01

Market Summery

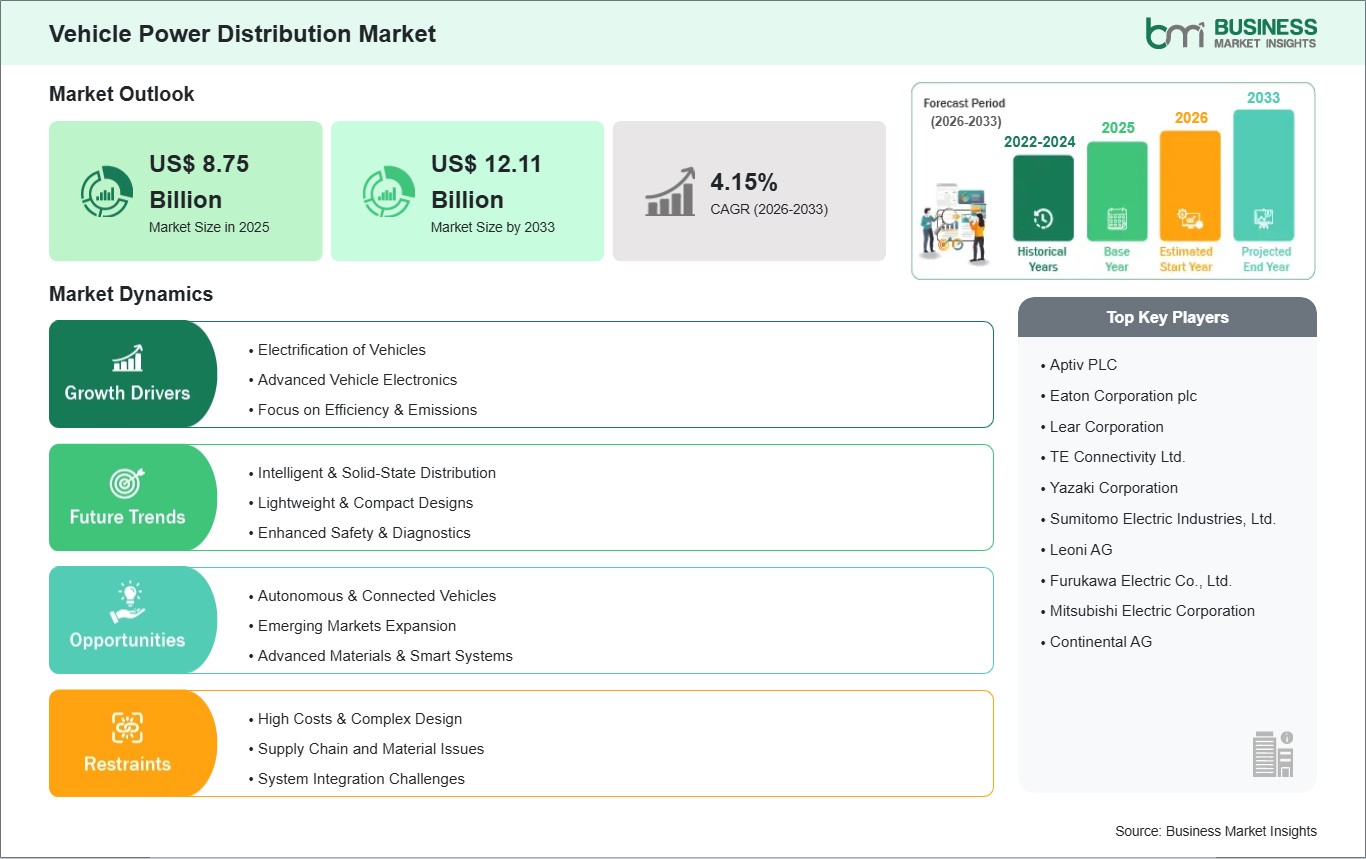

Executive Summary and Global Market Analysis

The vehicle power distribution system serves as the central nervous system of an automobile's electrical architecture, responsible for the safe and efficient routing of electrical energy from the battery and alternator to various electronic control units (ECUs), sensors, and actuators. As modern vehicles transition toward Software-Defined Vehicles (SDVs) and high-voltage electric powertrains, these distribution systems have evolved from simple mechanical fuse boxes into sophisticated, intelligent modules capable of real-time monitoring and diagnostic feedback.

