2030년까지 북미 세포 및 유전자 치료 제조 서비스 시장 전망 - 지역 분석 - 유형별 [세포 치료(자가 및 동종) 및 유전자 치료(바이러스 및 비바이러스 벡터)], 적응증(암, 정형외과 및 기타), 응용 분야(임상 제조 및 상업 제조), 최종 사용자별 [제약 및 생명공학 회사 및 계약 연구 기관(CRO)]

No. of Pages: 110 | Report Code: BMIRE00029298 | Category: Life Sciences

No. of Pages: 110 | Report Code: BMIRE00029298 | Category: Life Sciences

세포 및 유전자 치료 제조는 복잡한 프로세스이므로 작업의 적절한 실행과 감독이 중요합니다. 세포 및 유전자 치료 제조업체에는 생물학 및 공정 공학을 알고 있는 자격을 갖춘 인력이 제한되어 있습니다. 더욱이 숙련된 팀의 경우 수동 및 개방형 제조 방법을 사용하여 첫 번째 임상 시험에 도달하려는 시도를 관리한 다음 보다 상업적으로 적합한 프로세스를 구축하는 것이 까다로울 수 있습니다. 따라서 이들 기업은 CDMO(계약 개발 및 제조 기관)와 협력하여 임상 연구 및 상업화 프로세스를 가속화하기로 결정했습니다. CDMO는 계약을 통해 세포 및 유전자 치료 회사에 제품 개발, 제조, 임상 시험 지원 및 상용화 서비스를 제공합니다. CDMO와의 파트너십을 통해 세포 및 유전자 치료 제조업체는 확장성, 시장 출시 속도, 간접비 없이 기술 전문 지식에 대한 액세스, 비용 효율성을 얻을 수 있습니다. ThermoGenesis는 2022년 4월 미국 캘리포니아에 CDMO 시설을 설립하여 T세포 수용체(TCR), 키메라 항원 수용체-T 세포(CAR-T 세포), 종양 분야의 전문 지식을 활용하여 세포 및 유전자 치료 제조업체에 CDMO 서비스를 제공합니다. -침윤백혈구(TIL), iPSC, 자연살해세포(NK), 중간엽줄기세포(MSC) 제조 세포 및 유전자 치료 제조를 CDMO에 아웃소싱하는 것은 제조업체에게 비용 효과적인 것으로 입증되었습니다. 따라서 성장하는 세포 및 유전자 치료 제조를 CDMO에 아웃소싱하는 것에 대한 선호도가 높아지면서 북미 세포 및 유전자 치료 제조 서비스 시장 성장이 촉진됩니다.

세포 및 유전자 치료법(CGT)은 해결되지 않은 치료적 필요성이 있는 심각하고 희귀한 질병으로 고통받는 환자를 치료합니다. CGT 제조는 인프라와 전문성 부족이 주요 제한 요소인 매우 복잡한 프로세스입니다. 중간체 및 최종 제품과 관련된 물류 문제도 기업의 CGT 제조 역량을 제한합니다. CGT 제조 과정에는 \'성분채집술\'을 통해 자가 세포를 추출한 후 전문 실험실로 보내고, 환자에게 투여하기 위해 다시 진료소로 보내는 과정이 포함되며, 이 모든 과정은 엄격한 품질 관리를 통해 수행되어야 합니다. 미국 식품의약국(USFDA)은 7개의 CGT 약물만을 승인했으며 신제품 파이프라인은 ~1,200개의 실험 치료법에 달합니다. 이들 중 절반은 2상 임상 시험에 있으며, Chemical & 엔지니어링 뉴스(Engineering News) 보고서 2022. 2022년 3월 31일, CELL Technologies Inc.는 환자가 증거 기반 및 규제 승인 줄기세포 시술에 접근할 수 있도록 돕기 위해 캐나다 보건부(Health Canada)의 승인을 위해 통증 및 관절염에 대한 줄기세포 프로그램의 임상 데이터 제출을 발표했습니다. 캐나다 전역. 따라서 위에서 언급한 요인은 예측 기간 동안 세포 및 유전자 치료 제조 서비스 시장 성장을 촉진할 것으로 예상됩니다. 따라서 위에서 언급한 요인들은 북미 세포 및 유전자 치료 제조 서비스 시장의 성장에 책임이 있습니다.

