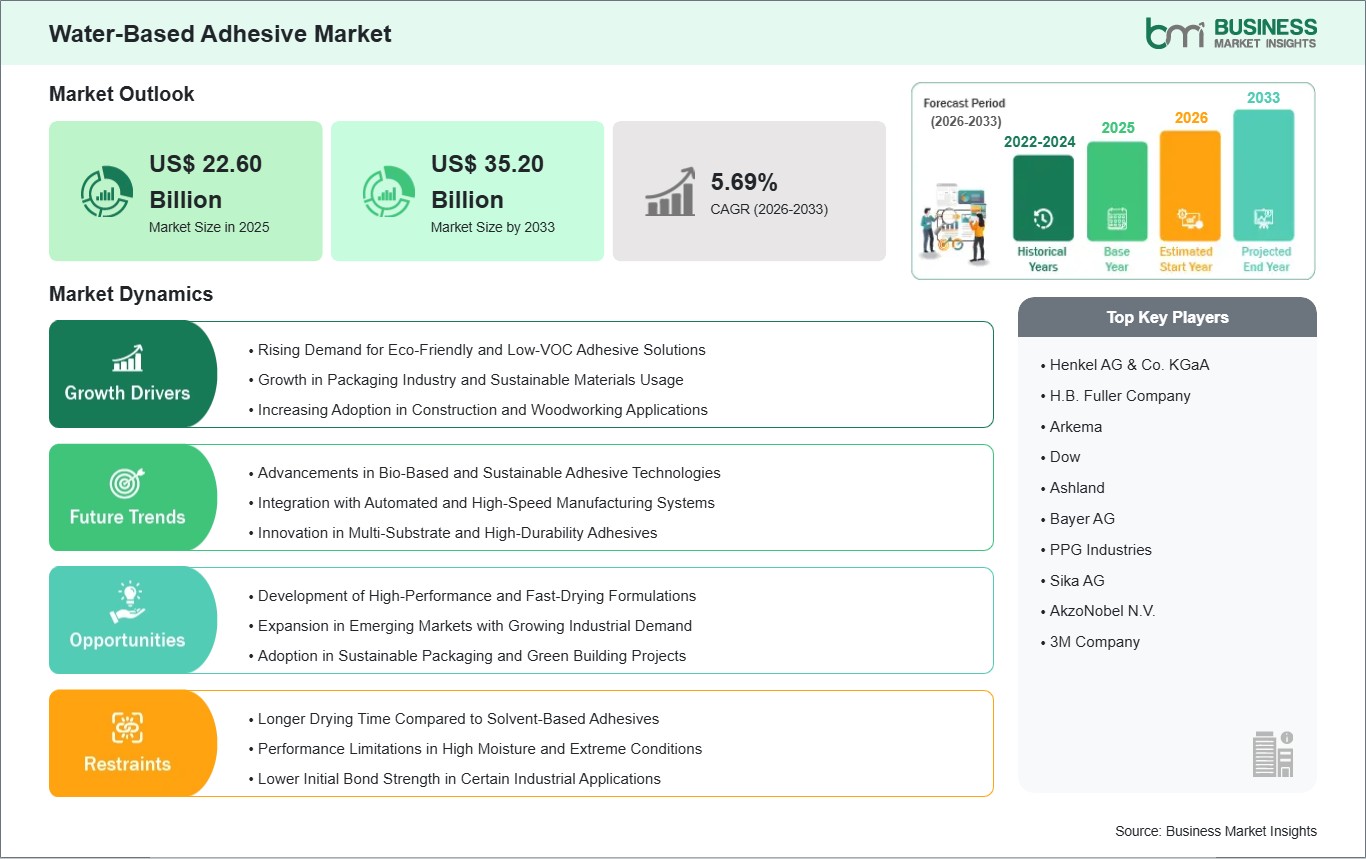

The Water-Based Adhesive Market size is expected to reach US$ 35.2 billion by 2033 from US$ 22.6 billion in 2025. The market is estimated to record a CAGR of 5.69% from 2026 to 2033.

Executive Summary and Global Market Analysis:

The global water-based adhesive market is witnessing strong growth because multiple industries require bonding solutions that meet environmental standards and produce minimal emissions. Water-based adhesives, which use water as their main solvent, are becoming more popular than solvent-based adhesives because they generate lower volatile organic compounds and present reduced toxicity while meeting strict environmental standards. The packaging industry employs these adhesives to create secure bonds that meet sustainability requirements throughout various industries, including woodworking, paper production, construction, automotive and textile markets.