However, the market faces significant restraints, including the extreme complexity of integrating 800V high-voltage systems with legacy low-voltage components and the rising cost of raw materials like copper and advanced semiconductors. Furthermore, the industry must navigate stringent electromagnetic compatibility (EMC) standards and thermal management hurdles as power densities increase within compact engine bays, potentially increasing development timelines by up to 25%.

Despite these challenges, lucrative opportunities remain in the surging demand for zonal E/E architectures and the rapid adoption of solid-state power distribution. These innovations allow for significant vehicle weight reduction, cutting wire harness length by up to 30%, and enhancing redundancy for safety-critical autonomous driving features. By implementing semiconductor-based "eFuses" and intelligent zone controllers, OEMs can achieve fail-operational capabilities and over-the-air (OTA) power management. As the industry prioritizes energy efficiency to extend EV range, the market is poised for a transformative shift toward intelligent, software-configurable power networks that support the next generation of intelligent mobility.

03

Segment Analysis

Vehicle Power Distribution Market Segmentation

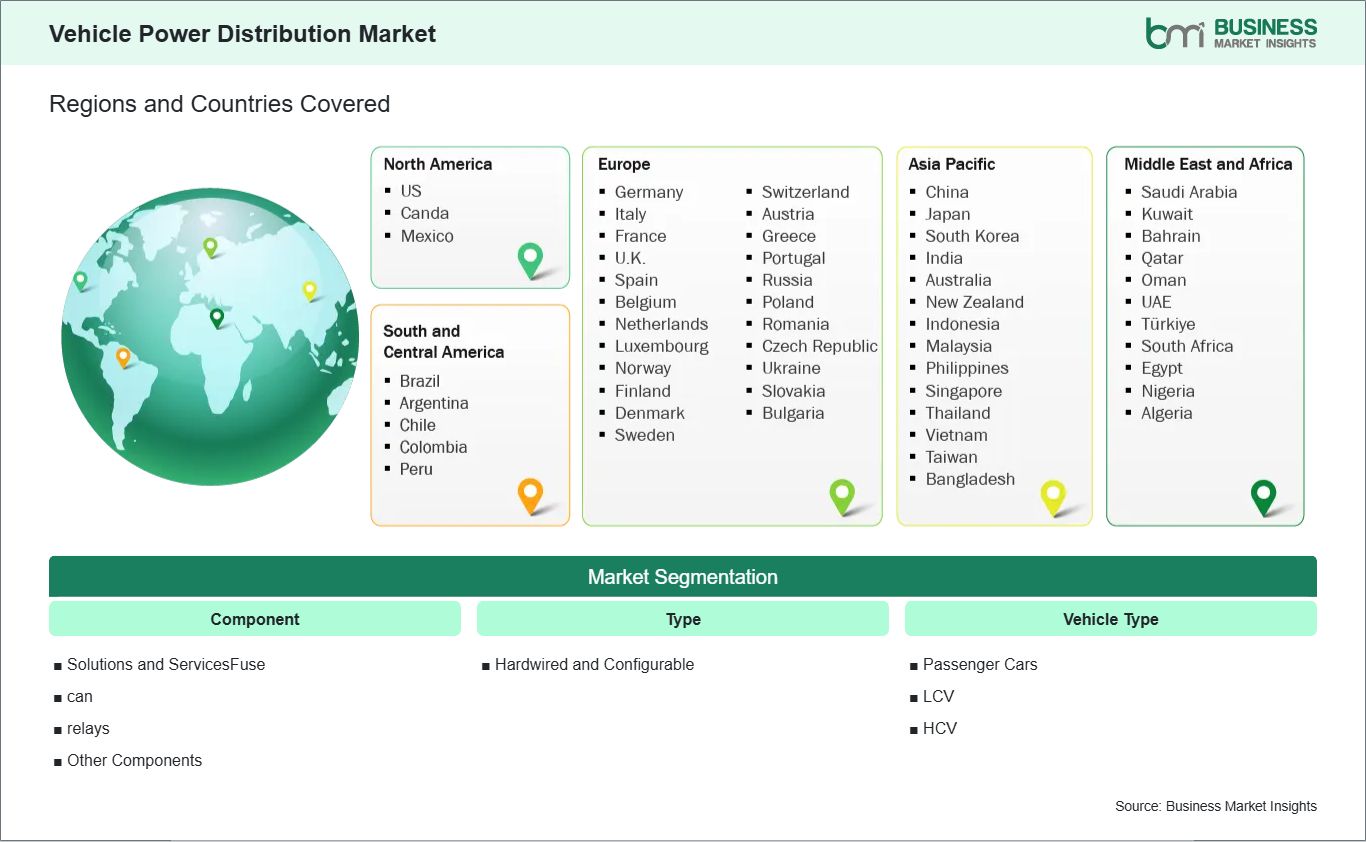

Key segments that contributed to the derivation of the Vehicle Power Distribution market analysis are component, type, and vehicle type.

- By Component, the market is segmented into Fuse, can, relays, and Others.

- By Type, the market is divided into Hardwired and Configurable.

- By Vehicle Type, the market is categorized into Passenger Cars, LCV (Light Commercial Vehicles), and HCV (Heavy Commercial Vehicles).

04

Market Forces

Vehicle Power Distribution Market Drivers and Opportunities

Evolution of Zonal E/E Architectures in Software-Defined Vehicles

The primary driver for the vehicle power distribution market is the industry-wide transition from traditional distributed electrical architectures to centralized zonal E/E architectures. In conventional setups, miles of heavy wiring harnesses connect individual components to a central power source, leading to excessive weight and manufacturing complexity. However, the rise of software-defined vehicles necessitates a more streamlined approach where zonal controllers manage power and data for specific physical sections of the vehicle. This shift significantly reduces the total length of the wiring harness, directly improving vehicle range and assembly efficiency.

