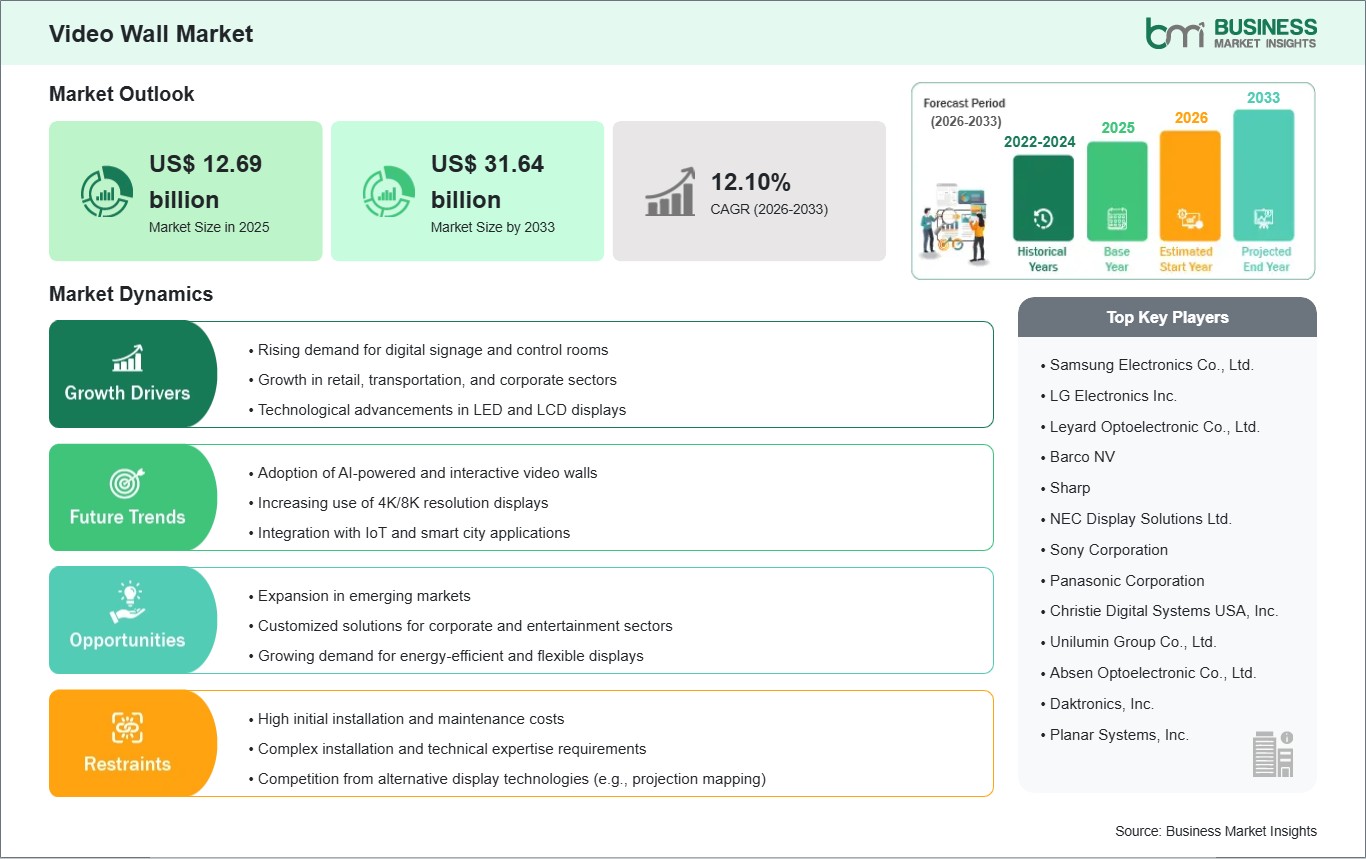

The Video Wall Market size is expected to reach US$ 31.64 billion by 2033 from US$ 12.69 billion in 2025. The market is estimated to record a CAGR of 12.10% from 2026 to 2033.

Executive Summary and Global Market Analysis:

Video walls are sophisticated visualization systems comprised of multiple displays—such as LED panels, LCD tiles, or rear-projection cubes—configured to operate as a single, contiguous canvas. By leveraging advanced tiling controllers and high-performance software, these systems provide massive scale, ultra-high resolutions, and superior brightness levels that far exceed the capabilities of standalone monitors. They serve as the critical visual backbone for mission-critical environments, including emergency command centers, corporate boardrooms, and large-scale public arenas.

