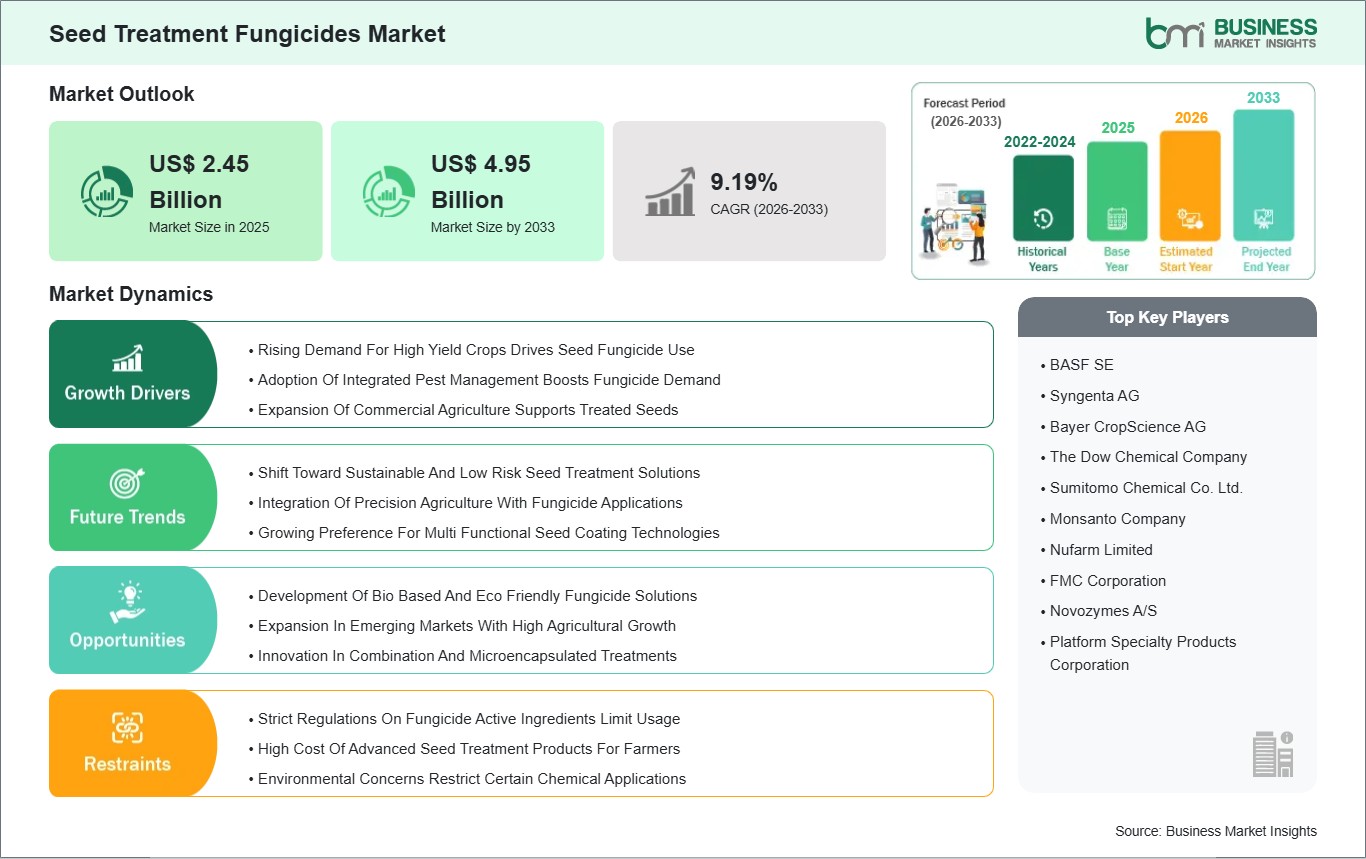

The Seed Treatment Fungicides Market size is expected to reach US$ 4.95 billion by 2033 from US$ 2.45 billion in 2025. The market is estimated to record a CAGR of 9.19% from 2026 to 2033.

Executive Summary and Global Market Analysis:

The global seed treatment fungicides market establishes its essential function for contemporary agriculture when it protects seeds and emerging seedlings from soil‑borne and seed‑borne fungal pathogens. The process of applying seed treatment fungicides requires users to put the fungicides directly on seeds before they start their planting activities to protect against seven different diseases which include damping-off and root rot and smut and rust and blights that bring about substantial losses in crop establishment and yield potential.