As the industry moves toward highly automated platforms, the deployment of high-performance computing systems requires these power distribution units to handle much higher data and power throughput with minimal latency. Consequently, the demand for intelligent power distribution blocks that can communicate with the vehicle's central processing unit is accelerating. These modules provide the granular control and over-the-air updateability required for modern, connected automotive platforms, allowing manufacturers to modify power logic through software rather than physical hardware changes. This architectural revolution ensures that power distribution is no longer a passive hardware layer but a dynamic, programmable component of the vehicle's digital ecosystem.

Adoption of Solid-State Power Distribution for Autonomous Redundancy

A substantial growth opportunity lies in the transition from traditional mechanical relays and fuses to solid-state power distribution technologies. Mechanical components are prone to wear over time and lack the precision required for mission-critical autonomous driving systems. Solid-state solutions, utilizing advanced wide-bandgap semiconductors, offer near-instantaneous switching and the ability to trip and reset digitally without human intervention. This is vital for high-level autonomous vehicles, which require redundant power paths to ensure that steering and braking systems remain operational even if a primary circuit fails.

Intelligent power management systems can now enable predictive maintenance by analyzing electrical signatures to detect impending failures before they occur. This transition not only enhances safety but also allows manufacturers to eliminate physical fuse access panels, giving designers more freedom in cabin layout and reducing the bill of materials for high-tech, fail-operational vehicle platforms. By replacing heavy copper-based protective devices with compact silicon-based alternatives, automakers can achieve a more sustainable and efficient energy profile. This shift represents a move toward a "smart" power grid within the car, capable of isolating faults and rerouting energy to critical systems in real-time to prevent catastrophic system loss.

05

Size and Share Analysis

Vehicle Power Distribution Market Size and Share Analysis

The Vehicle Power Distribution market demonstrates steady growth, with size and share analysis revealing evolving trends and competitive positioning among key players. The report further examines subsegments categorized within component, type, and vehicle type, offering insights into their contribution to overall market performance.

In the component classification, the Relay sub-segment is currently maintaining a steady share due to its proven reliability in switching high-current loads across entry-level vehicle models.

Within the type category, the Configurable sub-segment is witnessing the fastest growth as OEMs seek software-controlled power management to support diverse vehicle configurations on a single production line.

