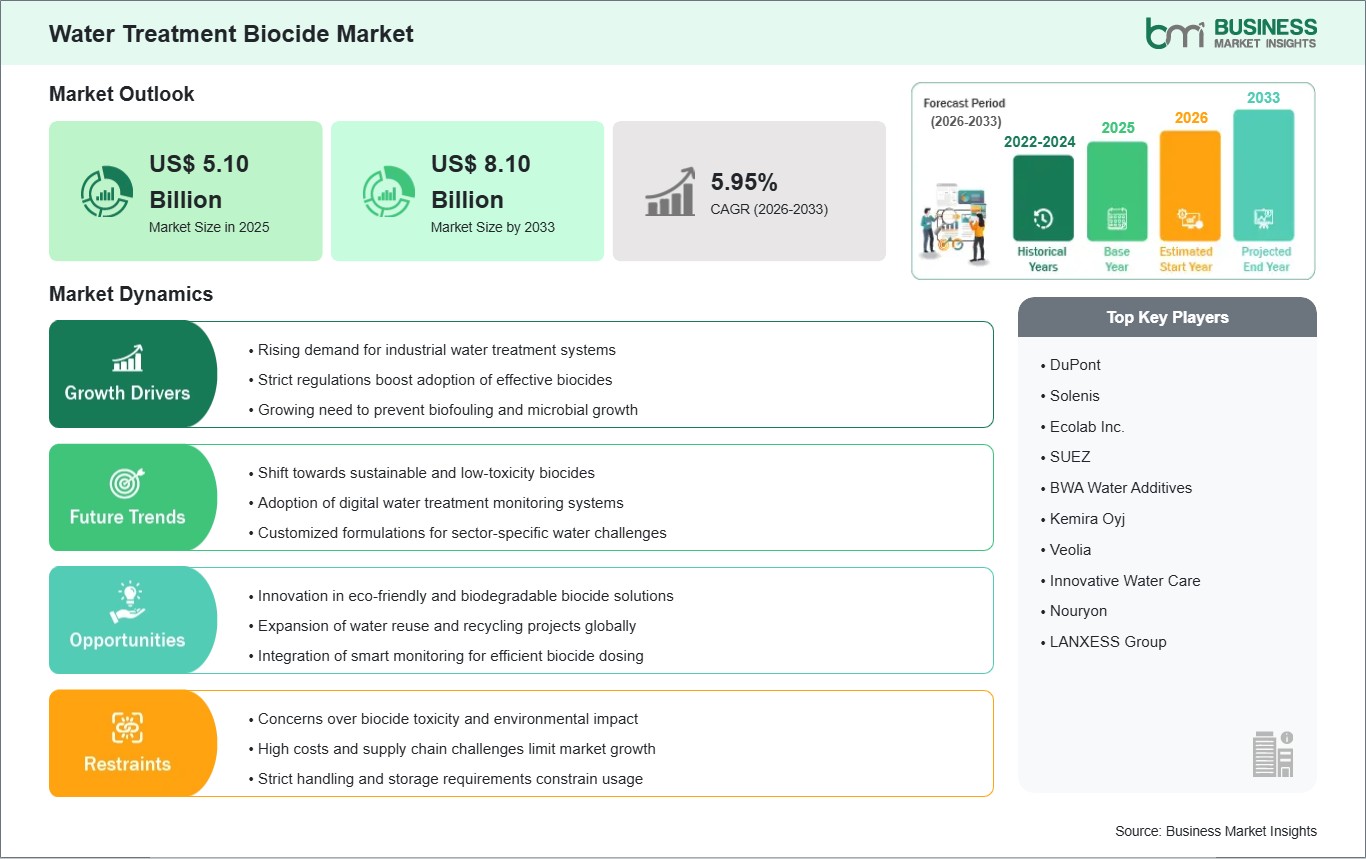

The Water Treatment Biocide Market size is expected to reach US$ 8.1 billion by 2033 from US$ 5.1 billion in 2025. The market is estimated to record a CAGR of 5.95% from 2026 to 2033.

