01

Market Summery

Executive Summary and Global Market Analysis

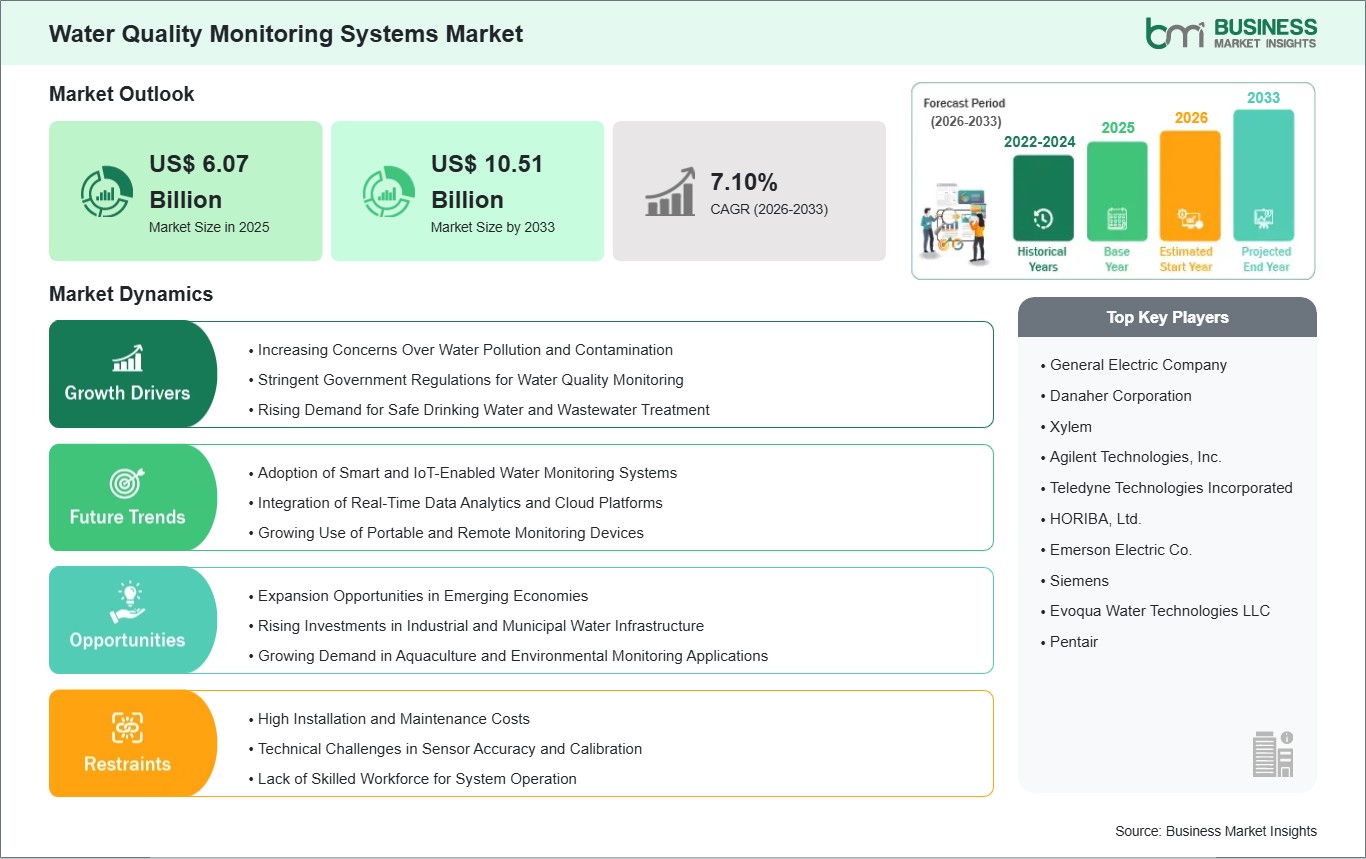

Water Quality Monitoring Systems represent a sophisticated convergence of electrochemical sensing, analytical chemistry, and digital telecommunications designed to provide real-time oversight of aqueous environments. These systems are fundamental to the global effort of safeguarding public health and industrial integrity, utilizing a diverse array of components—from pH and dissolved oxygen sensors to complex Total Organic Carbon (TOC) analyzers—to digitize the chemical and biological profile of water. By providing continuous, high-fidelity data, these platforms enable municipal utilities, industrial manufacturers, and environmental agencies to transition from reactive sampling to proactive, automated management.

