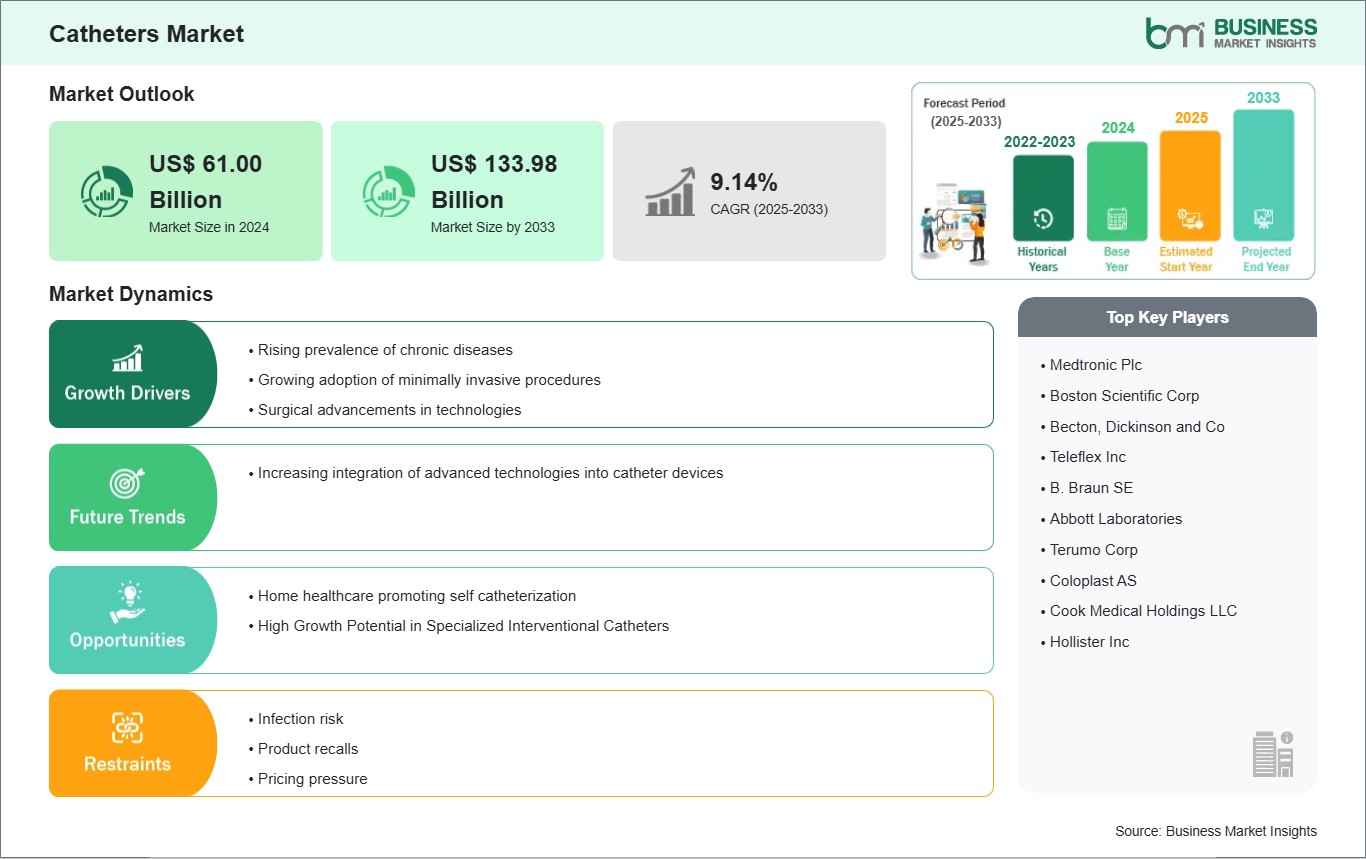

The Catheters Market size is expected to reach US$ 133.98 Billion by 2033 from US$ 61.00 Billion in 2024. The market is estimated to record a CAGR of 9.14% from 2025 to 2033.