Executive Summary and Global Market Analysis:

The global Water Treatment Biocide Market has expanded to become an essential element of industrial and municipal water treatment systems, which operate throughout the world, because of the essential need to manage microbial growth, biofouling and corrosion within all water-based systems. Industrial processes require advanced biocidal solutions for equipment maintenance, regulatory compliance and public health protection according to rising environmental regulations, which restrict water quality standards. Water treatment biocides function as chemical agents that stop bacteria, algae, fungi and other microorganisms from growing to protect water systems against operational problems and safety hazards. Developing economies and developed economies both drive market growth through their increasing commitment to sustainable water management, together with their need for improved water treatment methods. Businesses now need advanced treatment chemicals because of strict discharge regulations and environmental protection programs, which require them to achieve water reuse standards and effluent quality requirements.

The growing knowledge about how biofilm formation affects industrial heat exchangers, pipelines and membranes has resulted in increased demand for specific biocidal products which include both oxidizing and non-oxidizing solutions. Market expansion encounters specific limitations, even though the outlook appears positive. Traditional biocides contain toxic components that create safety hazards for workers and establish handling needs, while their residual chemicals pose environmental risks to natural water systems. Manufacturers face pressure to develop new, environmentally safe products that maintain effective performance standards. Supply chain difficulties, together with fluctuations in raw material prices, create obstacles for businesses that need to maintain product availability and control expenses.

The Water Treatment Biocide Market operates at a worldwide scale because its demand increases through regulatory and operational requirements, while the industry shifts toward sustainable practices that use safer chemicals to solve environmental problems.

Water Treatment Biocide Market - Strategic Insights:

Get more information on this report

Water Treatment Biocide Market Segmentation Analysis:

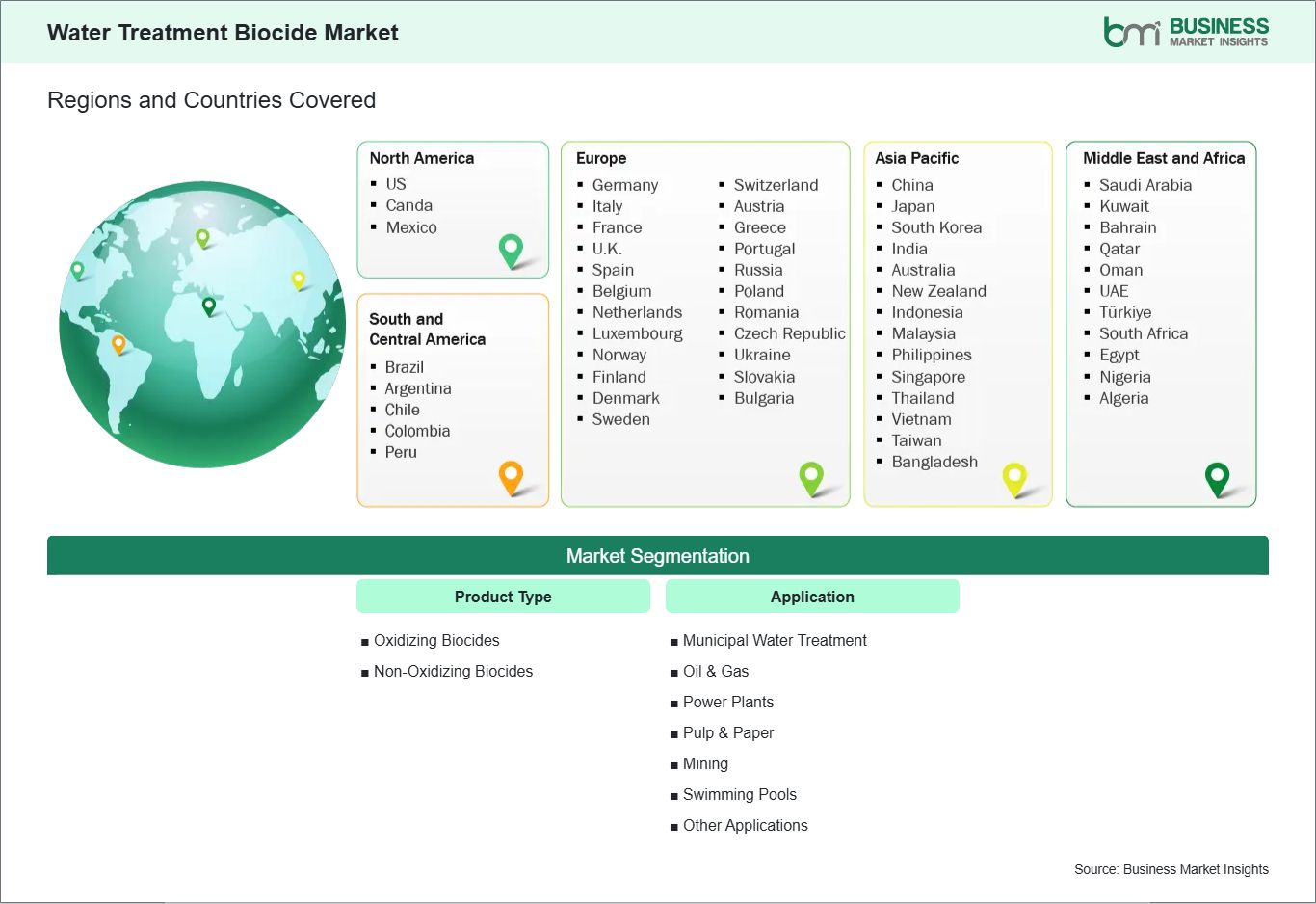

Key segments that contributed to the derivation of the water treatment biocide market analysis are product type and application.

By product type, the water treatment biocide market is segmented into oxidizing biocides, non‑oxidizing biocides. The non‑oxidizing biocides segment dominated the market in 2025.

Based on application, the water treatment biocide market is categorized into municipal water treatment, oil & gas, power plants, pulp & paper, mining, swimming pools, other applications. The oil & gas segment dominated the market in 2025.

Water Treatment Biocide Market Drivers and Opportunities:

Rising Demand for Industrial Water Treatment Systems

The global water treatment biocide market is experiencing robust momentum because industrial sectors that use water as their primary processing material need to control their water usage. The power generation, chemicals, oil and gas, paper and pulp and food and beverage industries use biocides to control three main problems, which include microbial contamination, biofilm growth and system corrosion. Water‑intensive operations need biocidal treatment because bacteria and algae cause three major problems, which include decreased heat transfer efficiency, piping network blockages and equipment system failures.

Industrial demand has increased because global manufacturing operations are expanding while advanced economies and developing economies establish stricter water quality standards. East Asian facilities are enhancing treatment systems to match their rapid industrial growth, while North American and Western European facilities implement biocide dosing methods that support their energy efficiency objectives. Cooling water systems in energy production use biocides to ensure operational continuity while preventing expensive shutdowns that result from microbial blockage.

Industrial water management practices are undergoing transformation worldwide because organizations increasingly focus on water reuse and recovery. Reuse initiatives require companies to establish effective treatment systems that use biocides to protect the quality of recycled water because many regions experience water scarcity issues. The comprehensive method uses water treatment biocides as essential elements that support industrial ecosystems to achieve operational stability, environmental regulations and sustainable development.

Innovation in Eco‑Friendly and Biodegradable Biocide Solutions

As environmental stewardship becomes a strategic imperative, the water treatment biocide market is shifting toward more eco‑friendly and biodegradable solutions. Traditional biocides, while effective at controlling microbes, have raised concerns about downstream ecological effects when residual chemicals enter natural water bodies. This has prompted manufacturers and chemical innovators to rethink formulation strategies, prioritizing chemistries that break down into benign byproducts without compromising antimicrobial efficacy, particularly in sensitive ecosystems.

Leading chemical developers in Europe and North America are pioneering next‑generation biocides infused with novel active components derived from renewable feedstocks or engineered for rapid environmental degradation. These innovations address the dual challenge of delivering reliable microbial control while minimizing long‑term persistence in aquatic environments, aligning with stricter effluent regulations and corporate sustainability commitments. In markets such as Scandinavia and Japan, where environmental performance standards are especially high, eco‑friendly biocides are increasingly integrated into municipal and industrial water treatment frameworks.

In parallel, research collaborations between academic institutions and industry stakeholders are expanding understanding of microbial ecology in treatment systems, enabling smarter targeting of biocide action with reduced overall chemical load. Such advancements not only support regulatory compliance but also help water managers mitigate public concerns about chemical footprints. As eco‑design principles continue to influence product roadmaps, innovations in biodegradable biocides are becoming essential levers for global water treatment strategies that balance performance, safety, and sustainability.

Water Treatment Biocide Market Size and Share Analysis:

The water treatment biocide market demonstrates steady growth, with size and share analysis highlighting evolving trends and competitive dynamics among key players. The report examines subsegments categorized within product type and application, offering insights into their contribution to overall market performance.

