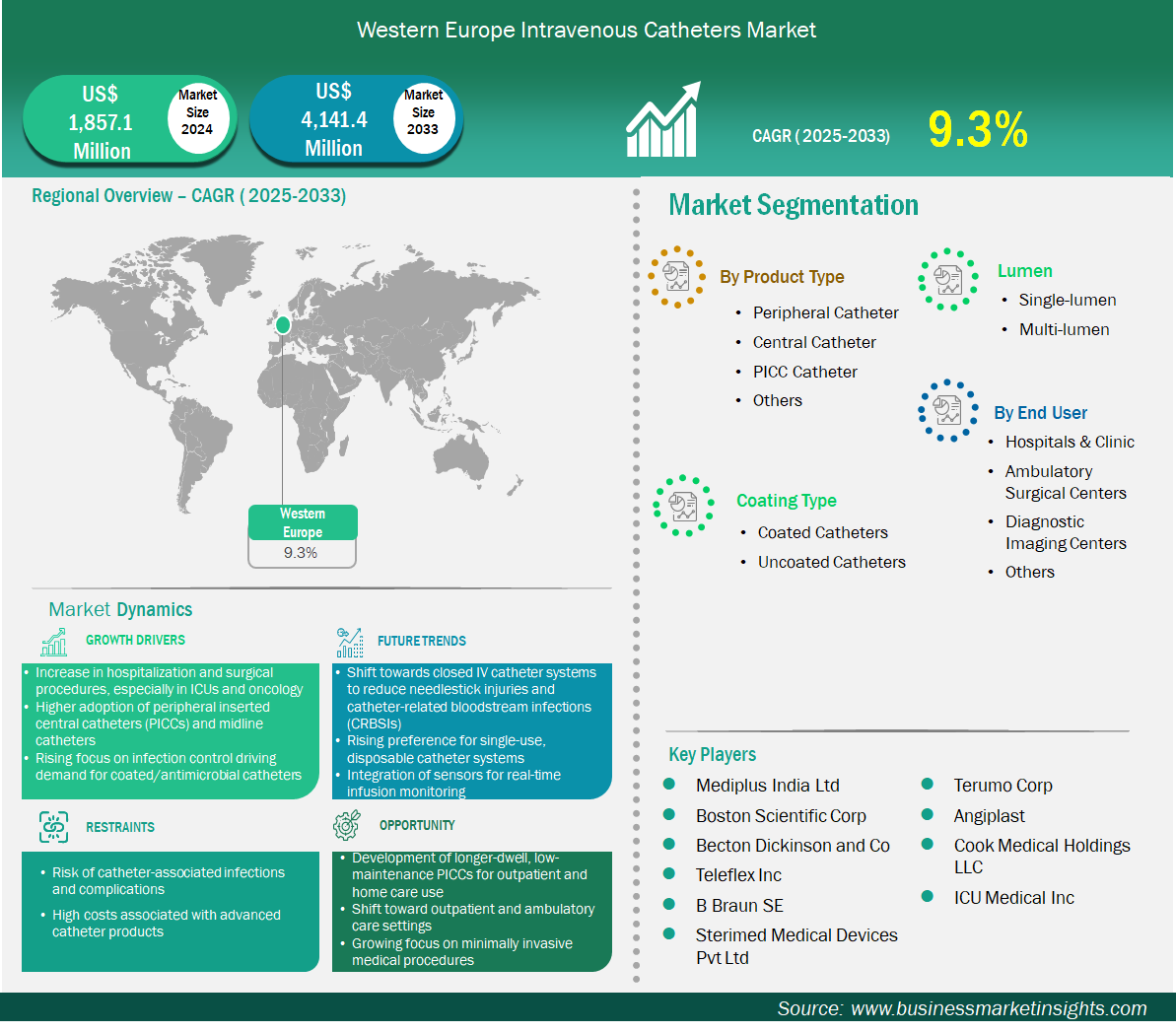

The Western Europe intravenous catheters market size is expected to reach US$ 4,141.4 million by 2033 from US$ 1,857.1 million in 2024. The market is estimated to record a CAGR of 9.3% from 2025 to 2033.