Regarding vehicle type categories, the Passenger Cars sub-segment commands the largest portion of the market, driven by the massive integration of infotainment and ADAS features that require complex power routing. Geographically, the market is highly influenced by the rapid electrification of passenger fleets, ensuring that intelligent power distribution remains a core requirement for future-ready automotive architectures.

07

Report Coverage

Vehicle Power Distribution Market Report Coverage and Deliverables

The "Vehicle Power Distribution Market Size and Forecast (2022 - 2033)" report provides a detailed analysis of the market covering below areas:

- Vehicle Power Distribution market size and forecast at global, regional, and country levels for all the key market segments covered under the scope

- Vehicle Power Distribution market trends, as well as market dynamics such as drivers, restraints, and key opportunities

- Vehicle Power Distribution market analysis covering key market trends, global and regional framework, major players, regulations, and recent market developments

- Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments for the Vehicle Power Distribution market

- Detailed company profiles, including SWOT analysis

08

Geographic Insights

Vehicle Power Distribution Market Geographic Insights

The geographical scope of the Vehicle Power Distribution market report is divided into five regions: North America, Asia Pacific, Europe, the Middle East and Africa, and South and Central America.

In North America, market activity is characterized by a strong focus on high-reliability systems for heavy-duty commercial fleets and the aggressive integration of autonomous driving sensors, which necessitate robust, redundant power networks.

Europe remains at the forefront of regulatory-driven innovation, where stringent carbon emission mandates and a mature luxury vehicle sector drive the adoption of high-voltage distribution architectures and advanced lightweighting solutions.

The Asia-Pacific region serves as the global powerhouse for both production and consumption, bolstered by a massive electronics manufacturing ecosystem and rapid urbanization that fuels the demand for cost-effective, high-volume electrical components.

In the Middle East and Africa, the market is expanding through the modernization of logistics infrastructure and the gradual implementation of smart city initiatives that incorporate electric public transit systems.

Meanwhile, South and Central America are witnessing a steady digital transformation as regional manufacturers modernize production lines to integrate advanced telematics and basic electronic safety features. Collectively, these regional dynamics ensure a resilient global market as local automotive sectors align their electrical architectures with the broader trends of connectivity, sustainability, and intelligent automation.

10

Industry Activity

Recent Developments

The Vehicle Power Distribution market is evaluated by gathering qualitative and quantitative data post primary and secondary research, which includes important corporate publications, association data, and databases. A few of the key developments in the Vehicle Power Distribution market are:

- In February 2025, TE Connectivity plc (NYSE: TEL), a world leader in connectors and sensors, entered into a definitive agreement to acquire Richards Manufacturing Co. from funds managed by Oaktree Capital Management, L.P., and members of the Bier family. This strategic acquisition was designed to bolster TE's capabilities in the Vehicle Power Distribution and utility infrastructure sectors by combining complementary product portfolios. The transaction strengthened TE's position in serving electrical utilities in North America and added the specialized expertise of the Richards team, enabling the company to benefit from robust growth trends in underground electrical networks.

- November 2024, Yazaki (China) Investment Corporation, a Chinese subsidiary of Yazaki Corporation, held an opening ceremony for Beijing IAT Yazaki New Energy Technology Co., Ltd. at the joint venture's headquarters in Beijing and officially commenced operations. This new entity, established through a joint venture agreement with IAT Automobile Technology Co., Ltd., was specifically designed to focus on the research, development, and mass production of high-voltage Vehicle Power Distribution systems and drive components. By combining Yazaki's global manufacturing scale with IAT's engineering expertise, the joint venture aimed to overcome core technical challenges in energy efficiency and safety for the next generation of new energy vehicles.

11

Trust & Transparency

Research Methodology

The market analysis combines proprietary research with secondary data from government agencies, company disclosures, regulatory filings, industry databases and expert interviews. Market estimates are validated through data triangulation, cross-market benchmarking and analyst

review.

View Full Research Methodology

Key Sources Referred:

World Bank - Global Trade Indicators World Trade Organization (WTO) International Monetary Fund (IMF) International Trade Administration (ITA) Company website Company annual reports Company investor presentations