Executive Summary and Global Market Analysis:

The global catheters market is experiencing significant growth driven by rising prevalence of chronic diseases, growing adoption of minimally invasive procedures, and technological advancements. However, the risk of catheter-associated infections & complications is slowing market evolution. Geographically, North America currently has the largest total share of the global market, due to the high prevalence of chronic diseases across the region.

Moreover, Asia Pacific is rapidly emerging as the fastest growing market driven by a combination of a rising burden of chronic diseases and the rapid adoption of innovative medical technologies. Medtronic Plc, Abbott Laboratories, and Boston Scientific Corp are major companies in the market actively pursuing product innovation, partnerships, and developing markets. As demand for catheters grows, manufacturers are developing advanced catheters, so a significant growth in global catheters is expected to emerge, driving down catheter cost, providing greater efficacy while improving global patient outcomes.

Catheters Market Strategic Insights

Key segments that contributed to the derivation of the Catheters market analysis are product, type, coating type, lumen, and end user.

- By product, catheters market is segmented into cardiovascular catheters, intravenous catheters, urological catheters, specialty catheters, neurovascular catheters. The cardiovascular catheters segment dominated the market in 2024.

- By type, catheters market is segmented into Foley catheter, intermittent catheter, IVUS catheter, balloon catheter, and others. The balloon catheter segment dominated the market in 2024.

- By coating type, catheters market is segmented into coated catheters and uncoated catheters. The coated catheters segment dominated the market in 2024.

- By lumen, catheters market is segmented into single-lumen and multi-lumen. The multi-lumen segment dominated the market in 2024.

- By end user, the market is segmented into hospitals & clinics, home care settings, ambulatory surgical centers, diagnostic imaging centers, and others. The hospitals & clinics segment held the largest share of the market in 2024.

Catheters Market Drivers and Opportunities:

Rising Prevalence of Chronic Diseases Driving Catheters Market

The demand for catheters is increasing significantly, primarily driven by a global surge in chronic diseases. As per the World Heart Federation’s May 2023 report, cardiovascular diseases are responsible for approximately 20.5 million deaths each year. Such conditions necessitate procedures, including angiography and angioplasty, which mostly rely on cardiac catheters. Furthermore, the prevalence of urinary incontinence affects an estimated 5% to 70% of the global population, while around 850 million individuals are living with kidney disease, as indicated by the International Society of Nephrology. This surge in urinary and renal issues underscores the growing need for urological catheters to manage bladder function and related treatments.

The World Stroke Organization reports around 12 million new stroke cases annually, often resulting in neurological complications that require catheter intervention for bladder control or various brain procedures. The International Diabetes Federation predicts that by 2024, approximately 589 million adults will be diagnosed with diabetes, which may lead to bladder dysfunction, further enhancing the demand for catheters. As the population continues to age and increasingly live with these chronic conditions, catheters play an essential role in diagnosis, treatment, and ongoing patient care. Consequently, the catheter market is anticipated to experience robust growth in the coming years.

Growing Demand for Home Healthcare and Increasing Adoption of Self-Catheterization

The rising demand for home healthcare and self-catheterization offers a huge opportunity for the players operating in the catheter market. The trend in healthcare is increasingly shifting from hospital-based care to in-home management, particularly for older adults with chronic conditions. As these individuals often face challenges related to diseases such as chronic urinary retention or neurogenic bladder—commonly associated with spinal cord injuries or multiple sclerosis, there is a heightened demand for effective disease management outside of traditional hospital settings.

Patients are increasingly opting for intermittent self-catheterization as a commonly used method for bladder management, as it not only supports enhanced mobility and independence but also mitigates risk concerning urinary tract infections compared to continuous catheterization methods.

Advancements in technology are contributing significantly to this transition, as newer catheter designs often feature specialized coatings and user-friendly designs that facilitate easier insertion and minimize the risk of infection. Telehealth has also proven invaluable in this context, as it enables remote patient education, thereby empowering individuals who utilize self-catheterization to build confidence and adhere to their care plans effectively.

The surge in telehealth usage since 2020 has demonstrated its capacity to deliver healthcare services directly into the home, simplifying the self-care process for many patients. As healthcare systems prioritize patient-centered care, there is an increasing necessity for user-friendly catheters specifically designed for home use and self-catheterization.

