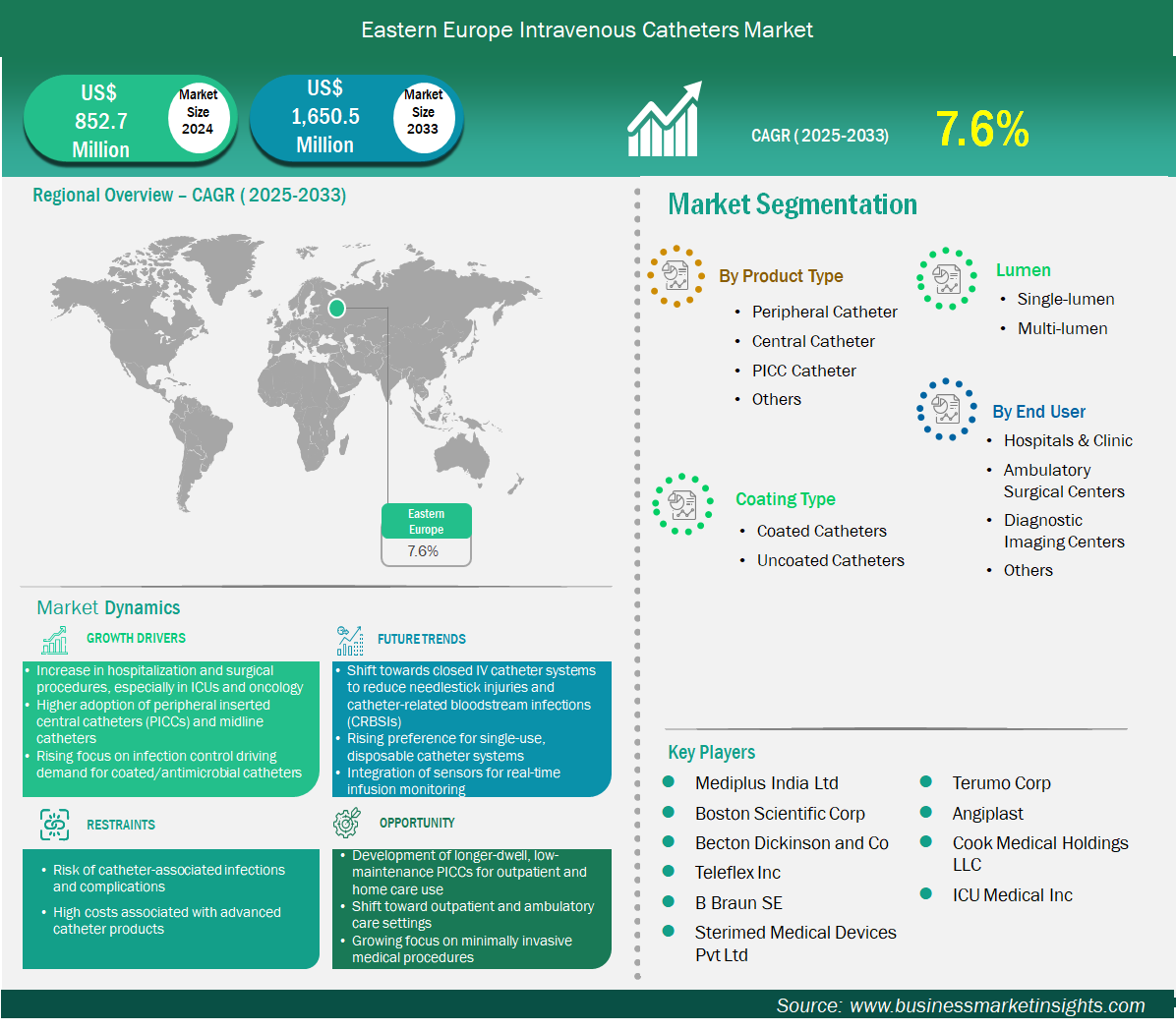

The Eastern Europe intravenous catheters market size is expected to reach US$ 1,650.5 million by 2033 from US$ 852.7 million in 2024. The market is estimated to record a CAGR of 7.6% from 2025 to 2033.

