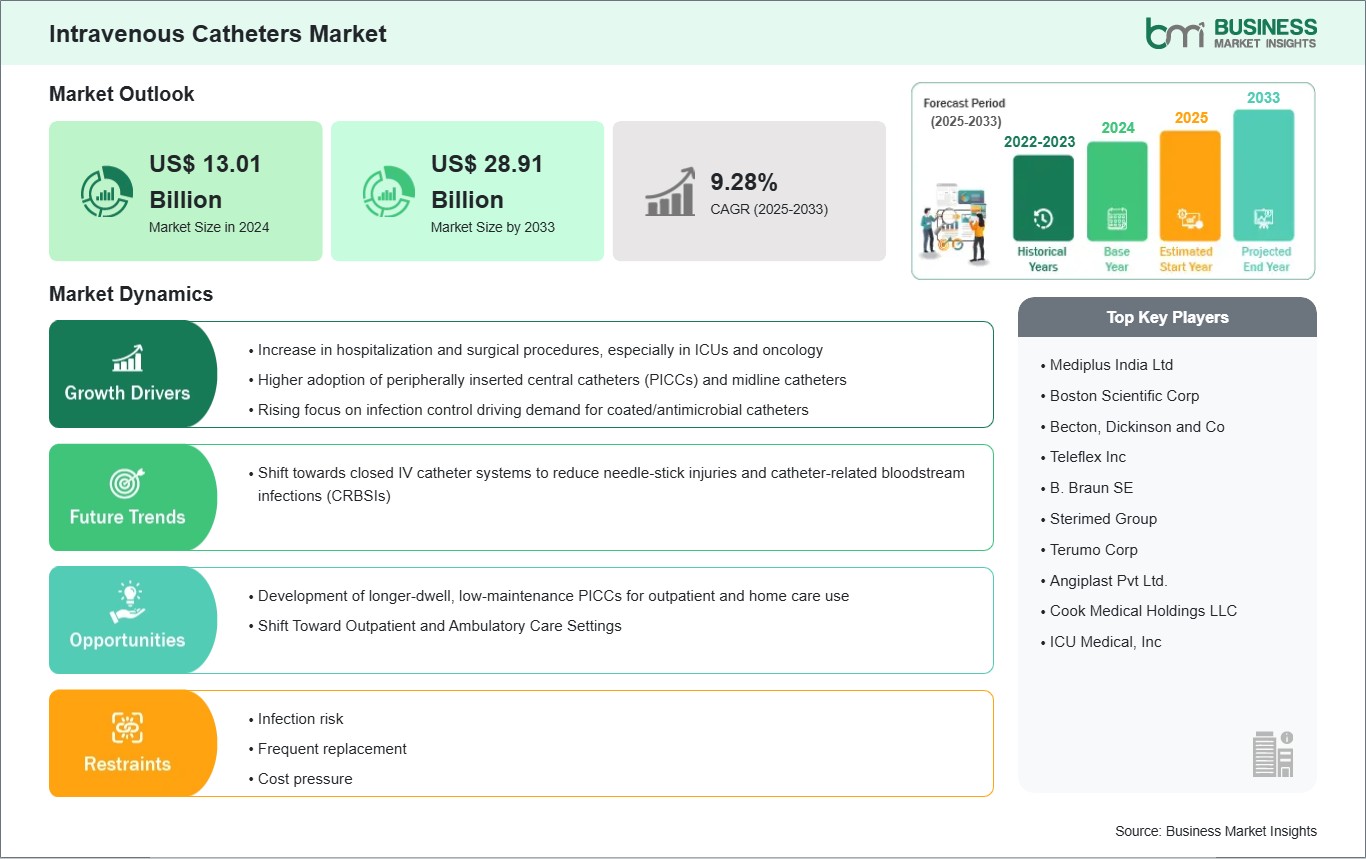

The Intravenous Catheters Market size is expected to reach US$ 28.91 Billion by 2033 from US$ 13.01 Billion in 2024. The market is estimated to record a CAGR of 9.28% from 2025 to 2033.

Executive Summary and Global Market Analysis:

The global intravenous catheters market is experiencing significant growth, driven by an increase in hospitalizations and surgical procedures, particularly in intensive care units (ICUs) and oncology. The higher adoption of peripherally inserted central catheters (PICCs) and midline catheters, along with a growing focus on infection control, is also driving demand for coated and antimicrobial catheters.

However, the risk of catheter-associated infections and complications is hindering market growth. Currently, North America holds the largest share of the global market, largely due to its high prevalence rates and the burden of chronic diseases. In contrast, the Asia Pacific region is rapidly emerging as the fastest-growing market, supported by a developing healthcare infrastructure and a large patient population.