Catheters Market Size and Share Analysis

The catheters market is classified by products into cardiovascular catheters, intravenous catheters, urological catheters, specialty catheters, and neurovascular catheters. The cardiovascular catheters segment has emerged as the leader in the market in 2024 and is projected to maintain this position moving forward. This growth can be attributed to the increasing preference for minimally invasive surgical techniques in cardiac care and related disciplines. This segment encompasses diagnostic, interventional, and electrophysiology catheters. The persistent prevalence of heart disease significantly influences the expansion of this market segment, as there is a clear correlation between the demand for these specialized catheters and the global challenge posed by cardiovascular diseases (CVDs). The World Health Organization (WHO) has identified CVDs as the foremost cause of mortality globally, highlighting the critical need for diagnostic and therapeutic approaches that frequently rely on catheters.

A pertinent example is percutaneous coronary intervention (PCI), a widely utilized method for addressing blocked arteries, which depends on guiding catheters, balloon catheters, and stents. The rising number of PCI procedures conducted globally, driven by increasing rates of coronary artery disease and heart attacks, further enhances the demand for these essential catheters.

By type, the catheters market is segmented into Foley catheter, intermittent catheter, IVUS catheter, balloon catheter, and others. The balloon catheter segment dominated the market in 2024, primarily due to its essential function, which involves an inflatable balloon at the tip of the catheter that can be expanded to dilate narrowed vessels or passages, deliver stents, or achieve temporary occlusion. This versatile nature renders balloon catheters indispensable for a variety of minimally invasive medical procedures. Their significance is largely influenced by the global prevalence of cardiovascular diseases (CVDs), particularly Coronary Artery Disease (CAD) and Peripheral Artery Disease (PAD). According to CDC data from 2023, CAD, the most common form of heart disease, affected around 1 in 20 adults aged over 20 in the United States.

Dr. Andreas Gruntzig's 1974 development of balloon angioplasty revolutionized the treatment of stenosed arteries, marking a transition from highly invasive surgical methods to less traumatic catheter-based interventions. Balloon angioplasty has since evolved into a cornerstone of contemporary cardiology. Balloon catheters are crucial in procedures like Percutaneous Transluminal Coronary Angioplasty and Percutaneous Transluminal Angioplasty. In Percutaneous Transluminal Angioplasty, these catheters help compress the coronary plaque against the arterial walls, thus restoring blood flow.

By coating type, the catheters market is segmented into coated catheters and uncoated catheters. In 2024, the segment of coated catheters captured the largest share of the market. Significant areas for improvement were identified, focusing on enhancing patient comfort and minimizing the occurrence of catheter-associated infections (CAIs). These specialized coatings can be utilized on different types of catheters, including those for urinary and cardiovascular applications, thereby upgrading standard instruments into sophisticated devices for both treatment and diagnostic purposes. Hydrophilic coatings remained the most common and extensively utilized option. These coatings significantly enhance the catheter insertion and removal process by becoming slippery and substantially reducing friction.

By lumen, the catheters market is segmented into single-lumen and multi-lumen. In 2024, the multi-lumen segment held the largest market share. This is attributed to the versatility of multi-lumen catheters, which makes them the most commonly used catheters in various medical situations. In contrast, a single-lumen catheter has one internal channel that allows for only one function at a time, such as fluid infusion, medication infusion, or drainage.

By end user, the catheters market is segmented into hospitals & clinics, home care settings, ambulatory surgical centers, diagnostic imaging centers, and others. In 2024, the hospitals and clinics segment held the dominant position in the market. This is due to their crucial role as primary points for patient admission for treatment, diagnosis, and surgical procedures, which often depend on catheter-based interventions. The high volume of patients receiving care in these facilities, along with the wide variety of medical conditions that require catheterization, helps maintain their leading position. A significant proportion of hospitalized patients require catheters during their stay.