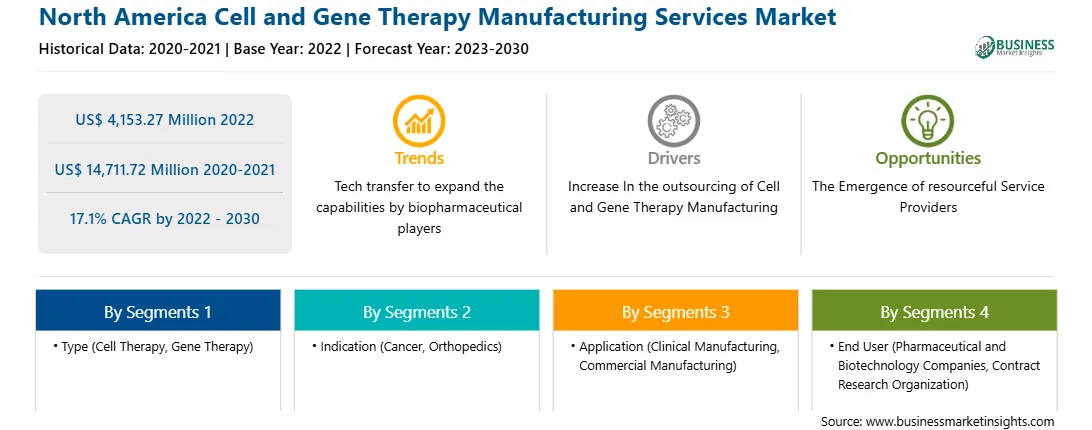

북미 세포 및 유전자 치료 제조 서비스 시장은 세분화되어 있습니다. 유형, 적응증, 용도, 최종 사용자 및 국가로 분류됩니다.

유형에 따라 북미 세포 및 유전자 치료 제조 서비스 시장은 세포 치료와 유전자 치료로 구분됩니다. 2022년에는 세포 치료 부문이 북미 세포 및 유전자 치료 제조 서비스 시장에서 더 큰 점유율을 기록했습니다. 세포치료 부문은 자가유래와 동종유래로 더 세분화됩니다. 유전자 치료 부문은 바이러스 벡터와 비바이러스 벡터로 더 세분화됩니다.

적응증에 따라 북미 세포 및 유전자 치료 제조 서비스 시장은 암, 정형외과 등으로 분류됩니다. 2022년 암 부문은 북미 세포 및 유전자 치료 제조 서비스 시장에서 가장 큰 점유율을 기록했습니다.

응용 프로그램을 기준으로 북미 세포 및 유전자 치료 제조 서비스 시장은 임상 제조 및 상업 시장으로 분류됩니다. 조작. 2022년에는 상업용 제조 부문이 북미 세포 및 유전자 치료 제조 서비스 시장에서 가장 큰 점유율을 기록했습니다.

최종 사용자를 기준으로 북미 세포 및 유전자 치료 제조 서비스 시장은 제약 및 유전자 치료 제조 서비스 시장으로 구분됩니다. 생명공학 기업 및 임상시험수탁기관(CRO). 2022년에는 제약 및 생명공학 기업 부문이 북미 세포 및 유전자 치료 제조 서비스 시장에서 더 큰 점유율을 기록했습니다.

국가를 기준으로 북미 세포 및 유전자 치료 제조 서비스 시장은 다음과 같이 분류됩니다. 미국, 캐나다, 멕시코. 2022년 미국은 북미 세포 및 유전자 치료 제조 서비스 시장에서 가장 큰 점유율을 기록했습니다.

