segments covered under the scope

- IoT hearing devices market trends, as well as market dynamics such as drivers, restraints, and key opportunities

- Detailed SWOT analysis

- IoT hearing devices market analysis covering key market trends, global and regional framework, major players, regulations, and recent market developments

- Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments for the IoT Hearing Devices market

- Detailed company profiles

The geographical scope of the IoT hearing devices market report is divided into five regions: North America, Asia Pacific, Europe, Middle East & Africa, and South & Central America. The IoT Hearing Devices market in Asia Pacific is expected to grow significantly during the forecast period.

Asia Pacific IoT hearing devices market includes China, Japan, India, South Korea, Australia, Bangladesh, New Zealand, Philippines, Singapore, Indonesia, Taiwan, Malaysia, Vietnam, and the rest of Asia Pacific. The Asia Pacific region is witnessing the highest growth in the IoT hearing devices market due to a unique combination of demographic shifts, a growing burden of disease, and considerable improvements in healthcare technology infrastructure and technology adoption.

Within APAC region, specific countries are taking the lead in this pace of growth. China is recognized as the most influential player in this market driven by its huge population, growing chronic disease burden, and government-led push to improve access to healthcare and the quality of healthcare services -- while also emphasizing greater focus on home healthcare. In addition, strong R&D and growing focus on digital health innovation will continue to drive adoption of smart hearing devices. India is also a rapidly expanding market, with a vast pool of chronic condition patients, increased awareness, and investment in improvements to medical infrastructure. The growing number of surgical procedures and a significant shift to treating chronic patients in their homes are major drivers of the demand for IoT hearing devices in India. Japan, although a mature market, is continuing to see solid growth in the market for IoT hearing devices, especially for insulin pumps, in response to the high ages population and others driving the demand.

IoT Hearing Devices Market Research Report Guidance

- The report includes qualitative and quantitative data in the IoT Hearing Devices market across product, technology, application, and end user, and geography.

- The report starts with the key takeaways (chapter 2), highlighting the key trends and outlook of the IoT hearing devices market.

- Chapter 3 includes the research methodology of the study.

- Chapter 4 further includes ecosystem analysis along with PEST analysis.

- Chapter 5 highlights the major industry dynamics in the IoT hearing devices market, including factors that are driving the market, prevailing deterrents, potential opportunities and future trends. Impact analysis of these drivers and restraints is also covered in this section.

- Chapter 6 discusses the IoT hearing devices market scenario, in terms of historical market revenues, and forecast till the year 2033.

- Chapters 7 to 10 cover IoT hearing devices market segments by product, technology, application, end user, and geography across North America, Europe, APAC, Middle East and Africa, South and Central America. They cover the market volume revenue forecast and factors driving the market.

- Chapter 11 describes the competitive analysis along with the heat map analysis for the key players operating in the market.

- Chapter 12 describes the industry landscape analysis. It provides detailed descriptions of various business activities such as market initiatives, new developments, mergers, and joint ventures globally, along with a competitive landscape.

- Chapter 13 provides a detailed profile of the major companies operating in the IoT Hearing Devices market. Companies have been profiled on the basis of their key facts, business description, products and services, financial overview, SWOT analysis, and key developments.

- Chapter 14, i.e., the appendix, is inclusive of a brief overview of the company, list of abbreviations, and disclaimer section.

IoT Hearing Devices Market News and Key Development:

The IoT hearing devices market is evaluated by gathering qualitative and quantitative data post primary and secondary research, which includes important corporate publications, association data, and databases. A few of the key developments in the IoT Hearing Devices market are:

- Cochlear Ltd. launched the Nucleus Nexa System, a new cochlear implant that supports firmware updates directly to the implant itself, akin to a smartphone. This groundbreaking feature, enabled by a new chip called NEXOS, allows users to receive new features and advancements throughout their lifetime without needing hardware upgrades. The Nexa system is also designed to be ready for Bluetooth LE Audio and Auracast broadcast support, marking a significant leap in the IoT capabilities for implantable hearing solutions. (Source: Cochlear Ltd., Company Website, June 2025)

- Demant signed an agreement to acquire KIND Group, one of the world's leading retailers of hearing aids with around 650 hearing care clinics. This represents Demant's largest-ever acquisition and will significantly expand its global Hearing Care business to over 4,500 clinics worldwide. This strategic move strengthens Demant's distribution network and market presence for its IoT-enabled hearing devices, reaching more end-users directly. (Source: Demant A/S, Press Release, June 2025)

Key Sources Referred:

- World Health Organization (WHO)

- The World Bank Group

- Eurostat

- United Nations Department of Economic and Social Affairs

- National Council of Aging (NCOA)

- Worldometer

- Health America

- International Bar Association

- International Trade Administration