The market operates because farmers need to improve their crop output while maintaining healthy plants throughout their various crop systems and boosting their farm profits during a time when food demand increases and available farmland decreases. The global seed treatment fungicides market experiences its main growth driver through global grower adoption of integrated pest management (IPM) practices. Seed treatment fungicides serve as the fundamental element of integrated pest management because they eliminate pathogens at the beginning of the crop growth phase which decreases the requirement for multiple foliar fungicide treatments during the upcoming part of the growing season.

Farmers in areas that experience severe disease outbreaks which include regions with humid and temperate weather now prefer seed treatment products that combine several active ingredients because these products provide both extensive control and lasting protection. The rising adoption of high-value crops including corn and soybean and cereals in developing agricultural markets has created a need for seed treatment products which improve both stand uniformity and vigor. The market shows positive developments but experiences limitations because developed regions enforce environmental and health-related rules that restrict specific active ingredients. The current fungicidal chemistries face two major challenges because they lose their approved status and need to follow new labeling rules which compel manufacturers to create safer products with different mechanisms of action.

The industry develops reduced-risk and bio-based fungicides because environmental sustainability needs to be fulfilled while developing products that meet strict safety requirements and maintain their effectiveness. The cost of advanced seed treatment technologies creates challenges for smallholder farmers who live in areas that lack financial resources. The market will experience global growth because new formulation technologies and people learn about the advantages of disease management.

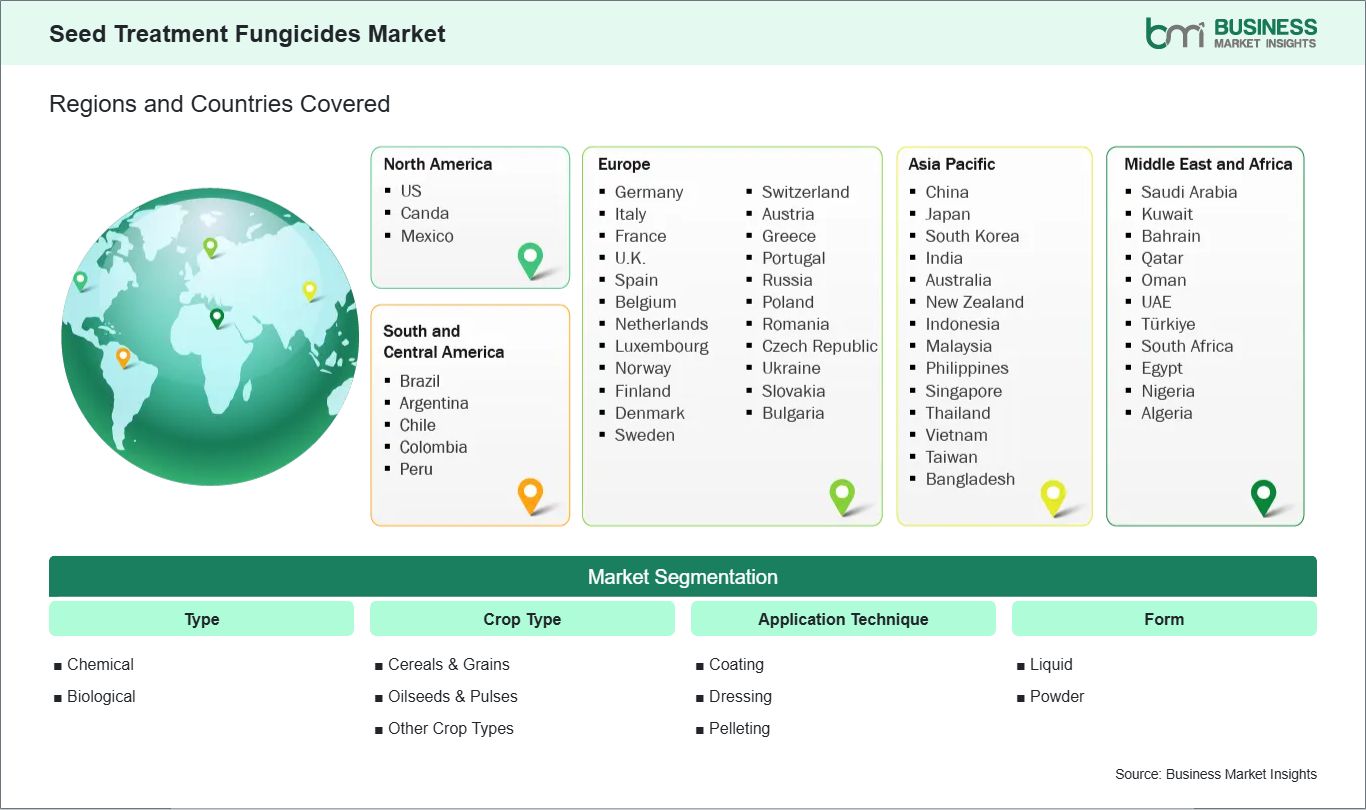

Key segments that contributed to the derivation of the seed treatment fungicides market analysis are type, crop type, application technique, and form.

