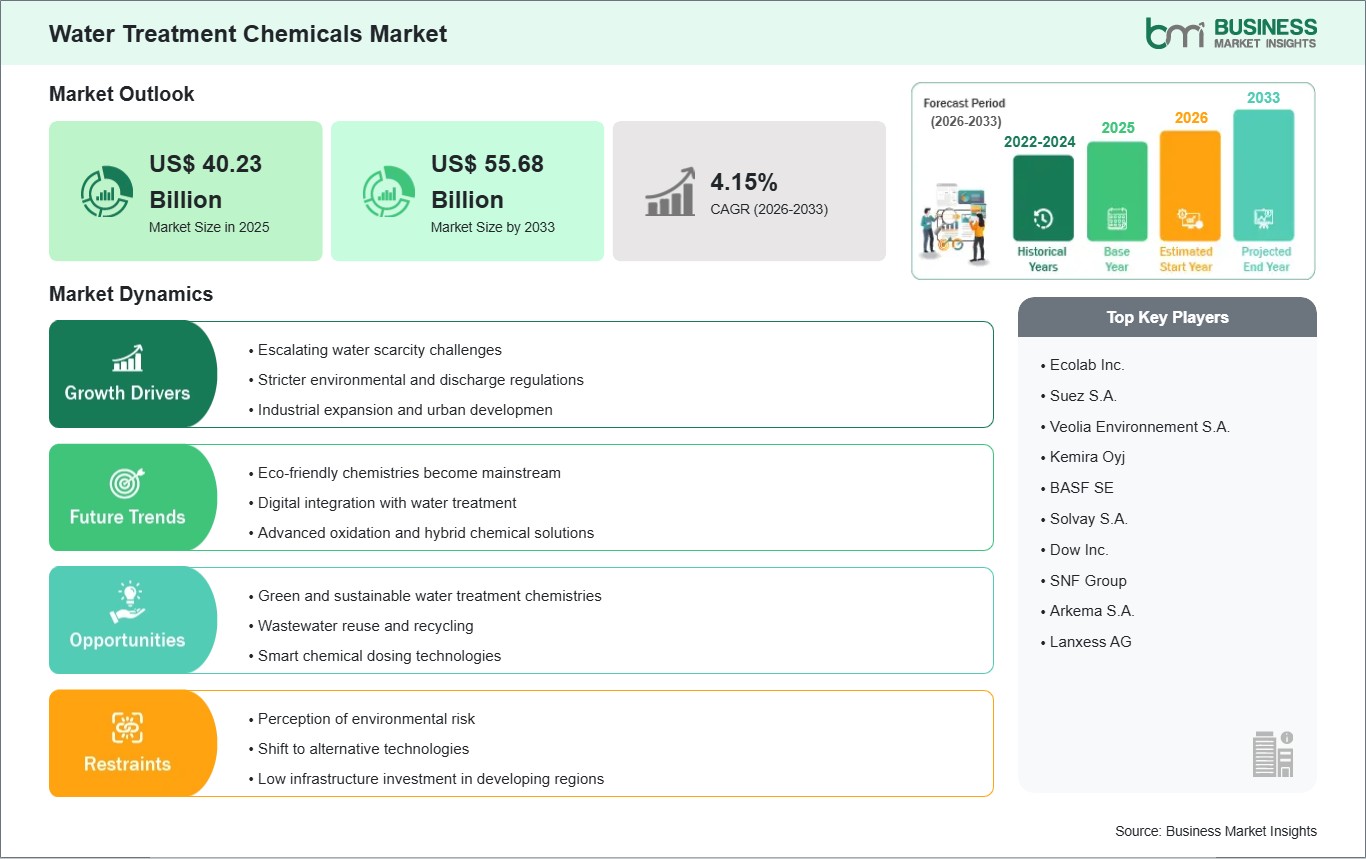

The Water Treatment Chemicals Market size is expected to reach US$ 55.68 billion by 2033 from US$ 40.23 billion in 2025. The market is estimated to record a CAGR of 4.15% from 2026 to 2033.

Executive Summary and Global Market Analysis:

The global water treatment chemicals market is a cornerstone of modern water management, addressing challenges from municipal drinking water safety to industrial process efficiency. These chemicals—including coagulants, disinfectants, flocculants, and scale inhibitors—are critical for ensuring water quality, controlling microbial contamination, and optimizing treatment operations. A primary factor driving global growth is the increasing demand for safe and reliable water sources amid population growth, urbanization, and industrial expansion. Heightened regulatory standards and public health awareness further accelerate the adoption of advanced chemical solutions across both developed and emerging regions. Another key driver is industrial water reuse and wastewater management initiatives, particularly in sectors such as power generation, manufacturing, and oil & gas. Companies are investing in specialized chemical formulations to improve process efficiency while minimizing environmental impact.