The worldwide transition toward sustainable manufacturing methods and environmentally friendly building practices is driving the growth of water-based adhesive technology. The packaging industry experiences rapid growth, which acts as the main market driver for the sector because e-commerce, food and beverage and consumer goods markets are expanding. Water-based adhesives serve multiple purposes in carton sealing and labeling and flexible packaging because they offer safe handling features and simple application methods, and they work well with paper-based materials. The growing demand for sustainable packaging materials strengthens the use of these adhesives because they meet recyclability and environmental compliance standards. The construction sector also contributes to market growth because water-based adhesives enable eco-friendly building certifications through their use in flooring, insulation and panel bonding applications.

The market experiences particular limitations that restrict its growth. Water-based adhesives generally exhibit longer drying times compared to solvent-based systems, which restrict their application in fast-paced manufacturing environments that lack special drying equipment. Moreover, the product performance decreases in extreme weather conditions, which include high humidity and low temperature, because this limits industrial applications. The ongoing progress in polymer chemistry and formulation technologies enables better adhesive performance through improved drying speed, higher bond strength and increased moisture resistance. Water-based adhesives will become the main solution for adhesive development throughout the world because industries now focus on environmentally friendly practices and need to meet government regulations.

Key segments that contributed to the derivation of the water-based adhesive market analysis are resin type and application.

By resin type, the water-based adhesives market is segmented into acrylic polymer emulsion (PAE), polyvinyl acetate emulsion, vinyl acetate ethylene emulsion, styrene butadiene latex, polyurethane dispersion, other resin types. The acrylic polymer emulsion segment dominated the market in 2025.

Based on application, the water-based adhesives market is categorized into tapes & labels, paper & packaging, building & construction, woodworking, automotive & transportation, other applications. The paper & packaging segment dominated the market in 2025.

Water-Based Adhesive Market Drivers and Opportunities:

Rising Demand for Eco‑Friendly and Low‑VOC Adhesive Solutions

The need for environmentally friendly adhesive products that produce low volatile organic compounds has increased because of growing environmental awareness and stricter emissions regulations. Water-based adhesives use water as the primary carrier instead of organic solvents, which leads to a decrease in volatile organic compound emissions. This advantage meets the requirements of international regulatory systems, which North America and Europe use to control indoor pollution and limit worker contact with dangerous substances. Manufacturers in sectors such as packaging, textiles, and construction increasingly view water‑based systems as not only compliant but also beneficial for corporate sustainability programs.

The packaging industry has adopted water-based adhesives at an increasing rate because recyclable materials and fiber-based materials have become standard practice in the industry. Adhesive systems that support recyclability without compromising performance have become essential for brands that want to meet consumer expectations for sustainable packaging. Fast-growing e-commerce and retail markets in Asia Pacific create a need for water-based solutions that can bond paperboard and corrugated board and labels while reducing environmental damage throughout the entire product lifecycle.

The global green building movement has created a positive effect on the adoption of environmentally friendly practices. Water-based adhesives are widely used in flooring, wall coverings, and panel lamination applications where low emissions contribute to healthier indoor environments. Water-based adhesive solutions serve as essential technologies that help various industries achieve both their performance and sustainability objectives because environmental responsibility becomes a key factor in procurement processes worldwide.

Development of High‑Performance and Fast‑Drying Formulations

Advancements in polymer science and formulation technology are enabling water‑based adhesives to achieve higher performance and faster drying rates, addressing historical limitations compared to solvent‑based systems. Innovative chemistries such as advanced acrylic emulsions, hybrid polymers, and modified polyurethane dispersions are enhancing bond strength, flexibility, and resistance to moisture and temperature variations. These improvements make water‑based solutions suitable for demanding applications in automotive assembly, electronics manufacturing, and high‑speed packaging lines.

Automotive manufacturers in North America and Europe are increasingly incorporating fast‑curing water‑based adhesives into interior assembly, headliner bonding, and lightweight composite joining processes. These formulations help improve production efficiency while adhering to strict environmental standards. In electronics, water‑based systems with optimized drying profiles are enabling faster throughput in display assembly and electronic component bonding without risking heat damage to sensitive parts.

Additionally, novel additive technologies are reducing dependency on extended thermal drying, allowing many formulations to cure effectively at ambient temperatures. This not only saves energy but also expands the applicability of water‑based adhesives in regions with limited access to advanced drying infrastructure. As research continues to refine performance characteristics, water‑based adhesives are expected to penetrate new industrial segments and replace traditional solvent‑based options, reinforcing their role as versatile, sustainable bonding solutions globally.

