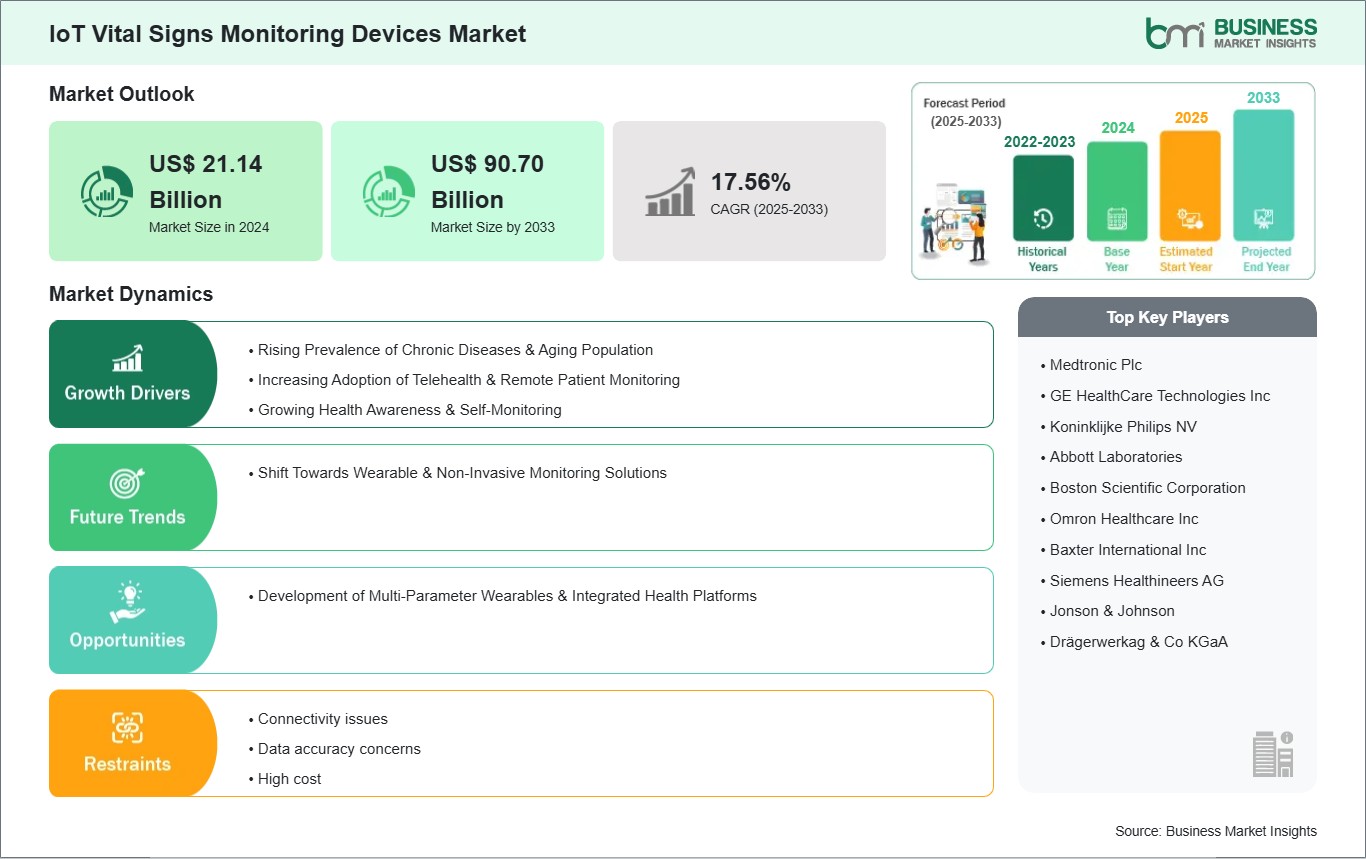

The IoT Vital Signs Monitoring Devices Market size is expected to reach US$ 90.70 Billion by 2033 from US$ 21.14 Billion in 2024. The market is estimated to record a CAGR of 17.56% from 2025 to 2033.

