Analysis - by Product (Occluders, Annuloplasty Rings, Heart Valve Balloons, and Others), Procedure (Heart Valve Stenosis, Heart Valve Regurgitation, and Left Atrial Appendage Closure), and End User (Hospitals, Ambulatory Surgical Centers, and Cardiac Centers)

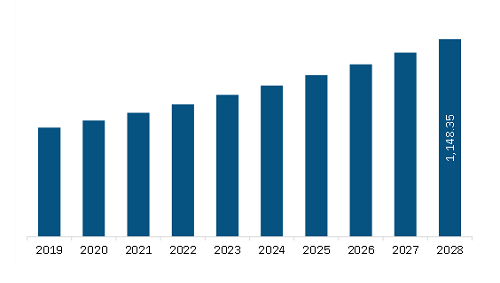

The South & Central America structural heart market is expected to grow from US$ 770.68 million in 2023 to US$ 1,148.35 million by 2028. It is estimated to grow at a CAGR of 6.9% from 2023 to 2028.

Rising Number of Cardiovascular Disease Cases and Training Programs Fuel South & Central America Structural Heart Market

According to the World Health Organization (WHO), cardiovascular diseases are the second leading cause of death South & Central America. Therefore, various initiatives are being taken to control cardiovascular diseases. Heart valve disease is expected to be one of the most common causes of heart failure. Degenerative diseases of aortic and mitral valves, and diseases of dysfunctional tricuspid valves lead to a worse clinical course in severe cases. Minimally invasive, surgical, and catheter-based interventions for structural heart disease have increased dramatically recently. The structural heart is an evolving field consisting of heart valve surgeries and transcatheter procedures; therefore, various training programs are being arranged for cardiac surgeons and physicians. Over the past decade, the burgeoning incidence of structural heart disease has necessitated the development of formal training programs to ensure the appropriate competency of workforces. The structure, length, and scope of training vary greatly between programs. Most programs provide solid exposure on transcatheter aortic valve replacement (TAVR) procedures, simultaneously providing a lesser and variable experience of atrial septal or ventricular septal defect closure, left atrial appendage closure, and congenital heart defect interventions. With the advent of TAVR, the MitraClip mitral valve repair system (Abbott Vascular), and left atrial appendage occlusion (LAAO) procedures, there has been a significant increase in the volume of structural cardiac procedures performed for treating patients with complex cardiovascular conditions. Many organizations have developed services and procedural offerings in an organized format for the structural cardiac program to accommodate the influx of patients. Training in SHD is exciting, challenging, and rewarding overall. As the field evolves, standardization of SHD training becomes extremely important to ensure the best quality of patient care. Finding a mentor to help navigate the numerous considerations outlined can be the best asset to successfully transitioning from training to practice.

South & Central America Structural Heart Market Overview

The South and Central America structural heart is segmented into Brazil, Argentina, and the Rest of South & Central America. Brazil is expected to register the largest market share in this region during the forecast period. The flourishing medical tourism sector and growing government initiatives to create awareness about modern healthcare products are the factors contributing to the structural heart market growth in South & Central America. Additionally, the rising prevalence of cardiovascular diseases and hypertension is propelling the structural heart market growth in the region.

South & Central America Structural Heart Market Revenue and Forecast to 2028 (US$ Million)

South & Central America Structural Heart Market Segmentation

Based on product, the South & Central America structural heart market is segmented into occluders, annuloplasty rings, heart valve balloons, and others. The occluders segment held the largest share of the South & Central America structural heart market in 2022.

Based on procedure, the South & Central America structural heart market is segmented into heart valve stenosis, heart valve regurgitation, and left atrial appendage closure. The heart valve stenosis segment held the largest share of the South & Central America structural heart market in 2022.

Based on end user, the South & Central America structural heart market is segmented into hospitals, ambulatory surgical centers, and others. The hospitals segment held the largest share of the South & Central America structural heart market in 2022.

Based on country, the South & Central America structural heart market is segmented into the Brazil, Argentina, and the Rest of South & Central America. Brazil dominated the South & Central America structural heart market in 2022.

