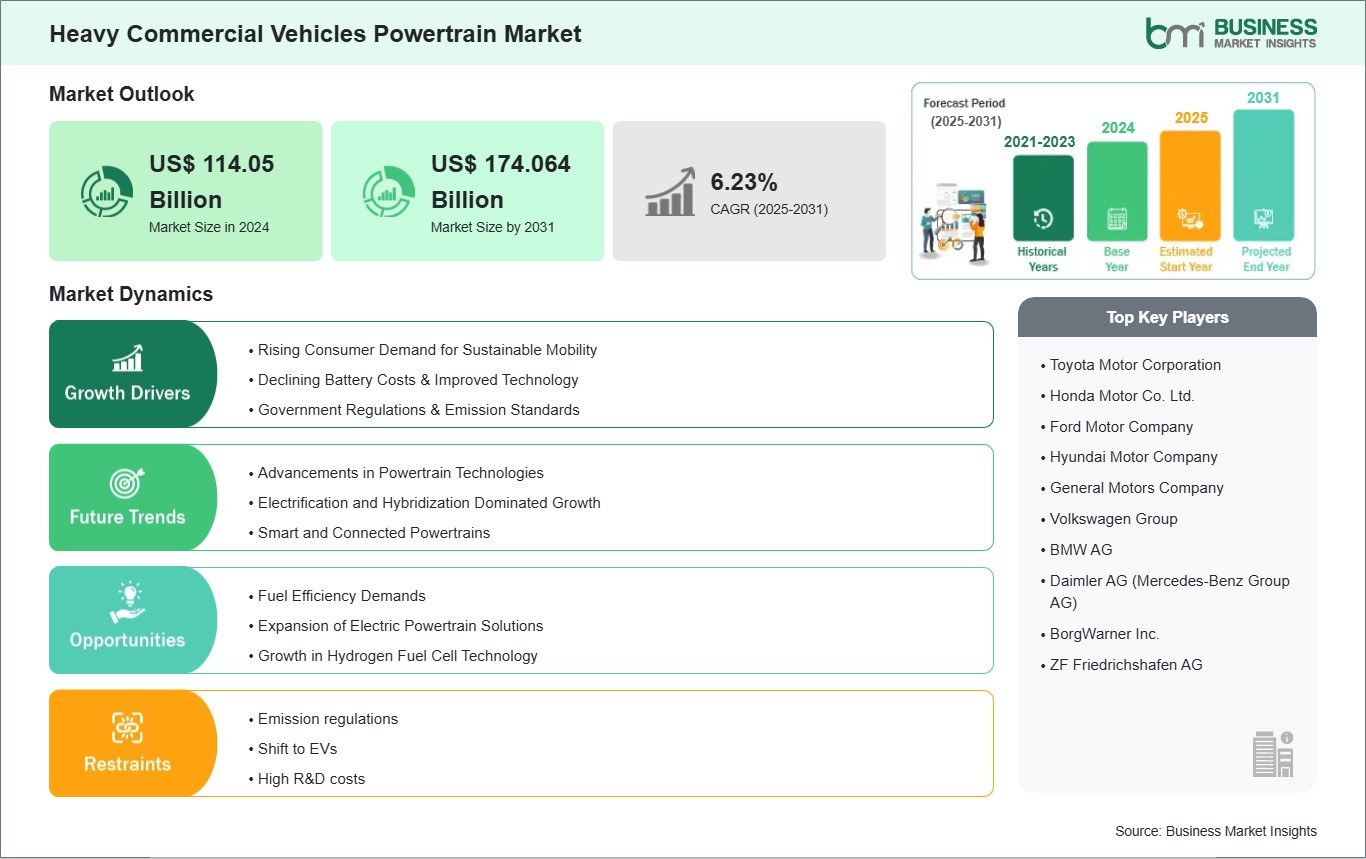

The Heavy Commercial Vehicles Powertrain Market size is expected to reach US$ 174.064 Billion by 2031 from US$ 114.05 Billion in 2024. The market is estimated to record a CAGR of 6.23% from 2025 to 2031.