However, the market faces constraints, including fluctuating raw material costs and environmental concerns associated with chemical overuse or improper disposal. Manufacturers are responding by developing eco-friendly and low-residue formulations that balance performance with sustainability. Overall, the global water treatment chemicals market reflects a convergence of regulatory pressure, technological advancement, and the growing need for reliable water quality, creating a dynamic landscape where innovation is critical to meeting regional and industrial demands.

Water Treatment Chemicals Market - Strategic Insights:

Get more information on this report

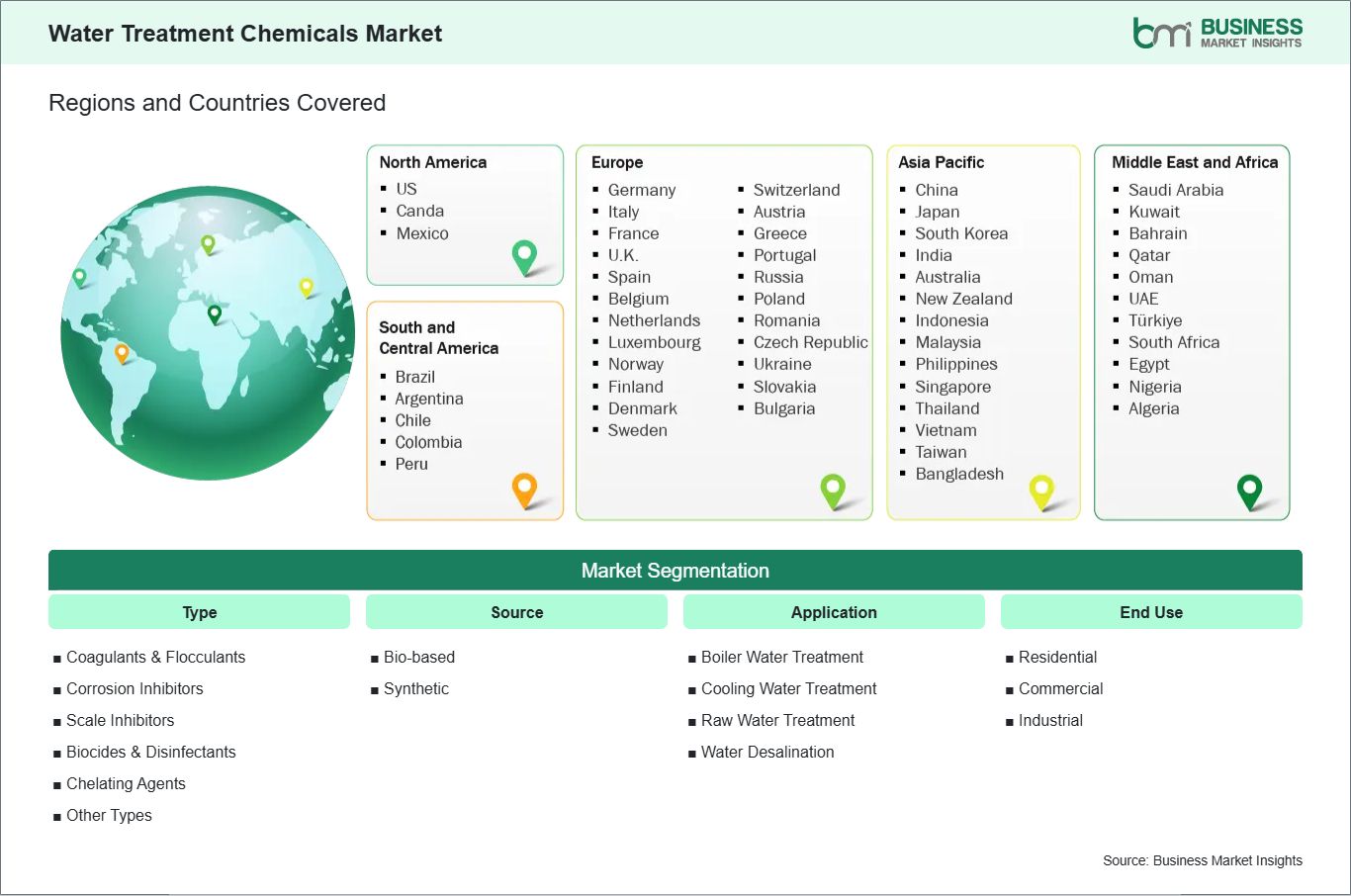

Water Treatment Chemicals Market Segmentation Analysis:

Key segments that contributed to the derivation of the Water treatment chemicals market analysis are type, source, application and end use

By type, the water treatment chemicals market is segmented into coagulants & flocculants, corrosion inhibitors, scale inhibitors, biocides & disinfectants, chelating agents, and others. The coagulants & flocculants segment dominated the market in 2025.