Catheters Market Report Highlights

| Report Attribute | Details |

| Market size in 2024 | US$ 61.00 Billion |

| Market Size by 2033 | US$ 133.98 Billion |

| Global CAGR (2025 - 2033) | 9.14% |

| Historical Data | 2022-2023 |

| Forecast period | 2025-2033 |

| Segments Covered |

By Product

|

|

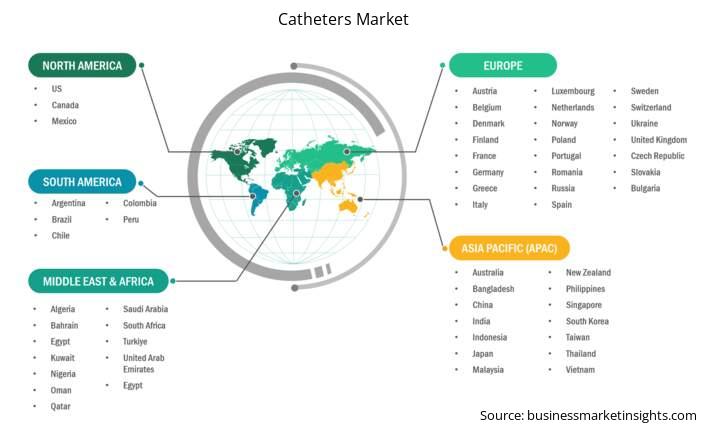

Regions and Countries Covered

|

|

| North America | US, Canada, Mexico |

| Europe | Belgium, Austria, Finland, Denmark, Greece, Poland, Romania, Russia, Ukraine, Czech Republic, Slovakia, Bulgaria, Italy, Luxembourg, Germany, Switzerland, France, Netherlands, Norway, Portugal, Spain, Sweden, United Kingdom |

| Asia-Pacific | Australia, China, India, Japan, South Korea, Indonesia, Malaysia, Philippines, Singapore, Thailand, Vietnam, Bangladesh, New Zealand, Taiwan |

| South and Central America | Brazil, Argentina, Peru, Chile, Colombia |

| Middle East and Africa | Bahrain, Kuwait, Oman, Qatar, Saudi Arabia, United Arab Emirates, Turkiye, South Africa, Egypt, Algeria, Nigeria |

| Market leaders and key company profiles |

|

Catheters Market Report Coverage and Deliverables

The "Catheters Market Size and Forecast (2022–2033)" report provides a detailed analysis of the market covering below areas:

- Catheters market size and forecast at global, regional, and country levels for all the key market segments covered under the scope

- Catheters market trends, as well as market dynamics such as drivers, restraints, and key opportunities

- Catheters market analysis covering key market trends, global and regional framework, major players, regulations, and recent market developments

- Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments for the Catheters market

- Detailed company profiles, including SWOT analysis

Catheters Market Country and Regional Insights

The geographical scope of the catheters market report is divided into five regions: North America, Asia Pacific, Europe, Middle East & Africa, and South & Central America. The Catheters market in Asia Pacific is expected to grow significantly during the forecast period.

The Asia Pacific catheters market comprises countries such as China, Japan, India, South Korea, Australia, Bangladesh, New Zealand, the Philippines, Singapore, Indonesia, Taiwan, Malaysia, Vietnam, and the Rest of the region. Several factors are driving the market's expansion. Many developing countries are rapidly enhancing their healthcare infrastructure, with governments investing significantly in the construction of hospitals and the upgrading of medical devices. One key factor contributing to the surged in demand for surgical procedures and consumables, including catheters, is the growth of medical tourism in countries such as Thailand, India, and Malaysia. Moreover, the private sector has become an increasingly significant part of the healthcare landscape in the region. This sector is competing vigorously on service quality and speed of procedures, resulting in a higher usage of essential consumable products, including catheters.

The region also benefits from a large and skilled workforce, which supports local production hubs, consequently lowering production costs and increasing the supply of catheter products in countries such as Vietnam, India, and Malaysia. Regulatory agencies in several Asia Pacific countries are actively seeking to expedite their approval processes and incentivize local production, encouraging new entrants and expansions among manufacturers. Additionally, the rise in health insurance subscriptions, particularly in urban and semi-urban areas, has improved access to hospital-supported health systems. This development translates into a higher number of surgical and diagnostic procedures requiring catheter interventions and consumables. These region-specific advancements suggest a strong and sustained growth trajectory for the catheter market in the Asia Pacific region in the coming years.