However, the market faces significant structural restraints, most notably the high total cost of ownership encompassing premium hardware, specialized installation labor, and the infrastructure required for thermal management. Technical challenges regarding "bezel-gap" synchronization and the maintenance of color uniformity across hundreds of individual modules over time also act as deterrents for budget-sensitive sectors. Furthermore, the significant power consumption of large-format outdoor arrays remains a concern amid tightening environmental regulations.

Despite these hurdles, the industry is entering a high-growth phase driven by the commercialization of Micro-LED technology, which offers unprecedented contrast and longevity. Lucrative opportunities are emerging from the integration of AI-powered content automation and the rise of "Virtual Production" in film and broadcast. As smart city initiatives accelerate global demand for centralized data monitoring, the video wall market is positioned as a vital tool for real-time analytics and immersive brand storytelling, ensuring a resilient trajectory through 2033.

Video Wall Market - Strategic Insights:

Get more information on this report

Video Wall Market Segmentation Analysis:

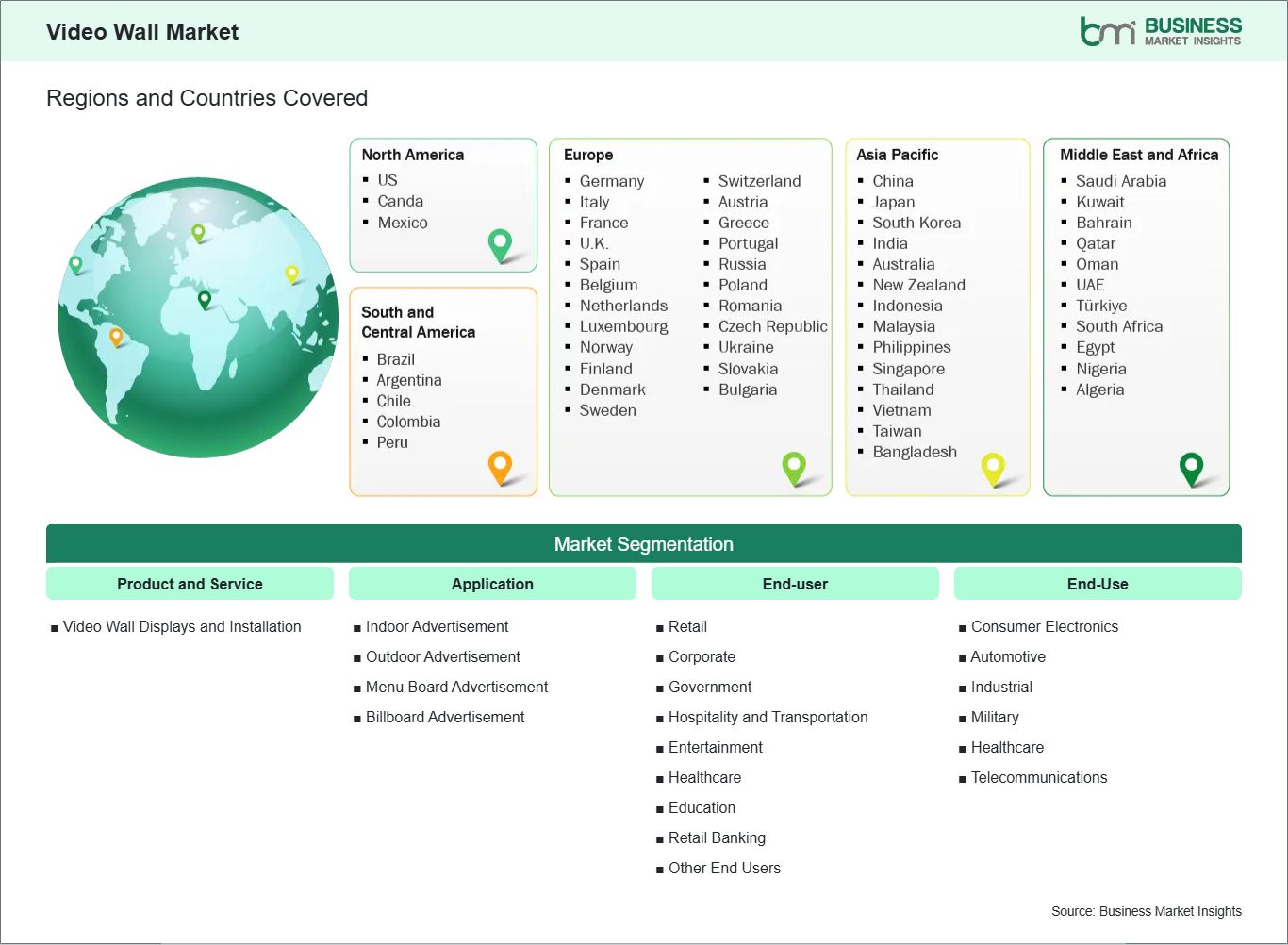

Key segments that contributed to the derivation of the Video Wall market analysis are product and service, application, and end-user.

By Product and Service, the market is segmented into Video Wall Displays and Installation.

By Application, the market is divided into Indoor Advertisement, Outdoor Advertisement, Menu Board Advertisement, and Billboard Advertisement.

By End-user, the market is categorized into Retail, Corporate, Government, Hospitality and Transportation, Entertainment, Healthcare, Education, Retail Banking, and Others.

Video Wall Market Drivers and Opportunities:

Proliferation of Digital Signage and Advertising Modernization

The global shift toward digital transformation in the advertising and media sectors acts as a foundational driver for the video wall market. As brands increasingly compete for audience attention in densely populated environments, traditional static signage is being phased out in favor of dynamic, high-impact digital canvases. These systems enable the real-time delivery of tailored messages, high-definition motion graphics, and interactive content that significantly enhance brand recall and customer engagement. The transition is especially evident in the retail and transportation sectors, where massive display arrays are used to create immersive experiences that standard signage cannot provide.

The widespread rollout of advanced wireless connectivity further catalyzes this growth, allowing for the seamless delivery of ultra-high-definition and crystal-clear content across geographically dispersed networks. Furthermore, the ability of these systems to function under various lighting conditions—specifically high-brightness outdoor configurations—ensures their utility in transit hubs and sports stadiums. Consequently, enterprises are allocating a greater portion of their marketing resources toward advanced digital hardware, viewing it as a critical asset for driving foot traffic and modernizing the consumer journey. This shift toward a "sensing-to-inference" advertising model allows displays to adjust content based on environmental cues, making visual communication more relevant and effective than ever before.

