Analysis - by Type (Ethylene, Benzene, Propylene, Xylene, and Others), Application (Polymers, Paints and Coatings, Solvent, Rubber, Adhesives, Surfactants, and Others), and End-use Industry (Packaging, Automotive, Construction, Electrical & Electronics, Healthcare, Agriculture, Aerospace & Defense, and Others)

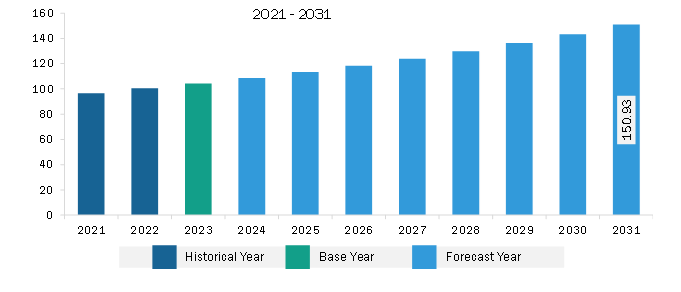

The Europe petrochemicals market was valued at US$ 104.32 billion in 2023 and is expected to reach US$ 150.93 billion by 2031; it is estimated to record a CAGR of 4.7% from 2023 to 2031.

Surge in Demand for Polymers across Various End-Use Industries Drives EuropePetrochemicals Market

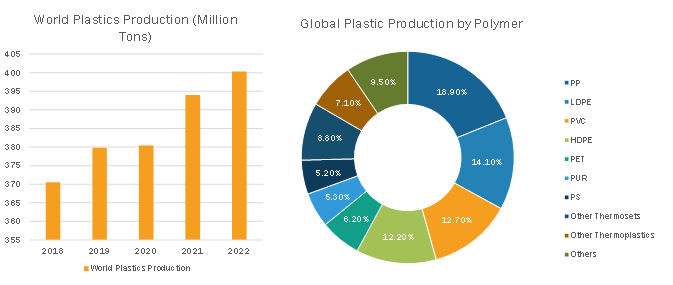

Petrochemical-based polymers such as polyamide, polypropylene, polystyrene, high-density polyethylene, thermoplastic elastomers, polyurethane, polycarbonate, and polyvinyl chloride are widely used in the automotive industry as these polymers offer excellent durability and resistance to corrosion. According to the CDI Products Company, the automotive industry is a significant consumer of polymers. These polymers enhance the longevity of automotive components, including interior parts and exterior body panels, as well as under-the-hood applications. As per the Plastics Europe 2023 report, the global production of plastics increased from 380.4 million tons in 2020 to 400.3 million tons in 2022.

Global Plastics Production — by Polymer, 2022

Source: Plastics Europe, 2023

According to the CDI Products Company, the automotive industry has various applications of petrochemical-based polymers, including PTFE seals, O-rings, bearings and thrust bearings, low-drag mudflaps, suspension cylinder seals, sensor covers, diaphragms, rotary seals, custom-made gaskets, wiring harnesses & housing, and battery sealing for pressure valves, among others. The EU registered the production of more than 9 million cars in the first three quarters of 2023, a rise of 14% from the same quarter in 2022, as per the European Automobile Manufacturers' Association. The growing utilization of polymers in the automotive industry, coupled with the developments in the automotive industry, fuels the demand for petrochemicals.

Polymers are used in construction for insulation, windows, pipes, and coatings due to their energy-efficient properties. They help reduce energy consumption in buildings by providing effective thermal insulation. With the rise in construction activities, the demand for petrochemical-based materials is also increasing. Thus, the rising demand for polymers across various end-use industries fuels the petrochemicals market growth.

Europe Petrochemicals Market Overview

Germany is one of the leading producers of automobiles in the world, and several major car manufacturing companies, including Volkswagen, BMW AG, and Audi, are located in the country. Germany produces ~6 million vehicles annually, including passenger cars and commercial vehicles. According to Germany Trade & Invest GmbH, Germany is Europe's largest automotive market, with strong production and sales, accounting for ~25% of all passenger cars manufactured and almost 20% of all new registrations. The country also possesses the largest concentration of original equipment manufacturer (OEM) plants in Europe. With 44 OEM sites located in Germany, the country's OEM market share in the European Union was more than 55% in 2021. The automotive industry, a cornerstone of Germany's economy, relies heavily on petrochemical products. Petrochemicals are essential in producing various automotive components such as plastics for interiors, synthetic rubber for tires, and polymers for lightweight, fuel-efficient parts. As German automakers continually innovate to produce efficient and lightweight vehicles, the demand for specialized petrochemicals remains high.

Moreover, the pharmaceutical and healthcare sectors in Germany contribute to the demand for petrochemicals. The country is a leader in pharmaceutical production, and petrochemical derivatives are critical in manufacturing drugs, medical devices, and packaging materials. The demand for high-quality plastics and polymers that meet stringent health and safety standards is high, supporting the production of syringes, IV bags, and other medical supplies.

Europe Petrochemicals Market Revenue and Forecast to 2031 (US$ Billion)

Europe Petrochemicals Market Segmentation

The Europe petrochemicals market is segmented based on type, application, end-use industry, and country. Based on type, the Europe petrochemicals market is segmented into ethylene, benzene, propylene, xylene, and others. The ethylene segment held the largest market share in 2023.

