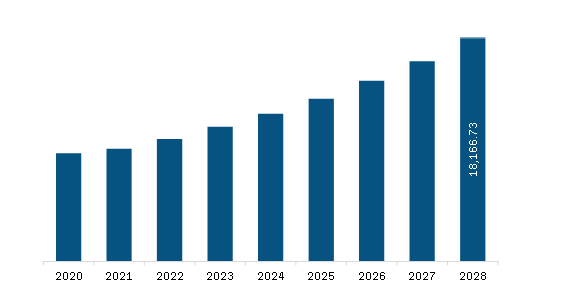

The Asia Pacific advanced composites market is expected to grow from US$ 9,990.80 million in 2022 to US$ 18,166.73 million by 2028. It is estimated to grow at a CAGR of 10.5% from 2022 to 2028.

Rise in Adoption of Biocomposites is Fuelling Asia Pacific Advanced Composites Market

Bio-based polymer matrices are environment-friendly and are the subject of extensive research in various fields. Bio-based matrices are also lightweight and exhibit long-term sustainability, which drives their use in commercial applications. Further, the easy availability of natural raw materials to produce bio-based resin is fueling its supply and demand. Bio-based matrices and biocomposites are employed in several secondary applications in the aerospace, automobiles, packaging, electronics, and construction sectors. In the construction industry, biocomposites are generally used to produce doors, windows, terrace decking, insulation material, and acoustic components. According to the report from the Global Alliance for Building and Construction, construction is one of the most harmful sectors to the environment. The study conducted by the alliance at the end of 2019 stated that the construction sector is responsible for 39% of the carbon dioxide emissions dispersed in the environment, 36% of the consumption of energy, and 50% of the extraction of raw materials. Conventional construction materials are highly resource- and energy-intensive. Hence, owing to the rising concern and awareness about the social and environmental impacts of conventional building materials, manufacturers of composites are shifting toward environment-friendly raw materials. Thus, the growing adoption of bio-based matrices or resins, sourced from carbohydrates, vegetable fats and oils, starch, bacteria, and other biological materials, over petroleum-derived plastic matrices is expected to emerge as an important trend in the Asia Pacific advanced composites market during the forecast period.

Asia Pacific Advanced Composites Market Overview

The Asia Pacific advanced composites market is segmented into China, Japan, India, Australia, South Korea, and the Rest of Asia Pacific. In 2021, Asia Pacific holds the largest share of the global advanced composites market. The market growth in the region is attributed to the development of various end-use industries, including automotive, wind energy, marine, electrical & electronics, and construction. Asia Pacific is a hub for automotive manufacturing with a large presence of international and domestic players operating in the region. According to a report published by the China Passenger Car Association, in 2022, Tesla Inc delivered 83,135 made-in-China electric vehicles, indicating growth in sales of electric vehicles compared to 2021. As per the International Organization of Motor Vehicle Manufacturers report, in 2021, various countries in Asia Pacific produced ~46.73 million units of motor vehicles. Advanced composites are used in various automotive parts to reduce tooling costs and improve design flexibility for manufacturers, while enhancing fuel efficiency and overall driving experience for the consumer by reducing noise and vibration. Such benefits of advanced composites, coupled with the growing automotive industry, propel the market growth.

Asia Pacific Advanced Composites Market Revenue and Forecast to 2028 (US$ Million)

Asia Pacific Advanced Composites Market Segmentation

Based on fiber type, the Asia Pacific advanced composites market is segmented into carbon fiber composites, aramid fiber composites, glass fiber composites, and others. The carbon fiber composites segment held the largest share of the Asia Pacific advanced composites market in 2022.

Based on matrix type, the Asia Pacific advanced composites market is segmented into epoxy resin, phenolics, polyester resin, polyurethane resin, polyphenylene sulfide (PPS), polyetherimide (PEI), and others. The epoxy resin segment held the largest share of the Asia Pacific advanced composites market in 2022.

Based on end-use industry, the Asia Pacific advanced composites market is segmented into aerospace & defense, automotive, wind energy, building & construction, electrical & electronics, and others. The aerospace & defense segment held the largest share of the Asia Pacific advanced composites market in 2022.

Based on country, the Asia Pacific advanced composites market has been categorized into China, India, Japan, South Korea, Australia, and the Rest of Asia Pacific. Our regional analysis states that China dominated the Asia Pacific advanced composites market in 2022.

