Analysis – by Fiber Type (Carbon/Aramid, Carbon/Glass, High-Modulus Polypropylene (HMPP)/Carbon, Ultra High Molecular Weight Polyethylene (UHMWPE)/ Carbon, and Others), Resin (Thermoset and Thermoplastic), and Application (Automotive, Aerospace, Marine, Wind Energy, Sporting Goods, and Others)

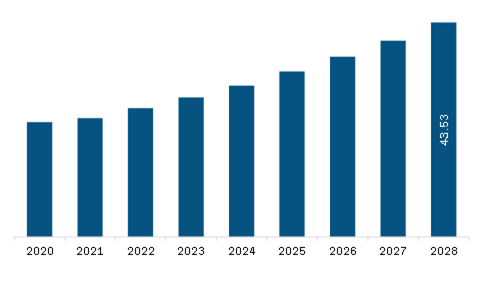

The Middle East & Africa hybrid composites market is expected to grow from US$ 28.32 million in 2023 to US$ 43.53 million by 2028. It is estimated to grow at a CAGR of 9.0% from 2023 to 2028.

Rising Use of Hybrid Composites in Wind Energy and Automotive Industries Fuels Middle East & Africa Hybrid Composites Market

Rapid developments in material technology continue to support variations in the structure of wind turbines. Many of these variations were primarily introduced to reduce the prices of turbines. Factors such as corrosion resistance, fatigue resistance, toughness, rigidity, weight, and appearance of wind turbines significantly impact their operations. Glass fiber-reinforced plastics (GRPs) are the most used type of composite material in wind turbine manufacturing. The major benefits of using GRPs include hybrid mechanical properties, high corrosion resistance, high-temperature tolerance, simplified manufacturing, and favorable costs.

Lightweight materials offer excellent potential for increasing vehicle efficiency as their acceleration requires less energy than heavier ones. According to the Office of Energy Efficiency & Renewable Energy, a 10% decrease in vehicle weight can improve fuel economy by 6–8%. Substituting cast iron and traditional steel components with lightweight materials, such as high-strength steel, aluminum (Al) alloys, magnesium (Mg) alloys, carbon fiber, and polymer composites, can reduce the weight of a vehicle body and chassis by up to 50%, thereby reducing the fuel consumption of a vehicle. The application of hybrid composites in the automotive sector is growing at a significant pace. In this sector, plastics are used in large quantities to produce composites. Hybrid composites have excellent acoustic and thermal properties, which makes them ideal for vehicle interior parts. Furthermore, they are suitable for the manufacturing of non-structural interior components, including seat fillers, seat backs, headliners, interior panels, and dashboards. Therefore, the growing demand for hybrid composites from the automotive industry for the manufacturing of fuel-efficient, lightweight vehicles such as electric vehicles (EVs) is driving the hybrid composites market.

Middle East & Africa Hybrid Composites Market Overview

The Middle East & Africa hybrid composites market is segmented into South Africa, Saudi Arabia, the UAE, and the Rest of Middle East & Africa. The growth of the aviation industry due to various government initiatives is among the significant factors driving the demand for hybrid composites in the region as it provides durability and toughness to the aircraft. For instance, on August 14, 2023, the Saudi Arabian government invested US$ 100 billion in the aviation sector to host at least 300 million passengers and 5 million tons of freight by 2030. The aviation industry in the Middle East & Africa is also fueled by rapid industrialization and growth in disposable income, resulting in a surge of passengers opting for air travel. Further, according to the report by International Trade Administration, the UAE government has supported and invested in various initiatives in the aerospace industry, thus increasing the number of partnerships among significant market players and Original Equipment Manufacturers (OEMs). Therefore, the growing aerospace industry in the region boosts the demand for hybrid composites.

Middle East & Africa Hybrid Composites Market Revenue and Forecast to 2028 (US$ Million)

Middle East & Africa Hybrid Composites Market Segmentation

The Middle East & Africa hybrid composites market is segmented into fiber type, resin, application, and country.

Based on fiber type, the Middle East & Africa hybrid composites market is segmented into carbon/aramid, carbon/glass, high-modulus polypropylene (HMPP)/carbon, ultra high molecular weight polyethylene (UHMWPE)/ carbon, and others. The carbon/aramid segment held the largest share of the Middle East & Africa hybrid composites market in 2023.

Based on resin, the Middle East & Africa hybrid composites market is segmented into thermoset and thermoplastic. The thermoset segment held a larger share of the Middle East & Africa hybrid composites market in 2023.

Based on application, the Middle East & Africa hybrid composites market is segmented into automotive, aerospace, marine, wind energy, sporting goods, and others. The automotive segment held the largest share of the Middle East & Africa hybrid composites market in 2023.

