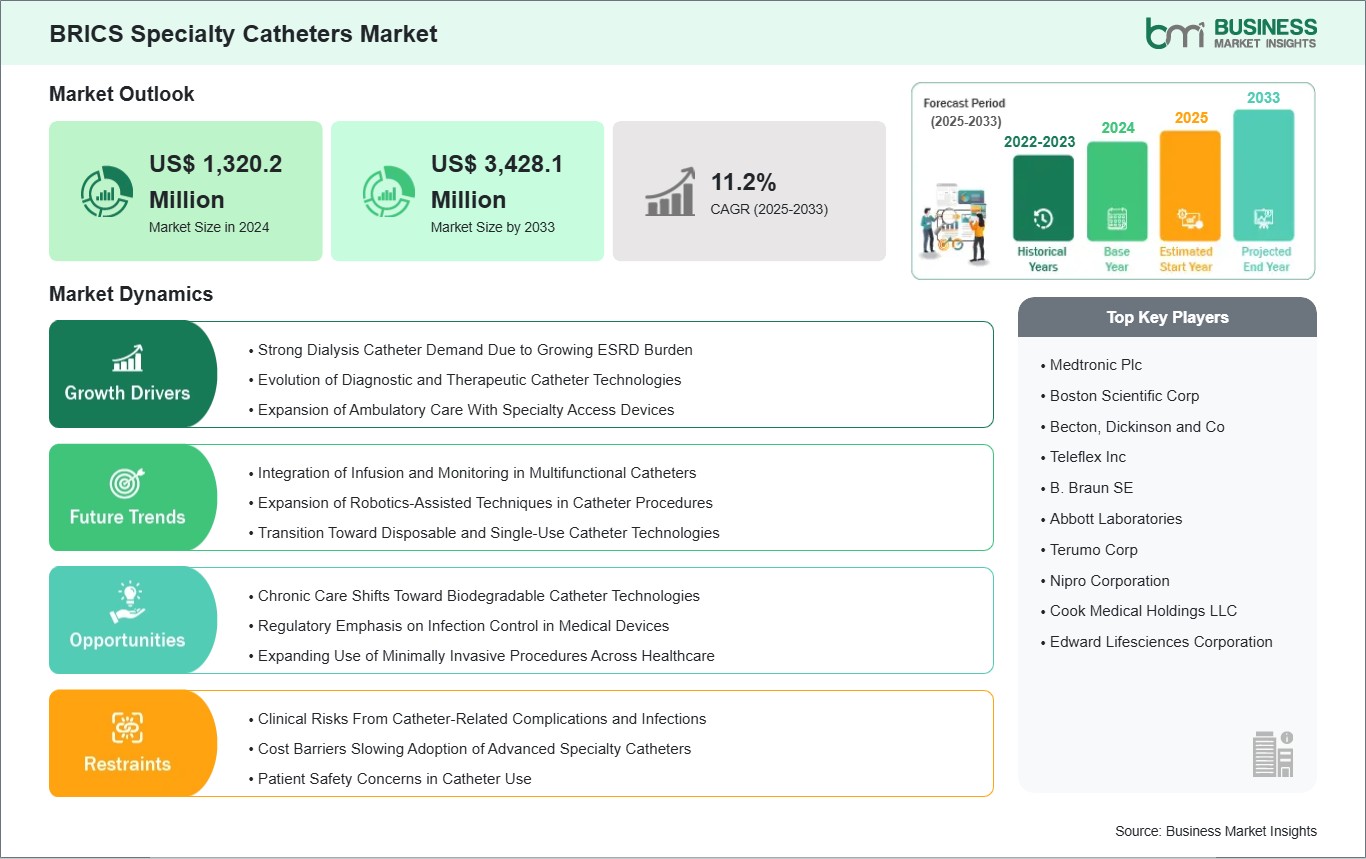

The BRICS Specialty Catheters market size is expected to reach US$ 3,428.1 million by 2033 from US$ 1,320.2 million in 2024. The market is estimated to register a CAGR of 11.2% from 2025 to 2033.