By source, the water treatment chemicals market is segmented into bio-based and synthetic. The synthetic segment dominated the market in 2025.

By application, the water treatment chemicals market is segmented into boiler water treatment, cooling water treatment, raw water treatment, and water desalination. The raw water treatment segment dominated the market in 2025.

In terms of end use, the water treatment chemicals market is segmented into residential, commercial, and industrial. The industrial segment dominated the market in 2025.

Water Treatment Chemicals Market Drivers and Opportunities:

Escalating Water Scarcity Challenge

The water scarcity in the Asia Pacific region has led to increased water treatment chemical demand as governments and industries are seeking ways to make the best use of the available water resources. India and China have witnessed alarming depletion in their groundwater tables, and it has recently been estimated that the groundwater depletion in the northwestern parts of India is as high as 1 meter per year. In this context, water treatment chemicals are being used in the Asia Pacific region to enhance the performance of water treatment facilities, with coagulants, flocculants, and pH stabilizers being dosed in water treatment facilities in water-scarce cities like Delhi, Bangkok, and Manila.

The industrial sector is also one of the major sectors contributing to the increasing chemical demand, especially in sectors with process water withdrawals that are strictly controlled due to water scarcity concerns. In the major industrial centers of Southeast Asia, water treatment chemicals are being employed in the treatment of industrial effluents in the production of electrical devices in Malaysia and Vietnam. For example, in the semiconductor industry in these countries, water treatment chemicals are being used in the treatment of industrial wastewater, which is then recycled and reused in the semiconductor fabrication process to achieve the strict discharge standards and internal water recycling goals. This has resulted in the reduction of water intake by 30-40%.

The agriculture sector, which consumes the largest percentage of water in the region, is also turning to the use of wastewater treatment chemicals to address the water scarcity concerns in the region, especially during the dry season. In the irrigation systems of the Murray-Darling Basin in Australia and the rice fields of Bangladesh, wastewater treatment chemicals are being employed in the treatment of wastewater and the blending of this water with fresh water for irrigation purposes.

Green And Sustainable Water Treatment Chemistries

Environmental policies and trends in the Asian Pacific region favor the adoption of green and sustainable water treatment chemicals. Incentivization policies have been implemented by governments in Japan and Korea for chemical companies that have shown lower toxicity and higher biodegradability. This has led to the adoption of alternative chemicals to traditional chemicals. In Japan, for instance, in its advanced wastewater treatment facilities, bio-polymers obtained from plant-based materials are being used to replace synthetic polyacrylamide-based flocculants.

Industrial sectors are also embracing sustainable chemistries in order to conform to global ESG standards. Large-scale food and beverage companies in China and India are now reformulating their water treatment protocols to replace harmful biocides with environmentally friendly disinfectants such as hydrogen peroxide-based disinfection chemistries and ultraviolet activation chemistries that do not generate harmful byproducts in water treatment plants. These environmentally friendly water treatment chemistries are particularly prevalent in water treatment plants serving export markets that have high standards for water quality.

With regard to water utilities, there is an increased emphasis on circular economy concepts that incorporate environmentally friendly water treatment chemicals as part of overall upgrades to water treatment plants. For example, in Seoul, South Korea, as well as Singapore, water utilities are modernizing water treatment plants with biological nutrient removal systems that utilize natural microbial processes assisted by minimal chemical dosing. This results in water treatment chemical intensity savings of over 20% while simultaneously providing better water quality and cost savings. These innovations represent a larger trend in regional water treatment chemistries that incorporate environmentally friendly chemistries in water treatment plants..

Water Treatment Chemicals Market Size and Share Analysis:

The global Water treatment chemicals market is experiencing steady growth, with market size and share analysis reflecting evolving treatment preferences and competitive dynamics among key players. The report evaluates important subsegments categorized within type, source, application and end use highlighting their respective contributions to overall market performance.