Executive Summary and Global Market Analysis:

The global IoT vital signs monitoring devices market is experiencing significant growth driven by rising prevalence of chronic diseases & aging population, increasing adoption of telehealth & remote patient monitoring, growing health awareness & self-monitoring. However, the lack of standardization and associated security and privacy concerns are slowing market evolution. Geographically, the market for IoT vital signs monitoring devices is largest in North America, because of the region's sophistication of healthcare infrastructure, the widespread adoption of digital health, the innovative reimbursement policies, and the presence of large market participants, such as Medtronic, GE HealthCare, Philips, and Omron Healthcare. North America has FDA regulatory incentives for remote monitoring and AI-enabled diagnostics in the region. The Asia-Pacific (APAC) region is growing the fastest in the healthcare technology space. The market is growing rapidly from the increase in geriatric population, rise in chronic diseases, exponential growth in internet-based applications, and the presence of government driven digitized healthcare in larger countries such as China, India, and Japan. The Competitive Analysis dimension includes global markets leaders and emerging regional players. Companies are continuing to innovate products that are smaller, and use AI to improve accuracy, more user-friendly products, and reduce the price for monitoring vital signs.

IoT Vital Signs Monitoring Devices Market Strategic Insights

Key segments that contributed to the derivation of the IoT Vital Signs Monitoring Devices market analysis are product, technology, application, and end user.

- By product, IoT vital signs monitoring devices market is segmented into IoT blood pressure monitors, IoT pulse oximeters, IoT thermometers, IoT ECG monitors, and others. The IoT blood pressure monitors segment dominated the market in 2024.

- By technology, IoT vital signs monitoring devices market is segmented into Wi-Fi, Bluetooth, cellular, and others. The Wi-Fi segment dominated the market in 2024.

- In terms of application, the market is segmented into blood pressure monitoring, respiratory monitoring, temperature monitoring, and others. The blood pressure monitoring segment held the largest share of the market in 2024.

- By end user, the market is segmented into hospitals & clinics, home care settings, and others. The Hospitals & clinics segment held the largest share of the market in 2024.

IoT Vital Signs Monitoring Devices Market Drivers and Opportunities:

The Increasing Adoption of Telehealth and Remote Patient Monitoring Driving IoT Vital Signs Monitoring Devices Market

Moving towards telehealth and remote patient monitoring (RPM) is a significant and complex driver for demand in the IoT smart vital signs monitoring devices market. The transition of healthcare delivery models to include telehealth, significantly sped-up by recent global healthcare experiences, has fundamentally changed healthcare delivery, including how patients are managed and cared for. With telehealth and RPM, clinicians and providers can collect, transmit, and analyze data collected from patient vital signs devices while outside of traditional clinical or face-to-face interactions. This type of innovative care delivery models allows for proactive, continuous management of patient care, which has been shown to improve health outcomes and reduce healthcare costs. The mode of the telehealth and RPM shift appears in several ways as well. For example, remote consultations will require reliable and real-time data to be generated and reported from connected vital signs monitoring devices to inform clinical reasoning and decision making. Additionally, RPM programs for chronic disease management (hypertension, diabetes, heart failure, etc.) rely on connected vital signs monitoring devices to track patients in their own home or community setting. Finally, the combination of convenience for patients, and efficiencies generated for healthcare systems (reduced hospital readmissions, resources deployed appropriately), creates a demand and a catalyst for the development, use, and continued innovation of IoT smart vital signs monitoring devices. In addition to being a technology for facilitating change in clinical and public health guidelines, IoT smart vital signs monitoring devices will continue to be an invaluable component of digital health.