Based on country, the Middle East & Africa hybrid composites market is segmented into South Africa, Saudi Arabia, the UAE, and the Rest of Middle East & Africa. Saudi Arabia dominated the Middle East & Africa hybrid composites market in 2023.

Avient Corp, Gurit Holding AG, Hexcel Corp, Lanxess AG, Mitsubishi Chemical Holdings Corp, PGTEX China Co Ltd, SGL Carbon SE, Solvay SA, and Toray Industries Inc are some of the leading companies operating in the Middle East & Africa hybrid composites market.

Middle East & Africa Hybrid Composites Market Strategic Insights

Get more information on this report

Middle East & Africa Hybrid Composites Market Segmentation Analysis

Middle East & Africa Hybrid Composites Market Report Highlights

Middle East & Africa Hybrid Composites Report Scope

Report Attribute

Details

Market size in 2023

US$ 28.32 Million

Market Size by 2028

US$ 43.53 Million

CAGR (2023 - 2028)

9.0%

Historical Data

2021-2022

Forecast period

2024-2028

Segments Covered

By Fiber Type

Carbon/Aramid

Carbon/Glass

High-Modulus Polypropylene/Carbon

Ultra High Molecular Weight Polyethylene/Carbon

By Resin

Thermoset and Thermoplastic

By Application

Automotive

Aerospace

Marine

Wind Energy

Sporting Goods

Regions and Countries Covered

Middle East and Africa

South Africa, Saudi Arabia, UAE, Rest of Middle East and Africa

Market leaders and key company profiles

Avient Corp

Gurit Holding AG

Hexcel Corp

Lanxess AG

Mitsubishi Chemical Holdings Corp

PGTEX China Co Ltd

SGL Carbon SE

Solvay SA

Toray Industries Inc

Get more information on this report

Middle East & Africa Hybrid Composites Market Country and Regional Insights

Get more information on this report

Identical Market Reports with other Region/Countries

The List of Companies - Middle East & Africa Hybrid Composites Market

Avient CorpGurit Holding AGHexcel CorpLanxess AGMitsubishi Chemical Holdings CorpPGTEX China Co LtdSGL Carbon SESolvay SAToray Industries Inc

Frequently Asked Questions

How big is the Middle East & Africa Hybrid Composites Market?

The Middle East & Africa Hybrid Composites Market is valued at US$ 28.32 Million in 2023, it is projected to reach US$ 43.53 Million by 2028.

What is the CAGR for Middle East & Africa Hybrid Composites Market by (2023 - 2028)?

As per our report Middle East & Africa Hybrid Composites Market, the market size is valued at US$ 28.32 Million in 2023, projecting it to reach US$ 43.53 Million by 2028. This translates to a CAGR of approximately 9.0% during the forecast period.

What segments are covered in this report?

The Middle East & Africa Hybrid Composites Market report typically cover these key segments-

Fiber Type (Carbon/Aramid, Carbon/Glass, High-Modulus Polypropylene/Carbon, Ultra High Molecular Weight Polyethylene/Carbon)

What is the historic period, base year, and forecast period taken for Middle East & Africa Hybrid Composites Market?

The historic period, base year, and forecast period can vary slightly depending on the specific market research report. However, for the Middle East & Africa Hybrid Composites Market report:

Historic Period : 2021-2022

Base Year : 2023

Forecast Period : 2024-2028

Who are the major players in Middle East & Africa Hybrid Composites Market?

The Middle East & Africa Hybrid Composites Market is populated by several key players, each contributing to its growth and innovation. Some of the major players include:

Avient Corp

Gurit Holding AG

Hexcel Corp

Lanxess AG

Mitsubishi Chemical Holdings Corp

PGTEX China Co Ltd

SGL Carbon SE

Solvay SA

Toray Industries Inc

Who should buy this report?

The Middle East & Africa Hybrid Composites Market report is valuable for diverse stakeholders, including:

Investors: Provides insights for investment decisions pertaining to market growth, companies, or industry insights. Helps assess market attractiveness and potential returns.

Industry Players: Offers competitive intelligence, market sizing, and trend analysis to inform strategic planning, product development, and sales strategies.

Suppliers and Manufacturers: Helps understand market demand for components, materials, and services related to concerned industry.

Researchers and Consultants: Provides data and analysis for academic research, consulting projects, and market studies.

Financial Institutions: Helps assess risks and opportunities associated with financing or investing in the concerned market.

Essentially, anyone involved in or considering involvement in the Middle East & Africa Hybrid Composites Market value chain can benefit from the information contained in a comprehensive market report.

Get Free Sample For Middle East & Africa Hybrid Composites Market

Get Free Sample For Middle East & Africa Hybrid Composites Market