The market faces notable growth restraints, primarily centered on the high total cost of ownership. The significant capital expenditure required for the installation of multi-parameter sensor arrays, coupled with the rigorous, ongoing costs of calibration, reagent replacement, and maintenance in harsh or fouling-prone environments, can be prohibitive for smaller municipalities. Furthermore, technical hurdles regarding data interoperability between legacy hardware and modern cloud-based IoT architectures often complicate large-scale deployments.

Despite these challenges, the market is entering a lucrative era defined by the integration of Artificial Intelligence (AI) and edge computing. These technologies allow for predictive anomaly detection and automated dosing control, significantly reducing operational waste. As global regulatory frameworks tighten and the "Smart City" movement gains momentum, the demand for integrated, low-power, and autonomous monitoring solutions presents a massive opportunity for manufacturers to offer value-added data services, ensuring the market remains resilient and highly profitable through 2033.

03

Segment Analysis

Water Quality Monitoring Systems Market Segmentation

Key segments that contributed to the derivation of the Water Quality Monitoring Systems market analysis are the Component and end-user.

- By Component, the market is segmented into Dissolved Oxygen Sensors, PH Sensors, Turbidity Sensors, Temperature Sensors, TOC Analyzer, and Others.

- By End-user, the market is divided into Industrial, Utility, Commercial, and Residential.

04

Market Forces

Water Quality Monitoring Systems Market Drivers and Opportunities

Stringent Environmental Regulations and Global Compliance Mandates

The primary catalyst propelling the water quality monitoring systems market is the aggressive expansion of environmental governance and public health mandates on a global scale. Regulatory agencies have moved beyond periodic manual checks to requiring continuous, high-fidelity data reporting to mitigate the risks associated with emerging contaminants such as perfluoroalkyl substances and heavy metal concentrations.

These mandates are particularly influential in the industrial sector, where "Zero Liquid Discharge" policies compel facilities to monitor every stage of their water cycle to ensure that treated effluent meets rigorous safety standards before being recycled or released into natural ecosystems. In developing regions, nationwide initiatives aimed at restoring major river basins and securing groundwater purity serve as a major driver for the mass adoption of sensing networks. This regulatory environment creates a non-discretionary demand for monitoring hardware, as non-compliance now carries significant legal and financial consequences for utility providers and private corporations alike. By shifting the burden of proof toward digital, auditable records, these laws ensure that the investment in sophisticated monitoring infrastructure remains a top priority for stakeholders committed to long-term environmental stewardship and public safety.

Integration of Artificial Intelligence and Edge Computing for Smart Management

A profound growth opportunity resides in the transformation of water monitoring from a passive sensing activity into an active, intelligent management ecosystem through Artificial Intelligence and edge computing. Traditional systems often rely on back-end analysis that introduces a lag between contamination detection and corrective action; however, edge-enabled devices now process vast amounts of sensor data locally, allowing for instantaneous decision-making at the point of contact. This capability enables the development of "self-optimizing" water networks where AI algorithms can predict fluctuating chemical demands or identify subtle mechanical failures before they escalate into system-wide outages.

For municipal utilities, this represents a shift toward predictive maintenance, reducing the overall waste of treatment chemicals and energy. Furthermore, as cities embrace the smart infrastructure model, the ability to integrate thousands of autonomous sensors into a unified digital twin provides a granular view of water health across entire urban landscapes. This technological evolution allows manufacturers to transition their business models from selling individual components to providing "Actionable Intelligence" and diagnostic services, capturing a larger portion of the value chain by offering software-driven insights that optimize operational resilience and resource efficiency.