Development of Multi-Parameter Wearables & Integrated Health Platforms

The evolution of multi-parameter wearables and integrated health platforms offers strong potential for the IoT vital signs monitoring devices market. Typically, vital sign monitoring and assessment involved using separate, dedicated devices to monitor each measurement, each producing separate data that did not provide a full assessment of the patient's health. With the introduction of multi-parameter wearables, vital signs may now be simultaneously, continuously, and non-invasively collected, so the integration of multiple vital signs collections provides the user with ease of use and more data. The changing economics of the device may also facilitate improvements in value and encourage integrated health platforms for a more sophisticated collection of health data. Integrated health platforms are the next advance in health monitoring, beyond environmental impacts. Integrated health platforms are a central platform and store that allows multi- parameter wearables to synchronize data collection to one location, along with data from other connected health devices that the user may have, along with characteristics of patient-reported outcome measurements. Integrated platforms that include cloud computing and AI/ML models can leverage huge datasets to allow the identification of nuanced patterns, determine risk for deterioration in health, and offer information for better healthy choices. Both the patient and clinician can benefit from this integrated health platform approach because patients have better knowledge of the status of their health, providing actionable intelligence to the clinician, and more advances toward the value proposition in healthcare. The integrated health platform approach promotes a health continuum model which represents a proactive health approach that can lead to better diagnosis, care of the patient, a better long-term plan for chronic disease management, and ultimately better patient health outcomes and a better system of care.

IoT Vital Signs Monitoring Devices Market Size and Share Analysis

The IoT vital signs monitoring devices market is classified according to products into IoT blood pressure monitors, IoT pulse oximeters, IoT thermometers, IoT ECG monitors, and others. The IoT blood pressure monitors segment led the market in 2024 and beyond. The segment's leading position is strengthened by the global prevalence of hypertension. Hypertension is a chronic condition afflicting billions of individuals, and it is a significant risk factor for more severe cardiovascular diseases, including heart Stroke. Therefore, the need for frequent, accurate, and consistent monitoring of blood pressure is immense, as blood pressure has to be monitored not only to make a diagnosis but to manage the patient afterward. IoT-enabled blood pressure monitors allow for home-based monitoring, with data sent remotely and automatically to providers, resulting in improved tracking and earlier intervention, adherence to treatment plans for the patient, and ultimately more successful management of this condition.

By technology, the market is segmented into Wi-Fi, Bluetooth, cellular, and others. The Wi-Fi segment held the largest share of the market in 2024. This is owing to its ubiquitous affordability, interoperable infrastructure, and high data transfer speeds. Almost all hospitals, clinics, and patients' homes have Wi-Fi networks, so for IoT devices, it is a cost-effective and convenient connectivity path without creating any new dedicated infrastructure. Wi-Fi enables transmission of data instantaneously and therefore allows for real-time data exchange, which is essential for continuous vital sign monitoring, where alerts may be time sensitive, and data analysis happens instantaneously.

In terms of applications, the market is segmented into blood pressure monitoring, respiratory monitoring, temperature monitoring, and others. The blood pressure monitoring segment had the largest market share in 2024. This is because blood pressure is critical for the diagnosis and management of many health conditions. While blood pressure is commonly associated with managing hypertension, it is also a primary indicator of cardiovascular health overall, and blood pressure is a vital sign measured almost everywhere from the emergency room, to the operating room and inpatient and outpatient settings. The sheer demand for blood pressure measurement routinely or continuously, for many different patient populations and many different clinical scenarios, indicates blood pressure will continue to be the largest application segment that serves acute care decisions and chronic disease management needs.

By end user, the market is segmented into hospitals & clinics, home care settings, others. The hospitals & clinics segment held the largest share of the market in 2024. This is because of their large number of patients, scope of care and provider purchasing discretion. These healthcare facilities admit patients with a breadth of conditions, ranging from an emergency room visit to long-term care being delivered to patients with chronic disease, and they all require vital signs monitoring continuously, particularly for vital signs that are critical to diagnosis. Hospitals have the economic capacity to pay for sophisticated multi-parameter monitoring systems in bulk, which are linked electronically and generate patient records across all aspects of patient management.