By product type, the non‑oxidizing biocides subsegment dominated the market in 2025, driven by their effectiveness in controlling microbial growth while minimizing corrosion and chemical reactivity.

Based on application, the oil & gas subsegment dominated the market in 2025, driven by the high demand for water treatment biocides in upstream and downstream operations to maintain equipment efficiency and safety.

Australia, China, India, Japan, South Korea, Indonesia, Malaysia, Philippines, Singapore, Thailand, Vietnam, Bangladesh, New Zealand, Taiwan

South and Central America

Brazil, Argentina, Peru, Chile, Colombia

Middle East and Africa

Bahrain, Kuwait, Oman, Qatar, Saudi Arabia, United Arab Emirates, Turkiye, South Africa, Egypt, Algeria, Nigeria

Market leaders and key company profiles

DuPont

Solenis

Ecolab Inc.

SUEZ

BWA Water Additives

Kemira Oyj

Veolia

Innovative Water Care

Nouryon

LANXESS Group

Get more information on this report

Water Treatment Biocide Market Report Coverage and Deliverables:

The "Water Treatment Biocide Market Size and Forecast (2022 - 2033)" report provides a detailed analysis of the market covering below areas:

Water Treatment Biocide Market size and forecast at global, regional, and country levels for all the key market segments covered under the scope

Water Treatment Biocide Market trends, as well as drivers, restraints, and opportunities

Water Treatment Biocide Market analysis covering key trends, global and regional framework, major players, regulations, and recent developments

Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments for the Water Treatment Biocide Market

Detailed company profiles, including SWOT analysis

Water Treatment Biocide Market Geographic Insights:

The geographical scope of the Water Treatment Biocide Market report is divided into North America, Asia Pacific, Europe, Middle East & Africa, and South & Central America. North America held the largest share in 2025.

North America leads the global Water Treatment Biocide Market because its industrial base has reached full development, combined with strict water quality regulations, power generation operations and oil and gas sector and municipal utility sector and the chemical industry sectors using advanced treatment technologies.

The U.S. and Canada implement regulatory frameworks that establish strict requirements for microbial control and effluent discharge standards, thus requiring facilities to use biocide solutions that combine high performance with minimal environmental impact. This requirement is met because facilities possess technical expertise and they maintain ongoing product development activities.

The Asia Pacific market grows because industrialization, urbanization and water infrastructure investments drive demand, with China, India, Japan and Southeast Asian nations investing to modernize their outdated water treatment facilities while using anti-biofouling methods in their manufacturing and cooling systems to satisfy increasing public health and environmental standards.

The European market maintains equilibrium because environmental regulations, chemical usage restrictions and sustainability practices dictate market operations. European stakeholders increasingly prioritize reduced‑toxicity and biodegradable biocides to meet both regulatory requirements and social expectations for environmental stewardship, with well‑established water reuse and recycling initiatives further amplifying the need for effective microbial control.

The Middle East and Africa face water scarcity challenges which necessitate desalination technology expansion, while desalination operations use biocides to stop microbial growth in their plants and industrial cooling systems and municipal distribution networks. The market environment exhibits distinct characteristics because of economic differences between countries and the existence of multiple regulatory frameworks in South and Central America, which shows increasing understanding of water infrastructure modernization and industrial water management through its wastewater treatment improvements and process efficiency enhancements.

Get more information on this report

Water Treatment Biocide Market Research Report Guidance:

The report includes qualitative and quantitative data in the Water Treatment Biocide Market across product type, application, and geography.

The report starts with the key takeaways (chapter 2), highlighting key trends and outlook of the Water Treatment Biocide Market.

Chapter 3 focuses on the research methodology of the study.

Chapter 4 includes ecosystem analysis.

Chapter 5 highlights the major industry dynamics in the Water Treatment Biocide Market, including factors that are driving the market, prevailing deterrents, potential opportunities, as well as future trends. Impact analysis of these drivers and restraints is also covered in this section.

Chapter 6 discusses the Water Treatment Biocide Market scenario, in terms of historical market revenues, and forecast till the year 2033.

Chapters 7 to 9 cover Water Treatment Biocide Market segments by product type, application, and geography across North America, Asia Pacific, Europe, Middle East & Africa, and South & Central America. They cover the market revenue forecast and factors driving the market.