Executive Summary and BRICS Specialty Catheters Market Analysis:

The specialty catheters market in BRICS is experiencing significant growth driven by the high demand for dialysis catheters used by patients with end-stage renal disease (ESRD). The region is characterized by heightened clinical demand across critical care and interventional segments, underpinned by evolving hospital protocols and expanding procedural portfolios. In recent years, healthcare providers across Brazil, Russia, India, China, and South Africa have integrated advanced catheter technologies to support diagnostic precision, therapeutic efficacy, and procedural safety. This trend is driven by a confluence of demographic shifts—such as aging populations and increased prevalence of chronic conditions requiring vascular access—and systemic upgrades in health infrastructure. Unlike commodity catheter products, specialty catheters are differentiated by design complexity, performance attributes, and application specificity, enabling healthcare professionals to address nuanced clinical challenges across cardiology, oncology, nephrology, and intensive care units. From an analytical standpoint, adoption patterns reveal that technologically enhanced products, such as those with antimicrobial coatings and multi‑function lumens, are achieving preference over legacy designs due to their contribution to reduced complication rates and improved workflow efficiencies.

Competitive dynamics in the market are evolving, with multinational medical device companies deepening regional footprints through channel partnerships, localized service delivery, and targeted educational initiatives. Regulatory environments across BRICS nations vary, but harmonization efforts around quality standards and device approvals have resulted in shorter time‑to‑market for compliant innovations. Procurement strategies within private hospital networks emphasize value‑based outcomes, fostering procurement preferences for premium products that demonstrate measurable impact on clinical pathways. As a result, the analytical landscape highlights the strategic importance of specialty catheters in modern care delivery and the operational imperatives providers face in balancing cost efficiency with clinical performance.