In terms of application, the Europe petrochemicals market is segmented into polymers, paints and coatings, solvent, rubber, adhesives, surfactants, and others. The polymers segment held the largest market share in 2023.

By end-use industry, the Europe petrochemicals market is categorized into packaging, automotive, construction, electrical & electronics, healthcare, agriculture, aerospace & defense, and others. The packaging segment held the largest market share in 2023.

Based on country, the Europe petrochemicals market is segmented into Germany, France, Italy, the UK, Russia, and the Rest of Europe. The Rest of Europe dominated the Europe petrochemicals market share in 2023.

Shell Plc, LyondellBasell Industries NV, Saudi Basic Industries Corp, BASF SE, INEOS Group Holdings SA, Dow Inc, Chevron Phillips Chemical Company LLC, China Petroleum & Chemical Corp, Mitsubishi Chemical Group Corp, and Exxon Mobil Corp are some of the leading players operating in the Europe petrochemicals market.

Europe Petrochemicals Market Strategic Insights

Get more information on this report

Europe Petrochemicals Market Segmentation Analysis

Europe Petrochemicals Market Report Highlights

Europe Petrochemicals Report Scope

Report Attribute

Details

Market size in 2023

US$ 104.32 Billion

Market Size by 2031

US$ 150.93 Billion

CAGR (2023 - 2031)

4.7%

Historical Data

2021-2023

Forecast period

2025-2031

Segments Covered

By Type

Ethylene

Benzene

Propylene

Xylene

By Application

Polymers

Paints and Coatings

Solvent

Rubber

Adhesives

Surfactants

By End-use Industry

Packaging

Automotive

Construction

Electrical & Electronics

Healthcare

Agriculture

Aerospace & Defense

Regions and Countries Covered

Europe

UK, Germany, France, Italy, Russia, Rest of Europe

Market leaders and key company profiles

Shell Plc

LyondellBasell Industries NV

Saudi Basic Industries Corp

BASF SE

INEOS Group Holdings SA

Dow Inc

Chevron Phillips Chemical Company LLC

China Petroleum & Chemical Corp

Mitsubishi Chemical Group Corp

Exxon Mobil Corp

Get more information on this report

Europe Petrochemicals Market Country and Regional Insights

Get more information on this report

Identical Market Reports with other Region/Countries

The List of Companies - Europe Petrochemicals Market

Shell PlcLyondellBasell Industries NVSaudi Basic Industries CorpBASF SEINEOS Group Holdings SADow IncChevron Phillips Chemical Company LLCChina Petroleum & Chemical CorpMitsubishi Chemical Group CorpExxon Mobil Corp

Frequently Asked Questions

How big is the Europe Petrochemicals Market?

The Europe Petrochemicals Market is valued at US$ 104.32 Billion in 2023, it is projected to reach US$ 150.93 Billion by 2031.

What is the CAGR for Europe Petrochemicals Market by (2023 - 2031)?

As per our report Europe Petrochemicals Market, the market size is valued at US$ 104.32 Billion in 2023, projecting it to reach US$ 150.93 Billion by 2031. This translates to a CAGR of approximately 4.7% during the forecast period.

What segments are covered in this report?

The Europe Petrochemicals Market report typically cover these key segments-

Type (Ethylene, Benzene, Propylene, Xylene)

Application (Polymers, Paints and Coatings, Solvent, Rubber, Adhesives, Surfactants)

What is the historic period, base year, and forecast period taken for Europe Petrochemicals Market?

The historic period, base year, and forecast period can vary slightly depending on the specific market research report. However, for the Europe Petrochemicals Market report:

Historic Period : 2021-2023

Base Year : 2023

Forecast Period : 2025-2031

Who are the major players in Europe Petrochemicals Market?

The Europe Petrochemicals Market is populated by several key players, each contributing to its growth and innovation. Some of the major players include:

Shell Plc

LyondellBasell Industries NV

Saudi Basic Industries Corp

BASF SE

INEOS Group Holdings SA

Dow Inc

Chevron Phillips Chemical Company LLC

China Petroleum & Chemical Corp

Mitsubishi Chemical Group Corp

Exxon Mobil Corp

Who should buy this report?

The Europe Petrochemicals Market report is valuable for diverse stakeholders, including:

Investors: Provides insights for investment decisions pertaining to market growth, companies, or industry insights. Helps assess market attractiveness and potential returns.

Industry Players: Offers competitive intelligence, market sizing, and trend analysis to inform strategic planning, product development, and sales strategies.

Suppliers and Manufacturers: Helps understand market demand for components, materials, and services related to concerned industry.

Researchers and Consultants: Provides data and analysis for academic research, consulting projects, and market studies.

Financial Institutions: Helps assess risks and opportunities associated with financing or investing in the concerned market.

Essentially, anyone involved in or considering involvement in the Europe Petrochemicals Market value chain can benefit from the information contained in a comprehensive market report.

Get Free Sample For Europe Petrochemicals Market

Get Free Sample For Europe Petrochemicals Market