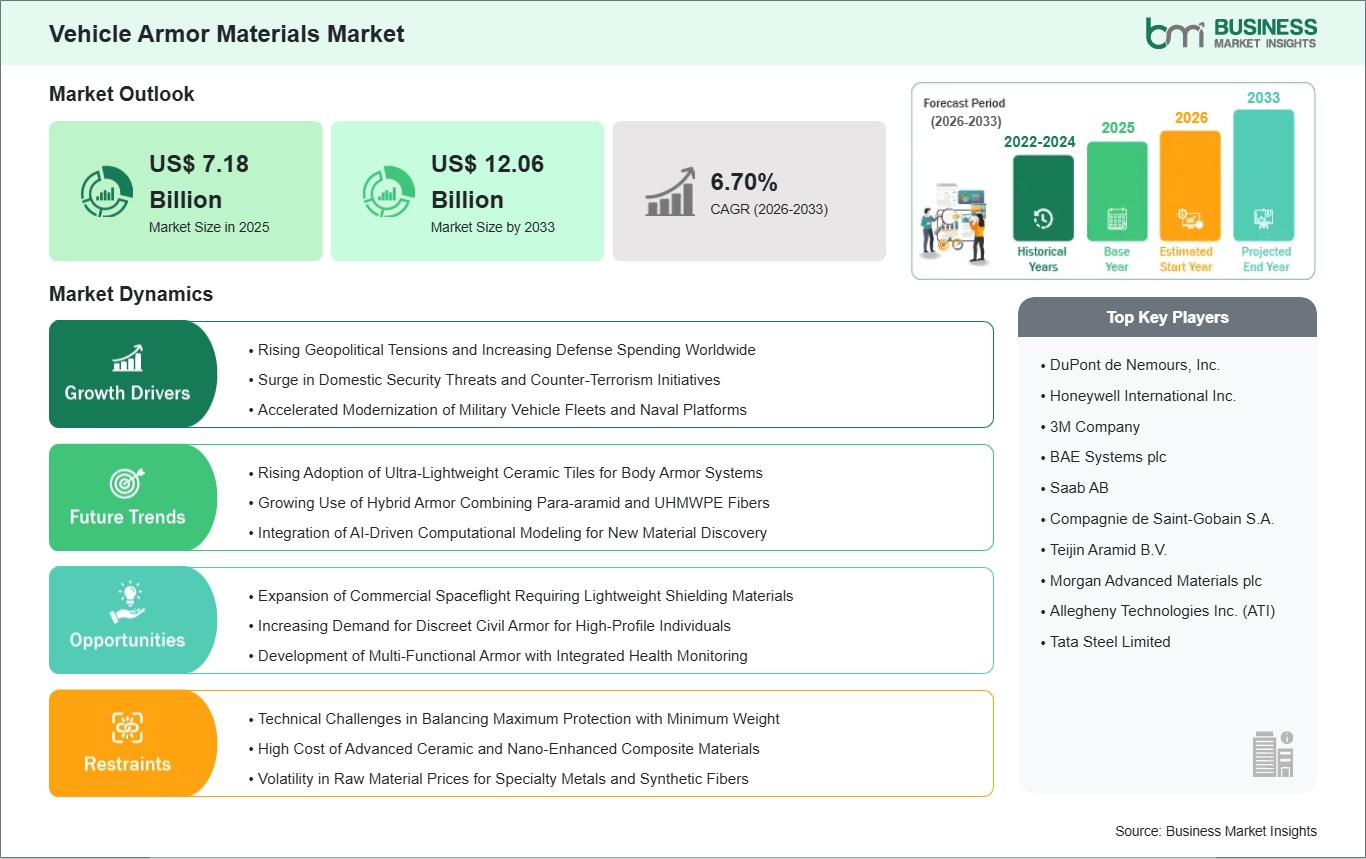

The Vehicle Armor Materials Market size is expected to reach US$ 12.06 billion by 2033 from US$ 7.18 billion in 2025. The market is estimated to record a CAGR of 6.70% from 2026 to 2033.

Executive Summary and Global Market Analysis:

The Vehicle Armor Materials market, which is a part of the aerospace and defense industry, is one of the most important pillars in the sector as it provides the required armor for the protection of personnel, vehicles, and infrastructure. The Vehicle Armor Materials market has witnessed the development of two parallel trends: the continuation of the use of conventional metal alloys in heavy-duty armor, and the rapid growth of advanced materials such as fibers and ceramics in lightweight armor. Although the Vehicle Armor Materials market is dominated by the defense sector, the footprint in the homeland security sector and civil use is increasing due to the instability in urban areas and the need for personal security. The market is in the midst of a high-innovation phase, where the goal is to increase survivability per pound to satisfy the mobility needs of modern security forces.

Growth is being driven by large-scale military modernization initiatives in North America and Asia Pacific, in addition to the commercialization of next-generation materials such as UHMWPE and carbon nanotube composite materials. Despite challenges related to high production costs and fluctuations in raw materials, opportunities related to space exploration and a burgeoning civil security market provide strong avenues for future growth. Going forward, the market is likely to transition toward smarter armor materials, which are capable of performing more than one function, including sensors and even energy harvesting. As a result, the Vehicle Armor Materials market is poised to remain a high-value segment of the global industrial sector.