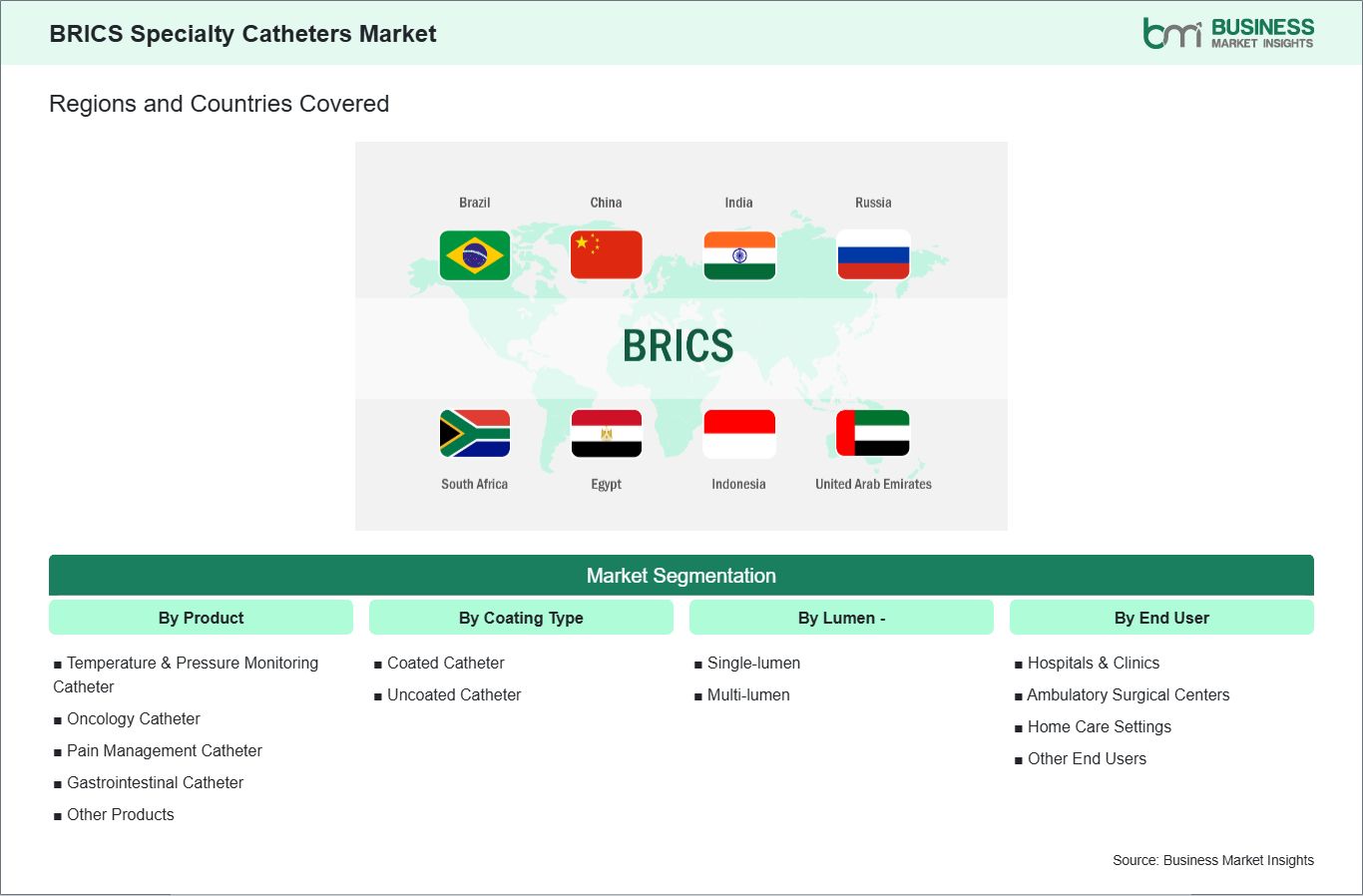

Key segments that contributed to the derivation of the BRICS Specialty Catheters market analysis are product, coating type, lumen, and end user.

By product, the specialty catheters market is segmented into temperature and pressure monitoring catheters, oncology catheters, pain management catheters, gastrointestinal catheters, and others. The temperature and pressure monitoring catheters segment dominated the market in 2024.

By coating type, the specialty catheters market is bifurcated into coated catheters and uncoated catheters. The coated catheters segment dominated the market in 2024.

By lumen, the market is divided into single-lumen and multi-lumen. The multi-lumen segment dominated the market in 2024.

By end user, the market is segmented into hospitals and clinics, ambulatory surgical centers, home care settings, and others. The hospitals and clinics segment dominated the market in 2024.

BRICS Specialty Catheters Market Drivers and Opportunities:

Evolution of Diagnostic and Therapeutic Catheter Options in Healthcare

Diagnostic catheters, including coronary angiography catheters, electrophysiology mapping catheters, and neurovascular diagnostic catheters, are widely used to detect and monitor cardiovascular, neurovascular, and urological disorders, which are prevalent across BRICS nations due to rising lifestyle-related diseases and aging populations. Healthcare providers are investing in advanced diagnostic tools, enabling early detection and timely intervention, which drives demand for high-precision catheters in these emerging markets.

Therapeutic catheters, such as angioplasty balloons, drug-eluting catheters, ablation catheters, and structural heart catheters, are being employed in minimally invasive procedures that reduce hospital stays, lower procedural risks, and improve patient outcomes. BRICS countries are seeing expansion of cardiac catheterization labs, interventional radiology centers, and tertiary care hospitals, especially in Brazil, China, India, and South Africa, providing the infrastructure necessary for catheter-based interventions. Training programs for interventional cardiologists, radiologists, and urologists are enhancing procedural volumes, supporting catheter demand.

Technological advancements, including catheters with improved flexibility, steerability, imaging compatibility, and drug-delivery capabilities, allow clinicians to perform complex diagnostic and therapeutic interventions safely. Combined with increasing patient awareness, expanding insurance coverage, and private healthcare investments, diagnostic and therapeutic catheters are becoming central to interventional care in BRICS nations, driving market growth.

Chronic Care Adoption of Biodegradable and Antimicrobial Catheters

Patients with conditions such as urinary retention, chronic kidney disease, or long-term vascular access requirements often need catheters for extended periods, which carry risks such as infection, encrustation, and biofilm formation. Biodegradable catheters, which naturally degrade within the body or after removal, reduce the need for repeated replacements, minimizing procedural risks and lowering healthcare costs.

Antimicrobial-coated catheters, treated with silver ions, antibiotics, or hydrophilic coatings, have proven effective in preventing catheter-associated infections (CAIs) — a concern even in tertiary hospitals across BRICS countries. Adoption is pronounced in urban teaching hospitals, specialized renal centers, and urology clinics, where long-term catheter use is common.

Increasing awareness among clinicians about the clinical and economic benefits of these catheters is accelerating their integration into treatment protocols. Governments and private hospital networks are supporting the use of advanced catheters through procurement programs, clinical guidelines, and partnerships with international medical device companies. With the prevalence of chronic diseases rising and patient safety gaining higher priority, biodegradable and antimicrobial catheters are expected to see steady adoption across BRICS nations, representing a public health advancement and a significant opportunity for specialty catheter manufacturers.

BRICS Specialty Catheters Market Size and Share Analysis:

The BRICS specialty catheters market demonstrates steady growth, with size and share analysis highlighting evolving trends and competitive dynamics among key players. The report further examines subsegments categorized within product, coating type, lumen, and end user, offering insights into their contribution to overall market performance.