By type, the seed treatment fungicides market is segmented into chemical and biological. The chemical segment dominated the market in 2025.

Based on crop type, the seed treatment fungicides market is categorized into cereals & grains, oilseeds & pulses, others. The cereals & grains segment dominated the market in 2025.

On the basis of application technique, the seed treatment fungicides market is categorized into coating, dressing, pelleting. The seed dressing segment dominated the market in 2025.

In terms of form, the seed treatment fungicides market is categorized into liquid and powder. The liquid segment dominated the market in 2025.

Seed Treatment Fungicides Market Drivers and Opportunities:

Rising Demand For High Yield Crops Drives Seed Fungicide Use

Global agriculture is increasingly focused on improving crop output per hectare to meet rising food, feed, and biofuel demand. Farmers need seed treatment fungicides to achieve their yield objectives because these products protect seeds and seedlings from fungal diseases which decrease plant establishment and early development. In major agricultural regions like North America and Europe corn soybean and wheat growers routinely apply seed fungicides before planting to protect against soil‑borne pathogens such as Fusarium Pythium and Rhizoctonia which can devastate young crops before they develop robust root systems.

Fungicide seed treatments in Asia Pacific enable rice and vegetable farmers to achieve maximum crop output from restricted arable land because the treatments protect crops from disease during germination. This is particularly important in monsoon‑influenced climates where high humidity accelerates fungal proliferation. Emerging markets in Latin America and Africa are also adopting these solutions as part of broader efforts to close yield gaps. In Brazil and Argentina seed fungicides become part of soybean and maize planting programs which protect premium seed investments and support global yield enhancement strategies.

Development Of Bio Based And Eco Friendly Fungicide Solutions

The seed treatment fungicides market now operates under the influence of environmental sustainability which drives the global adoption of bio-based and low-impact solutions. The use of traditional chemical fungicides provides effective results but it creates problems because these substances damage soil health and leave toxic residues which impact beneficial organisms. European and North American companies create bio-based fungicide products through the development of microbial agents and plant extracts and enzymes that fight pathogens without using harsh chemicals. Growers prefer these formulations because they provide effective disease control while decreasing their environmental impact. The Indian and Chinese markets experience increased agricultural research because governments require sustainable farming practices which focus on developing eco-friendly seed treatments that meet national pesticide reduction targets.

Local agribusinesses team up with international biotech companies to develop bio-based fungicides that target local crop diseases and adapt to specific weather patterns. The emerging market trend shows that agricultural products which combine chemical actives that have low risk with biological components, now provide growers a complete solution which protects their crops while maintaining sustainable practices. The current trend towards eco‑friendly seed treatments will lead to increased usage because farmers now consider environmental protection as a standard requirement in their agricultural practices.

Seed Treatment Fungicides Market Size and Share Analysis:

The seed treatment fungicides market demonstrates steady growth, with size and share analysis highlighting evolving trends and competitive dynamics among key players. The report examines subsegments categorized within type, crop type, application technique, and form, offering insights into their contribution to overall market performance.

By type, the chemical subsegment dominated the market in 2025, driven by its broad-spectrum effectiveness, cost-efficiency, and established adoption in seed protection.

Based on crop type, the cereals & grains subsegment dominated the market in 2025, driven by their status as staple crops with high seed treatment demand to ensure productivity and disease protection.

On the basis of application technique, the seed dressing subsegment dominated the market in 2025, driven by its ease of application, precise dosage control, and compatibility with large-scale farming operations.

In terms of form, the liquid subsegment dominated the market in 2025, driven by better coverage, uniform coating, and higher absorption rates on seeds compared to other forms.

