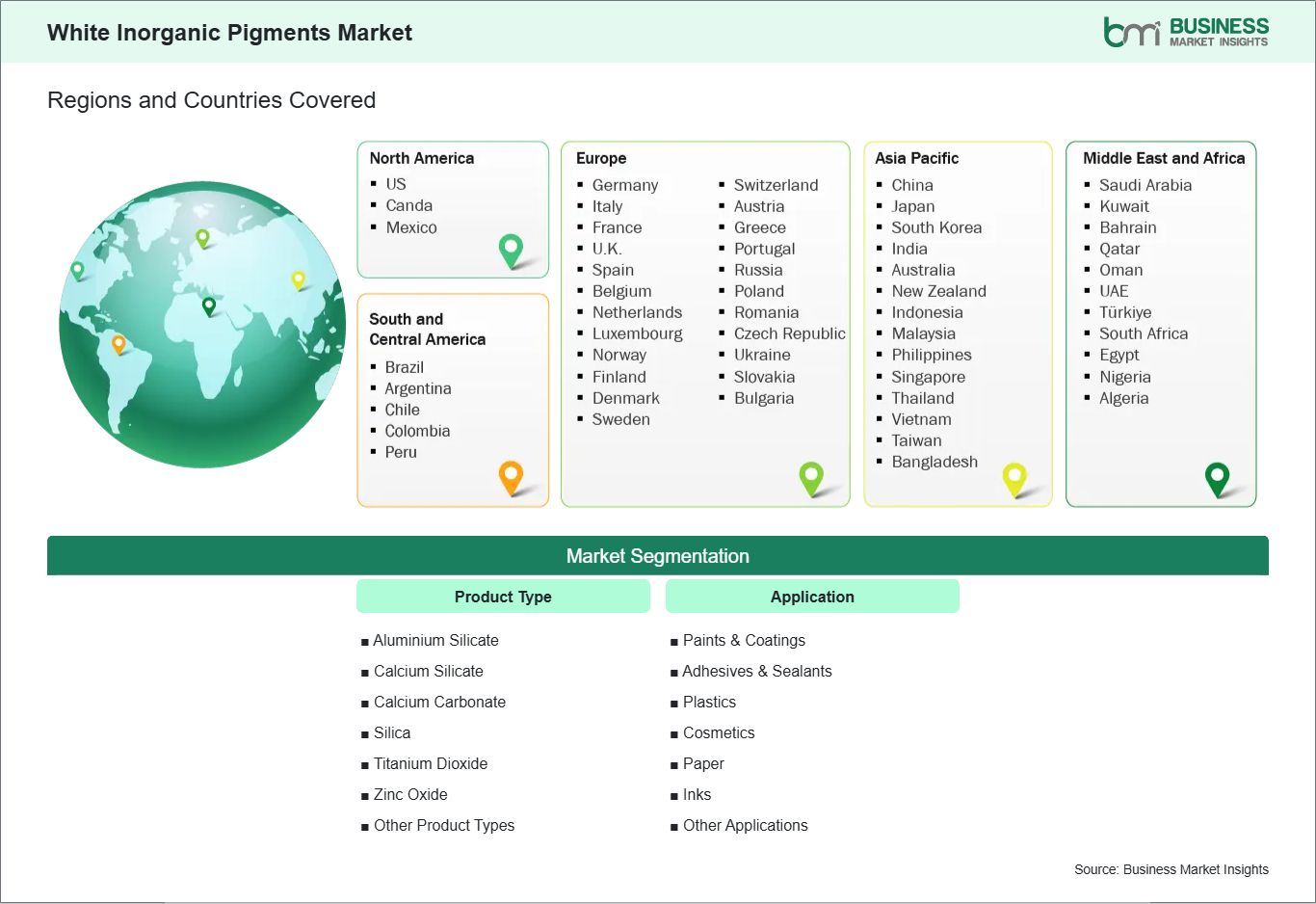

The geographical scope of the White Inorganic Pigments Market report is divided into North America, Asia Pacific, Europe, Middle East & Africa, and South & Central America. North America held the largest share in 2025.

The North American market for white inorganic pigments presently leads the global white inorganic pigments market because its established coatings, plastics and construction sectors require pigments that meet performance standards and regulatory needs. The United States and Canada use titanium dioxide as their main pigment because it provides better opacity and brightness and UV stability than other pigments in architectural coatings, automotive finishes and industrial applications. The demand exists because environmental regulations require low-VOC durable coatings, and consumers want products that maintain high quality through prolonged use.

The European market stands as the next major market because sustainability efforts and urban development projects create demand for white inorganic pigments in paints and plastics, and specialized industrial uses. Germany, France and the U.K. concentrate on developing high-performance pigments that produce energy-saving reflective coatings that withstand the test of time while adhering to REACH and environmental regulations.

The Asia Pacific region experiences strong demand for white inorganic pigments because its industrial and urban development, automotive, packaging, and construction industries create demand for these pigments in China, India and Japan, where manufacturers require products to have consistent quality, full opacity and UV protection capabilities. The Middle East and Africa market expansion is happening at a slow pace because infrastructure projects, industrial coatings and new manufacturing centers create chances for pigment use, which depends on environmental conditions and the presence of top-quality materials.

South and Central America experience continuous growth of white inorganic pigments, which Brazil and Mexico drive for use in residential and commercial construction, automotive coatings and packaging applications, because infrastructure development and durable material investment have increased.

All regions of the market develop through the combination of governmental regulations, industrial expansion, urban development and new technological advancements in pigment production and design. The North American market maintains its leading position because of its established industrial base, research and development capabilities and ability to meet regulations, while emerging markets adopt white inorganic pigments because of their long-lasting quality, dense covering ability and positive environmental impact, which creates a worldwide market system that exists in various regions.