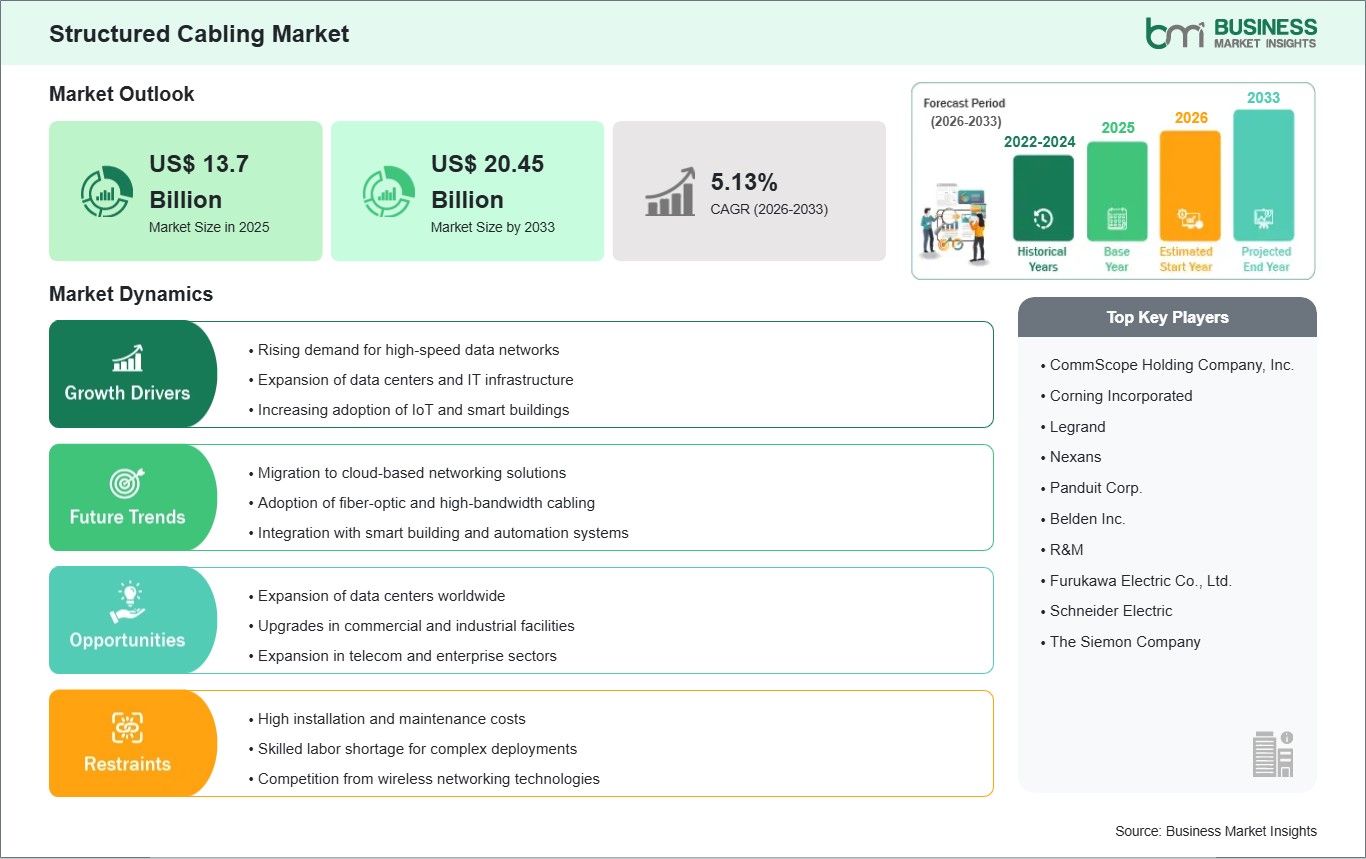

The Structured Cabling Market size is expected to reach US$ 20.45 billion by 2033 from US$ 13.7 billion in 2025. The market is estimated to record a CAGR of 5.13% from 2026 to 2033.