By product, the temperature and pressure monitoring catheters subsegment dominated the market in 2024, driven by growing demand for accurate and continuous hemodynamic monitoring in critical care and complex surgical procedures.

Based on coating type, the coated catheters subsegment dominated the market in 2024, driven by increasing focus on reducing infection risks and improving biocompatibility and patient safety.

Based on lumen, the multi-lumen subsegment dominated the market in 2024, driven by the need for multitasking during interventions, enabling simultaneous infusion, monitoring, and therapy through a single access.

By end user, the hospitals and clinics subsegment dominated the market in 2024, driven by higher procedure volumes and the availability of advanced care infrastructure that requires extensive use of specialty catheters.

BRICS Specialty Catheters Market Report Coverage and Deliverables:

The "BRICS Specialty Catheters Market Size and Forecast (2025–2033)" report provides a detailed analysis of the market covering below areas:

BRICS Specialty Catheters market size and forecast at the regional and country levels for all the key market segments covered under the scope

BRICS Specialty Catheters market trends, as well as market dynamics such as drivers, restraints, and key opportunities

BRICS Specialty Catheters market analysis covering key market trends, regional framework, major players, regulations, and recent market developments

Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments for the BRICS Specialty Catheters market

Detailed company profiles, including SWOT analysis

The geographical scope of the BRICS Specialty Catheters market report is divided into: Russia, Brazil, South Africa, India, the UAE, and China. China held the largest share in 2024.

Within the BRICS cohort, each country presents a unique operational and strategic context that influences specialty catheter utilization and demand archetypes. China stands out for its scale and rapid integration of digitally enabled catheter technologies, supported by domestic manufacturing acceleration and policy incentives for innovation. Hospitals in China are leveraging advanced catheter platforms in cardiology and oncology, where procedure volumes have grown substantially. Brazil has seen increasing integration of advanced catheterization suites within private and public hospitals, driven by competitive pressures among premier healthcare providers to deliver differentiated cardiac and interventional services. Clinician networks in Brazil are notable for early adoption of next‑generation coated and multi‑lumen catheters, reflecting a strong procedural confidence and rigorous clinical evaluation culture.

In Russia, demand is concentrated in urban tertiary facilities where governmental reforms have prioritized modernization of diagnostic and critical care units; this has catalyzed procurement of specialty catheters aligned with standardized clinical pathways. India's landscape is marked by a dual demand stream: high‑end private care facilities adopting cutting‑edge solutions and a growing base of mid‑tier hospitals upgrading from basic catheter systems to reduce infection rates and improve clinical throughput. India's robust medical education ecosystem plays a role in shaping adoption curves. South Africa exhibits a demand profile influenced by public‑private healthcare dynamics and a strong emphasis on addressing infectious disease comorbidities through specialty catheter solutions that reduce hospital stay durations and complication margins. Across these nations, regulatory nuances, clinician training paradigms, and procurement strategies vary, but all reflect an overarching commitment to improving care standards through targeted adoption of specialty catheter technologies.

Get more information on this report

BRICS Specialty Catheters Market Research Report Guidance:

The report includes qualitative and quantitative data in the BRICS Specialty Catheters market across product, coating type, lumen, end user, and geography.

The report starts with the key takeaways (chapter 2), highlighting the key trends and outlook of the BRICS Specialty Catheters market.

Chapter 3 includes the research methodology of the study.

Chapter 4 further includes ecosystem analysis.

Chapter 5 highlights the major industry dynamics in the BRICS Specialty Catheters market, including factors that are driving the market, prevailing deterrents, potential opportunities, as well as future trends. Impact analysis of these drivers and restraints is also covered in this section.

Chapter 6 discusses the BRICS Specialty Catheters market scenario, in terms of historical market revenues, and forecast till the year 2033.

Chapters 7 to 11 cover the BRICS Specialty Catheters market segments by product, coating type, lumen, end user, and geography across Russia, Brazil, South Africa, India, the UAE, and China. They cover the market revenue, forecast, and factors driving the market.

Chapter 12 describes the competitive analysis along with the heat map analysis for the key players operating in the market.

Chapter 13 describes the industry landscape analysis. It provides detailed descriptions of business activities such as market initiatives, new developments, mergers, and joint ventures globally, along with a competitive landscape.

Chapter 14 provides detailed profiles of the major companies operating in the BRICS Specialty Catheters market. Companies have been profiled on the basis of their key facts, business descriptions, products, financial overview, SWOT analysis, and key developments.