Water-Based Adhesive Market Size and Share Analysis:

The water-based adhesive market demonstrates steady growth, with size and share analysis highlighting evolving trends and competitive dynamics among key players. The report examines subsegments categorized within resin type and application, offering insights into their contribution to overall market performance.

By resin type, the acrylic polymer emulsion subsegment dominated the market in 2025, driven by its excellent adhesion performance, versatility, and wide usage across multiple applications.

Based on application, the paper & packaging subsegment dominated the market in 2025, driven by the high demand for eco-friendly adhesives in packaging and labeling applications.

Australia, China, India, Japan, South Korea, Indonesia, Malaysia, Philippines, Singapore, Thailand, Vietnam, Bangladesh, New Zealand, Taiwan

South and Central America

Brazil, Argentina, Peru, Chile, Colombia

Middle East and Africa

Bahrain, Kuwait, Oman, Qatar, Saudi Arabia, United Arab Emirates, Turkiye, South Africa, Egypt, Algeria, Nigeria

Market leaders and key company profiles

HenkelAGCoKgaA

HBFullerCompany

Arkema

Dow

Ashland

BayerAG

PPGIndustries

SikaAG

AkzoNobelNV

ThreeMCompany

Get more information on this report

Water-Based Adhesive Market Report Coverage and Deliverables:

The "Water-Based Adhesive Market Size and Forecast (2022 - 2033)" report provides a detailed analysis of the market covering below areas:

Water-Based Adhesive Market size and forecast at global, regional, and country levels for all the key market segments covered under the scope

Water-Based Adhesive Market trends, as well as drivers, restraints, and opportunities

Water-Based Adhesive Market analysis covering key trends, global and regional framework, major players, regulations, and recent developments

Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments for the Water-Based Adhesive Market

Detailed company profiles, including SWOT analysis

Water-Based Adhesive Market Geographic Insights:

The geographical scope of the Water-Based Adhesive Market report is divided into North America, Asia Pacific, Europe, Middle East & Africa, and South & Central America. North America held the largest share in 2025.

North America controls the worldwide water-based adhesive industry because it has strong regulatory systems, a developed industrial sector and its first usage of sustainable technologies in various industries establishes environmental standards.

The United States and Canada lead demand, particularly in packaging, construction, woodworking, and automotive applications, where strict regulations on volatile organic compound emissions have accelerated the transition toward water-based formulations. The region's strong e-commerce industry, together with its increasing demand for eco-friendly packaging materials, establishes a basis for using these adhesives in carton sealing and labeling and paper-based packaging applications.

The European market functions as a developed market that focuses on sustainability because Germany, France and the UK promote environmentally sustainable production methods and circular economy business models. The regulatory frameworks that create incentives for using products that produce low emissions and materials that can be recycled now drive manufacturers to use water-based adhesives for their packaging, construction and automotive interior needs.

The Asia Pacific region serves as a fast-developing market, which China, India, Japan and South Korea lead because industrial growth, city development and increasing consumer needs create a demand for adhesives used in packaging and textiles and construction. The rising public understanding of environmental standards, together with the adoption of sustainable production methods, is driving increased adoption in the area.

The Middle East and Africa market is developing at a slow pace because infrastructure development, construction projects and packaging industry expansion are growing in countries like the UAE, Saudi Arabia and South Africa. South and Central America experience continuous growth, which Brazil and Mexico primarily drive through their enhanced manufacturing capabilities, their rising need for packaging materials and their growing foreign investment in industrial development. Sustainable practices, together with regulatory requirements and new adhesive formulation technologies are determining market trends in all regions, while North America maintains its market leadership through its product innovations, compliance practices and strong customer demand from various industries.

Get more information on this report

Water-Based Adhesive Market Research Report Guidance:

The report includes qualitative and quantitative data in the Water-Based Adhesive Market across resin type, application, and geography.

The report starts with the key takeaways (chapter 2), highlighting key trends and outlook of the Water-Based Adhesive Market.

Chapter 3 focuses on the research methodology of the study.

Chapter 4 includes ecosystem analysis.

Chapter 5 highlights the major industry dynamics in the Water-Based Adhesive Market, including factors that are driving the market, prevailing deterrents, potential opportunities, as well as future trends. Impact analysis of these drivers and restraints is also covered in this section.

