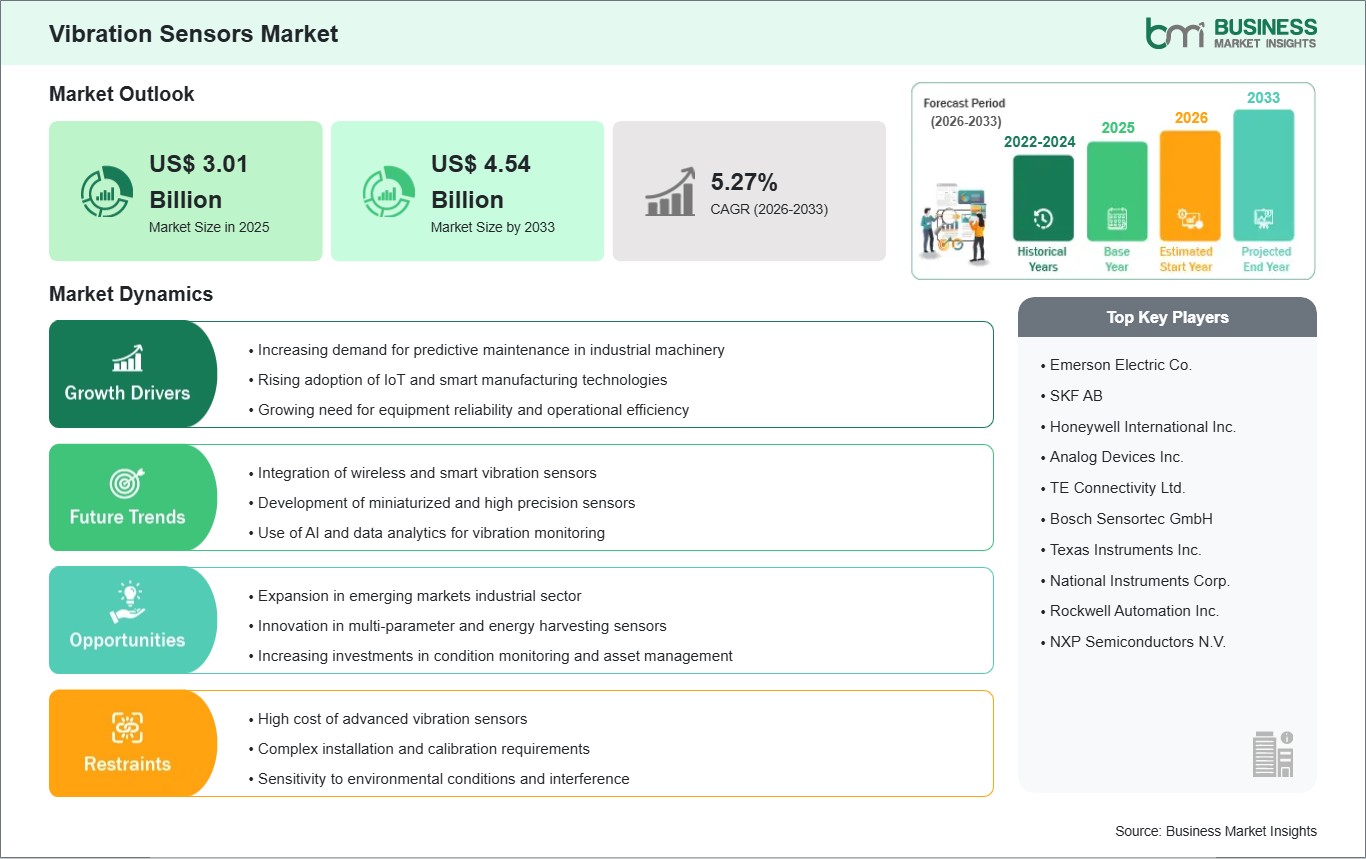

The Vibration Sensors Market size is expected to reach US$ 4.54 billion by 2033 from US$ 3.01 billion in 2025. The market is estimated to record a CAGR of 5.27% from 2026 to 2033.

Executive Summary and Global Market Analysis:

Vibration sensors are sophisticated electromechanical instruments engineered to detect, measure, and analyze mechanical oscillations or movements within various systems. These components serve as the critical "nervous system" for modern machinery, converting physical motion into measurable electrical signals—typically through piezoelectric, piezoresistive, or capacitive technologies. By providing real-time data on displacement, velocity, and acceleration, vibration sensors enable the early detection of structural imbalances, bearing wear, and mechanical fatigue, making them indispensable in high-stakes environments such as aerospace turbines, industrial manufacturing lines, and automotive safety systems. As the backbone of condition-based monitoring, they are the primary enabler of the global shift from reactive repair to intelligent, data-driven maintenance.