Chapter 10 describes the competitive analysis along with the heat map analysis for the key players operating in the market.

Chapter 11 describes the industry landscape analysis. It provides detailed descriptions of business activities such as market initiatives, new developments, mergers, and joint ventures globally, along with a competitive landscape.

Chapter 12 provides detailed profiles of the major companies operating in the Water Treatment Biocide Market. Companies have been profiled on the basis of their key facts, business descriptions, products, financial overview, SWOT analysis, and key developments.

Chapter 13, i.e., the appendix, is inclusive of a brief overview of the company, a list of abbreviations, and a disclaimer.

Water Treatment Biocide Market News and Key Development:

The Water Treatment Biocide Market is evaluated by gathering qualitative and quantitative data post primary and secondary research, which includes important corporate publications, association data, and databases. A few of the key developments in the water treatment biocide market are:

In January 2023, Nouryon introduced Triameen® Y12D antimicrobial active for the U.S. cleaning market. Although positioned across household, institutional, and industrial applications, this antimicrobial active reflects Nouryon’s broader strategy to expand its portfolio of effective, lower‑toxicity biocides suitable for various water and surface disinfection needs globally.

In July 2025, Kemira announced a strategic investment to expand its water treatment chemical production with a new Aluminium Chloro Hydrate (ACH) production line at its Tarragona site in Spain. The expanded facility will strengthen Kemira’s portfolio of high‑performance water treatment chemicals, particularly for drinking water applications, enhancing its ability to meet global demand for advanced water treatment solutions.

Key Sources Referred:

World Health Organization (WHO)Organisation for Economic Cooperation and Development (OECD)The World Bank GroupWorldometerThe LancetInternational Bar AssociationInternational Trade Administration

The List of Companies - Water Treatment Biocide Market

DuPont

Solenis

Ecolab Inc.

SUEZ

BWA Water Additives

Kemira Oyj

Veolia

Innovative Water Care

Nouryon

LANXESS Group

Frequently Asked Questions

How big is the Water Treatment Biocide Market?

The Water Treatment Biocide Market is valued at US$ 5.10 Billion in 2025, it is projected to reach US$ 8.10 Billion by 2033.

What is the CAGR for Water Treatment Biocide Market by (2026 - 2033)?

As per our report Water Treatment Biocide Market, the market size is valued at US$ 5.10 Billion in 2025, projecting it to reach US$ 8.10 Billion by 2033. This translates to a CAGR of approximately 5.95% during the forecast period.

What segments are covered in this report?

The Water Treatment Biocide Market report typically cover these key segments-

Product Type (Oxidizing Biocides, Non-Oxidizing Biocides)

Application (Municipal Water Treatment, Oil & Gas, Power Plants, Pulp & Paper, Mining, Swimming Pools, Other Applications)

What is the historic period, base year, and forecast period taken for Water Treatment Biocide Market?

The historic period, base year, and forecast period can vary slightly depending on the specific market research report. However, for the Water Treatment Biocide Market report:

Historic Period : 2022-2024

Base Year : 2025

Forecast Period : 2026-2033

Who are the major players in Water Treatment Biocide Market?

The Water Treatment Biocide Market is populated by several key players, each contributing to its growth and innovation. Some of the major players include:

DuPont

Solenis

Ecolab Inc.

SUEZ

BWA Water Additives

Kemira Oyj

Veolia

Innovative Water Care

Nouryon

LANXESS Group

Who should buy this report?

The Water Treatment Biocide Market report is valuable for diverse stakeholders, including:

Investors: Provides insights for investment decisions pertaining to market growth, companies, or industry insights. Helps assess market attractiveness and potential returns.

Industry Players: Offers competitive intelligence, market sizing, and trend analysis to inform strategic planning, product development, and sales strategies.

Suppliers and Manufacturers: Helps understand market demand for components, materials, and services related to concerned industry.

Researchers and Consultants: Provides data and analysis for academic research, consulting projects, and market studies.

Financial Institutions: Helps assess risks and opportunities associated with financing or investing in the concerned market.

Essentially, anyone involved in or considering involvement in the Water Treatment Biocide Market value chain can benefit from the information contained in a comprehensive market report.

Get Free Sample For Water Treatment Biocide Market

Get Free Sample For Water Treatment Biocide Market