By type, the coagulants & flocculants subsegment dominated the market in 2025 because they are critical in removing suspended solids, turbidity, and colloidal impurities from water. Their role in both municipal and industrial water treatment ensures consistent and high-volume demand, making them the most widely used chemical type.

By source, the synthetic segment subsegment dominated the market in 2025 because synthetic chemicals account for the largest share as they offer higher performance, reliability, and scalability compared to bio-based alternatives. They are cost-effective, consistent in quality, and widely available, making them the preferred choice for large-scale industrial and municipal water treatment.

By application, the raw water treatment subsegment dominated the market in 2025 because it is the first and most essential step in water processing, ensuring that surface or groundwater meets quality standards. High chemical consumption at this stage drives dominance over other applications like boiler or cooling water treatment.

By end use, the industrial subsegment dominated the market in 2025 because industries such as power, oil & gas, and chemicals require large volumes of water treatment chemicals for corrosion control, scaling prevention, and efficiency in high-throughput systems.

Water Treatment Chemicals Market Report Highlights:

Australia, China, India, Japan, South Korea, Indonesia, Malaysia, Philippines, Singapore, Thailand, Vietnam, Bangladesh, New Zealand, Taiwan

South and Central America

Brazil, Argentina, Peru, Chile, Colombia

Middle East and Africa

Bahrain, Kuwait, Oman, Qatar, Saudi Arabia, United Arab Emirates, Turkiye, South Africa, Egypt, Algeria, Nigeria

Market leaders and key company profiles

Ecolab Inc.

Suez S.A.

Veolia Environnement S.A.

Kemira Oyj

BASF SE

Solvay S.A.

Dow Inc.

SNF Group

Arkema S.A.

Lanxess AG

Get more information on this report

Water Treatment Chemicals Market Report Coverage and Deliverables:

The "Water Treatment Chemicals Market Size and Forecast (2022 - 2033)" report provides a detailed analysis of the market covering below areas:

Water treatment chemicals market size and forecast at the regional and country levels for segments covered under the scope

Water treatment chemicals market trends, as well as drivers, restraints, and opportunities

Water treatment chemicals market analysis covering key trends, regional framework, major players, regulations, and recent developments

Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments for the water treatment chemicals market.

Detailed company profiles, including SWOT analysis

Water Treatment Chemicals Market Geographic Insights:

The geographical scope of the Water treatment chemicals market report is divided into: North America, Asia Pacific, Europe, Middle East & Africa, and South & Central America. North America held the largest share in 2025.

North America dominates the global water treatment chemicals market, driven by its mature water infrastructure, stringent regulatory frameworks, and high awareness of water quality standards. The region’s extensive municipal water systems rely heavily on chemical solutions for coagulation, disinfection, and scaling control to ensure public health and maintain compliance with environmental regulations. Industrial demand is also robust, particularly in sectors such as power, oil & gas, and food & beverage processing, where chemical treatments are crucial for process water management, corrosion control, and wastewater recycling.

The United States leads the region, propelled by investments in advanced treatment technologies and innovation in sustainable chemical formulations. Emphasis on green chemicals, low-chlorine alternatives, and multifunctional treatment agents highlights the market’s focus on environmental stewardship. Canada complements this growth through initiatives in water reuse, industrial effluent treatment, and infrastructure modernization.

North America’s dominance is reinforced by the integration of digital monitoring systems in water treatment processes, allowing real-time dosing and optimized chemical utilization. The combination of regulatory rigor, technological advancement, and diversified industrial applications positions North America as the global benchmark for water treatment, chemical adoption and innovation.

Get more information on this report

Water Treatment Chemicals Market Research Report Guidance:

The report includes qualitative and quantitative data in the water treatment chemicals market across type, source, te, application, endues, and geography.

The report starts with the key takeaways (chapter 2), highlighting the key trends and outlook of the Water treatment chemicals market.

Chapter 3 focuses on the research methodology of the study.

Chapter 4 includes ecosystem analysis.

Chapter 5 highlights the major industry dynamics in the water treatment chemicals market, including factors that are driving the market, prevailing deterrents, potential opportunities, as well as future trends. Impact analysis of these drivers and restraints is also covered in this section.

Chapter 6 discusses the Water treatment chemicals market scenario, in terms of historical market revenues, and forecast till the year 2033.

Chapters 7 to 11 cover the water treatment chemicals market segments by type, source, application, end use and geography across North America, Europe, Asia Pacific, the Middle East and Africa, and South and Central America. They cover the market revenue, forecast, and factors driving the market.

Chapter 12 describes the competitive analysis along with the heat map analysis for the key players operating in the market.