Despite their critical utility, the market faces significant restraints, including high initial installation costs for complex multi-sensor networks and technical challenges related to signal interference in electromagnetically noisy industrial environments. Furthermore, the integration of these sensors into legacy equipment often requires specialized expertise and significant downtime, which can deter small-to-medium-sized enterprises from immediate adoption.

However, these challenges are increasingly outweighed by lucrative opportunities stemming from the rapid maturation of Industry 4.0. The convergence of 5G connectivity, miniaturized MEMS (Micro-Electro-Mechanical Systems) technology, and edge-native AI processing is creating a new frontier for "smart" vibration sensing. These advancements allow for ultra-low-power, wireless deployments that provide granular, autonomous insights, ensuring the market remains on a robust upward trajectory as global industries prioritize operational resilience and hyper-automation.

Vibration Sensors Market - Strategic Insights:

Get more information on this report

Vibration Sensors Market Segmentation Analysis:

Key segments that contributed to the derivation of the Vibration Sensors market analysis are product and end user.

By Product, the market is segmented into Accelerometers, Velocity Sensors, Non-contact Displacement Transducers, and Others.

By End-User, the market is categorized into Automotive, Healthcare, Aerospace and Defense, Consumer Electronics, Oil and Gas, and Others.

Vibration Sensors Market Drivers and Opportunities:

The Paradigm Shift Toward Predictive Maintenance and Industrial IoT

The primary catalyst driving the vibration sensors market is the aggressive global transition toward predictive maintenance (PdM) frameworks within the industrial sector. Traditional maintenance cycles—either reactive or strictly schedule-based—are increasingly viewed as inefficient and prone to causing unplanned downtime, which can cost manufacturers millions of dollars in lost productivity. Vibration sensors act as the foundational hardware for Industrial Internet of Things (IIoT) ecosystems, providing the continuous data stream necessary to identify "silent" failures before they manifest as catastrophic breakdowns.

By monitoring the specific frequency signatures of rotating equipment such as motors, pumps, and compressors, these sensors allow facility managers to optimize asset lifecycles and reduce maintenance overhead by up to 30%. This driver is further amplified by the roll-out of 5G Standalone networks, which provide the high-bandwidth, low-latency communication required to manage thousands of sensor nodes in real-time across vast manufacturing footprints. As industries like oil and gas and power generation strive for "zero-downtime" targets, the demand for high-precision, wide-bandwidth vibration sensors continues to escalate, positioning them as a non-discretionary investment in the modern industrial signal chain.

Integration of Edge AI and Autonomous "Sensing-to-Inference" Pipelines

A significant growth opportunity lies in the evolution of vibration sensors from simple data collectors into intelligent edge-processing nodes. Traditionally, raw vibration data—which can be extremely high-frequency—had to be transmitted to centralized servers or the cloud for complex Fast Fourier Transform (FFT) analysis, leading to significant latency and high power consumption. The emergence of Edge AI allows machine learning algorithms to be embedded directly into the sensor's micro-circuitry, enabling the device to perform on-board anomaly detection and only transmit relevant "health alerts" rather than massive streams of raw data. This shift is particularly transformative for the automotive and aerospace sectors, where instantaneous decision-making is critical for safety.

For instance, in autonomous vehicles, edge-integrated vibration sensors can detect subtle changes in road surface or mechanical integrity in milliseconds, informing the vehicle's central computer of potential hazards without the delay of cloud processing. By 2033, as AI-driven "micro-intelligence" becomes the standard, manufacturers have a massive opportunity to develop specialized, low-power vibration SoCs (System-on-Chip) that offer a plug-and-play solution for the next generation of autonomous robotics and intelligent structural health monitoring systems.

Vibration Sensors Market Size and Share Analysis:

The Vibration Sensors market demonstrates steady growth, with size and share analysis revealing evolving trends and competitive positioning among key players. The report further examines subsegments categorized within product and end user, offering insights into their contribution to overall market performance.

Within the product category, the Accelerometers sub-segment represents a major share of the market due to their versatile application in measuring both static and dynamic forces across the automotive and consumer electronics sectors.