Catalent Inc, Charles River Laboratories International Inc, FUJIFILM Holdings Corp, Lonza Group AG, Merck KgaA, National Resilience Inc, Nikon Corp, Oxford BioMedica Plc, Takara Bio Inc, Thermo Fisher Scientific Inc 및 WuXi AppTec Co Ltd는 북미 세포 및 유전자 치료 제조 서비스 시장에서 활동하는 선도적인 회사입니다.

Strategic insights for North America Cell and Gene Therapy Manufacturing Services involve closely monitoring industry trends, consumer behaviours, and competitor actions to identify opportunities for growth. By leveraging data analytics, businesses can anticipate market shifts and make informed decisions that align with evolving customer needs. Understanding these dynamics helps companies adjust their strategies proactively, enhance customer engagement, and strengthen their competitive edge. Building strong relationships with stakeholders and staying agile in response to changes ensures long-term success in any market.

| Report Attribute | Details |

|---|---|

| Market size in 2022 | US$ 4,153.27 Million |

| Market Size by 2030 | US$ 14,711.72 Million |

| Global CAGR (2022 - 2030) | 17.1% |

| Historical Data | 2020-2021 |

| Forecast period | 2023-2030 |

| Segments Covered |

By 유형

|

| Regions and Countries Covered | 북미

|

| Market leaders and key company profiles |

The regional scope of North America Cell and Gene Therapy Manufacturing Services refers to the geographical area in which a business operates and competes. Understanding regional nuances, such as local consumer preferences, economic conditions, and regulatory environments, is crucial for tailoring strategies to specific markets. Businesses can expand their reach by identifying underserved regions or adapting their offerings to meet regional demands. A clear regional focus allows for more effective resource allocation, targeted marketing, and better positioning against local competitors, ultimately driving growth in those specific areas.

1. Catalent Inc

2. Charles River Laboratories International Inc

3. FUJIFILM Holdings Corp

4. Lonza Group AG

5. Merck KgaA

6. National Resilience Inc

7. Nikon Corp

8. Oxford BioMedica Plc

9. Takara Bio Inc

10. Thermo Fisher Scientific Inc

11. WuXi AppTec Co Ltd?

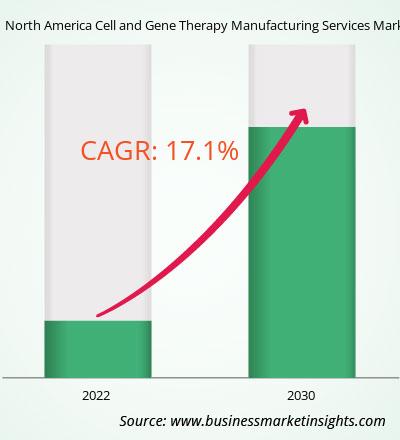

The North America Cell and Gene Therapy Manufacturing Services Market is valued at US$ 4,153.27 Million in 2022, it is projected to reach US$ 14,711.72 Million by 2030.

As per our report North America Cell and Gene Therapy Manufacturing Services Market, the market size is valued at US$ 4,153.27 Million in 2022, projecting it to reach US$ 14,711.72 Million by 2030. This translates to a CAGR of approximately 17.1% during the forecast period.

The North America Cell and Gene Therapy Manufacturing Services Market report typically cover these key segments-

The historic period, base year, and forecast period can vary slightly depending on the specific market research report. However, for the North America Cell and Gene Therapy Manufacturing Services Market report:

The North America Cell and Gene Therapy Manufacturing Services Market is populated by several key players, each contributing to its growth and innovation. Some of the major players include:

The North America Cell and Gene Therapy Manufacturing Services Market report is valuable for diverse stakeholders, including:

Essentially, anyone involved in or considering involvement in the North America Cell and Gene Therapy Manufacturing Services Market value chain can benefit from the information contained in a comprehensive market report.

E 1803, Panchshil Towers, Vagholi, Haveli, Pune- 412207, Maharashtra, India

US:+16467917070

sales@businessmarketinsights.com

Get Free Sample For North America Cell and Gene Therapy Manufacturing Services Market

Get Free Sample For North America Cell and Gene Therapy Manufacturing Services Market