Analysis - by Product and Services (Medical Device Connectivity Solutions and Medical Device Connectivity Services), Technology (Wireless Technologies, Hybrid Technologies, and Wired Technologies), Application (Vital Signs and Patient Monitors, Anaesthesia Machines and Ventilators, Infusion Pumps, and Others), and End User (Hospitals, Ambulatory Surgical Centers, Imaging and Diagnostic Centers, and Homecare Settings)

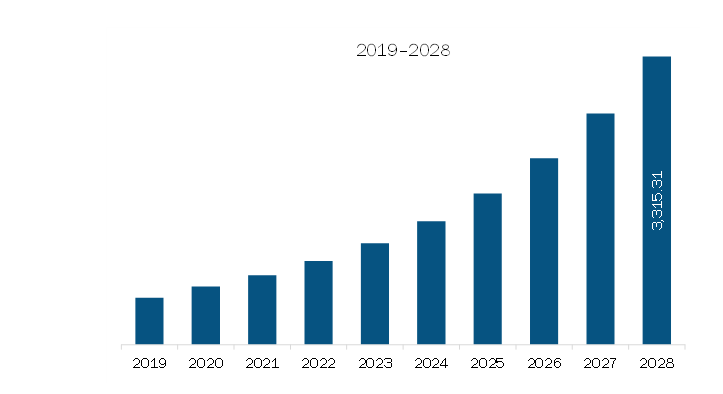

The North America medical device connectivity market was valued at US$ 964.54 million in 2022 and is expected to reach US$ 3,315.31 million by 2028; it is estimated to register a CAGR of 22.8% from 2022 to 2028.

Massive Acceleration of Telehealth Services Amid COVID-19 Pandemic Fuels North America Medical Device Connectivity Market Growth

Due to the outbreak of COVID-19 in November 2019, the Centers for Disease Control and Prevention (CDC) issued a guidance in February 2020 for the healthcare providers and people residing in the affected areas to maintain social distancing and offer clinical services through virtual means such as telehealth. To examine changes in the frequency of use of telehealth services during the early pandemic period, CDC analyzed data from four of the largest US telehealth providers that offer services in all states. According to this data, the number of telehealth visits increased by 50% during the first quarter of 2020 as compared to the same period in 2019. Further, during the surveillance week 13 in 2020, the visits increased by 154% as compared to the same period in 2019. As telehealth bridged the gap between people, physicians, and health systems by enabling patients to stay at home and communicate with physicians through virtual channels, it is helping in reducing unnecessary visits to hospitals for minor issues. When combined with telehealth services, wearable technology can help care providers study real-time patient data to generate intelligent individualized insights and curate the best treatment plan from the comfort and safety of their homes.

North America Medical Device Connectivity Market Overview

The medical device connectivity market in North America is segmented into the US, Canada, and Mexico. The US is expected to be the largest contributor to the market in this region. The market growth in North America is ascribed to the rapid changes in the regulations of medical devices. According to a system architect of Drägerwerk AG and Co. KGaA, with continuous advancements in medical technology, interoperability capabilities between devices such as ventilators and fusion pumps have lagged. The standards of medical device interoperability are finalized and approved by the US Department of Health and Human Services' Office of the National Coordinator for Health Information Technology and the Centers for Medicare and Medicaid Services.

North America Medical Device Connectivity Market Revenue and Forecast to 2028 (US$ Million)

North America Medical Device Connectivity Market Segmentation

The North America medical device connectivity market is segmented on the basis of product and services, technology, application, end user, and country. Based on product and services, the North America medical device connectivity market is bifurcated into medical device connectivity solutions and medical device connectivity services. The medical device connectivity solutions segment registered a larger market share in 2022.

Based on technology, the North America medical device connectivity market is segmented into wireless technologies, hybrid technologies, and wired technologies. The wireless technologies segment registered the largest market share in 2022.

Based on application, the North America medical device connectivity market is segmented into vital signs and patient monitors, anesthesia machines and ventilators, infusion pumps, and others. The vital signs and patient monitors segment registered the largest market share in 2022.

Based on end user, the North America medical device connectivity market is segmented into hospitals, ambulatory surgical centers, imaging and diagnostic centers, and homecare settings. The hospitals segment registered the largest market share in 2022.

Based on country, the North America medical device connectivity market is segmented into the US, Canada, and Mexico. The US dominated the market share in 2022.