From an end-user perspective, the Automotive sub-segment is demonstrating significant growth as manufacturers integrate vibration monitoring into advanced driver assistance systems (ADAS) and electric vehicle (EV) powertrain diagnostics.

Additionally, the Oil and Gas sub-segment under end-user classification continues to be a vital contributor, utilizing high-temperature, explosion-proof vibration sensors to maintain the integrity of critical drilling and refinery infrastructure in harsh environments.

Australia, China, India, Japan, South Korea, Indonesia, Malaysia, Philippines, Singapore, Thailand, Vietnam, Bangladesh, New Zealand, Taiwan

South and Central America

Brazil, Argentina, Peru, Chile, Colombia

Middle East and Africa

Bahrain, Kuwait, Oman, Qatar, Saudi Arabia, United Arab Emirates, Turkiye, South Africa, Egypt, Algeria, Nigeria

Market leaders and key company profiles

Emerson Electric Co.

SKF AB

Honeywell International Inc.

Analog Devices Inc.

TE Connectivity Ltd.

Bosch Sensortec GmbH

Texas Instruments Inc.

National Instruments Corp.

Rockwell Automation Inc.

NXP Semiconductors N.V.

Get more information on this report

Vibration Sensors Market Report Coverage and Deliverables:

The "Vibration Sensors Market Size and Forecast (2022–2033)" report provides a detailed analysis of the market covering below areas:

Vibration Sensors market size and forecast at global, regional, and country levels for all the key market segments covered under the scope

Vibration Sensors market trends, as well as market dynamics such as drivers, restraints, and key opportunities

Vibration Sensors market analysis covering key market trends, global and regional framework, major players, regulations, and recent market developments

Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments for the Vibration Sensors market

Detailed company profiles, including SWOT analysis

Vibration Sensors Market Geographic Insights:

The geographical scope of the Vibration Sensors market report is divided into five regions: North America, Asia Pacific, Europe, the Middle East & Africa, and South & Central America.

In North America, the market is primarily sustained by an advanced aerospace and defense sector that mandates rigorous structural health monitoring and high-precision signal integrity for mission-critical assets.

Europe demonstrates a sophisticated focus on the integration of high-end vibration sensing within automated automotive production lines and the expanding renewable energy infrastructure, particularly for offshore wind turbine diagnostics.

The Asia Pacific region functions as a high-volume manufacturing hub, where aggressive nationwide digital transformation initiatives and the rapid expansion of semiconductor fabrication facilities propel widespread sensor adoption.

In the Middle East & Africa, market activity is increasingly defined by the modernization of legacy oil and gas infrastructure through the implementation of wireless condition-monitoring systems in remote environments. South & Central America are witnessing a progressive shift toward industrial automation, driven by the digital overhaul of regional mining operations and the adoption of smart processing technologies to enhance worker safety and operational efficiency. This geographical spread ensures a stable market environment as localized industries transition toward high-fidelity, data-centric operational frameworks.

Get more information on this report

Vibration Sensors Market Research Report Guidance:

The report includes qualitative and quantitative data in the Vibration Sensors market across product, end user, and geography.

The report starts with the key takeaways (chapter 2), highlighting the key trends and outlook of the Vibration Sensors market.

Chapter 3 includes the research methodology of the study.

Chapter 4 further includes ecosystem analysis.

Chapter 5 highlights the major industry dynamics in the Vibration Sensors market, including factors that are driving the market, prevailing deterrents, potential opportunities, as well as future trends. Impact analysis of these drivers and restraints is also covered in this section.

Chapter 6 discusses the Vibration Sensors market scenario, in terms of historical market revenues, and forecast till the year 2033.

Chapters 7 to 10 cover the Vibration Sensors market segments by product, end user, and geography across North America, Europe, Asia Pacific, the Middle East and Africa, and South and Central America. They cover the market revenue, forecast, and factors driving the market.

Chapter 11 describes the competitive analysis along with the heat map analysis for the key players operating in the market.

Chapter 12 describes the industry landscape analysis. It provides detailed descriptions of business activities such as market initiatives, new developments, mergers, and joint ventures globally, along with a competitive landscape.

Chapter 13 provides detailed profiles of the major companies operating in the Vibration Sensors market. Companies have been profiled on the basis of their key facts, business descriptions, products and services, financial overview, SWOT analysis, and key developments.

Chapter 14, i.e., the appendix, is inclusive of a brief overview of the company, list of abbreviations, and a disclaimer.

