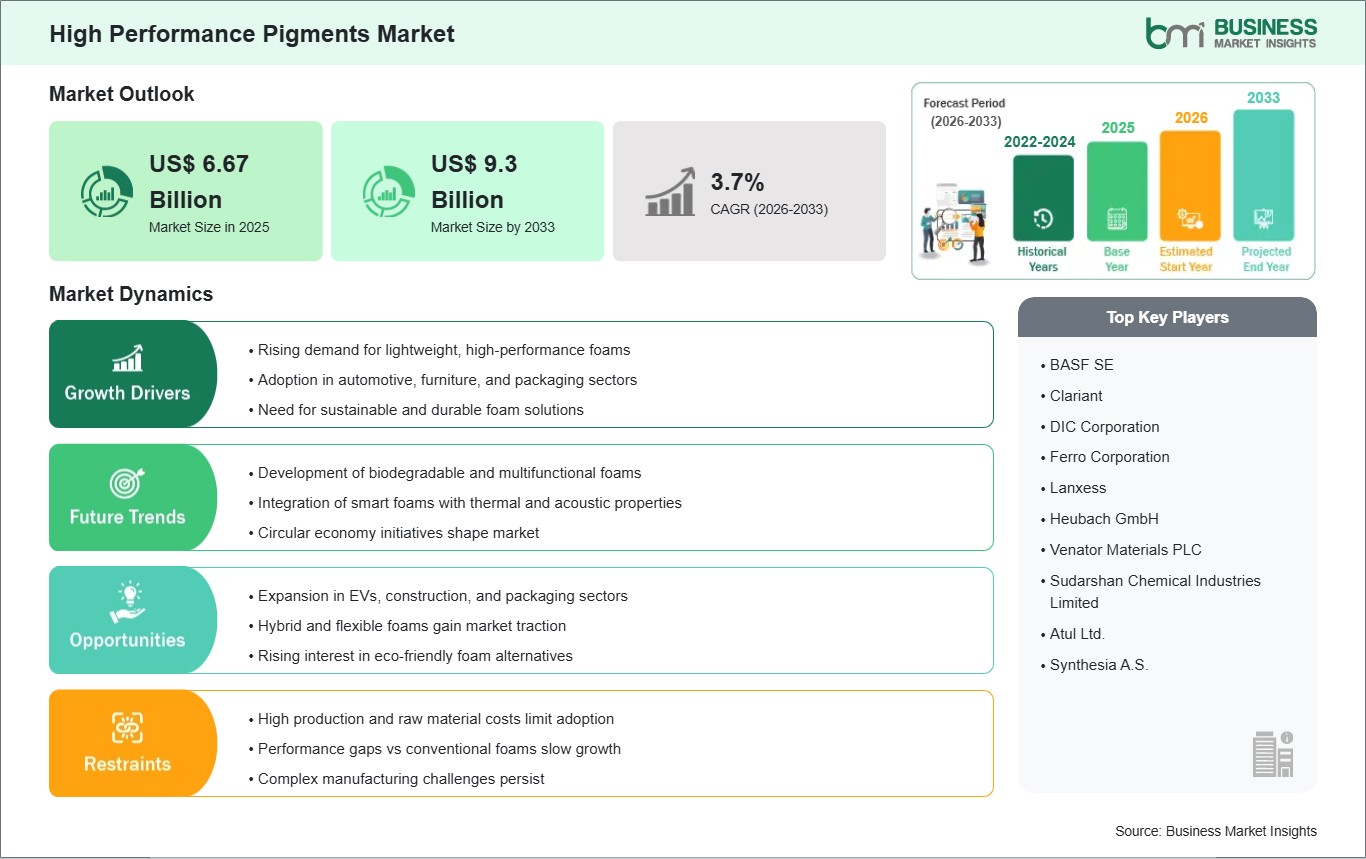

The High Performance Pigments Market size is expected to reach US$ 9.3 Billion by 2033 from US$ 6.67 Billion in 2025. The market is estimated to record a CAGR of 4.24% from 2026 to 2033.

Executive Summary and Global Market Analysis:

High Performance Pigments (HPPs) represent a specialized class of colorants engineered to provide superior durability, heat stability, and chemical resistance compared to conventional organic and inorganic pigments. These materials are indispensable in environments where extreme lightfastness and weatherability are required, such as in high-end automotive finishes, industrial protective coatings, and outdoor plastics. Unlike standard pigments, HPPs maintain their color integrity and gloss under intense UV exposure and thermal stress, making them the primary choice for mission-critical aesthetic and functional applications. The market is currently driven by the rapid global shift toward high-quality aesthetic finishes in the automotive sector and the rising demand for long-lasting architectural materials in modern urban infrastructure.