Emerging Demand for Immersive Entertainment and Smart City Control Hubs

A significant opportunity for the video wall market lies in the rising demand for sophisticated visualization within smart city frameworks and the creative entertainment industry. As urban centers become more interconnected, there is a vital need for advanced command and control centers that utilize seamless display technology to monitor a constant stream of data from traffic sensors, public safety cameras, and utility grids. These mission-critical environments require the absolute reliability and constant operational capacity that modern video wall architectures provide. Simultaneously, the entertainment sector—including high-end cinema and virtual production—is pivoting toward self-emissive display technologies to create wrap-around, lifelike environments.

Virtual production studios are increasingly utilizing large-scale display volumes to replace traditional backgrounds, offering a more efficient and flexible workflow for content creators. As the industry moves forward, the integration of artificial intelligence and edge computing into display ecosystems will unlock new avenues for interactive public information kiosks and high-fidelity private viewing experiences. This technological evolution presents manufacturers with a specialized market to develop application-specific, energy-efficient solutions tailored for the next generation of intelligent urban infrastructure and creative storytelling. These systems not only improve daily communication but also contribute to long-term sustainability by reducing physical waste and optimizing power usage through intelligent brightness adjustments.

Video Wall Market Size and Share Analysis:

The Video Wall market demonstrates steady growth, with size and share analysis revealing evolving trends and competitive positioning among key players. The report further examines subsegments categorized within product and service, application, and end-user, offering insights into their contribution to overall market performance.

Based on product and service, the Video Wall Displays sub-segment commands the majority share, driven by the shift toward bezel-less panels and innovative self-emissive chips.

Within applications, the Outdoor Advertisement sub-segment accounts for a substantial portion of revenue due to the massive scale of installations in urban centers and stadiums.

Regarding end-users, the Retail sub-segment remains a dominant contributor, leveraging interactive walls to boost consumer engagement, while the Hospitality and Transportation sub-segment is seeing rapid share expansion as airports and rail terminals modernize their passenger information systems.