Executive Summary and Western Europe Intravenous Catheters Market Analysis:

The intravenous catheters market in Western Europe is experiencing significant growth driven by the increase in hospitalization and surgical procedures; especially in ICUs and oncology, higher adoption of peripherally inserted central catheters (PICCs) and midline catheters, and rising focus on infection control driving demand for coated/antimicrobial catheters. Western Europe—Germany, France, UK, Italy, Spain, Austria, Switzerland, Portugal—combines scale, regulatory rigor, and outcome-driven procurement. Peripheral catheters dominate routine admissions and perioperative care, guided by nurse-led cannulation protocols and pathway standardization that reduce insertion attempts and failure. Coated catheters expand under MDR scrutiny and hospital quality charters targeting CRBSI; antimicrobial and hydrophilic options gain traction in teaching hospitals and high-volume medical wards. Multi-lumen devices are concentrated in university hospitals and tertiary ICUs, enabling concurrent chemo, TPN, and vasoactive therapy with strict lumen management. Hospitals and integrated clinics remain the primary end-users, with outpatient infusion centers embedded in public systems and private providers. Procurement is sophisticated: value analysis committees require published evidence, real-world audits, and training commitments; awards increasingly factor implementation support and supply resilience. Distribution networks are robust, with pan-European contracts supplemented by regional service teams. Market dynamics reward portfolios that balance peripheral reliability, coated performance for extended dwell, and multi-lumen precision for complex protocols. Sustainability, staff ergonomics, and digital traceability are ascending selection criteria. Country variance is notable—Germany’s breadth of hospitals drives volume and innovation pilots; France emphasizes accessibility and infection metrics; the UK’s NHS frameworks standardize adoption while controlling cost. Overall, Western Europe is a mature, quality-centric market that shifts share through validated clinical gains, workforce productivity, and dependable logistics rather than aggressive pricing alone.

Western Europe Intravenous Catheters Market Segmentation Analysis:

Key segments that contributed to the derivation of the intravenous catheters market analysis are product, coating type, lumen, and end user.

- By product, the intravenous catheters market is segmented into peripheral catheter, central catheter, PICC catheter, and others. Peripheral catheter dominated the market in 2024, driven by the standardized perioperative pathways and high ED throughput.

- By coating type, the intravenous catheters market is segmented into coated catheters, uncoated catheters. Coated catheters dominated the market in 2024, driven by MDR-driven biocompatibility and infection performance requirements.

- By lumen, the market is segmented into single-lumen, multi-lumen. Multi-lumen dominated the market in 2024, driven by the tertiary oncology and ICU protocol intensity.

- By end user, the market is segmented into hospitals & clinics, ambulatory surgical centers, diagnostic imaging centers, and others. Hospitals & clinics dominated the market in 2024, driven by robust public financing and matured outpatient infusion networks.

Western Europe Intravenous Catheters Market Outlook

The Western Europe intravenous catheters market is segmented into Belgium, the Netherlands, Luxembourg, Germany, France, Italy, Spain, Switzerland, Sweden, Austria, the United Kingdom, Denmark, Portugal, Norway, and Finland. Growth in Western Europe will be powered by oncology pipeline density, outpatient care expansion, and stricter infection mandates. Peripheral catheters will remain the bedrock, but demand will skew toward vein-sparing materials, securement systems, and designs that cut reinsertion rates. Coated catheters will accelerate under MDR-aligned procurement and hospital targets; outcome-linked contracts and post-market surveillance data will influence renewals. Multi-lumen adoption will rise with ICU modernization and complex chemo regimens; comprehensive kits, standard accessories, and streamlined maintenance protocols offer differentiation. Supply assurance—European warehousing, dual-sourcing, and service SLAs—will be decisive after recent disruption learnings. Workforce realities push devices that reduce workload: intuitive insertion aids, fewer maintenance steps, and securement solutions that prevent accidental dislodgement. Sustainability is now embedded in tenders—packaging reductions, recyclability, and emissions transparency can swing decisions. Digital integration—barcode tracking, EMR line records, and adverse event dashboards—enables outcome-linked purchasing and continuous improvement. Strategic edge depends on evidence-backed infection reductions, training fidelity, and resilient logistics. Expect steady, quality-driven growth with coated and multi-lumen segments gaining share while peripheral usage remains structurally high.

Western Europe Intravenous Catheters Market Country Insights

Based on region, the Western Europe intravenous catheters market is further segmented into Belgium, the Netherlands, Luxembourg, Germany, France, Italy, Spain, Switzerland, Sweden, Austria, the United Kingdom, Denmark, Portugal, Norway, and Finland. Germany held the largest share in 2024.