IoT Vital Signs Monitoring Devices Market Report Highlights| Report Attribute | Details |

| Market size in 2024 | US$ 21.14 Billion |

| Market Size by 2033 | US$ 90.70 Billion |

| Global CAGR (2025 - 2033) | 17.56% |

| Historical Data | 2022-2023 |

| Forecast period | 2025-2033 |

| Segments Covered |

By Product

|

|

Regions and Countries Covered

|

|

| North America | US, Canada, Mexico |

| Europe | Germany, Italy, France, U.K., Spain, Belgium, Netherlands, Luxembourg, Norway, Finland, Denmark, Sweden, Switzerland, Austria, Greece, Portugal, Russia, Poland, Romania, Czech Republic, Ukraine, Slovakia, Bulgaria |

| Asia-Pacific | China, Japan, South Korea, India, Australia, New Zealand, Indonesia, Malaysia, Philippines, Singapore, Thailand, Vietnam, Taiwan, Bangladesh |

| South and Central America | Brazil, Argentina, Chile, Colombia, Peru |

| Middle East and Africa | Saudi Arabia, United Arab Emirates, Kuwait, Bahrain, Qatar, Oman, Turkiye, South Africa, Egypt, Nigeria, Algeria |

| Market leaders and key company profiles |

|

IoT Vital Signs Monitoring Devices Market Report Coverage and Deliverables

The "IoT Vital Signs Monitoring Devices Market Size and Forecast (2022–2033)" report provides a detailed analysis of the market covering below areas:

- IoT vital signs monitoring devices market size and forecast at global, regional, and country levels for all the key market segments covered under the scope

- IoT vital signs monitoring devices market trends, as well as market dynamics such as drivers, restraints, and key opportunities

- Detailed SWOT analysis

- IoT vital signs monitoring devices market analysis covering key market trends, global and regional framework, major players, regulations, and recent market developments

- Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments for the IoT Vital Signs Monitoring Devices market

- Detailed company profiles

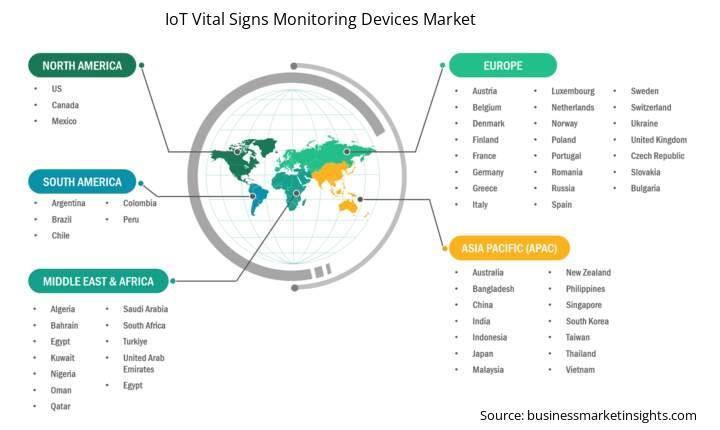

The geographical scope of the IoT vital signs monitoring devices market report is divided into five regions: North America, Asia Pacific, Europe, Middle East & Africa, and South & Central America. The IoT Vital Signs Monitoring Devices market in Asia Pacific is expected to grow significantly during the forecast period.