Vibration Sensors Market News and Key Development:

The Vibration Sensors market is evaluated by gathering qualitative and quantitative data post primary and secondary research, which includes important corporate publications, association data, and databases. A few of the key developments in the Vibration Sensors market are:

In January 2026, Texas Instruments (TI) introduced new automotive semiconductors and development resources to enhance safety and autonomy across various vehicle models. At the event, TI's scalable TDA5 high-performance computing system-on-a-chip (SoC) family offered power- and safety-optimized processing and edge artificial intelligence (AI) that supported up to Society of Automotive Engineers Level 3 vehicle autonomy. TI also unveiled the AWR2188, a single-chip, eight-by-eight 4D imaging radar transceiver, which worked alongside high-fidelity Vibration Sensors to help engineers simplify high-resolution radar and safety systems. These devices, alongside the DP83TD555J-Q1 10BASE-T1S Ethernet physical layer (PHY), joined TI's broader automotive portfolio for next-generation advanced driver assistance systems (ADAS) and software-defined vehicles (SDVs). TI debuted these products at CES 2026, held from Jan. 6-9 in Las Vegas, Nevada.

In March 2025, TE Connectivity launched the 85x1N and 89x1N series of IoT-enabled wireless Vibration Sensors, which utilized long-range LoRaWAN and Bluetooth connectivity to support predictive maintenance in harsh industrial environments. These compact devices featured a high-stability piezoelectric core and integrated edge computing for localized signal processing, providing up to ten years of battery life for remote monitoring applications.

Key Sources Referred:

World Bank – Global Trade IndicatorsWorld Trade Organization (WTO)(International Monetary Fund )IMFInternational Trade Administration (ITA)Company websiteCompany annual reportsCompany investor presentations

The List of Companies - Vibration Sensors Market

Emerson Electric Co.

SKF AB

Honeywell International Inc.

Analog Devices Inc.

TE Connectivity Ltd.

Bosch Sensortec GmbH

Texas Instruments Inc.

National Instruments Corp.

Rockwell Automation Inc.

NXP Semiconductors N.V.

Frequently Asked Questions

How big is the Vibration Sensors Market?

The Vibration Sensors Market is valued at US$ 3.01 Billion in 2025, it is projected to reach US$ 4.54 Billion by 2033.

What is the CAGR for Vibration Sensors Market by (2026 - 2033)?

As per our report Vibration Sensors Market, the market size is valued at US$ 3.01 Billion in 2025, projecting it to reach US$ 4.54 Billion by 2033. This translates to a CAGR of approximately 5.27% during the forecast period.

What segments are covered in this report?

The Vibration Sensors Market report typically cover these key segments-

Product (Sensors/Detectors,Smoke Detectors,Call Points,Fire Alarm Panels and Devices,Input/Output Modules)

System Type (Fully Wireless Systems,Hybrid Systems)

Installation Type (New Installation,Retrofit Installation)

What is the historic period, base year, and forecast period taken for Vibration Sensors Market?

The historic period, base year, and forecast period can vary slightly depending on the specific market research report. However, for the Vibration Sensors Market report:

Historic Period : 2022-2024

Base Year : 2025

Forecast Period : 2026-2033

Who are the major players in Vibration Sensors Market?

The Vibration Sensors Market is populated by several key players, each contributing to its growth and innovation. Some of the major players include:

Emerson Electric Co.

SKF AB

Honeywell International Inc.

Analog Devices Inc.

TE Connectivity Ltd.

Bosch Sensortec GmbH

Texas Instruments Inc.

National Instruments Corp.

Rockwell Automation Inc.

NXP Semiconductors N.V.

Who should buy this report?

The Vibration Sensors Market report is valuable for diverse stakeholders, including:

Investors: Provides insights for investment decisions pertaining to market growth, companies, or industry insights. Helps assess market attractiveness and potential returns.

Industry Players: Offers competitive intelligence, market sizing, and trend analysis to inform strategic planning, product development, and sales strategies.

Suppliers and Manufacturers: Helps understand market demand for components, materials, and services related to concerned industry.

Researchers and Consultants: Provides data and analysis for academic research, consulting projects, and market studies.

Financial Institutions: Helps assess risks and opportunities associated with financing or investing in the concerned market.

Essentially, anyone involved in or considering involvement in the Vibration Sensors Market value chain can benefit from the information contained in a comprehensive market report.

Get Free Sample For Vibration Sensors Market

Get Free Sample For Vibration Sensors Market