Abbott Laboratories, Medtronic Plc, Boston Scientific Corp, Artivion Inc, Edwards Lifesciences Corp, and Braile Biomedica Industry, Commerce and Representations Ltd are some of the leading companies operating in the South & Central America structural heart market.

South & Central America Structural Heart Market Strategic Insights

Get more information on this report

South & Central America Structural Heart Market Segmentation Analysis

South & Central America Structural Heart Market Report Highlights

South & Central America Structural Heart Report Scope

Report Attribute

Details

Market size in 2023

US$ 770.68 Million

Market Size by 2028

US$ 1,148.35 Million

CAGR (2023 - 2028)

6.9%

Historical Data

2021-2022

Forecast period

2024-2028

Segments Covered

By Product

Occluders

Annuloplasty Rings

Heart Valve Balloons

By Procedure

Heart Valve Stenosis

Heart Valve Regurgitation

Left Atrial Appendage Closure

By End User

Hospitals

Ambulatory Surgical Centers

Cardiac Centers

Regions and Countries Covered

South and Central America

Brazil, Argentina, Rest of South and Central America

Market leaders and key company profiles

Abbott Laboratories

Medtronic Plc

Boston Scientific Corp

Artivion Inc

Edwards Lifesciences Corp

Braile Biomedica Industry, Commerce and Representations Ltd

Get more information on this report

South & Central America Structural Heart Market Country and Regional Insights

Get more information on this report

Identical Market Reports with other Region/Countries

The List of Companies - South & Central America Structural Heart Market

Abbott Laboratories Medtronic Plc Boston Scientific Corp Artivion IncEdwards Lifesciences Corp Braile Biomedica Industry, Commerce and Representations Ltd

Frequently Asked Questions

How big is the South & Central America Structural Heart Market?

The South & Central America Structural Heart Market is valued at US$ 770.68 Million in 2023, it is projected to reach US$ 1,148.35 Million by 2028.

What is the CAGR for South & Central America Structural Heart Market by (2023 - 2028)?

As per our report South & Central America Structural Heart Market, the market size is valued at US$ 770.68 Million in 2023, projecting it to reach US$ 1,148.35 Million by 2028. This translates to a CAGR of approximately 6.9% during the forecast period.

What segments are covered in this report?

The South & Central America Structural Heart Market report typically cover these key segments-

End User (Hospitals, Ambulatory Surgical Centers, Cardiac Centers)

What is the historic period, base year, and forecast period taken for South & Central America Structural Heart Market?

The historic period, base year, and forecast period can vary slightly depending on the specific market research report. However, for the South & Central America Structural Heart Market report:

Historic Period : 2021-2022

Base Year : 2023

Forecast Period : 2024-2028

Who are the major players in South & Central America Structural Heart Market?

The South & Central America Structural Heart Market is populated by several key players, each contributing to its growth and innovation. Some of the major players include:

Abbott Laboratories

Medtronic Plc

Boston Scientific Corp

Artivion Inc

Edwards Lifesciences Corp

Braile Biomedica Industry, Commerce and Representations Ltd

Who should buy this report?

The South & Central America Structural Heart Market report is valuable for diverse stakeholders, including:

Investors: Provides insights for investment decisions pertaining to market growth, companies, or industry insights. Helps assess market attractiveness and potential returns.

Industry Players: Offers competitive intelligence, market sizing, and trend analysis to inform strategic planning, product development, and sales strategies.

Suppliers and Manufacturers: Helps understand market demand for components, materials, and services related to concerned industry.

Researchers and Consultants: Provides data and analysis for academic research, consulting projects, and market studies.

Financial Institutions: Helps assess risks and opportunities associated with financing or investing in the concerned market.

Essentially, anyone involved in or considering involvement in the South & Central America Structural Heart Market value chain can benefit from the information contained in a comprehensive market report.

Get Free Sample For South & Central America Structural Heart Market

Get Free Sample For South & Central America Structural Heart Market