Australia, China, India, Japan, South Korea, Indonesia, Malaysia, Philippines, Singapore, Thailand, Vietnam, Bangladesh, New Zealand, Taiwan

South and Central America

Brazil, Argentina, Peru, Chile, Colombia

Middle East and Africa

Bahrain, Kuwait, Oman, Qatar, Saudi Arabia, United Arab Emirates, Turkiye, South Africa, Egypt, Algeria, Nigeria

Market leaders and key company profiles

Samsung Electronics Co., Ltd.

LG Electronics Inc.

Leyard Optoelectronic Co., Ltd.

Barco NV

Sharp

NEC Display Solutions Ltd.

Sony Corporation

Panasonic Corporation

Christie Digital Systems USA, Inc.

Unilumin Group Co., Ltd.

Absen Optoelectronic Co., Ltd.

Daktronics, Inc.

Planar Systems, Inc.

Get more information on this report

Video Wall Market Report Coverage and Deliverables:

The "Video Wall Market Size and Forecast (2022–2033)" report provides a detailed analysis of the market covering below areas:

Video Wall market size and forecast at global, regional, and country levels for all the key market segments covered under the scope

Video Wall market trends, as well as market dynamics such as drivers, restraints, and key opportunities

Video Wall market analysis covering key market trends, global and regional framework, major players, regulations, and recent market developments

Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments for the Video Wall market

Detailed company profiles, including SWOT analysis

Video Wall Market Geographic Insights:

The geographical scope of the Video Wall market report is divided into five regions: North America, Asia Pacific, Europe, the Middle East & Africa, and South & Central America.

In North America, the landscape is shaped by a highly developed corporate ecosystem and a robust defense sector, where the demand for ultra-high-resolution displays for mission-critical command centers and collaborative executive spaces remains a central focus.

Europe demonstrates a sophisticated market specialized in high-end retail and public transportation, where stringent environmental standards drive the adoption of green, energy-efficient display technologies and sustainable architectural integrations.

The Asia-Pacific region stands as a dominant force for both large-scale production and rapid consumption, fueled by massive urbanization, extensive smart city initiatives, and an aggressive shift toward digital-out-of-home advertising in densely populated metropolitan hubs.

In the Middle East & Africa, market expansion is characterized by the development of iconic tourism infrastructure and the modernization of governmental facilities through large-scale visual installations in emerging smart districts. Meanwhile, South & Central America are witnessing a steady digital transformation as regional retail and hospitality sectors increasingly invest in high-impact visual communication to enhance consumer engagement and modernize public information systems. This diverse regional activity ensures a resilient global market as local economies continue to pivot toward data-driven visual environments and immersive digital experiences.

Get more information on this report

Video Wall Market Research Report Guidance:

The report includes qualitative and quantitative data in the Video Wall market across product and service, application, end-user, and geography.

The report starts with the key takeaways (chapter 2), highlighting the key trends and outlook of the Video Wall market.

Chapter 3 includes the research methodology of the study.

Chapter 4 further includes ecosystem analysis.

Chapter 5 highlights the major industry dynamics in the Video Wall market, including factors that are driving the market, prevailing deterrents, potential opportunities, as well as future trends. Impact analysis of these drivers and restraints is also covered in this section.

Chapter 6 discusses the Video Wall market scenario, in terms of historical market revenues, and forecast till the year 2033.

Chapters 7 to 10 cover Video Wall market segments by product and service, application, end-user, and geography across North America, Europe, Asia Pacific, the Middle East and Africa, and South and Central America. They cover the market revenue, forecast, and factors driving the market.

Chapter 11 describes the competitive analysis along with the heat map analysis for the key players operating in the market.

Chapter 12 describes the industry landscape analysis. It provides detailed descriptions of business activities such as market initiatives, new developments, mergers, and joint ventures globally, along with a competitive landscape.

Chapter 13 provides detailed profiles of the major companies operating in the Video Wall market. Companies have been profiled on the basis of their key facts, business descriptions, products and services, financial overview, SWOT analysis, and key developments.

Chapter 14, i.e., the appendix, is inclusive of a brief overview of the company, list of abbreviations, and a disclaimer.

