01

Market Summery

Executive Summary and Global Market Analysis

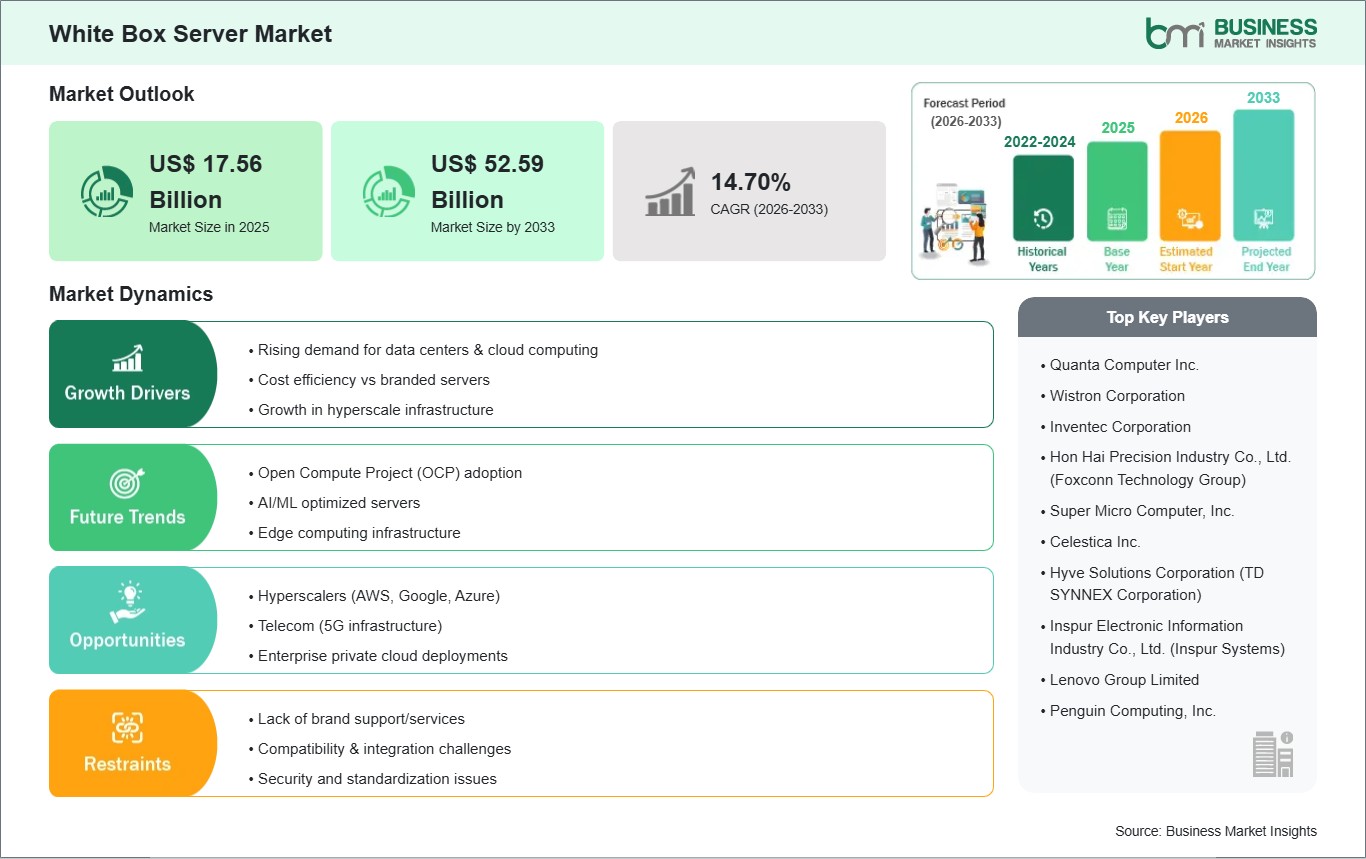

White box servers refer to unbranded, highly customizable data center servers constructed using off-the-shelf components from diverse original design manufacturers (ODMs). By decoupling hardware innovation from legacy brand constraints, these systems allow for the precise specification of processor architectures, memory capacity, and storage configurations. This technology is fundamental to the operational architecture of hyperscale cloud providers and internet giants that prioritize cost optimization and hardware transparency. Market expansion is being propelled by the rapid proliferation of artificial intelligence (AI) and machine learning workloads, the global shift toward software-defined infrastructure, and the increasing institutional adoption of open hardware standards such as the Open Compute Project (OCP).