Avient Corp, Ensinger GmbH, Johns Manville Corp, Mitsubishi Chemical Corp, Owens Corning, SGL Carbon SE, Solvay SA, Teijin Ltd, and Toray Industries Inc are the leading companies operating in the Asia Pacific advanced composites market.

Asia Pacific Advanced Composites Market Strategic Insights

Get more information on this report

Asia Pacific Advanced Composites Market Segmentation Analysis

Asia Pacific Advanced Composites Market Report Highlights

Asia Pacific Advanced Composites Report Scope

Report Attribute

Details

Market size in 2022

US$ 9,990.80 Million

Market Size by 2028

US$ 18,166.73 Million

CAGR (2022 - 2028)

10.5%

Historical Data

2020-2021

Forecast period

2023-2028

Segments Covered

By Fiber Type

Carbon Fiber Composites

Aramid Fiber Composites

Glass Fiber Composites

By Matrix Type

Epoxy Resin

Phenolics

Polyester Resin

Polyurethane Resin

Polyphenylene Sulfide

Polyetherimide

By End-Use Industry

Aerospace & Defense

Automotive

Wind Energy

Building & Construction

Electrical & Electronics

Regions and Countries Covered

Asia-Pacific

China, India, Japan, Australia, Rest of Asia-Pacific

Market leaders and key company profiles

Avient Corp

Ensinger GmbH

Johns Manville Corp

Mitsubishi Chemical Corp

Owens Corning

SGL Carbon SE

Solvay SA

Teijin Ltd

Toray Industries Inc

Get more information on this report

Asia Pacific Advanced Composites Market Country and Regional Insights

Get more information on this report

Identical Market Reports with other Region/Countries

The List of Companies - Asia Pacific Advanced Composites Market

Avient CorpEnsinger GmbHJohns Manville CorpMitsubishi Chemical CorpOwens CorningSGL Carbon SESolvay SA Teijin Ltd Toray Industries Inc

Frequently Asked Questions

How big is the Asia Pacific Advanced Composites Market?

The Asia Pacific Advanced Composites Market is valued at US$ 9,990.80 Million in 2022, it is projected to reach US$ 18,166.73 Million by 2028.

What is the CAGR for Asia Pacific Advanced Composites Market by (2022 - 2028)?

As per our report Asia Pacific Advanced Composites Market, the market size is valued at US$ 9,990.80 Million in 2022, projecting it to reach US$ 18,166.73 Million by 2028. This translates to a CAGR of approximately 10.5% during the forecast period.

What segments are covered in this report?

The Asia Pacific Advanced Composites Market report typically cover these key segments-

End-Use Industry (Aerospace & Defense, Automotive, Wind Energy, Building & Construction, Electrical & Electronics)

What is the historic period, base year, and forecast period taken for Asia Pacific Advanced Composites Market?

The historic period, base year, and forecast period can vary slightly depending on the specific market research report. However, for the Asia Pacific Advanced Composites Market report:

Historic Period : 2020-2021

Base Year : 2022

Forecast Period : 2023-2028

Who are the major players in Asia Pacific Advanced Composites Market?

The Asia Pacific Advanced Composites Market is populated by several key players, each contributing to its growth and innovation. Some of the major players include:

Avient Corp

Ensinger GmbH

Johns Manville Corp

Mitsubishi Chemical Corp

Owens Corning

SGL Carbon SE

Solvay SA

Teijin Ltd

Toray Industries Inc

Who should buy this report?

The Asia Pacific Advanced Composites Market report is valuable for diverse stakeholders, including:

Investors: Provides insights for investment decisions pertaining to market growth, companies, or industry insights. Helps assess market attractiveness and potential returns.

Industry Players: Offers competitive intelligence, market sizing, and trend analysis to inform strategic planning, product development, and sales strategies.

Suppliers and Manufacturers: Helps understand market demand for components, materials, and services related to concerned industry.

Researchers and Consultants: Provides data and analysis for academic research, consulting projects, and market studies.

Financial Institutions: Helps assess risks and opportunities associated with financing or investing in the concerned market.

Essentially, anyone involved in or considering involvement in the Asia Pacific Advanced Composites Market value chain can benefit from the information contained in a comprehensive market report.

Get Free Sample For Asia Pacific Advanced Composites Market

Get Free Sample For Asia Pacific Advanced Composites Market