The catheter market in China, India, and Japan is experiencing significant growth, driven by each country's unique demographics and healthcare landscapes. In China, a large and rapidly aging population, coupled with a rising prevalence of chronic diseases and significant government investment in healthcare infrastructure, is fueling demand for advanced catheter technologies, particularly in minimally invasive procedures. India's market is similarly growing, supported by a huge population and a rising case of chronic conditions such as cardiovascular diseases and diabetes. Furthermore, government initiatives like Ayushman Bharat are expanding healthcare access, leading to a growing demand for affordable yet advanced medical devices. There is also a strong trend towards antimicrobial and home-care compatible catheters.

In Japan, the catheter market is characterized by a highly advanced healthcare system and an aging population that experiences a high incidence of age-related ailments. This results in a steady demand for high-quality, specialized catheters. Favorable reimbursement policies, well-established healthcare facilities, and a strong emphasis on technological innovation and patient comfort further enhance the growth of the catheter market in Japan. Collectively, these three nations represent a dynamic and expanding market for catheters, driven by demographic shifts, evolving disease patterns, and continuous advancements in medical technology and healthcare accessibility.

Catheters Market Research Report Guidance

- The report includes qualitative and quantitative data in the Catheters market across product, type, coating type, lumen, end user, and geography.

- The report starts with the key takeaways (chapter 2), highlighting the key trends and outlook of the catheters market.

- Chapter 3 includes the research methodology of the study.

- Chapter 4 further includes ecosystem analysis.

- Chapter 5 highlights the major industry dynamics in the catheters market, including factors that are driving the market, prevailing deterrents, potential opportunities and future trends. Impact analysis of these drivers and restraints is also covered in this section.

- Chapter 6 discusses the catheters market scenario, in terms of historical market revenues, and forecast till the year 2033.

- Chapters 7 to 12 cover catheters market segments by product, type, coating type, lumen, end user, and geography across North America, Europe, APAC, Middle East and Africa, and South and Central America. They cover the market volume revenue forecast and factors driving the market.

- Chapter 13 describes the competitive analysis along with the heat map analysis for the key players operating in the market.

- Chapter 14 describes the industry landscape analysis. It provides detailed descriptions of various business activities such as market initiatives, new developments, mergers, and joint ventures globally, along with a competitive landscape.

- Chapter 15 provides a detailed profile of the major companies operating in the Catheters market. Companies have been profiled on the basis of their key facts, business description, products and services, financial overview, SWOT analysis, and key developments.

- Chapter 16, i.e., the appendix, is inclusive of a brief overview of the company, list of abbreviations, and disclaimer section.

Catheters Market News and Key Development:

The catheters market is evaluated by gathering qualitative and quantitative data post primary and secondary research, which includes important corporate publications, association data, and databases. A few of the key developments in the Catheters market are:

- Medtronic announced its IN. PACT AV drug-coated balloon catheter (DCB) will be reimbursed in Korea starting in May for use in dialysis patients who experience early re-narrowing of their vascular access site. The device is used to treat stenotic lesions -narrowed blood vessels -in patients with end-stage renal disease (ESRD), most of whom undergo hemodialysis, a procedure that filters waste from the blood when the kidneys no longer function. (Source: Medtronic, Company Website, April 2025)

- FDA approved BD CentroVena Central Venous Catheter (CVC) with CentroVena One Insertion System. This approval expands BD's offerings in acute central venous access, designed for short-term use (less than 30 days) to administer fluids, blood products, drugs, and for blood withdrawal and central venous pressure monitoring, including power injection capabilities. (Source: Becton Dickinson and Co, Press Release, April 2025)

Key Sources Referred:

- World Health Organization (WHO)

- The World Bank Group

- World Heart Federation (WHF)

- Eurostat

- Centers for Disease Control and Prevention

- Worldometer

- The Lancet

- International Trade Administration