Major companies in the market, such as Medtronic Plc, Abbott Laboratories, and Boston Scientific Corp, are actively pursuing product innovation, forming partnerships, and exploring new markets. As the demand for intravenous catheters increases and new advanced catheters are developed, a noticeable growth rate in the global intravenous catheter market is expected. This will likely lead to reduced catheter costs, improved effectiveness, and ultimately enhanced patient outcomes worldwide.

Intravenous Catheters Market Segmentation Analysis:

Key segments that contributed to the derivation of the Intravenous Catheters market analysis are product, coating type, lumen, and end user.

- By product, intravenous catheters market is segmented into peripheral catheter, central catheter, PICC catheter, and others. The peripheral catheter segment dominated the market in 2024.

- By coating type, intravenous catheters market is segmented into coated catheter and uncoated catheter. The coated catheter segment dominated the market in 2024.

- By lumen, intravenous catheters market is segmented into single-lumen and multi-lumen. The multi-lumen segment dominated the market in 2024.

- By end user, the market is segmented into hospitals & clinics, ambulatory surgical centers, diagnostic imaging centers, and others. The hospitals & clinics segment held the largest share of the market in 2024.

Intravenous Catheters Market Drivers and Opportunities:

Higher Adoption of Peripherally Inserted Central Catheters (PICCs) and Midline Catheters Driving Intravenous Catheters Market

The growing use of Peripherally Inserted Central Catheters (PICCs) and midline catheters is becoming increasingly important in advancing the intravenous (IV) catheter market. PICCs, in particular, are valuable for providing long-term IV therapy that lasts more than one week. This increased demand is largely due to the rise in chronic diseases such as cancer, which often require chemotherapy and other infusions that extend beyond a week.

Additionally, central venous catheters (CVCs), including PICCs, present a lower risk of bloodstream infections than other CVC types. Since PICCs are commonly inserted in the arm, they may provide a more comfortable option for patients undergoing prolonged infusions. The trend towards outpatient and home care has also made PICCs more appealing, as they align with patient preferences and can be utilized in non-traditional care settings. This shift is likely influenced by various factors, including changes in patient preferences and the post-COVID landscape, which has encouraged care to move back into homes and away from hospitals.

Midline catheters are expected to further support this market by fulfilling a unique role between short peripheral IVs and PICCs. This segment caters to therapies that last approximately 1 to 4 weeks, making midline catheters particularly suitable for prolonged antibiotic treatments. As central venous catheters, midlines reduce the need for frequent catheter changes compared to short peripheral IVs, enhancing patient comfort, minimizing supply usage, and often eliminating the necessity to replace short peripheral IVs altogether.

Development of Longer-dwell, Low Maintenance PICCs for Outpatient and Home Care Use

The transition to outpatient and home care presents a significant opportunity for the intravenous catheter market, particularly for longer-dwell, low-maintenance peripheral inserted central catheters (PICCs). Healthcare systems are moving away from hospital settings to reduce costs, driving demand for devices that provide safe and reliable venous access for weeks or even months in non-hospital environments. This shift has spurred ongoing innovation in catheter materials and designs.

Manufacturers of PICCs are now developing a new generation of catheters featuring antimicrobial coatings to minimize the risk of infection. These innovations utilize a unique polyurethane and hydrogel composite that enhances durability and biocompatibility, thereby decreasing the likelihood of complications such as thrombosis and occlusion.

Ensuring patient safety and comfort, especially in home care settings, where medical professionals provide less oversight, remains a challenge. There is a considerable opportunity to design catheters that offer long-term access while reducing the workload for patients and visiting nurses. This could include the implementation of valve PICCs, which maintain a closed system and eliminate the need for heparin flushing. Such advancements may help lower the frequency of required maintenance.

Intravenous Catheters Market Size and Share Analysis

The intravenous catheter market is categorized by product type into peripheral, central, PICC, and others. Peripheral catheters represent the largest segment due to their widespread use and importance for delivering short-term intravenous (IV) therapy. They are utilized extensively across healthcare settings for routine procedures such as administering fluids, medications, or drawing blood samples.

The high usage of peripheral catheters can be attributed to several factors. They are cost-effective, simple to use, and easy to insert. Additionally, short-term vascular access provided by peripheral catheters is suitable for most patients. The demand for these devices is surging, driven by the increasing prevalence of chronic diseases, a growing geriatric population, and more frequent hospitalizations and surgeries. Furthermore, the development of safety-engineered peripheral catheters offers added protection for healthcare workers, addressing the significant concern of needlestick injuries that can occur in clinical practice.