However, the market faces significant restraints, primarily stemming from the high manufacturing complexity and the steep cost of specialized raw materials. The synthesis of HPPs often involves multi-step chemical processes that are energy-intensive and require stringent quality control to ensure batch-to-batch consistency. Furthermore, increasing regulatory scrutiny under frameworks like REACH and the EPA regarding the use of heavy metals and hazardous solvents adds a layer of compliance cost and technical difficulty for manufacturers. These economic and regulatory hurdles can limit the adoption of HPPs in price-sensitive segments, where lower-cost alternatives are often prioritized despite their inferior performance profiles.

Despite these challenges, lucrative opportunities remain prevalent, particularly in the development of sustainable and bio-based pigment formulations. As global industries pivot toward a circular economy, there is a surging demand for "green" HPPs that offer a reduced carbon footprint without compromising on performance. Additionally, the integration of HPPs into smart coatings, capable of reflecting near-infrared (NIR) light to manage solar heat or providing antimicrobial properties, opens new growth avenues in the aerospace, construction, and healthcare sectors. The ongoing digitalization of color matching and the expansion of the electric vehicle (EV) market also provide a fertile ground for manufacturers to introduce innovative, application-specific pigment solutions that align with the next generation of high-tech industrial requirements.

High Performance Pigments Market - Strategic Insights:

Get more information on this report

High Performance Pigments Market Segmentation Analysis:

Key segments that contributed to the derivation of the High Performance Pigments market analysis are type, application, and end-use industry.