Cisco Systems Inc, Digi International Inc., GE HealthCare Technologies Inc, iHealth Labs Inc, Infosys Ltd, Koninklijke Philips NV, Lantronix Inc., Medtronic Plc, Oracle Corp, and Silicon & Software Systems Ltd are the leading companies operating in the North America medical device connectivity market.

North America Medical Device Connectivity Market Strategic Insights

Get more information on this report

North America Medical Device Connectivity Market Segmentation Analysis

North America Medical Device Connectivity Market Report Highlights

North America Medical Device Connectivity Report Scope

Report Attribute

Details

Market size in 2022

US$ 964.54 Million

Market Size by 2028

US$ 3,315.31 Million

CAGR (2022 - 2028)

22.8%

Historical Data

2020-2021

Forecast period

2023-2028

Segments Covered

By Product and Services

Medical Device Connectivity Solutions

Medical Device Connectivity Services

By Technology

Wireless Technologies

Hybrid Technologies

Wired Technologies

By Application

Vital Signs and Patient Monitors

Anaesthesia Machines and Ventilators

Infusion Pumps

By End User

Hospitals

Ambulatory Surgical Centers

Imaging and Diagnostic Centers

Homecare Settings

Regions and Countries Covered

North America

US, Canada, Mexico

Market leaders and key company profiles

Cisco Systems Inc

Digi International Inc.

GE HealthCare Technologies Inc

iHealth Labs Inc

Infosys Ltd

Koninklijke Philips NV

Lantronix Inc.

Medtronic Plc

Oracle Corp

Silicon & Software Systems Ltd

Get more information on this report

North America Medical Device Connectivity Market Country and Regional Insights

Get more information on this report

Identical Market Reports with other Region/Countries

The List of Companies - North America Medical Device Connectivity Market

1. Cisco Systems Inc2. Digi International Inc.3. GE HealthCare Technologies Inc4. iHealth Labs Inc5. Infosys Ltd6. Koninklijke Philips NV7. Lantronix Inc.8. Medtronic Plc9. Oracle Corp10. Silicon & Software Systems Ltd

Frequently Asked Questions

How big is the North America Medical Device Connectivity Market?

The North America Medical Device Connectivity Market is valued at US$ 964.54 Million in 2022, it is projected to reach US$ 3,315.31 Million by 2028.

What is the CAGR for North America Medical Device Connectivity Market by (2022 - 2028)?

As per our report North America Medical Device Connectivity Market, the market size is valued at US$ 964.54 Million in 2022, projecting it to reach US$ 3,315.31 Million by 2028. This translates to a CAGR of approximately 22.8% during the forecast period.

What segments are covered in this report?

The North America Medical Device Connectivity Market report typically cover these key segments-

Product and Services (Medical Device Connectivity Solutions, Medical Device Connectivity Services)

Application (Vital Signs and Patient Monitors, Anaesthesia Machines and Ventilators, Infusion Pumps)

End User (Hospitals, Ambulatory Surgical Centers, Imaging and Diagnostic Centers, Homecare Settings)

What is the historic period, base year, and forecast period taken for North America Medical Device Connectivity Market?

The historic period, base year, and forecast period can vary slightly depending on the specific market research report. However, for the North America Medical Device Connectivity Market report:

Historic Period : 2020-2021

Base Year : 2022

Forecast Period : 2023-2028

Who are the major players in North America Medical Device Connectivity Market?

The North America Medical Device Connectivity Market is populated by several key players, each contributing to its growth and innovation. Some of the major players include:

Cisco Systems Inc

Digi International Inc.

GE HealthCare Technologies Inc

iHealth Labs Inc

Infosys Ltd

Koninklijke Philips NV

Lantronix Inc.

Medtronic Plc

Oracle Corp

Silicon & Software Systems Ltd

Who should buy this report?

The North America Medical Device Connectivity Market report is valuable for diverse stakeholders, including:

Investors: Provides insights for investment decisions pertaining to market growth, companies, or industry insights. Helps assess market attractiveness and potential returns.

Industry Players: Offers competitive intelligence, market sizing, and trend analysis to inform strategic planning, product development, and sales strategies.

Suppliers and Manufacturers: Helps understand market demand for components, materials, and services related to concerned industry.

Researchers and Consultants: Provides data and analysis for academic research, consulting projects, and market studies.

Financial Institutions: Helps assess risks and opportunities associated with financing or investing in the concerned market.

Essentially, anyone involved in or considering involvement in the North America Medical Device Connectivity Market value chain can benefit from the information contained in a comprehensive market report.

Get Free Sample For North America Medical Device Connectivity Market

Get Free Sample For North America Medical Device Connectivity Market