Video Wall Market News and Key Development:

The Video Wall market is evaluated by gathering qualitative and quantitative data post primary and secondary research, which includes important corporate publications, association data, and databases. A few of the key developments in the Video Wall market are:

In November 2025, Samsung Electronics announced a new edition of its flagship large-format LED display, The Wall MPF series, which marked a pivotal expansion of its Chip on Board lineup. This latest video wall was engineered to optimize viewing experiences across diverse environments, serving as a high-performance centerpiece for corporate offices, command centers, and luxury residences. By leveraging Black Seal Technology+ and AI-driven upscaling, the series delivered enhanced brightness and superior black levels, further solidifying the role of the video wall as an essential tool for immersive visual communication in high-impact commercial and private spaces.

In September 2025, Barco showcased its leadership in the premium segment by introducing the Runar and TruePix Bifrost TP-I, two groundbreaking video wall solutions specifically engineered for the luxury home cinema market at CEDIA 2025. The Barco Runar debuted as the first video wall designed to meet DCI-certified HDR performance standards for residential use. At the same time, the TruePix Bifrost TP-I utilized advanced architecture to deliver exceptional brightness and energy efficiency in high-ambient-light environments. Additionally, the company demonstrated its Heimdall projector platform, highlighting a comprehensive portfolio of high-fidelity visual technologies.

Key Sources Referred:

World Bank – Global Trade IndicatorsWorld Trade Organization (WTO)(International Monetary Fund )IMFInternational Trade Administration (ITA)Company websiteCompany annual reportsCompany investor presentations

The List of Companies - Video Wall Market

Samsung Electronics Co., Ltd.

LG Electronics Inc.

Leyard Optoelectronic Co., Ltd.

Barco NV

Sharp

NEC Display Solutions Ltd.

Sony Corporation

Panasonic Corporation

Christie Digital Systems USA, Inc.

Unilumin Group Co., Ltd.

Absen Optoelectronic Co., Ltd.

Daktronics, Inc.

Planar Systems, Inc.

Frequently Asked Questions

How big is the Video Wall Market?

The Video Wall Market is valued at US$ 12.69 billion in 2025, it is projected to reach US$ 31.64 billion by 2033.

What is the CAGR for Video Wall Market by (2026 - 2033)?

As per our report Video Wall Market, the market size is valued at US$ 12.69 billion in 2025, projecting it to reach US$ 31.64 billion by 2033. This translates to a CAGR of approximately 12.10% during the forecast period.

What segments are covered in this report?

The Video Wall Market report typically cover these key segments-

Product and Service (Video Wall Displays and Installation)

Application (Indoor Advertisement, Outdoor Advertisement, Menu Board Advertisement, and Billboard Advertisement)

End-user (Retail, Corporate, Government, Hospitality and Transportation, Entertainment, Healthcare, Education, Retail Banking, and Other End Users)

End-Use (Consumer Electronics, Automotive, Industrial, Military, Healthcare, and Telecommunications)

What is the historic period, base year, and forecast period taken for Video Wall Market?

The historic period, base year, and forecast period can vary slightly depending on the specific market research report. However, for the Video Wall Market report:

Historic Period : 2022-2024

Base Year : 2025

Forecast Period : 2026-2033

Who are the major players in Video Wall Market?

The Video Wall Market is populated by several key players, each contributing to its growth and innovation. Some of the major players include:

Samsung Electronics Co., Ltd.

LG Electronics Inc.

Leyard Optoelectronic Co., Ltd.

Barco NV

Sharp

NEC Display Solutions Ltd.

Sony Corporation

Panasonic Corporation

Christie Digital Systems USA, Inc.

Unilumin Group Co., Ltd.

Absen Optoelectronic Co., Ltd.

Daktronics, Inc.

Planar Systems, Inc.

Who should buy this report?

The Video Wall Market report is valuable for diverse stakeholders, including:

Investors: Provides insights for investment decisions pertaining to market growth, companies, or industry insights. Helps assess market attractiveness and potential returns.

Industry Players: Offers competitive intelligence, market sizing, and trend analysis to inform strategic planning, product development, and sales strategies.

Suppliers and Manufacturers: Helps understand market demand for components, materials, and services related to concerned industry.

Researchers and Consultants: Provides data and analysis for academic research, consulting projects, and market studies.

Financial Institutions: Helps assess risks and opportunities associated with financing or investing in the concerned market.

Essentially, anyone involved in or considering involvement in the Video Wall Market value chain can benefit from the information contained in a comprehensive market report.

Get Free Sample For Video Wall Market

Get Free Sample For Video Wall Market