Australia, China, India, Japan, South Korea, Indonesia, Malaysia, Philippines, Singapore, Thailand, Vietnam, Bangladesh, New Zealand, Taiwan

South and Central America

Brazil, Argentina, Peru, Chile, Colombia

Middle East and Africa

Bahrain, Kuwait, Oman, Qatar, Saudi Arabia, United Arab Emirates, Turkiye, South Africa, Egypt, Algeria, Nigeria

Market leaders and key company profiles

BASF SE

Syngenta AG

Bayer CropScience AG

The Dow Chemical Company

Sumitomo Chemical Co. Ltd.

Monsanto Company

Nufarm Limited

FMC Corporation

Novozymes A/S

Platform Specialty Products Corporation

Get more information on this report

Seed Treatment Fungicides Market Report Coverage and Deliverables:

The "Seed Treatment Fungicides Market Size and Forecast (2022 - 2033)" report provides a detailed analysis of the market covering below areas:

Seed Treatment Fungicides Market size and forecast at global, regional, and country levels for all the key market segments covered under the scope

Seed Treatment Fungicides Market trends, as well as drivers, restraints, and opportunities

Seed Treatment Fungicides Market analysis covering key trends, global and regional framework, major players, regulations, and recent developments

Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments for the Seed Treatment Fungicides Market

Detailed company profiles, including SWOT analysis

The geographical scope of the Seed Treatment Fungicides Market report is divided into North America, Asia Pacific, Europe, Middle East & Africa, and South & Central America. North America held the largest share in 2025.

The global market for seed treatment fungicides in North America shows its highest market share because advanced farming methods and extensive row crop farming and widespread use of integrated pest management systems drive the market. Farmers in the United States and Canada use seed treatment fungicides on corn, soybean, wheat, and cotton to protect their crops from soil-borne and seed-borne fungal pathogens such as Rhizoctonia, Fusarium, and Pythium. The commercial seed processing and treatment facilities work together with agronomist expertise and farmer knowledge to create a common practice of using fungicidal blends which produce consistent germination results and strong initial plant growth.

The European market operates on established business models which determine the fungicide products used because safety regulations require eco-friendly and lower-risk chemical solutions that provide effective crop protection.

The seed treatment industry in France, Germany, and Italy operates sophisticated systems which produce advanced treatment solutions for different crop types including cereals and vegetables and oilseeds. The agricultural modernization movement in Asia Pacific brings about two changes which include expanded high-value crop production and increased disease management knowledge that drive seed treatment fungicides adoption in China, India, and Australia. The dual approach of governments together with private agribusinesses promotes treated seed usage as a method to achieve higher crop yields while decreasing losses from post-emergence diseases.

The Middle East and Africa market develops through its adoption of high-value crops which include wheat and maize and vegetables together with regional programs that aim to enhance food security and agricultural productivity under adverse weather conditions. South American and Central American markets experience slow growth which is most evident in Brazil and Argentina as commercial farms use treated seeds to protect soybean and maize and wheat crops from fungal diseases that occur in tropical and subtropical regions. Innovations in reduced-risk and bio-based fungicides together with combination treatments and application technologies enable growers across all regions to protect their seedlings while they comply with environmental and sustainability requirements which drives the global growth of the seed treatment fungicides market and its regional market variations.

Get more information on this report

Seed Treatment Fungicides Market Research Report Guidance:

The report includes qualitative and quantitative data in the Seed Treatment Fungicides Market across type, crop type, application technique, form and geography.

The report starts with the key takeaways (chapter 2), highlighting key trends and outlook of the Seed Treatment Fungicides Market.

Chapter 3 focuses on the research methodology of the study.

Chapter 4 includes ecosystem analysis.

Chapter 5 highlights the major industry dynamics in the Seed Treatment Fungicides Market, including factors that are driving the market, prevailing deterrents, potential opportunities, as well as future trends. Impact analysis of these drivers and restraints is also covered in this section.

Chapter 6 discusses the Seed Treatment Fungicides Market scenario, in terms of historical market revenues, and forecast till the year 2033.

Chapters 7 to 11 cover Seed Treatment Fungicides Market segments by type, crop type, application technique, form and geography across North America, Asia Pacific, Europe, Middle East & Africa, and South & Central America. They cover the market revenue forecast and factors driving the market.

Chapter 12 describes the competitive analysis along with the heat map analysis for the key players operating in the market.

Chapter 13 describes the industry landscape analysis. It provides detailed descriptions of business activities such as market initiatives, new developments, mergers, and joint ventures globally, along with a competitive landscape.