Executive Summary and Global Market Analysis:

The global structured cabling market is witnessing significant growth as enterprises, data centers, and telecom providers seek reliable, high-speed, and scalable network infrastructure. Structured cabling systems provide standardized pathways and components for data, voice, and video communications, enabling streamlined installation, easier maintenance, and enhanced network performance. Increasing demand for high-bandwidth applications, cloud computing, IoT connectivity, and 5G deployment is driving the adoption of structured cabling across commercial, industrial, and institutional sectors. Technological advancements are shaping market trends, with innovations in high-speed fiber optic cabling, Category 6A/7 twisted pair solutions, and modular connectivity enabling improved data transfer rates, reduced latency, and future-proof infrastructure. The adoption of intelligent cabling management systems and integrated monitoring tools ensures optimized network performance, simplified troubleshooting, and reduced operational downtime.

Additionally, hybrid copper-fiber systems are gaining traction to balance cost efficiency with performance requirements. The market is further supported by global digital transformation initiatives, smart building development, and expansion of enterprise networks. Growing demand for robust and flexible cabling solutions in data-intensive applications, including cloud computing, AI, and multimedia streaming, is driving continuous innovation. Overall, the structured cabling market is evolving toward high-performance, scalable, and sustainable infrastructure solutions that support modern communication and digital business operations.

Structured Cabling Market - Strategic Insights:

Get more information on this report

Structured Cabling Market Segmentation Analysis:

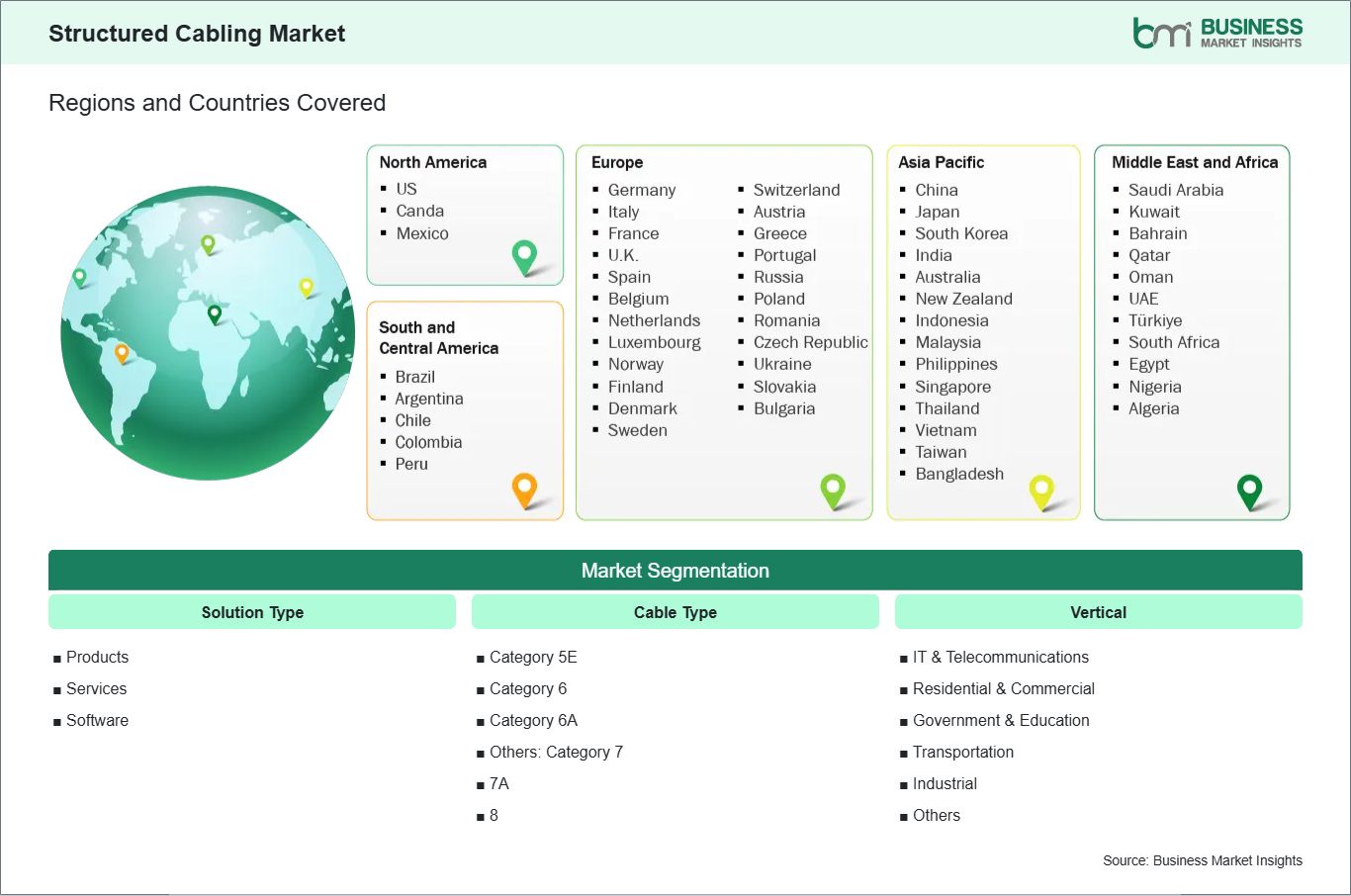

Key segments that contributed to the derivation of the structured cabling market analysis are solution type, cable type, and vertical.

Solution Type, the structured cabling market is segmented into products, services, and software. The products segment dominated the market in 2025.

Cable Type, the structured cabling market is categorized into category 5e, category 6, category 6a, and others. The category 6 segment dominated the market in 2025.

Vertical, the structured cabling market is classified into IT & telecommunications, residential & commercial, government & education, transportation, industrial, and others. The IT & telecommunications segment dominated the market in 2025.

Structured Cabling Market Drivers and Opportunities:

Rising demand for high-speed data networks

The global structured cabling market is driven by the escalating demand for high‑speed data networks across commercial, industrial, and enterprise environments. As digital transformation accelerates, organizations require cabling infrastructures capable of supporting higher bandwidths for applications such as cloud computing, unified communications, and real‑time data transfer. High‑performance cabling systems like Category 6A, Category 8, and fiber optics are increasingly replacing legacy copper cabling to deliver superior throughput, reduced latency, and enhanced network reliability. This transition is fundamental to supporting modern networking standards. In addition, the proliferation of bandwidth‑intensive applications such as video conferencing, virtualized desktops, and big data analytics has intensified the need for structured cabling systems that can scale effectively. End users are prioritizing cabling solutions that future‑proof network architectures, allowing seamless integration of emerging technologies like Wi‑Fi 6/6E and beyond. This has prompted structured cabling manufacturers to innovate modular and flexible designs that accommodate rapid upgrades without major overhauls. Furthermore, the rise of connected devices from IoT sensors to high‑definition surveillance systems places additional pressure on network infrastructure. Structured cabling serves as the backbone for these expanding networks, ensuring consistent performance as device density grows. With enterprises and service providers alike upgrading network backbones, the market for advanced cabling systems continues to expand on a global scale.

Expansion of data centers worldwide

The expansion of data centers worldwide is a key catalyst for structured cabling market growth. As demand for cloud services, edge computing, and hyperscale data processing rises, new facilities are being deployed with extensive cabling infrastructures to support high‑density interconnections. Structured cabling systems play a pivotal role in data center architecture by facilitating efficient connectivity between servers, storage arrays, and networking equipment. High‑capacity fiber cabling solutions are particularly vital to enable rapid data throughput and low latency within these environments. Beyond new builds, existing data centers are undergoing significant upgrades to accommodate increased compute loads and evolving network topologies. Modern workloads related to artificial intelligence, machine learning, and large‑scale virtualization require cabling solutions that can handle substantial traffic spikes while maintaining signal integrity. Structured cabling systems, with their standardized layouts and scalable designs, are integral to achieving these performance benchmarks and ensuring operational resilience. In addition, the trend toward modular and prefabricated data center designs underscores the importance of structured cabling. These approaches demand cabling solutions that are both flexible and easy to deploy, allowing rapid scaling of capacity without disrupting ongoing operations. As digital services proliferate and network demands intensify, structured cabling remains central to supporting the global data center ecosystem’s expansion and long‑term growth.

Structured Cabling Market Size and Share Analysis:

The Structured Cabling Market demonstrates steady growth, with size and share analysis highlighting evolving trends and competitive dynamics among key players. The report examines subsegments categorized within solution type, cable type, and vertical, offering insights into their contribution to overall market performance.