By coating type, the intravenous catheter market is divided into two segments: coated catheters and uncoated catheters. Among these, coated catheters, particularly hydrophilic and antimicrobial coated catheters, represent the largest segment. These devices are designed to address the critical need to reduce catheter-related complications, specifically catheter-associated bloodstream infections (CASSI). CASSI remains a significant issue in healthcare, contributing to increased patient morbidity, mortality, and costs.

Catheter manufacturers are developing devices with antimicrobial coatings that inhibit the growth of bacteria and other microorganisms on the catheter's surface. Furthermore, some catheters are coated with biocompatible materials to reduce the risk of thrombosis and phlebitis. The goal is to enhance both patient safety and comfort. The increasing need to improve patient safety and the efficiency of clinical practices to achieve positive patient outcomes will drive the adoption of coated catheters, especially for patients who are at higher risk and require vascular access for extended periods.

The intravenous catheter market is categorized by lumen into single-lumen and multi-lumen types. The larger segment in this category is multi-lumen catheters, which are favored for their versatility and capability to facilitate multiple functions through a single access point. These catheters feature two or more distinct channels (lumens) that enable healthcare providers to administer incompatible fluids, medications, or blood products simultaneously into the same vein without the chance of mixing them. This capability is particularly vital in settings such as intensive care, emergencies, or for patients undergoing complex therapies like chemotherapy or parenteral nutrition. Additionally, multi-lumen catheters diminish the need for several puncture sites, thus alleviating patient discomfort and reducing risks such as infection and vein injury. They enhance the efficiency of clinical staff by allowing several procedures to be performed from one catheter, leading to better workflow. This increased efficiency makes multi-lumen catheters the preferred choice in critical care environments.

The intravenous catheter market is segmented by end users into hospitals and clinics, ambulatory surgical centers, diagnostic imaging centers, and others. In 2024, the hospitals and clinics segment held the largest share of the market. These facilities are the primary sites for patient care, encompassing surgeries, emergency care, long-term treatment for chronic illnesses, and diagnostic procedures—all of which often require intravenous (IV) access. The high volume of hospital admissions and the increasing prevalence of chronic diseases that necessitate intravenous therapy contribute to the growing demand for catheters. Hospitals and clinics possess the necessary systems and trained healthcare professionals to safely insert and manage various types of catheters, including central and peripheral ones. Despite the rising trend of home care and ambulatory centers, most complex and critical care procedures that significantly depend on IV catheters are still performed in hospitals and clinics.

Intravenous Catheters Market Report Highlights

Intravenous Catheters Market Report Coverage and Deliverables

The "Intravenous Catheters Market Size and Forecast (2022–2033)" report provides a detailed analysis of the market covering below areas:

- Intravenous Catheters market size and forecast at global, regional, and country levels for all the key market segments covered under the scope

- Intravenous Catheters market trends, as well as market dynamics such as drivers, restraints, and key opportunities

- Intravenous Catheters market analysis covering key market trends, global and regional framework, major players, regulations, and recent market developments

- Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments for the Intravenous Catheters market

- Detailed company profiles, including SWOT analysis

Intravenous Catheters Market Country and Regional Insights

The geographical scope of the intravenous catheters market report is divided into five regions: North America, Asia Pacific, Europe, Middle East & Africa, and South & Central America. The Intravenous Catheters market in Asia Pacific is expected to grow significantly during the forecast period.

The Asia Pacific intravenous catheters market encompasses countries such as China, Japan, India, South Korea, Australia, Bangladesh, New Zealand, the Philippines, Singapore, Indonesia, Taiwan, Malaysia, Vietnam, and the Rest of Asia Pacific. This region is the fastest-growing market for intravenous catheters, driven by a combination of demographic, economic, and healthcare-related factors.

A major contributor to this growth is the expansion of inpatient and outpatient services in both public and private hospitals, fueled by increasing government healthcare budgets and investments in infrastructure. For instance, China, India, and Indonesia are in the process of opening new hospitals and increasing surgical volumes. The adoption of IV catheters as the standard method for drug delivery, fluid administration, and anesthesia in these facilities is a significant driver of market growth. Furthermore, the focus on infection control and procedural safety is encouraging hospitals to adopt high-quality, single-use IV catheters to meet international sanitation standards.