Executive Summary and Eastern Europe Intravenous Catheters Market Analysis:

The intravenous catheters market in Eastern Europe is experiencing significant growth driven by the increase in hospitalization and surgical procedures; especially in ICUs and oncology, higher adoption of peripherally inserted central catheters (PICCs) and midline catheters, and rising focus on infection control driving demand for coated/antimicrobial catheters. Eastern Europe’s intravenous catheter market reflects heterogeneous systems transitioning from legacy practices to modern, outcome-oriented care. Peripheral catheters constitute the foundational device category, supporting high-volume medical wards, surgical units, and emergency departments where swift cannulation and short dwell dominate. Coated catheters are gaining share in urban tertiary hospitals engaged in accreditation cycles and quality incentive schemes; antimicrobial and hydrophilic surfaces are adopted to curb phlebitis and catheter-related bloodstream infections that strain limited ICU capacity. Multi-lumen devices see targeted deployment in oncology hubs and advanced ICUs, aligning with centralization of complex care in capital cities and regional university hospitals. The end-user base is overwhelmingly public, with clinics attached to hospital networks and polyclinics expanding infusion capacity. Procurement is increasingly professionalized: national tenders and hospital consortia emphasize lifecycle cost, training inclusions, and documented performance under local conditions. Distributors remain pivotal, bridging language, regulatory particulars, and last-mile logistics across fragmented geographies. Market access is sensitive to formularies and coding; vendors that tailor submission dossiers, participate in pilot studies, and offer clinician education gain influence in guideline updates. Affordability and reliability trump novelty in many districts, but visible wins on infection rates and nurse workload accelerate coated adoption where budgets allow. Regional variance is marked—EU members align faster with MDR expectations and quality metrics, while non-EU neighbours progress through phased upgrades. Overall, the region values pragmatic devices that reduce complications, sustain throughput, and fit constrained staffing models, rewarding portfolios that combine robust peripheral lines, selectively deployed coatings, and multi-lumen options for consolidated specialty care.

Eastern Europe Intravenous Catheters Market Strategic Insights

Get more information on this report

Eastern Europe Intravenous Catheters Market Segmentation Analysis

Key segments that contributed to the derivation of the intravenous catheters market analysis are product, coating type, lumen, and end user.

By product, the intravenous catheters market is segmented into peripheral catheter, central catheter, PICC catheter, and others. Peripheral catheter dominated the market in 2024, driven by the budget-conscious protocols and high-volume inpatient throughput.

By coating type, the intravenous catheters market is segmented into coated catheters, uncoated catheters. Coated catheters dominated the market in 2024, driven by hospital modernization programs targeting infection indices.

By lumen, the market is segmented into single-lumen, multi-lumen. Multi-lumen dominated the market in 2024, driven by the consolidation of oncology services and ICU capacity expansions.

By end user, the market is segmented into hospitals & clinics, ambulatory surgical centers, diagnostic imaging centers, and others. Hospitals & clinics dominated the market in 2024, driven by public sector dominance and EU-funded facility upgrades.