Solution Type, the products subsegment dominated the market in 2025, driven by increasing installations of cables, patch panels, communication outlets, and racks across enterprise and commercial networks.

Based on Cable Type, the category 6 subsegment dominated the market in 2025, driven by its optimal combination of bandwidth support, reliability, and cost-effectiveness for modern IT and telecom networks.

In terms of Vertical, the IT & telecommunications subsegment dominated the market in 2025, driven by rapid growth in data centers, cloud adoption, and enterprise networking requirements worldwide.

Australia, China, India, Japan, South Korea, Indonesia, Malaysia, Philippines, Singapore, Thailand, Vietnam, Bangladesh, New Zealand, Taiwan

South and Central America

Brazil, Argentina, Peru, Chile, Colombia

Middle East and Africa

Bahrain, Kuwait, Oman, Qatar, Saudi Arabia, United Arab Emirates, Turkiye, South Africa, Egypt, Algeria, Nigeria

Market leaders and key company profiles

CommScope Holding Company, Inc.

Corning Incorporated

Legrand

Nexans

Panduit Corp.

Belden Inc.

R&M

Furukawa Electric Co., Ltd.

Schneider Electric

The Siemon Company

Get more information on this report

Structured Cabling Market Report Coverage and Deliverables:

The "Structured Cabling Market Size and Forecast (2022 - 2033)" report provides a detailed analysis of the market covering below areas:

Structured Cabling Market size and forecast at global, regional, and country levels for all the key market segments covered under the scope

Structured Cabling Market trends, as well as drivers, restraints, and opportunities

Structured Cabling Market analysis covering key trends, global and regional framework, major players, regulations, and recent developments

Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments for the Structured Cabling Market

Detailed company profiles, including SWOT analysis

Structured Cabling Market Geographic Insights:

The geographical scope of the Structured Cabling Market report is divided into North America, Asia Pacific, Europe, Middle East & Africa, and South & Central America. North America held the largest share in 2025.

Regional adoption of structured cabling systems is driven by enterprise network expansion, digital infrastructure development, and technology investments. North America dominates the market due to extensive data center infrastructure, high cloud adoption, and demand for high-speed enterprise networks. The United States and Canada lead in deploying advanced fiber optic cabling, modular patch panels, and intelligent cable management solutions to support enterprise, government, and telecom applications. Asia Pacific is a high-growth region, fueled by rapid urbanization, industrial digitalization, and increasing adoption of smart city projects.

Countries such as China, India, Japan, and South Korea are implementing structured cabling in corporate offices, data centers, and 5G network expansions to enable high-speed, reliable connectivity. Europe emphasizes compliance with standardized network protocols, energy efficiency, and high-performance infrastructure.

Germany, France, and the United Kingdom are integrating fiber optic and hybrid cabling systems for enterprise and industrial networks, supporting digital transformation and IoT deployment.

Middle East & Africa is gradually adopting structured cabling in commercial, industrial, and educational sectors, particularly in the UAE, Saudi Arabia, and South Africa, to strengthen digital infrastructure.

South & Central America is expanding structured cabling deployment in corporate, telecom, and government networks, with Brazil, Mexico, and Chile driving adoption to enhance connectivity, network reliability, and scalability across emerging markets.

Get more information on this report

Structured Cabling Market Research Report Guidance:

The report includes qualitative and quantitative data in the Structured Cabling Market across solution type, cable type, vertical and geography.

The report starts with the key takeaways (chapter 2), highlighting key trends and outlook of the Structured Cabling Market.

Chapter 3 focuses on the research methodology of the study.

Chapter 4 includes ecosystem analysis.

Chapter 5 highlights the major industry dynamics in the Structured Cabling Market, including factors that are driving the market, prevailing deterrents, potential opportunities, as well as future trends. Impact analysis of these drivers and restraints is also covered in this section.

Chapter 6 discusses the Structured Cabling Market scenario, in terms of historical market revenues, and forecast till the year 2033.

Chapters 7 to 10 cover Structured Cabling Market segments solution type, cable type, vertical and geography across North America, Asia Pacific, Europe, the Middle East & Africa, and South & Central America. They cover the market revenue forecast and factors driving the market.

Chapter 11 describes the competitive analysis along with the heat map analysis for the key players operating in the market.