Within the Asia Pacific region, China, India, and Japan are expected to be key players in terms of market growth. China is projected to be a major contributor to regional growth, both in revenue and volume, due to its large population, rapidly developing healthcare infrastructure, and government policies that support domestic manufacturing of medical devices and health expenditures—all backed by a strong economic outlook and increasing disposable income.

India is also poised to be a significant market contributor and is expected to be one of the fastest-growing markets. The factors driving this growth include its vast and growing population, the rising burden of chronic diseases, and increasing investments in both public and potential private healthcare institutions.

Japan, characterized by a high ratio of elderly citizens, presents a steady market demand for long-term care and related medical products. Although Japan represents a mature market, its well-developed healthcare system and emphasis on advanced, high-quality medical products will sustain strong demand for innovative intravenous catheters that enhance patient safety and comfort.

Intravenous Catheters Market Research Report Guidance

- The report includes qualitative and quantitative data in the Intravenous Catheters market across product, coating type, lumen, and end user, and geography.

- The report starts with the key takeaways (chapter 2), highlighting the key trends and outlook of the intravenous catheters market.

- Chapter 3 includes the research methodology of the study.

- Chapter 4 further includes ecosystem analysis.

- Chapter 5 highlights the major industry dynamics in the intravenous catheters market, including factors that are driving the market, prevailing deterrents, potential opportunities and future trends. Impact analysis of these drivers and restraints is also covered in this section.

- Chapter 6 discusses the intravenous catheters market scenario, in terms of historical market revenues, and forecast till the year 2033.

- Chapters 7 to 11 cover intravenous catheters market segments by product, coating type, lumen, end user, and geography across North America, Europe, APAC, Middle East and Africa, South and Central America. They cover the market volume revenue forecast and factors driving the market.

- Chapter 12 describes the competitive analysis along with the heat map analysis for the key players operating in the market.

- Chapter 13 describes the industry landscape analysis. It provides detailed descriptions of various business activities such as market initiatives, new developments, mergers, and joint ventures globally, along with a competitive landscape.

- Chapter 14 provides a detailed profile of the major companies operating in the Intravenous Catheters market. Companies have been profiled on the basis of their key facts, business description, products and services, financial overview, SWOT analysis, and key developments.

- Chapter 15, i.e., the appendix, is inclusive of a brief overview of the company, list of abbreviations, and disclaimer section.

Intravenous Catheters Market News and Key Development:

The intravenous catheters market y

- FDA approved BD CentroVena Central Venous Catheter (CVC) with CentroVena One Insertion System. This approval expands BD's offerings in acute central venous access, designed for short-term use (less than 30 days) to administer fluids, blood products, drugs, and for blood withdrawal and central venous pressure monitoring, including power injection capabilities. (Source: Becton Dickinson and Co, Press Release, April 2025)

- B. Braun Medical received FDA clearance for its Introcan Safety 2 Deep Access IV Catheter. This new device is designed to improve safety and patient comfort by providing deeper venous access while incorporating safety features to reduce needlestick injuries and blood exposure to healthcare providers. (Source: B Braun SE, Press Release, October 2024)

Key Sources Referred:

- World Health Organization (WHO)

- The World Bank Group

- World Heart Federation (WHF)

- Eurostat

- Centers for Disease Control and Prevention

- Worldometer

- The Lancet

- International Trade Administration

Intravenous Catheters Market Strategic Insights

Intravenous CathetersMarket Report Highlights

| Report Attribute | Details |

| Market size in 2024 | US$ 13.01 Billion |

| Market Size by 2033 | US$ 28.91 Billion |

| Global CAGR (2025 - 2033) | 9.28% |

| Historical Data | 2022-2023 |

| Forecast period | 2025-2033 |

| Segments Covered |

By Product

|

|

Regions and Countries Covered

|

|

| North America | US, Canada, Mexico |

| Europe | Belgium, Austria, Finland, Denmark, Greece, Poland, Romania, Russia, Ukraine, Czech Republic, Slovakia, Bulgaria, Italy, Luxembourg, Germany, Switzerland, France, Netherlands, Norway, Portugal, Spain, Sweden, United Kingdom |

| Asia-Pacific | Australia, China, India, Japan, South Korea, Indonesia, Malaysia, Philippines, Singapore, Thailand, Vietnam, Bangladesh, New Zealand, Taiwan |

| South and Central America | Brazil, Argentina, Peru, Chile, Colombia |

| Middle East and Africa | Bahrain, Kuwait, Oman, Qatar, Saudi Arabia, United Arab Emirates, Turkiye, South Africa, Egypt, Algeria, Nigeria |

| Market leaders and key company profiles |

|

Intravenous Catheters Market Country and Regional Insights