However, several factors may restrain market progression. The high capital intensity associated with building and maintaining massive, standardized server fleets remains a significant hurdle for organizations lacking the scale of global cloud providers. The industry also faces technical challenges regarding vendor support limitations, as white box hardware typically lacks the comprehensive on-site service and global warranty packages provided by traditional branded manufacturers. Additionally, persistent concerns regarding firmware integrity and the complexity of managing multi-vendor component lifecycles can create operational risk for enterprise IT departments. These hurdles, compounded by a global scarcity of in-house technical expertise required to design and deploy non-proprietary hardware, increase the total cost of ownership for smaller institutions.

Despite these hurdles, the market outlook remains favorable. Opportunities are emerging through the adoption of specialized GPU-accelerated and liquid-cooled configurations, which are essential for managing the extreme thermal and computational demands of large-scale AI training. The expansion of edge computing is gaining traction; the demand for compact, ruggedized white box units is rising to support low-latency processing for 5G telecommunications and industrial automation. Furthermore, the growth of non-x86 architectures, including ARM and RISC-V processors, aligns with global goals for hardware sovereignty and energy efficiency in next-generation data centers. Collectively, these innovations position the white box server industry for sustained long-term development as a cornerstone of the modern, agile, and decentralized digital infrastructure.

03

Segment Analysis

White Box Server Market Segmentation

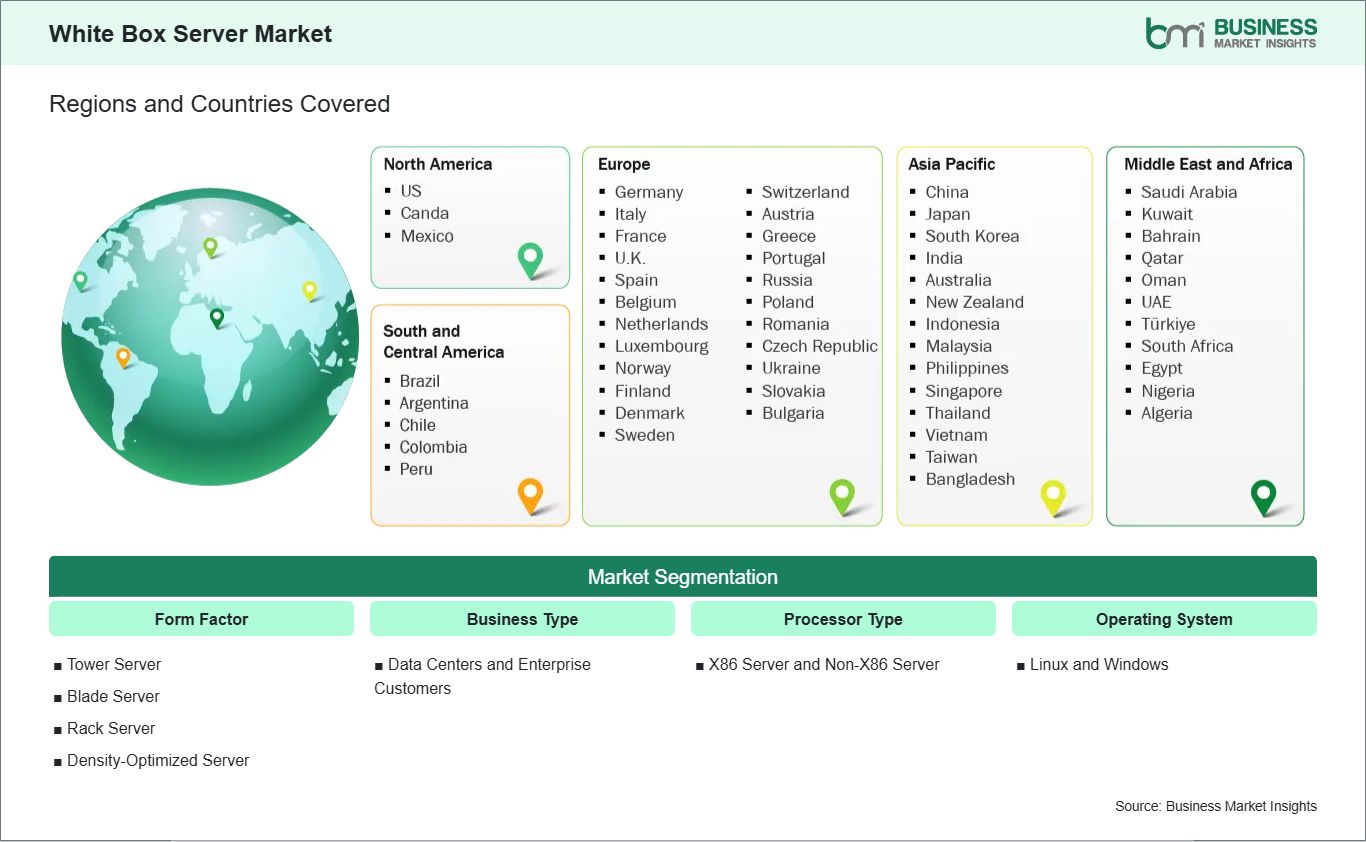

Key segments that contributed to the derivation of the White Box Server market analysis are form factor, business type, processor type, and operating system.

- By Form Factor, the market is segmented into Tower Server, Blade Server, Rack Server, and Density-Optimized Server.

- By Business Type, the market is divided into Data Centers and Enterprise Customers.

- By Processor Type, the market is categorized into X86 Server and Non-X86 Server.

- By Operating System, the market is segmented into Linux and Windows.

04

Market Forces

White Box Server Market Drivers and Opportunities

Rising Demand for Cost Efficiency, Customization, and Cloud Expansion