Executive Summary and Global Market Analysis:

The global Heavy Commercial Vehicle (HCV) powertrain market is undergoing a profound transformation, shifting from traditional internal combustion engine (ICE) dominance towards a future increasingly shaped by electrification and alternative fuels.

This evolution is primarily driven by stringent global emission regulations, the imperative for improved fuel efficiency, the booming e-commerce and logistics sectors, significant infrastructure development, and continuous technological advancements. The market is highly competitive, with major OEMs investing heavily in R&D for cleaner, more efficient powertrains, and the aftermarket playing a crucial role in maintaining the existing fleet.

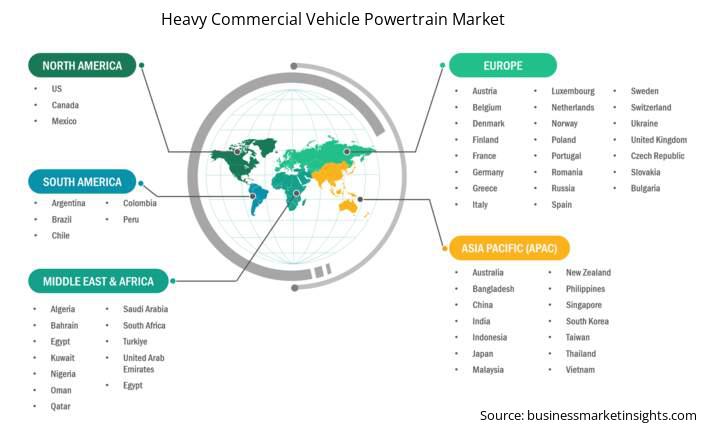

Asia Pacific stands as the leading region in the global Heavy commercial vehicle (HCV) powertrain market, expected to maintain its top position in market share. Its dynamics are shaped by a unique blend of robust economic growth, massive infrastructure development, a booming e-commerce sector, and increasingly aggressive environmental regulations.

Europe stands as a mature yet highly dynamic region in the Heavy Commercial Vehicle (HCV) powertrain market, characterized by stringent environmental regulations.

North America represents a critical and evolving market for Heavy Commercial Vehicle (HCV) powertrains, characterized by a unique blend of strong demand for heavy-duty trucks (especially pickups and Class 8), a robust existing diesel fleet, and an accelerating transition towards electrification and alternative fuels.

Heavy Commercial Vehicles Powertrain Market Strategic Insights

Get more information on this report

Heavy Commercial Vehicles Powertrain Market Segmentation Analysis

Key segments that contributed to the derivation of the Heavy Commercial Vehicle Powertrain market analysis are drive type, propulsion, sales channel, and geography.

By drive type, the Heavy Commercial Vehicle Powertrain market is segmented into Front-Wheel Drive, Rear-Wheel Drive, All-Wheel Drive. The Rear-Wheel Drive segment dominated the market in 2024.

By propulsion type, the Heavy Commercial Vehicle Powertrain market is segmented into ICE, Electric. ICE segment dominated the market in 2024.

By sales channel, the Heavy Commercial Vehicle Powertrain market is segmented into OEM, and Aftermarket.

By geography, the Heavy Commercial Vehicle Powertrain market is segmented into. APAC region dominated the market in 2024.

Heavy Commercial Vehicle Powertrain Market Drivers and Opportunities:

Stringent Emission Regulations

Governments worldwide are implementing stricter emission standards (e.g., Euro 7, CARB regulations) to combat air pollution and climate change, forcing manufacturers to innovate cleaner powertrain technologies.

Fuel Efficiency Demands

Escalating fuel costs necessitate more fuel-efficient powertrains, driving the adoption of advanced ICE technologies (turbocharging, direct injection) and the shift towards electric and hybrid solutions.