Chapter 12 describes the industry landscape analysis. It provides detailed descriptions of business activities such as market initiatives, new developments, mergers, and joint ventures globally, along with a competitive landscape.

Chapter 13 provides detailed profiles of the major companies operating in the Structured Cabling Market. Companies have been profiled on the basis of their key facts, business descriptions, products, financial overview, SWOT analysis, and key developments.

Chapter 14, i.e., the appendix, is inclusive of a brief overview of the company, a list of abbreviations, and a disclaimer.

Structured Cabling Market News and Key Development:

The Structured Cabling Market is evaluated by gathering qualitative and quantitative data post primary and secondary research, which includes important corporate publications, association data, and databases. A few of the key developments in the spatial light Modulator market are:

In August 2025, Amphenol Corporation agreed to acquire the Connectivity and Cable Solutions (CCS) business from CommScope for US$10.5 billion in cash, a strategic deal that significantly expands Amphenol’s footprint in fiber optic and structured cabling connectivity products serving global broadband, enterprise, and building infrastructure markets.

In June 2025, CommScope Holding Company, Inc. announced that it unveiled new structured cabling solutions the FiberREACH hybrid fiber & power platform and CableGuide 360 cable management suite as part of its SYSTIMAX 2.0 portfolio to support denser, faster enterprise and edge network deployments worldwide.

Key Sources Referred:

World Health Organization (WHO)Organisation for Economic Cooperation and Development (OECD)The World Bank GroupWorldometerThe LancetInternational Bar AssociationInternational Trade Administration

The List of Companies - Structured Cabling Market

CommScope Holding Company, Inc.

Corning Incorporated

Legrand

Nexans

Panduit Corp.

Belden Inc.

R&M

Furukawa Electric Co., Ltd.

Schneider Electric

The Siemon Company

About Author— Electronics and Semiconductor Research Team

Siddhika is an experienced market research professional with over five years of expertise in delivering actionable market intelligence and strategic insights to support business growth and decision-making. She has strong experience in designing and managing end-to-end research engagements, including research planning, data collection, and insight generation.

Proficient in research methodologies, Siddhika synthesizes diverse information sources to deliver accurate, high-quality insights and strategic recommendations. She excels at translating complex market information into strategic narratives that support executive decision-making..

Show More

Frequently Asked Questions

How big is the Structured Cabling Market?

The Structured Cabling Market is valued at US$ 13.7 Billion in 2025, it is projected to reach US$ 20.45 Billion by 2033.

What is the CAGR for Structured Cabling Market by (2026 - 2033)?

As per our report Structured Cabling Market, the market size is valued at US$ 13.7 Billion in 2025, projecting it to reach US$ 20.45 Billion by 2033. This translates to a CAGR of approximately 5.13% during the forecast period.

What segments are covered in this report?

The Structured Cabling Market report typically cover these key segments-

What is the historic period, base year, and forecast period taken for Structured Cabling Market?

The historic period, base year, and forecast period can vary slightly depending on the specific market research report. However, for the Structured Cabling Market report:

Historic Period : 2022-2024

Base Year : 2025

Forecast Period : 2026-2033

Who are the major players in Structured Cabling Market?

The Structured Cabling Market is populated by several key players, each contributing to its growth and innovation. Some of the major players include:

CommScope Holding Company, Inc.

Corning Incorporated

Legrand

Nexans

Panduit Corp.

Belden Inc.

R&M

Furukawa Electric Co., Ltd.

Schneider Electric

The Siemon Company

Who should buy this report?

The Structured Cabling Market report is valuable for diverse stakeholders, including:

Investors: Provides insights for investment decisions pertaining to market growth, companies, or industry insights. Helps assess market attractiveness and potential returns.

Industry Players: Offers competitive intelligence, market sizing, and trend analysis to inform strategic planning, product development, and sales strategies.

Suppliers and Manufacturers: Helps understand market demand for components, materials, and services related to concerned industry.

Researchers and Consultants: Provides data and analysis for academic research, consulting projects, and market studies.

Financial Institutions: Helps assess risks and opportunities associated with financing or investing in the concerned market.

Essentially, anyone involved in or considering involvement in the Structured Cabling Market value chain can benefit from the information contained in a comprehensive market report.

Get Free Sample For Structured Cabling Market

Get Free Sample For Structured Cabling Market