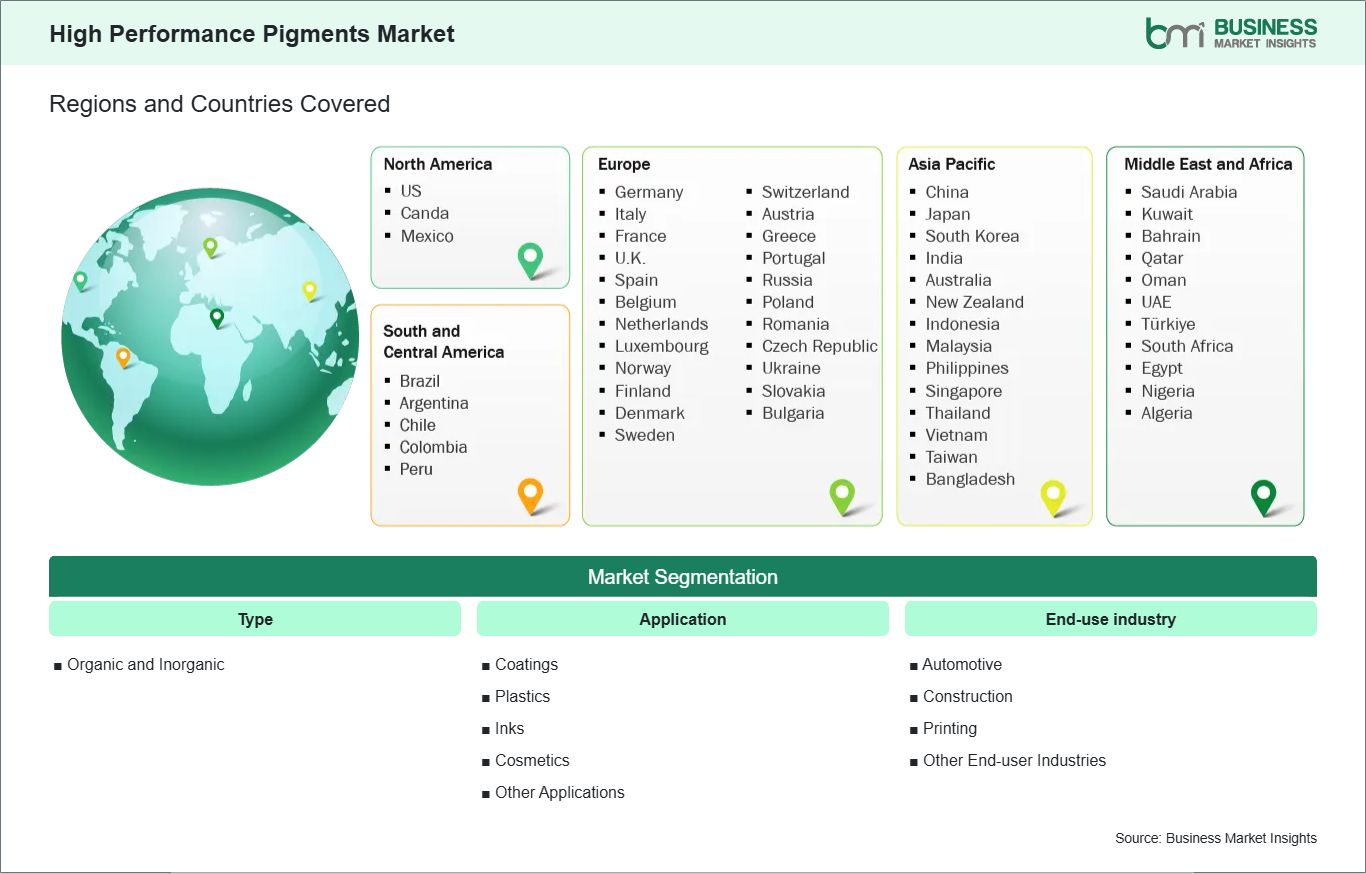

By Type, the market is segmented into Organic and Inorganic.

By Application, the market is divided into Coatings, Plastics, Inks, Cosmetics, and Others.

By End-use industry, the market is categorized into Automotive, Construction, Printing, and Others.

High Performance Pigments Market Drivers and Opportunities:

Surge in Automotive OEM Demand for Advanced Color Aesthetic

The global automotive Original Equipment Manufacturer (OEM) sector serves as a primary driver for the high-performance pigments market, dictated by the increasing consumer appetite for premium finishes and the technical demands of next-generation vehicle architectures. As automotive designs evolve toward electric and autonomous platforms, branding is increasingly tied to "signature" colors, high-chroma reds, deep blues, and sophisticated metallic pearls that require pigments with exceptional tinting strength and saturation. Unlike standard colorants, HPPs such as quinacridones and perylenes provide the necessary chemical resistance to withstand environmental pollutants and the thermal stability required for high-temperature curing processes in modern paint shops.

Furthermore, the rise of Advanced Driver Assistance Systems (ADAS) has transformed exterior coatings from purely aesthetic layers into functional components. New HPP formulations are being engineered to be "radar-transparent" or "LiDAR-reflective," ensuring that the dark or metallic pigments used on a vehicle's body do not interfere with the sensors used for autonomous navigation. This convergence of high-end aesthetics and sensor-compatibility necessitates a shift toward advanced inorganic and organic pigments that maintain color integrity under intense UV exposure without degrading the vehicle's safety hardware. Consequently, OEMs are intensifying their partnerships with pigment manufacturers to develop proprietary, high-performance coating systems that offer both a competitive visual edge and long-term structural durability.

Expansion into Sustainable and Bio-Based Pigment Technologies

The transition toward a circular economy represents the most significant growth opportunity for the high-performance pigments industry, driven by global regulatory shifts and the "green chemistry" movement. Traditional pigment manufacturing often relies on petroleum-based feedstocks and heavy metals like cadmium or lead, which face increasing restrictions under frameworks such as the EU's REACH and the US EPA's TSCA. This has created a lucrative opening for bio-based HPPs derived from renewable biomass, agricultural waste, or microbial fermentation. These sustainable alternatives are designed to offer a "drop-in" replacement for synthetic pigments, matching their performance in terms of lightfastness and heat stability while significantly reducing the overall carbon footprint of the end-product.

Innovation in this space is particularly robust within the packaging and consumer electronics sectors, where brands are eager to market VOC-free and biodegradable products to eco-conscious consumers. For example, recent breakthroughs in "carbon black" alternatives derived from wood waste (bio-char) allow manufacturers to achieve deep, high-performance blacks without the environmental cost of traditional furnace-black production. Additionally, the integration of bio-pigments into waterborne coating systems, which are naturally lower in solvent content, positions HPP manufacturers to lead the industry's shift away from hazardous chemical dependencies. As production scales and the cost-parity with synthetic HPPs improves by 2033, companies that have invested in bio-based IP will be uniquely positioned to capture market share in a regulatory landscape that increasingly penalizes carbon-intensive materials.

High Performance Pigments Market Size and Share Analysis:

The High Performance Pigments market demonstrates steady growth, with size and share analysis revealing evolving trends and competitive positioning among key players. The report further examines subsegments categorized within type, application, and end-use industry, offering insights into their contribution to overall market performance.