The white box server market is being driven by the growing need for cost‑effective, customizable, and scalable computing solutions across industries such as cloud services, telecommunications, and enterprise IT. Unlike branded servers, white box servers are built with off‑the‑shelf components, offering flexibility and affordability without vendor lock‑in. The rapid expansion of cloud computing and hyperscale data centers is amplifying adoption, as service providers seek to optimize costs while maintaining performance. Telecom operators deploying 5G infrastructure are also fueling demand, leveraging white box servers for network functions virtualization (NFV) and edge computing. Enterprises are increasingly adopting these systems to support big data analytics, AI workloads, and high‑performance computing, where customization and scalability are critical. Additionally, the growing emphasis on open standards and software‑defined architectures is reinforcing adoption, as white box servers integrate seamlessly with modern IT ecosystems. Collectively, cost efficiency, customization, and cloud expansion are propelling sustained growth in the global white box server market.

Rising Integration of AI, Edge Computing, and Open-Source Ecosystems

Opportunities in the white box server market are expanding through the integration of artificial intelligence, edge computing, and open-source ecosystems. AI‑enabled workloads are opening lucrative opportunities, as white box servers provide the flexibility to tailor hardware configurations for machine learning and deep learning applications. Edge computing is gaining traction, with white box servers deployed in distributed environments to process data closer to the source, reducing latency and improving efficiency in IoT and 5G applications. The growing emphasis on open-source platforms and software‑defined infrastructure is fueling demand for interoperable white box solutions that support innovation and reduce dependency on proprietary systems.

Emerging applications in blockchain, cybersecurity, and content delivery networks are also driving adoption, as organizations seek scalable, cost‑effective computing power. Additionally, sustainability trends are encouraging the development of energy‑efficient white box servers that align with global environmental goals. Vendors who focus on AI‑ready, edge‑optimized, and open source‑friendly solutions are well‑positioned to capture growth. The convergence of AI, edge computing, and open ecosystems underscores a transformative trajectory for the global white box server market.

