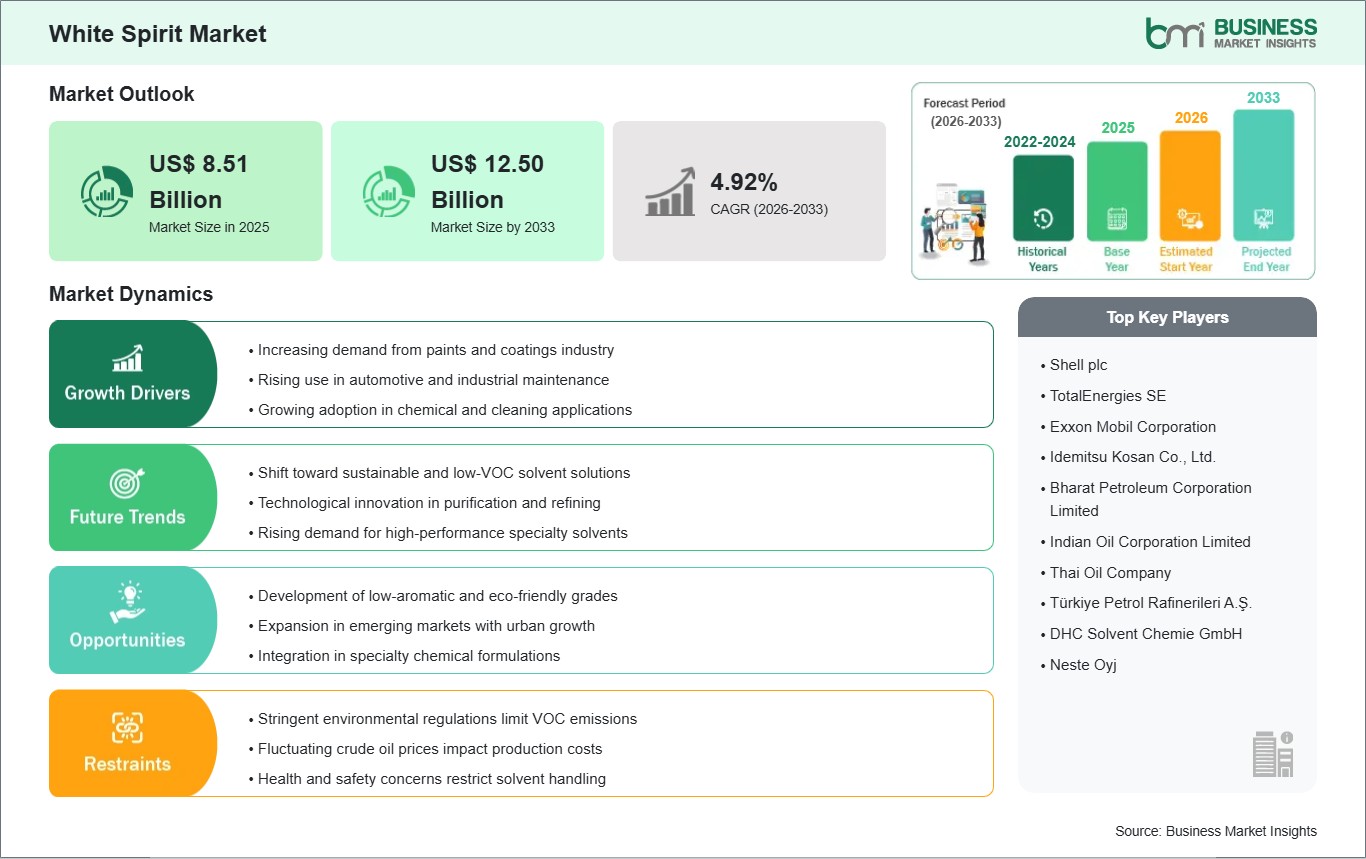

Increasing Demand from Paints and Coatings Industry

The paints and coatings industry is a major end use segment driving steady consumption of white spirit, due to its widespread role as a solvent in formulation, thinning, and surface preparation processes. Its capability to work well with alkyd paints and provide benefits in terms of improved application characteristics makes it more popular among paint manufacturers. Despite the rise of water-based technologies, there is still some use of solvent-based paints in those applications that require better performance. Thus, a steady demand for white spirit can be guaranteed in industrial, decorative, and protective paints.

Demand is reinforced by ongoing activity in construction, infrastructure development, automotive refinishing, and industrial maintenance. The key applications are characterized by heavy usage of paints, which depend largely on solvent-based formulations, especially in places where economic considerations take precedence over the fast adoption of newer chemistries. Regular repainting and maintenance needs within existing installations keep the substance in demand despite the regulatory push toward reduced emissions.

The paints and coatings industry will continue to anchor white spirit demand, although usage intensity may gradually moderate as formulation technologies evolve. It is anticipated that growth in protective and maintenance coatings will offset partial substitution, but manufacturers will be concerned with finding a balance between performance and regulatory requirements. This trend is more likely to redirect demand rather than eliminate consumption.