Heavy Commercial Vehicle Powertrain Market Size and Share Analysis

By drive type, Front-Wheel Drive (FWD), Rear-Wheel Drive (RWD), and All-Wheel Drive (AWD) – RWD is the most prevalent and dominant drive type in the heavy commercial vehicle market. This configuration is standard for most heavy trucks, buses, and other large commercial vehicles. With weight transferring to the rear during acceleration, RWD provides excellent traction for getting a heavy load moving efficiently.

By propulsion type, ICE holds the largest market share in HCVs (approximately 80% automotive powertrain market in 2024), primarily diesel. This dominance is due to proven reliability, extensive fuelling infrastructure, and established performance for heavy loads and long distances. However, its share is declining due to emission regulations and the push for electrification. Battey Electric Vehicles (BEV) are expected to become the fastest-growing segment in HCVs. Driven by zero tailpipe emissions, lower operating costs (fuel and maintenance), and government incentives. Ideal for short-haul and urban delivery applications. Significant OEM investment is observed (e.g., Daimler Truck's new heavy-duty electric truck with a modular electric powertrain).

By sales channel, OEMs dominate the HCV powertrain market, representing the sale of completely new vehicles with integrated powertrains. OEMs are at the forefront of investing in and integrating advanced technologies, especially in electrification, to meet regulations and customer demands. This segment held the Lion’s share in the overall automotive powertrain market value in 2024. The growth of the aftermarket is linked to the size and age of the existing HCV fleet. Electrification is creating new opportunities in the aftermarket for specialized EV powertrain parts, diagnostics, and battery repair/replacement services.

By geography, Asia Pacific is the largest and most dominant region in the global HCV market, and the leader in electric Commercial Vehicle adoption, driven by rapid industrialization, urbanization, e-commerce boom, and strong government support for EVs (especially China & India).

Heavy Commercial Vehicles Powertrain Market Report Highlights

China, Japan, South Korea, India, Australia, New Zealand, Indonesia, Malaysia, Philippines, Singapore, Thailand, Vietnam, Taiwan, Bangladesh

South and Central America

Brazil, Argentina, Chile, Colombia, Peru

Middle East and Africa

Saudi Arabia, United Arab Emirates, Kuwait, Bahrain, Qatar, Oman, Turkiye, South Africa, Egypt, Nigeria, Algeria

Market leaders and key company profiles

Toyota Motor Corporation

Honda Motor Co. Ltd.

Ford Motor Company

Hyundai Motor Company

General Motors Company

Volkswagen Group

BMW AG

Daimler AG (Mercedes-Benz Group AG)

BorgWarner Inc.

ZF Friedrichshafen AG

Get more information on this report

Heavy Commercial Vehicles Powertrain Market Report Coverage and Deliverables

The "Heavy Commercial Vehicle Powertrain Market Outlook (2021–2031)" report provides a detailed analysis of the market covering below areas:

Heavy Commercial Vehicle Powertrain market size and forecast at global, regional, and country levels for all the key market segments covered under the scope.

Heavy Commercial Vehicle Powertrain market trends, as well as market dynamics such as drivers, restraints, and key opportunities

Detailed Porter's Five Forces and SWOT analysis.

Heavy Commercial Vehicle Powertrain market analysis covering key market trends, global and regional framework, major players, regulations, and recent market developments.

Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments for the Heavy Commercial Vehicle Powertrain market.

Detailed company profiles

Heavy Commercial Vehicles Powertrain Market Country and Regional Insights

Get more information on this report

The geographical coverage of the Heavy Commercial Vehicle Powertrain market report is divided into five regions: North America, Asia Pacific, Europe, Middle East & Africa, and South & Central America. The Heavy Commercial Vehicle Powertrain market in Asia Pacific is expected to grow significantly during the forecast period.