Chapter 13 describes the industry landscape analysis. It provides detailed descriptions of business activities such as market initiatives, new developments, mergers, and joint ventures globally, along with a competitive landscape.

Chapter 14 provides detailed profiles of the major companies operating in the water treatment chemicals market. Companies have been profiled on the basis of their key facts, business descriptions, products, financial overview, SWOT analysis, and key developments.

Chapter 15, i.e., the appendix, is inclusive of a brief overview of the company, list of abbreviations, and disclaimer.

Water Treatment Chemicals Market News and Key Development:

The water treatment chemicals market is evaluated by gathering qualitative and quantitative data post primary and secondary research, which includes important corporate publications, association data, and databases. A few of the key developments in the Water treatment chemicals market are:

In October 2025, Kemira Oyj announced that it will invest in a new activated carbon reactivation plant at its Helsingborg, Sweden site, strengthening its water treatment portfolio—particularly for the removal of micropollutants such as PFAS—which supports broader European (including Eastern Europe) water quality compliance and advanced treatment capabilities.

In April 2023, Veolia Water Technologies & Solutions and Locus Performance Ingredients announced that they would collaborate on developing new sustainable water and process treatment additives, advancing bio‑based water treatment chemical solutions in European markets.

In November 2024, Solenis completed its acquisition of BASF’s flocculant mining business (related water treatment chemical technologies) in the broader EMEA region, expanding its portfolio and capabilities in key chemicals used for treatment processes across Europe.

Key Sources Referred:

EU REACH RegulationEuropean Chemicals Agency (ECHA)World Health Organization (WHO)Clean Water Act (CWA)Environmental Protection Agency (EPACompany WebsitesCompany Annual ReportsCompany Investor Presentations

The List of Companies - Water Treatment Chemicals Market

Ecolab Inc.

Suez S.A.

Veolia Environnement S.A.

Kemira Oyj

BASF SE

Solvay S.A.

Dow Inc.

SNF Group

Arkema S.A.

Lanxess AG

Frequently Asked Questions

How big is the Water Treatment Chemicals Market?

The Water Treatment Chemicals Market is valued at US$ 40.23 Billion in 2025, it is projected to reach US$ 55.68 Billion by 2033.

What is the CAGR for Water Treatment Chemicals Market by (2026 - 2033)?

As per our report Water Treatment Chemicals Market, the market size is valued at US$ 40.23 Billion in 2025, projecting it to reach US$ 55.68 Billion by 2033. This translates to a CAGR of approximately 4.15% during the forecast period.

What segments are covered in this report?

The Water Treatment Chemicals Market report typically cover these key segments-

Type (Coagulants & Flocculants, Corrosion Inhibitors, Scale Inhibitors, Biocides & Disinfectants, Chelating Agents, Other Types)

Source (Bio-based, Synthetic)

Application (Boiler Water Treatment, Cooling Water Treatment, Raw Water Treatment, Water Desalination)

End Use (Residential, Commercial, Industrial)

What is the historic period, base year, and forecast period taken for Water Treatment Chemicals Market?

The historic period, base year, and forecast period can vary slightly depending on the specific market research report. However, for the Water Treatment Chemicals Market report:

Historic Period : 2022-2024

Base Year : 2025

Forecast Period : 2026-2033

Who are the major players in Water Treatment Chemicals Market?

The Water Treatment Chemicals Market is populated by several key players, each contributing to its growth and innovation. Some of the major players include:

Ecolab Inc.

Suez S.A.

Veolia Environnement S.A.

Kemira Oyj

BASF SE

Solvay S.A.

Dow Inc.

SNF Group

Arkema S.A.

Lanxess AG

Who should buy this report?

The Water Treatment Chemicals Market report is valuable for diverse stakeholders, including:

Investors: Provides insights for investment decisions pertaining to market growth, companies, or industry insights. Helps assess market attractiveness and potential returns.

Industry Players: Offers competitive intelligence, market sizing, and trend analysis to inform strategic planning, product development, and sales strategies.

Suppliers and Manufacturers: Helps understand market demand for components, materials, and services related to concerned industry.

Researchers and Consultants: Provides data and analysis for academic research, consulting projects, and market studies.

Financial Institutions: Helps assess risks and opportunities associated with financing or investing in the concerned market.

Essentially, anyone involved in or considering involvement in the Water Treatment Chemicals Market value chain can benefit from the information contained in a comprehensive market report.

Get Free Sample For Water Treatment Chemicals Market

Get Free Sample For Water Treatment Chemicals Market