Eastern Europe Intravenous Catheters Market Outlook

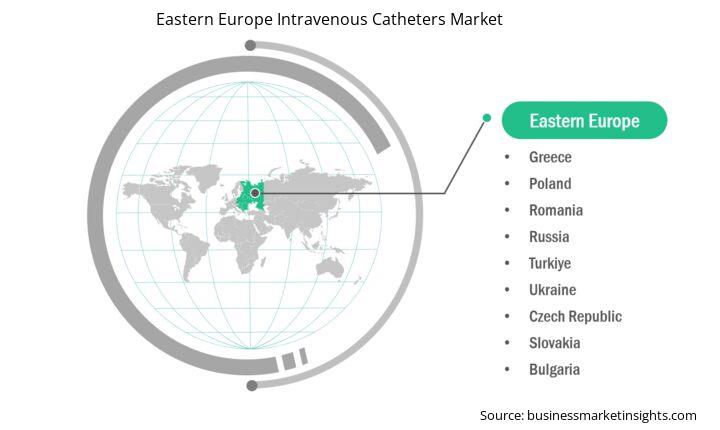

The Eastern Europe intravenous catheters market is segmented into Russia, Poland, Ukraine, Romania, the Czech Republic, Slovakia, Bulgaria, and Greece. Eastern Europe’s trajectory will be steered by EU cohesion funding, hospital consolidation, and workforce optimization. Peripheral catheter demand will remain resilient as hospitals tackle bed flow pressures and shrink average length of stay, favouring easy-insertion, vein-friendly designs that reduce failure and repeat cannulation. Coated catheters will expand with MDR-aligned procurement and infection control mandates—expect bundled tenders that link price to verified reductions in CRBSI and phlebitis, plus vendor-supported audits. Multi-lumen use will rise in oncology and critical care as treatment protocols intensify and referral pathways concentrate complex cases; devices with dependable lumen separation and simplified maintenance will gain preference. Supply chain resilience is becoming a board-level topic—institutions will favour regional warehousing, guaranteed replenishment windows, and dual-distributor frameworks to mitigate transport and customs delays. Training remains a growth lever: simulation-driven insertion courses and standardized securement practices can unlock coated adoption and reduce complication-related bed days. Digital initiatives—barcode tracking, EMR integration of line data, and adverse event dashboards—will spread from capitals to tier-2 cities, enabling outcome-based purchasing. Price sensitivity endures; vendors must articulate total cost advantages through fewer complications, lower reinsertions, and reduced nurse time. Sustainability criteria will enter tender scoring in EU members, encouraging lighter packaging and recyclability. Strategic success depends on blending affordability with measurable clinical gains, local service presence, and policy fluency—aligning bids with national cancer plans, infection targets, and workforce strategies. Expect steady growth, rooted in modernization projects and quality-driven procurement that elevates coated and multi-lumen segments without displacing peripheral mainstays.

Eastern Europe Intravenous Catheters Market Country Insights

Based on region, the Eastern Europe intravenous catheters market is further segmented into Russia, Poland, Ukraine, Romania, the Czech Republic, Slovakia, Bulgaria, and Greece. Russia held the largest share in 2024.

Russia’s large public hospital networks and oncology centers drive structured demand: peripheral lines dominate ward-level use, while coated devices gain traction in teaching hospitals pursuing accreditation benchmarks. Romania and Bulgaria prioritize affordability but are piloting coated catheters in capitals to address infection indicators; university hospitals anchor multi-lumen adoption for complex regimens. Czechia and Slovakia showcase tighter MDR alignment and mature procurement committees, valuing vendor education packages and guaranteed supply continuity. Across the region, infusion clinics attached to hospital systems are expanding, but independent private centers remain limited outside major cities. Tender success hinges on local references, clinician champions, and post-award training fidelity. Value narratives that emphasize fewer complications, consistent dwell times, and ergonomic insertion resonate with nurse leaders tasked with throughput under staffing constraints. Policy touchpoints—cancer plans, MDR timelines, and infection reporting—shape portfolio choices; vendors that align with national priorities and provide audit-ready data gain durable contracts. Country diversity necessitates tiered offerings: baseline peripheral ranges for volume wards, coated options for tertiary hubs, and multi-lumen SKUs for oncology and ICU anchors.

Eastern Europe Intravenous Catheters Market Report Highlights

Eastern Europe Intravenous Catheters Market Company Profiles

Mediplus India Ltd, Boston Scientific Corp, Becton Dickinson and Co, Teleflex Inc, B Braun SE, Sterimed Medical Devices Pvt Ltd, Terumo Corp, Angiplast, Cook Medical Holdings LLC, ICU Medical Inc, are among the key players operating in the market. These players adopt strategies such as expansion, product innovation, and mergers and acquisitions to stay competitive in the market and offer innovative products to their consumers.

Eastern Europe Intravenous Catheters Market Research Methodology:

The following methodology has been followed for the collection and analysis of data presented in this report:

Secondary Research

The research process begins with comprehensive secondary research, utilizing both internal and external sources to gather qualitative and quantitative data for each market. Commonly referenced secondary research sources include, but are not limited to:

Company websites, annual reports, financial statements, broker analyses, and investor presentations

Industry trade journals and other relevant publications

Government documents, statistical databases, and market reports

News articles, press releases, and webcasts specific to companies operating in the market

Note: All financial data included in the Company Profiles section has been standardized to US$. For companies reporting in other currencies, figures have been converted to US$ using the relevant exchange rates for the corresponding year.