Chapter 14 provides detailed profiles of the major companies operating in the Seed Treatment Fungicides Market. Companies have been profiled on the basis of their key facts, business descriptions, products, financial overview, SWOT analysis, and key developments.

Chapter 15, i.e., the appendix, is inclusive of a brief overview of the company, a list of abbreviations, and a disclaimer.

Seed Treatment Fungicides Market News and Key Development:

The Seed Treatment Fungicides Market is evaluated by gathering qualitative and quantitative data post primary and secondary research, which includes important corporate publications, association data, and databases. A few of the key developments in the seed treatment fungicides market are:

In November 2025, BASF SE announced that its Integral® Pro fungicide seed treatment for sunflowers received official registration in France, providing growers across the EU with a new sustainable seed treatment solution to prevent key soil‑ and seed‑borne fungal diseases and support crop resilience.

In October 2023, Corteva Agriscience announced that it had commercialized Straxan™ fungicide seed treatment in Canada, offering advanced protection against early‑season seed and soil‑borne cereal diseases with a ready‑to‑use formulation that enhances cereal crop stand establishment.

Key Sources Referred:

World Health Organization (WHO)Organisation for Economic Cooperation and Development (OECD)The World Bank GroupWorldometerThe LancetInternational Bar AssociationInternational Trade Administration

The List of Companies - Seed Treatment Fungicides Market

BASF SE

Syngenta AG

Bayer CropScience AG

The Dow Chemical Company

Sumitomo Chemical Co. Ltd.

Monsanto Company

Nufarm Limited

FMC Corporation

Novozymes A/S

Platform Specialty Products Corporation

About Author— Chemicals and Materials Research Team

Suraj Sajeev is a market research and consulting professional with nearly 10 years of experience across Life Sciences, Consumer Goods, Food & Beverages, Materials & Chemicals, and Automotive industries. Throughout his career, he has successfully managed and delivered custom market research and consulting engagements, enabling clients to make informed strategic decisions through actionable market intelligence.

Suraj has extensive expertise in end-to-end project management, including proposal development, market assessment, competitive intelligence, opportunity analysis, market sizing and forecasting, strategic recommendation..

Frequently Asked Questions

How big is the Seed Treatment Fungicides Market?

The Seed Treatment Fungicides Market is valued at US$ 2.45 Billion in 2025, it is projected to reach US$ 4.95 Billion by 2033.

What is the CAGR for Seed Treatment Fungicides Market by (2026 - 2033)?

As per our report Seed Treatment Fungicides Market, the market size is valued at US$ 2.45 Billion in 2025, projecting it to reach US$ 4.95 Billion by 2033. This translates to a CAGR of approximately 9.19% during the forecast period.

What segments are covered in this report?

The Seed Treatment Fungicides Market report typically cover these key segments-

Type (Chemical, Biological)

Crop Type (Cereals & Grains, Oilseeds & Pulses, Other Crop Types)

What is the historic period, base year, and forecast period taken for Seed Treatment Fungicides Market?

The historic period, base year, and forecast period can vary slightly depending on the specific market research report. However, for the Seed Treatment Fungicides Market report:

Historic Period : 2022-2024

Base Year : 2025

Forecast Period : 2026-2033

Who are the major players in Seed Treatment Fungicides Market?

The Seed Treatment Fungicides Market is populated by several key players, each contributing to its growth and innovation. Some of the major players include:

BASF SE

Syngenta AG

Bayer CropScience AG

The Dow Chemical Company

Sumitomo Chemical Co. Ltd.

Monsanto Company

Nufarm Limited

FMC Corporation

Novozymes A/S

Platform Specialty Products Corporation

Who should buy this report?

The Seed Treatment Fungicides Market report is valuable for diverse stakeholders, including:

Investors: Provides insights for investment decisions pertaining to market growth, companies, or industry insights. Helps assess market attractiveness and potential returns.

Industry Players: Offers competitive intelligence, market sizing, and trend analysis to inform strategic planning, product development, and sales strategies.

Suppliers and Manufacturers: Helps understand market demand for components, materials, and services related to concerned industry.

Researchers and Consultants: Provides data and analysis for academic research, consulting projects, and market studies.

Financial Institutions: Helps assess risks and opportunities associated with financing or investing in the concerned market.

Essentially, anyone involved in or considering involvement in the Seed Treatment Fungicides Market value chain can benefit from the information contained in a comprehensive market report.

Get Free Sample For Seed Treatment Fungicides Market

Get Free Sample For Seed Treatment Fungicides Market