Germany’s expansive hospital base and university centers lead pilot-driven adoption of coated and multi-lumen devices; procurement emphasizes evidence and implementation support. France balances national accessibility with infection targets, expanding coated usage in public systems while outpatient infusions sustain peripheral demand. The UK’s NHS frameworks standardize portfolios and pricing, rewarding vendors with training programs and supply dependability; multi-lumen use is concentrated in tertiary trusts. Italy’s regionalized governance supports oncology and ICU investments, boosting multi-lumen demand in teaching hospitals; peripheral devices dominate short-stay pathways. Spain’s regional health services invest in catheter-related infection reduction, favouring coated lines, while robust ED volumes sustain peripheral throughput. Switzerland and Austria prioritize premium devices and sustainability criteria, with precise documentation and service expectations; Portugal scales coated adoption tied to accreditation efforts. Cross-country success depends on aligning with procurement norms, sustainability charters, and clinical outcome tracking. Vendors that offer audit-ready data, reliable replenishment, and tailored education secure durable contracts. Diverse reimbursement and governance models require calibrated strategies—volume-oriented peripheral ranges for high-throughput wards, coated offerings for infection goals, and multi-lumen SKUs for concentrated tertiary care.

Western Europe Intravenous Catheters Market Company Profiles

Mediplus India Ltd, Boston Scientific Corp, Becton Dickinson and Co, Teleflex Inc, B Braun SE, Sterimed Medical Devices Pvt Ltd, Terumo Corp, Angiplast, Cook Medical Holdings LLC, ICU Medical Inc, are among the key players operating in the market. These players adopt strategies such as expansion, product innovation, and mergers and acquisitions to stay competitive in the market and offer innovative products to their consumers.

Western Europe Intravenous Catheters Market Research Methodology:

The following methodology has been followed for the collection and analysis of data presented in this report:

-

Secondary Research

The research process begins with comprehensive secondary research, utilizing both internal and external sources to gather qualitative and quantitative data for each market. Commonly referenced secondary research sources include, but are not limited to:

- Company websites, annual reports, financial statements, broker analyses, and investor presentations

- Industry trade journals and other relevant publications

- Government documents, statistical databases, and market reports

- News articles, press releases, and webcasts specific to companies operating in the market

Note: All financial data included in the Company Profiles section has been standardized to US$. For companies reporting in other currencies, figures have been converted to US$ using the relevant exchange rates for the corresponding year.

-

Primary Research

Business Market Insights conducts a significant number of primary interviews each year with industry stakeholders and experts to validate and analyze the data and gain valuable insights. These research interviews are designed to:

- Refine findings from secondary research

- Enhance the expertise and market understanding of the analysis team

- Gain insights into market size, trends, growth patterns, competitive dynamics, and future prospects

Primary research is conducted via email interactions and telephone interviews with industry experts across various markets, categories, segments, and sub-segments in different regions. Participants typically include:

- Industry stakeholders: Vice Presidents, business development managers, market intelligence managers, and national sales managers

- External experts: Valuation specialists, research analysts, and key opinion leaders with industry-specific expertise

Key Sources Referred:

- World Health Organization (WHO)

- World Heart Federation (WHF)

- Organisation for Economic Cooperation and Development (OECD)

- The World Bank Group

- Worldometer

- The Lancet

- International Bar Association

- International Trade Administration

- Eurostat

Western Europe Intravenous Catheters Market Strategic Insights

Western Europe Intravenous CathetersMarket Report Highlights

| Report Attribute | Details |

| Market size in 2024 | US$ 1,857.1 Million |

| Market Size by 2033 | US$ 515.0 Million |

| CAGR (2025 - 2033) | 9.3% |

| Historical Data | 2022-2023 |

| Forecast period | 2025-2033 |

| Segments Covered |

By Product

|

|

Regions and Countries Covered

|

|

| Western Europe | Belgium, Netherlands, Luxembourg, Germany, France, Italy, Spain, Switzerland, Sweden, Austria, United Kingdom, Denmark, Portugal, Norway, Finland |

| Market leaders and key company profiles |

|

Western Europe Intravenous Catheters Market Country and Regional Insights