Within the type category, the organic sub-segment is gaining substantial traction due to its vibrant hue ranges and superior tinting strength, which are highly valued in the decorative and automotive sectors.

Regarding applications, the coatings sub-segment continues to represent the most significant portion of the market, fueled by the necessity for weather-resistant finishes in high-rise architectural projects.

In terms of end-use industry, the automotive sub-sector remains a dominant force as manufacturers increasingly adopt high-performance effect pigments to enhance vehicle aesthetics and durability, ensuring that the market for specialized colorants remains resilient amid broader industrial shifts toward high-tech and sustainable mobility.

High Performance Pigments Market Report Highlights:

Australia, China, India, Japan, South Korea, Indonesia, Malaysia, Philippines, Singapore, Thailand, Vietnam, Bangladesh, New Zealand, Taiwan

South and Central America

Brazil, Argentina, Peru, Chile, Colombia

Middle East and Africa

Bahrain, Kuwait, Oman, Qatar, Saudi Arabia, United Arab Emirates, Turkiye, South Africa, Egypt, Algeria, Nigeria

Market leaders and key company profiles

BASF SE

Clariant

DIC Corporation

Ferro Corporation

Lanxess

Heubach GmbH

Venator Materials PLC

Sudarshan Chemical Industries Limited

Atul Ltd.

Synthesia A.S.

Get more information on this report

High Performance Pigments Market Report Coverage and Deliverables:

The "High Performance Pigments Market Size and Forecast (2022 - 2033)" report provides a detailed analysis of the market covering below areas:

High Performance Pigments market size and forecast at global, regional, and country levels for all the key market segments covered under the scope

High Performance Pigments market trends, as well as market dynamics such as drivers, restraints, and key opportunities

High Performance Pigments market analysis covering key market trends, global and regional framework, major players, regulations, and recent market developments

Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments for the High Performance Pigments market

Detailed company profiles, including SWOT analysis

High Performance Pigments Market Geographic Insights:

The geographical scope of the High Performance Pigments market report is divided into five regions: North America, Asia Pacific, Europe, the Middle East &Africa, and South &Central America.

In North America, market activity is driven by a sophisticated industrial base where high-speed signal integrity and extreme environmental resilience are paramount for aerospace, defense, and premium automotive sectors. The regional focus remains on the integration of smart pigments that complement advanced sensor technologies and autonomous vehicle hardware. Europe maintains its position as a global leader in regulatory excellence and green chemistry, where stringent environmental mandates and a profound shift toward sustainable, non-toxic pigment formulations for high-end architectural and automotive finishes shape the market. This commitment to eco-friendly innovation aligns with a broad regional preference for high-fidelity, light-stable materials that meet long-term sustainability goals.

The Asia Pacific region serves as a central engine for the market, characterized by rapid urbanization and a robust manufacturing ecosystem that necessitates large-scale consumption of durable colorants across the construction and electronics industries. Regional development is fueled by the expansion of automotive production hubs and an increasing focus on upgrading local manufacturing capabilities to produce higher-value, application-specific pigments. In the Middle East &Africa, the market is expanding through massive infrastructure investments and smart city initiatives that require pigments capable of withstanding intense thermal stress and solar radiation. Meanwhile, South &Central America are witnessing steady progress as regional industrial sectors modernize, driving the adoption of high-performance finishes to enhance the quality and lifespan of domestic consumer goods and industrial equipment. This diversified growth ensures a resilient global market as regions align their digital and industrial frameworks with high-performance standards.

Get more information on this report

High Performance Pigments Market Research Report Guidance:

The report includes qualitative and quantitative data in the High Performance Pigments market across type, application, end-use industry, and geography.

The report starts with the key takeaways (chapter 2), highlighting the key trends and outlook of the High Performance Pigments market.

Chapter 3 includes the research methodology of the study.

Chapter 4 further includes ecosystem analysis.

Chapter 5 highlights the major industry dynamics in the High Performance Pigments market, including factors that are driving the market, prevailing deterrents, potential opportunities, as well as future trends. Impact analysis of these drivers and restraints is also covered in this section.

Chapter 6 discusses the High Performance Pigments market scenario, in terms of historical market revenues, and forecast till the year 2033.

Chapters 7 to 10 cover High Performance Pigments market segments by type, application, end-use industry, and geography across North America, Europe, Asia Pacific, the Middle East and Africa, and South and Central America. They cover the market revenue, forecast, and factors driving the market.