Chapter 15, i.e., the appendix, is inclusive of a brief overview of the company, list of abbreviations, and disclaimer.

BRICS Specialty Catheters Market News and Key Development:

The Benelux Specialty Catheters market is evaluated by gathering qualitative and quantitative data post primary and secondary research, which includes important corporate publications, association data, and databases. A few of the key developments in the Benelux specialty catheters market are:

In August 2024, BIOTRONIK expanded its catheter portfolio with the launch of FlowGuide and Guidion Short guide extension catheters, designed to provide enhanced support in complex vascular procedures. These catheters improve deliverability and support during interventional treatments and are available across Europe, including Benelux countries, aiding physicians in advanced endovascular interventions.

In September 2023, BIOTRONIK announced the two‑year results from the BIOLUX P‑III BENELUX all‑comers registry evaluating its Passeo‑18 Lux drug‑coated balloon (DCB) catheter for isolated popliteal artery lesions. The registry enrolled patients across Belgium, the Netherlands, and Luxembourg, showing the safety and clinical effectiveness of the DCB‑only approach in a challenging vascular segment. The results were presented at CIRSE 2023, reinforcing clinical confidence in using this specialty catheter in lower‑limb vascular interventions.

Key Sources Referred:

World Health Organization (WHO)World Heart Federation (WHF)Organisation for Economic Cooperation and Development (OECD)The World Bank GroupWorldometerThe LancetInternational Bar AssociationInternational Trade Administration

Identical Market Reports with other Region/Countries

Krishna is a Market Research Analyst with over 4 years of experience across Life Sciences and Materials & Chemicals industries. He holds a Bachelor's degree in Pharmacy (B.Pharm.) and a Master's degree in Pharmaceutical Medicinal Chemistry (M.Pharm.). His expertise spans market intelligence, competitive benchmarking, market sizing and forecasting, primary and secondary research, and strategic consulting.

Krishna has successfully contributed to numerous syndicated and custom research engagements, delivering industry reports, market assessments, competitive analyses, and business proposals for clients across diverse sectors. With ..

Show More

Frequently Asked Questions

How big is the BRICS Specialty Catheters Market?

The BRICS Specialty Catheters Market is valued at US$ 1,320.2 Million in 2024, it is projected to reach US$ 3,428.1 Million by 2033.

What is the CAGR for BRICS Specialty Catheters Market by (2025 - 2033)?

As per our report BRICS Specialty Catheters Market, the market size is valued at US$ 1,320.2 Million in 2024, projecting it to reach US$ 3,428.1 Million by 2033. This translates to a CAGR of approximately 11.2% during the forecast period.

What segments are covered in this report?

The BRICS Specialty Catheters Market report typically cover these key segments-

End User (Hospitals & Clinics, Ambulatory Surgical Centers, Home Care Settings, Other End Users)

What is the historic period, base year, and forecast period taken for BRICS Specialty Catheters Market?

The historic period, base year, and forecast period can vary slightly depending on the specific market research report. However, for the BRICS Specialty Catheters Market report:

Historic Period : 2022-2023

Base Year : 2024

Forecast Period : 2025-2033

Who are the major players in BRICS Specialty Catheters Market?

The BRICS Specialty Catheters Market is populated by several key players, each contributing to its growth and innovation. Some of the major players include:

Medtronic Plc

Boston Scientific Corp

Becton, Dickinson and Co

Teleflex Inc

B. Braun SE

Abbott Laboratories

Terumo Corp

Nipro Corporation

Cook Medical Holdings LLC

Edward Lifesciences Corporation

Who should buy this report?

The BRICS Specialty Catheters Market report is valuable for diverse stakeholders, including:

Investors: Provides insights for investment decisions pertaining to market growth, companies, or industry insights. Helps assess market attractiveness and potential returns.

Industry Players: Offers competitive intelligence, market sizing, and trend analysis to inform strategic planning, product development, and sales strategies.

Suppliers and Manufacturers: Helps understand market demand for components, materials, and services related to concerned industry.

Researchers and Consultants: Provides data and analysis for academic research, consulting projects, and market studies.

Financial Institutions: Helps assess risks and opportunities associated with financing or investing in the concerned market.

Essentially, anyone involved in or considering involvement in the BRICS Specialty Catheters Market value chain can benefit from the information contained in a comprehensive market report.

Get Free Sample For BRICS Specialty Catheters Market

Get Free Sample For BRICS Specialty Catheters Market