05

Size and Share Analysis

Water Quality Monitoring Systems Market Size and Share Analysis

The Water Quality Monitoring Systems market demonstrates steady growth, with size and share analysis revealing evolving trends and competitive positioning among key players. The report further examines subsegments categorized within Component and end-user, offering insights into their contribution to overall market performance.

Within the component industry, the pH Sensors sub-segment remains a foundational element of the market, widely adopted across all sectors for its essential role in measuring basic water stability and chemical balance in both drinking water and industrial discharge.

Within the end-user sector, currently Utility sub-segment is commanding a significant share due to the massive scale of municipal water treatment projects and the urgent need for real-time public health surveillance.

07

Report Coverage

Water Quality Monitoring Systems Market Report Coverage and Deliverables

The "Water Quality Monitoring Systems Market Size and Forecast (2022–2033)" report provides a detailed analysis of the market covering below areas:

- Water Quality Monitoring Systems market size and forecast at global, regional, and country levels for all the key market segments covered under the scope

- Water Quality Monitoring Systems market trends, as well as market dynamics such as drivers, restraints, and key opportunities

- Water Quality Monitoring Systems market analysis covering key market trends, global and regional framework, major players, regulations, and recent market developments

- Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments for the Water Quality Monitoring Systems market

- Detailed company profiles, including SWOT analysis

08

Geographic Insights

Water Quality Monitoring Systems Market Geographic Insights

The geographical scope of the Water Quality Monitoring Systems market report is divided into five regions: North America, Asia Pacific, Europe, the Middle East & Africa, and South & Central America.

In North America, the market is sustained by a robust framework of environmental mandates and a concerted focus on upgrading aging municipal infrastructure with high-precision digital sensing technologies.

Europe maintains a sophisticated market environment where the integration of automated monitoring systems is driven by a deep-seated commitment to sustainability and the rigorous enforcement of cross-border water protection directives.

The Asia-Pacific region functions as a high-growth engine, propelled by the urgent need to mitigate the environmental impacts of rapid industrialization and the large-scale deployment of smart water management solutions within emerging urban centers.

In the Middle East & Africa, market activity is increasingly centered on the implementation of advanced desalination monitoring and the development of resilient water grids to combat extreme water scarcity in arid climates.

Meanwhile, South & Central America are witnessing a progressive transition toward modernized monitoring practices as regional industries and government bodies prioritize the protection of vital freshwater resources against agricultural and mining runoff. This collective regional progress ensures a stable global demand for integrated monitoring solutions as nations harmonize their industrial growth with environmental preservation goals.

10

Industry Activity

Recent Developments

The Water Quality Monitoring Systems market is evaluated by gathering qualitative and quantitative data post primary and secondary research, which includes important corporate publications, association data, and databases. A few of the key developments in the Water Quality Monitoring Systems market are:

- In January 2026, Texas Instruments introduced a suite of high-precision analog-to-digital converters specifically tailored for multi-parameter sensors used within Water Quality Monitoring Systems, a development that enabled thirty percent faster signal processing in remote monitoring kiosks.

- In March 2026, Xylem Inc. announced the launch of its next-generation YSI EXO multiparameter water quality sonde, designed for real-time monitoring in environmental, industrial, and municipal applications. The system features enhanced sensor accuracy, improved anti-fouling technology, and cloud-connected data analytics for continuous remote monitoring of key parameters such as pH, dissolved oxygen, and turbidity. This development supports more efficient water resource management and strengthens Xylem’s portfolio of smart water monitoring solutions.

11

Trust & Transparency

Research Methodology

The market analysis combines proprietary research with secondary data from government agencies, company disclosures, regulatory filings, industry databases and expert interviews. Market estimates are validated through data triangulation, cross-market benchmarking and analyst

review.

View Full Research Methodology

Key Sources Referred:

World Bank – Global Trade Indicators World Trade Organization (WTO) (International Monetary Fund )IMF International Trade Administration (ITA) Company website Company annual reports Company investor presentations