05

Size and Share Analysis

White Box Server Market Size and Share Analysis

The White Box Server market demonstrates steady growth, with size and share analysis revealing evolving trends and competitive positioning among key players. The report examines subsegments categorized within form factor, business type, processor type, and operating system, offering insights into their contribution to overall market performance.

Based on Form Factor, the Rack Server subsegment holds the primary market presence. Rack servers are indispensable for data centers, offering scalability, efficient space utilization, and high performance. The Tower Server subsegment is essential for small enterprises and branch offices, providing cost‑effective solutions with simpler deployment. The Blade Server subsegment anchors demand in enterprises requiring modularity and high‑density computing, enabling streamlined management and reduced footprint. The Density‑Optimized Server subsegment is critical for hyperscale environments, offering maximum compute power per square foot, ideal for cloud and big data workloads.

07

Report Coverage

White Box Server Market Report Coverage and Deliverables

The "White Box Server Market Size and Forecast (2022 - 2033)" report provides a detailed analysis of the market covering below areas:

- White Box Server market size and forecast at global, regional, and country levels for all market segments covered under the scope

- White Box Server market trends, as well as drivers, restraints, and opportunities

- White Box Server market analysis covering key trends, global and regional framework, major players, regulations, and recent developments

- Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments for the White Box Server market

- Detailed company profiles, including SWOT analysis

08

Geographic Insights

White Box Server Market Geographic Insights

The geographical scope of the White Box Server market report is divided into five regions: North America, Asia Pacific, Europe, Middle East & Africa, and South & Central America.

North America maintains a preeminent position within the global industry, a status reinforced by the presence of primary hyperscale cloud providers and an extensive network of sophisticated data centers. The regional landscape is characterized by high-density investments in the United States and Canada, where the transition toward Customizable Hardware and Open Compute Project (OCP) Standards has become a strategic priority. This market leadership is further supported by the dominance of major technology pioneers who utilize white box architectures to reduce capital expenditure while maintaining granular control over server specifications for high-performance computing tasks.

Technological progression in the United States and Canada is largely driven by a decisive shift toward AI-Driven Workloads and GPU-Dense Server Configurations. These advanced systems utilize off-the-shelf, high-performance components to support large-scale machine learning, deep learning, and data-intensive analytical applications. Furthermore, the region is witnessing an increasing utilization of Density-Optimized Rack Servers, as operators seek to maximize the computational power of their existing facility footprints while reducing energy consumption. This focus on Hardware Agility allows North American institutions to bypass traditional vendor lock-in, enabling a more rapid deployment of specialized infrastructure for next-generation digital services.

10

Industry Activity

Recent Developments

The White Box Server market is evaluated by gathering qualitative and quantitative data post primary and secondary research, which includes important corporate publications, association data, and databases. A few of the key developments in the White Box Server market are:

- In April 2025, Fujitsu expanded its strategic collaboration with Supermicro to launch the PRIMERGY GX2570 M8S, an OEM Supermicro server featuring NVIDIA HGX B200 GPUs in air‑cooled and liquid‑cooled models. The partnership combines Supermicros high‑performance servers with Fujitsu’s maintenance, integrated management tools, and Takane LLM to deliver a comprehensive generative AI platform. This collaboration reinforces the role of white box servers in powering secure, scalable AI infrastructure for enterprise adoption.

- In October 2024, Supermicro launched liquid‑cooled SuperClusters powered by NVIDIA GB200 NVL72, delivering exascale AI computing in a single rack. While positioned as an AI infrastructure breakthrough, these systems are part of Supermicros broader server portfolio, directly reinforcing its role as a leading white box server vendor. By integrating advanced cooling, GPU density, and sustainable design, the launch strengthens the competitiveness of white box servers in next‑generation data centers.

11

Trust & Transparency

Research Methodology

The market analysis combines proprietary research with secondary data from government agencies, company disclosures, regulatory filings, industry databases and expert interviews. Market estimates are validated through data triangulation, cross-market benchmarking and analyst

review.

View Full Research Methodology

Key Sources Referred:

World Bank - Global Trade Indicators World Trade Organization (WTO) International Monetary Fund (IMF) International Trade Administration (ITA) Company Websites Company Annual Reports Company Investor Presentations