Primary Research

Business Market Insights conducts a significant number of primary interviews each year with industry stakeholders and experts to validate and analyze the data and gain valuable insights. These research interviews are designed to:

Refine findings from secondary research

Enhance the expertise and market understanding of the analysis team

Gain insights into market size, trends, growth patterns, competitive dynamics, and future prospects

Primary research is conducted via email interactions and telephone interviews with industry experts across various markets, categories, segments, and sub-segments in different regions. Participants typically include:

Industry stakeholders: Vice Presidents, business development managers, market intelligence managers, and national sales managers

External experts: Valuation specialists, research analysts, and key opinion leaders with industry-specific expertise

Eastern Europe Intravenous Catheters Market Country and Regional Insights

Get more information on this report

Eastern Europe Intravenous Catheters Key Sources Referred:

World Health Organization (WHO)

World Heart Federation (WHF)

Organisation for Economic Cooperation and Development (OECD)

The World Bank Group

Worldometer

The Lancet

International Bar Association

International Trade Administration

Eurostat

Identical Market Reports with other Region/Countries

The List of Companies - Eastern Europe Intravenous Catheters Market

Mediplus India Ltd Boston Scientific Corp Becton Dickinson and Co Teleflex Inc B Braun SE Sterimed Medical Devices Pvt Ltd Terumo Corp Angiplast Cook Medical Holdings LLC ICU Medical Inc

Frequently Asked Questions

How big is the Eastern Europe Intravenous Catheters Market?

The Eastern Europe Intravenous Catheters Market is valued at US$ 852.7 Million in 2024, it is projected to reach US$ 1,650.5 Million by 2033.

What is the CAGR for Eastern Europe Intravenous Catheters Market by (2025 - 2033)?

As per our report Eastern Europe Intravenous Catheters Market, the market size is valued at US$ 852.7 Million in 2024, projecting it to reach US$ 1,650.5 Million by 2033. This translates to a CAGR of approximately 7.6% during the forecast period.

What segments are covered in this report?

The Eastern Europe Intravenous Catheters Market report typically cover these key segments-

Product (Peripheral Catheter, Central Catheter, PICC Catheter, Others)

Coating Type (Coated Catheter, Uncoated Catheter)

Lumen (Single-lumen, Multi-lumen)

End User (Hospitals & Clinics, Ambulatory Surgical Centers, Diagnostic Imaging Centers, Others)

What is the historic period, base year, and forecast period taken for Eastern Europe Intravenous Catheters Market?

The historic period, base year, and forecast period can vary slightly depending on the specific market research report. However, for the Eastern Europe Intravenous Catheters Market report:

Historic Period : 2022-2023

Base Year : 2024

Forecast Period : 2025-2033

Who are the major players in Eastern Europe Intravenous Catheters Market?

The Eastern Europe Intravenous Catheters Market is populated by several key players, each contributing to its growth and innovation. Some of the major players include:

Mediplus India Ltd

Boston Scientific Corp

Becton Dickinson and Co

Teleflex Inc

B Braun SE

Sterimed Medical Devices Pvt Ltd

Terumo Corp

Angiplast

Cook Medical Holdings LLC

ICU Medical Inc

Who should buy this report?

The Eastern Europe Intravenous Catheters Market report is valuable for diverse stakeholders, including:

Investors: Provides insights for investment decisions pertaining to market growth, companies, or industry insights. Helps assess market attractiveness and potential returns.

Industry Players: Offers competitive intelligence, market sizing, and trend analysis to inform strategic planning, product development, and sales strategies.

Suppliers and Manufacturers: Helps understand market demand for components, materials, and services related to concerned industry.

Researchers and Consultants: Provides data and analysis for academic research, consulting projects, and market studies.

Financial Institutions: Helps assess risks and opportunities associated with financing or investing in the concerned market.

Essentially, anyone involved in or considering involvement in the Eastern Europe Intravenous Catheters Market value chain can benefit from the information contained in a comprehensive market report.

Get Free Sample For Eastern Europe Intravenous Catheters Market

Get Free Sample For Eastern Europe Intravenous Catheters Market