Chapter 11 describes the competitive analysis along with the heat map analysis for the key players operating in the market.

Chapter 12 describes the industry landscape analysis. It provides detailed descriptions of business activities such as market initiatives, new developments, mergers, and joint ventures globally, along with a competitive landscape.

Chapter 13 provides detailed profiles of the major companies operating in the High Performance Pigments market. Companies have been profiled on the basis of their key facts, business descriptions, products and services, financial overview, SWOT analysis, and key developments.

Chapter 14, i.e., the appendix, is inclusive of a brief overview of the company, a list of abbreviations, and a disclaimer.

High Performance Pigments Market News and Key Development:

The High Performance Pigments market is evaluated by gathering qualitative and quantitative data post primary and secondary research, which includes important corporate publications, association data, and databases. A few of the key developments in the High Performance Pigments market are:

In November 2025, DIC Corporation and its subsidiary Sun Chemical introduced several world premieres within their High Performance Pigments portfolio at CHINACOAT 2025. Among the highlights, they debuted the Paliocrom Brilliant Ruby L 3558, an intense bluish-red aluminum effect pigment specifically engineered for modern automotive and industrial coatings.

In November 2025, BASF officially commissioned its new high-performance dispersant production line at the Jiangbei New Material Technology Park in Nanjing, China. This strategic investment enabled the local manufacturing of advanced dispersants utilizing Controlled Free Radical Polymerization (CFRP) technology, which significantly improved the dispersion and stability of High Performance Pigments in industrial and automotive coatings. The resulting increase in global capacity bolstered supply reliability and flexibility, complementing the company's existing operations at its site in Heerenveen, the Netherlands.

Key Sources Referred:

World Bank - Global Trade IndicatorsWorld Trade Organization (WTO)International Monetary Fund (IMF)International Trade Administration (ITA)Company websiteCompany annual reportsCompany investor presentations

The List of Companies - High Performance Pigments Market

BASF SE

Clariant

DIC Corporation

Ferro Corporation

Lanxess

Heubach GmbH

Venator Materials PLC

Sudarshan Chemical Industries Limited

Atul Ltd.

Synthesia A.S.

Frequently Asked Questions

How big is the High Performance Pigments Market?

The High Performance Pigments Market is valued at US$ 6.67 Billion in 2025, it is projected to reach US$ 9.3 Billion by 2033.

What is the CAGR for High Performance Pigments Market by (2026 - 2033)?

As per our report High Performance Pigments Market, the market size is valued at US$ 6.67 Billion in 2025, projecting it to reach US$ 9.3 Billion by 2033. This translates to a CAGR of approximately 4.24% during the forecast period.

What segments are covered in this report?

The High Performance Pigments Market report typically cover these key segments-

Type (Organic and Inorganic)

Application (Coatings, Plastics, Inks, Cosmetics, and Other Applications)

End-use industry (Automotive, Construction, Printing, and Other End-user Industries)

What is the historic period, base year, and forecast period taken for High Performance Pigments Market?

The historic period, base year, and forecast period can vary slightly depending on the specific market research report. However, for the High Performance Pigments Market report:

Historic Period : 2022-2024

Base Year : 2025

Forecast Period : 2026-2033

Who are the major players in High Performance Pigments Market?

The High Performance Pigments Market is populated by several key players, each contributing to its growth and innovation. Some of the major players include:

BASF SE

Clariant

DIC Corporation

Ferro Corporation

Lanxess

Heubach GmbH

Venator Materials PLC

Sudarshan Chemical Industries Limited

Atul Ltd.

Synthesia A.S.

Who should buy this report?

The High Performance Pigments Market report is valuable for diverse stakeholders, including:

Investors: Provides insights for investment decisions pertaining to market growth, companies, or industry insights. Helps assess market attractiveness and potential returns.

Industry Players: Offers competitive intelligence, market sizing, and trend analysis to inform strategic planning, product development, and sales strategies.

Suppliers and Manufacturers: Helps understand market demand for components, materials, and services related to concerned industry.

Researchers and Consultants: Provides data and analysis for academic research, consulting projects, and market studies.

Financial Institutions: Helps assess risks and opportunities associated with financing or investing in the concerned market.

Essentially, anyone involved in or considering involvement in the High Performance Pigments Market value chain can benefit from the information contained in a comprehensive market report.

Get Free Sample For High Performance Pigments Market

Get Free Sample For High Performance Pigments Market