Asia Pacific IoT vital signs monitoring devices market includes China, Japan, India, South Korea, Australia, Bangladesh, New Zealand, Philippines, Singapore, Indonesia, Taiwan, Malaysia, Vietnam, and the rest of Asia Pacific. Asia Pacific is rapidly gaining momentum as the fastest growing region in the IoT vital signs monitoring devices market due to the strong overlap of demographic, technology and economic factors. Asia Pacific has a rapidly developing and aging population, which is naturally associated with an increased incidence of chronic diseases such as cardiovascular disease, diabetes and respiratory disease. This higher incidence of chronic disease drives the increasing demand for vital signs monitoring. At the same time, the region exhibits an increasing amount of health care dollars being spent due to rising disposable income and a growing awareness of health and wellness issues amongst the population. To add to these factors is a rapid pace of adoption of digital healthcare technologies, including IoT and AI. Governments throughout the region are expanding investments to modernize the healthcare experience, investing in digital health initiatives, and expanding the delivery of healthcare because the demand for healthcare is rapidly increasing across all economies and pace of development.

In Asia Pacific, certain inward focused countries lead the growth for IoT vital signs monitoring. China dominates the region for IoT medical devices, driven by massive government investment in healthcare infrastructure, smart hospitals, and a very large population creating brisk demand for monitoring solutions, primarily in relation to chronic, non-communicable disease. Similarly, India is growing rapidly with its very large population, growing awareness of health and growing middle class, it too is contributing to brisk growth in IoT monitoring devices.

IoT Vital Signs Monitoring Devices Market Research Report Guidance

- The report includes qualitative and quantitative data in the IoT Vital Signs Monitoring Devices market across product, technology, application, and end user, and geography.

- The report starts with the key takeaways (chapter 2), highlighting the key trends and outlook of the IoT vital signs monitoring devices market.

- Chapter 3 includes the research methodology of the study.

- Chapter 4 further includes ecosystem analysis along with PEST analysis.

- Chapter 5 highlights the major industry dynamics in the IoT vital signs monitoring devices market, including factors that are driving the market, prevailing deterrents, potential opportunities and future trends. Impact analysis of these drivers and restraints is also covered in this section.

- Chapter 6 discusses the IoT vital signs monitoring devices market scenario, in terms of historical market revenues, and forecast till the year 2033.

- Chapters 7 to 10 cover IoT vital signs monitoring devices market segments by product, technology, application, end user, and geography across North America, Europe, APAC, Middle East and Africa, South and Central America. They cover the market volume revenue forecast and factors driving the market.

- Chapter 11 describes the competitive analysis along with the heat map analysis for the key players operating in the market.

- Chapter 12 describes the industry landscape analysis. It provides detailed descriptions of various business activities such as market initiatives, new developments, mergers, and joint ventures globally, along with a competitive landscape.

- Chapter 13 provides a detailed profile of the major companies operating in the IoT Vital Signs Monitoring Devices market. Companies have been profiled on the basis of their key facts, business description, products and services, financial overview, SWOT analysis, and key developments.

- Chapter 14, i.e., the appendix, is inclusive of a brief overview of the company, list of abbreviations, and disclaimer section.

IoT Vital Signs Monitoring Devices Market News and Key Development:

The IoT vital signs monitoring devices market is evaluated by gathering qualitative and quantitative data post primary and secondary research, which includes important corporate publications, association data, and databases. A few of the key developments in the IoT Vital Signs Monitoring Devices market are:

- Masimo, a prominent player in patient monitoring, received FDA approval for its MightySat Medical, making it the world's first over-the-counter (OTC) fingertip pulse oximeter. This is a significant development as it greatly expands access to medical-grade vital sign monitoring for consumers, facilitating remote patient monitoring and self-management for conditions where oxygen saturation is a key indicator. (Source: Masimo, Company Website, February 2024)

- GE HealthCare received US FDA 510(k) clearance for its CARESCAPE Canvas patient monitoring platform. This platform provides a unified and scalable solution for precise, flexible patient care, emphasizing connectivity and adaptability across various healthcare settings, making it a key offering in the vital signs monitoring market. (Source: GE Healthcare, Press Release, April 2023)

Key Sources Referred:

- World Health Organization (WHO)

- The World Bank Group

- Eurostat

- United Nations Department of Economic and Social Affairs

- National Council of Aging (NCOA)

- Worldometer

- Health America

- International Bar Association

- International Trade Administration