The Heavy Commercial Vehicle (LCV) powertrain market displays significant regional disparities driven by unique economic, regulatory, and logistical factors. The Asia-Pacific (APAC) region is the clear frontrunner in the global Heavy Commercial Vehicle (HCV) market and plays a significant role in advancing HCV powertrain technologies. This leadership is driven by a combination of strong economic expansion, extensive infrastructure projects, rapid growth in e-commerce, and increasingly stringent environmental regulations.

Europe represents a mature yet highly dynamic market for Heavy Commercial Vehicle (HCV) powertrains, distinguished by rigorous environmental standards, a strong commitment to decarbonization, and substantial public and private investment in zero-emission transportation solutions. Europe has some of the world's most aggressive emission standards. The Euro 7 regulation, agreed upon in 2024 and coming into force for new HCV models by May 29, 2028 (and for all new registrations by May 29, 2029), is a major driver.

North America is a vital and rapidly evolving market for Heavy Commercial Vehicle (HCV) powertrains, marked by strong demand for heavy-duty trucks—particularly pickups and Class 8 vehicles—a substantial existing diesel fleet, and a swift shift toward electrification and alternative fuel solutions.

Meanwhile, South and Central America, and Middle East & Africa (MEA) present diverse heavy commercial vehicle (HCV) powertrain markets, each with unique growth drivers, challenges, and evolving technology adoption patterns. The South and Central American commercial vehicle market, including HCVs, is experiencing growth driven by infrastructure investment, mining development and exports, multimodal transportation projects, and expansion of e-commerce. The MEA commercial vehicles market is driven by increasing demand across industries such as logistics, construction, waste management, and petrochemicals. Heavy-duty commercial vehicles are gaining prominence due to rising investments in large-scale infrastructure projects.

Heavy Commercial Vehicle Powertrain Market Research Report Guidance

The report includes qualitative and quantitative data in the Heavy Commercial Vehicle Powertrain market across drive type, propulsion, sales channel, and geography.

The report starts with the key takeaways (chapter 2), highlighting the key trends and outlook of the Heavy Commercial Vehicle Powertrain market.

Chapter 3 includes the research methodology of the study.

Chapter 4 further includes ecosystem analysis along with Porter’s analysis.

Chapter 5 highlights the major industry dynamics in the Heavy Commercial Vehicle Powertrain market, including factors that are driving the market, prevailing deterrents, potential opportunities as well as future trends. Impact analysis of these drivers and restraints is covered in this section.

Chapter 6 discusses the Heavy Commercial Vehicle Powertrain market scenario, in terms of historical market revenues, and forecast till the year 2031.

Chapters 7 to 9 cover Heavy Commercial Vehicle Powertrain market segments by product type, portability, technology, application, end user and geography across North America, Europe, Asia Pacific, Middle East and Africa, and South and Central America. They cover market revenue forecast and factors driving the market.

Chapter 10 describes the competitive analysis along with the heat map analysis for the key players operating in the market.

Chapter 11 describes the industry landscape analysis. It provides detailed description of business activities such as market initiatives, new developments, mergers, and joint ventures globally, along with a competitive landscape.

Chapter 12 provides detailed profiles of the major companies operating in the Heavy Commercial Vehicle Powertrain market. The companies have been profiled on the basis of their key facts, business descriptions, products and services, financial overview, SWOT analysis, and key developments.

Chapter 13, i.e., the appendix is inclusive of a brief overview of the company, list of abbreviations, and disclaimer.

Heavy Commercial Vehicle Powertrain Market News and Key Development:

The Heavy Commercial Vehicle Powertrain market is evaluated by gathering qualitative and quantitative data post primary and secondary research, which includes important corporate publications, association data, and databases. A few of the key developments in the Heavy Commercial Vehicle Powertrain market are:

On September 13, 2024, Toyota expanded its European Heavy commercial vehicle lineup with the introduction of the PROACE MAX, marking its debut in the heavy-duty van market. This new addition, alongside the updated PROACE, PROACE CITY, and Hilux, solidifies Toyota's comprehensive "Toyota Professional" portfolio. The electrification of its LCV range underscores Toyota's multi-path technology strategy for achieving carbon neutrality, emphasizing its belief in providing diverse, affordable, and practical options to rapidly reduce CO2 emissions and facilitate a transition to zero-emission mobility.