Chapter 6 discusses the Water-Based Adhesive Market scenario, in terms of historical market revenues, and forecast till the year 2033.

Chapters 7 to 9 cover Water-Based Adhesive Market segments by resin type, application, and geography across North America, Asia Pacific, Europe, Middle East & Africa, and South & Central America. They cover the market revenue forecast and factors driving the market.

Chapter 10 describes the competitive analysis along with the heat map analysis for the key players operating in the market.

Chapter 11 describes the industry landscape analysis. It provides detailed descriptions of business activities such as market initiatives, new developments, mergers, and joint ventures globally, along with a competitive landscape.

Chapter 12 provides detailed profiles of the major companies operating in the Water-Based Adhesive Market. Companies have been profiled on the basis of their key facts, business descriptions, products, financial overview, SWOT analysis, and key developments.

Chapter 13, i.e., the appendix, is inclusive of a brief overview of the company, a list of abbreviations, and a disclaimer.

Water-Based Adhesive Market News and Key Development:

The Water-Based Adhesive Market is evaluated by gathering qualitative and quantitative data post primary and secondary research, which includes important corporate publications, association data, and databases. A few of the key developments in the water-based adhesive market are:

In February 2023, H.B. Fuller announced advancements in its sustainable adhesive portfolio at INDEX™23, including the expansion of bio-based and low-emission adhesive technologies aimed at improving environmental performance and supporting circular economy initiatives.

In January 2026, Henkel AG & Co. KGaA announced that it had signed an agreement to acquire ATP Adhesive Systems, a leader in high‑performance water‑based specialty tape technologies, expanding its adhesive portfolio and strengthening its sustainable, low‑VOC offerings across automotive, electronics, medical, and construction sectors.

Key Sources Referred:

World Health Organization (WHO)Organisation for Economic Cooperation and Development (OECD)The World Bank GroupWorldometerThe LancetInternational Bar AssociationInternational Trade Administration

The List of Companies - Water-Based Adhesive Market

HenkelAGCoKgaA

HBFullerCompany

Arkema

Dow

Ashland

BayerAG

PPGIndustries

SikaAG

AkzoNobelNV

ThreeMCompany

Frequently Asked Questions

How big is the Water-Based Adhesive Market?

The Water-Based Adhesive Market is valued at US$ 22.60 Billion in 2025, it is projected to reach US$ 35.20 Billion by 2033.

What is the CAGR for Water-Based Adhesive Market by (2026 - 2033)?

As per our report Water-Based Adhesive Market, the market size is valued at US$ 22.60 Billion in 2025, projecting it to reach US$ 35.20 Billion by 2033. This translates to a CAGR of approximately 5.69% during the forecast period.

What segments are covered in this report?

The Water-Based Adhesive Market report typically cover these key segments-

Application (Tapes & Labels, Paper & Packaging, Building & Construction, Woodworking, Automotive & Transportation, Other Applications)

What is the historic period, base year, and forecast period taken for Water-Based Adhesive Market?

The historic period, base year, and forecast period can vary slightly depending on the specific market research report. However, for the Water-Based Adhesive Market report:

Historic Period : 2022-2024

Base Year : 2025

Forecast Period : 2026-2033

Who are the major players in Water-Based Adhesive Market?

The Water-Based Adhesive Market is populated by several key players, each contributing to its growth and innovation. Some of the major players include:

HenkelAGCoKgaA

HBFullerCompany

Arkema

Dow

Ashland

BayerAG

PPGIndustries

SikaAG

AkzoNobelNV

ThreeMCompany

Who should buy this report?

The Water-Based Adhesive Market report is valuable for diverse stakeholders, including:

Investors: Provides insights for investment decisions pertaining to market growth, companies, or industry insights. Helps assess market attractiveness and potential returns.

Industry Players: Offers competitive intelligence, market sizing, and trend analysis to inform strategic planning, product development, and sales strategies.

Suppliers and Manufacturers: Helps understand market demand for components, materials, and services related to concerned industry.

Researchers and Consultants: Provides data and analysis for academic research, consulting projects, and market studies.

Financial Institutions: Helps assess risks and opportunities associated with financing or investing in the concerned market.

Essentially, anyone involved in or considering involvement in the Water-Based Adhesive Market value chain can benefit from the information contained in a comprehensive market report.

Get Free Sample For Water-Based Adhesive Market

Get Free Sample For Water-Based Adhesive Market