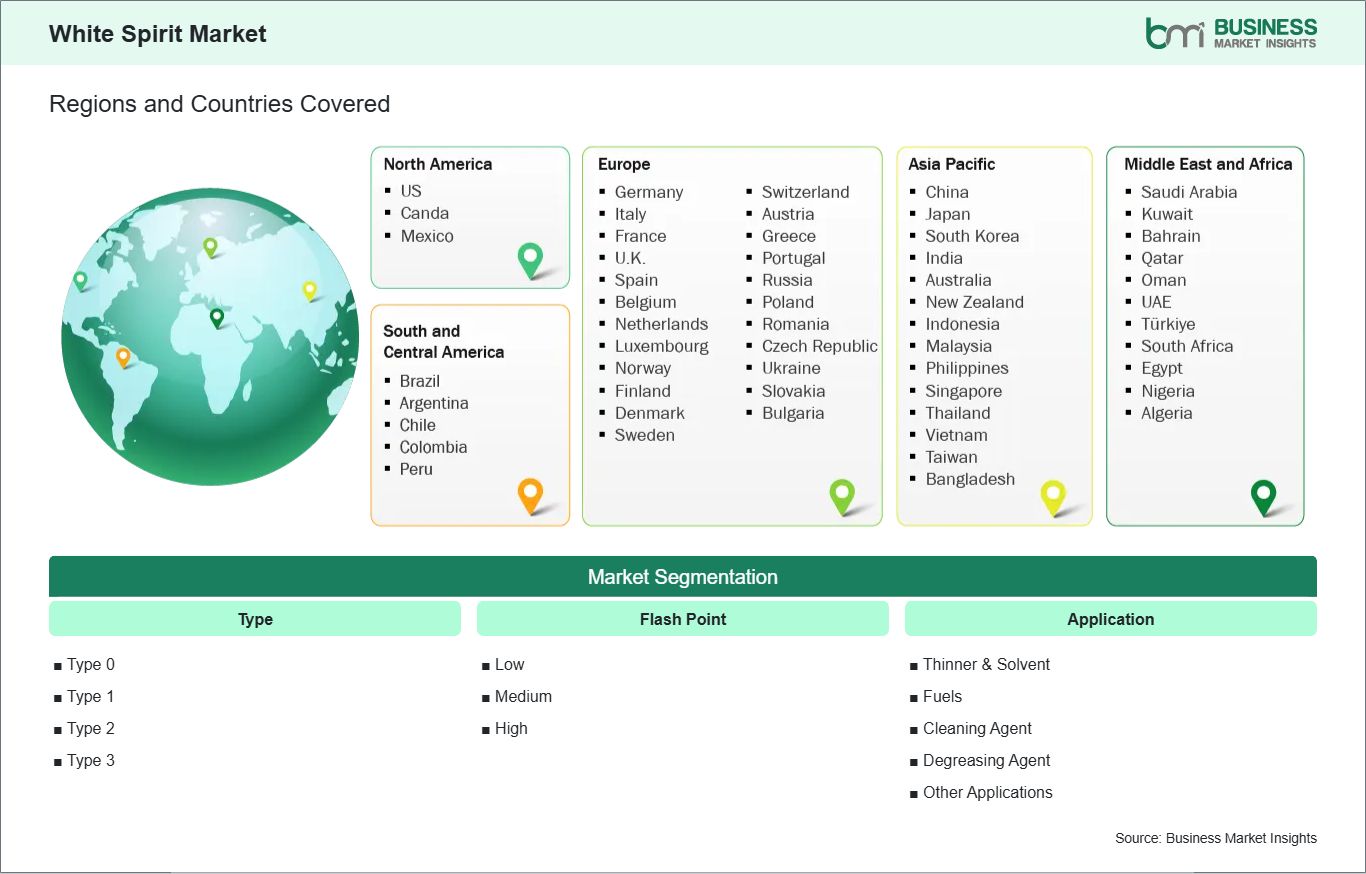

Development of Low-Aromatic and Eco-Friendly Grades

Increasing emphasis on environmental compliance and occupational safety is accelerating the shift toward low-aromatic and eco-friendly white spirit grades across industrial solvent applications. These formulations reduce hazardous aromatic content, enabling manufacturers and end users to meet tightening emission thresholds while improving handling safety in workplace environments. As regulatory frameworks are becoming more stringent, product substitution is gaining momentum in coatings, adhesives, degreasing, and cleaning applications, prompting refiners to modify production processes and invest in cleaner separation and hydrogenation technologies.

Regulatory bodies in key consuming markets have reduced the use of VOC-based solvents, thus promoting more environmentally friendly alternatives in their respective industries. This trend has transformed purchasing criteria such that performance and environmental footprint carry more weight than cost savings. It is contributing to growing preference for high-grade solvents with low levels of aromatics, in addition to advancements in process efficiency for ensuring consistency and stability of the final output.

Over the coming years, the development of eco-friendly white spirit grades is expected to become a central competitive differentiator for producers. Companies that align product portfolios with evolving sustainability standards will strengthen market positioning and secure long-term contracts with regulated industries. Continued tightening of environmental norms will likely sustain this transition, reducing reliance on conventional solvent formulations in favor of cleaner, performance-optimized alternatives.