In June 2024, Powertrain solutions provider Horse and WEG, a manufacturer of electric motors, have announced an R&D partnership to develop Range Extender technology for Heavy commercial and heavy-duty vehicles. The Range Extender powertrain will be developed jointly, with WEG supplying critical components such as electric generators, e-motors, electrical inverters, and battery packs.

Key Sources Referred:

The World Bank

International Council on Clean Transportation

United States Department of Transportation

International Organization of Motor Vehicle Manufacturers

European Automobile Manufacturers’ Association (ACEA)

Trade Databases and Paid Data Providers

Government and Regulatory Publications

Company Reports and Annual Filings

The List of Companies - Heavy Commercial Vehicles Powertrain Market

Toyota Motor Corporation Honda Motor Co. Ltd., Ford Motor Company Hyundai Motor Company General Motors Company Volkswagen Group BMW AG Daimler AG (Mercedes-Benz Group AG) BorgWarner Inc. ZF Friedrichshafen AG

Frequently Asked Questions

How big is the Heavy Commercial Vehicles Powertrain Market?

The Heavy Commercial Vehicles Powertrain Market is valued at US$ 114.05 Billion in 2024, it is projected to reach US$ 174.064 Billion by 2031.

What is the CAGR for Heavy Commercial Vehicles Powertrain Market by (2025 - 2031)?

As per our report Heavy Commercial Vehicles Powertrain Market, the market size is valued at US$ 114.05 Billion in 2024, projecting it to reach US$ 174.064 Billion by 2031. This translates to a CAGR of approximately 6.23% during the forecast period.

What segments are covered in this report?

The Heavy Commercial Vehicles Powertrain Market report typically cover these key segments-

Drive Type (Front-Wheel Drive, Rear-Wheel Drive, All-Wheel Drive)

Propulsion Type (ICE, Electric)

Sales Channel (OEM, Aftermarket)

What is the historic period, base year, and forecast period taken for Heavy Commercial Vehicles Powertrain Market?

The historic period, base year, and forecast period can vary slightly depending on the specific market research report. However, for the Heavy Commercial Vehicles Powertrain Market report:

Historic Period : 2021-2023

Base Year : 2024

Forecast Period : 2025-2031

Who are the major players in Heavy Commercial Vehicles Powertrain Market?

The Heavy Commercial Vehicles Powertrain Market is populated by several key players, each contributing to its growth and innovation. Some of the major players include:

Toyota Motor Corporation

Honda Motor Co. Ltd.,

Ford Motor Company

Hyundai Motor Company

General Motors Company

Volkswagen Group

BMW AG

Daimler AG (Mercedes-Benz Group AG)

BorgWarner Inc.

ZF Friedrichshafen AG

Who should buy this report?

The Heavy Commercial Vehicles Powertrain Market report is valuable for diverse stakeholders, including:

Investors: Provides insights for investment decisions pertaining to market growth, companies, or industry insights. Helps assess market attractiveness and potential returns.

Industry Players: Offers competitive intelligence, market sizing, and trend analysis to inform strategic planning, product development, and sales strategies.

Suppliers and Manufacturers: Helps understand market demand for components, materials, and services related to concerned industry.

Researchers and Consultants: Provides data and analysis for academic research, consulting projects, and market studies.

Financial Institutions: Helps assess risks and opportunities associated with financing or investing in the concerned market.

Essentially, anyone involved in or considering involvement in the Heavy Commercial Vehicles Powertrain Market value chain can benefit from the information contained in a comprehensive market report.

Get Free Sample For Heavy Commercial Vehicles Powertrain Market

Get Free Sample For Heavy Commercial Vehicles Powertrain Market