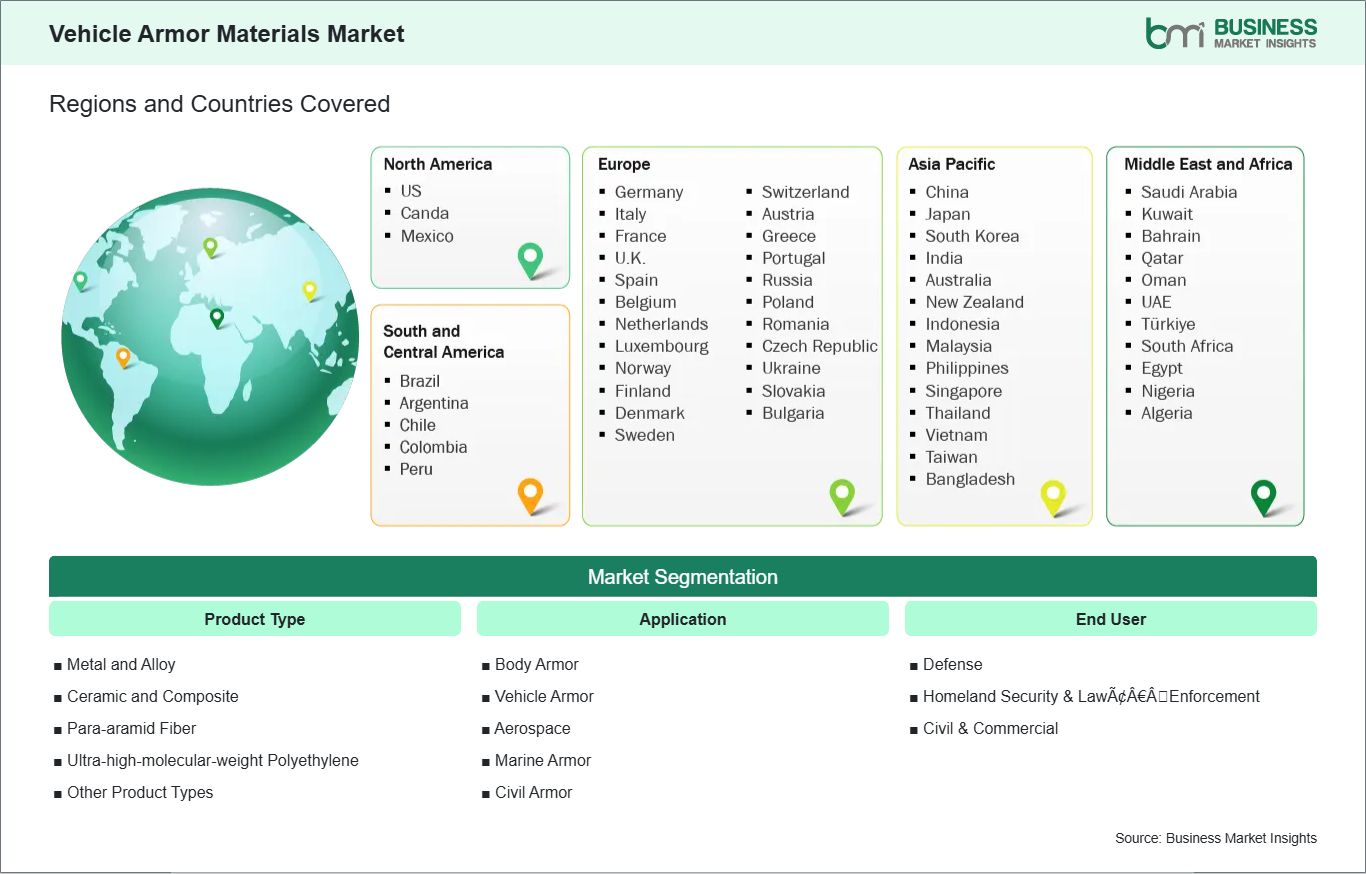

Key segments that contributed to the derivation of the Vehicle Armor Materials market analysis are product type, application, and end user.

By product type, the Vehicle Armor Materials market is segmented into Metal and Alloy, Ceramic and Composite, Para-aramid Fiber, Ultra-high-molecular-weight Polyethylene (UHMWPE), and Other Product Types. The Metal and Alloy segment dominated the market in 2025.

By application, the Vehicle Armor Materials market is segmented into Body Armor, Vehicle Armor, Aerospace, Marine Armor, and Civil Armor. The Vehicle Armor segment dominated the market in 2025.

By end user, the Vehicle Armor Materials market is segmented into Defense, Homeland Security & Law Enforcement, and Civil & Commercial. The Defense segment dominated the market in 2025.

Vehicle Armor Materials Market Drivers and Opportunities:

Rising Geopolitical Tensions and Increasing Defense Spending Worldwide

The current world security environment is characterized by changing alliances and regional wars, and in response, nations are in the process of heavily fortifying their defense systems. This has led to an increased budget in the defense sector with the aim of improving the survivability of frontline personnel and equipment. Vehicle Armor Materials are the epicenter of this increased budget in the defense sector as nations focus on acquiring the best materials that can offer protection against changing ballistic and unconventional explosive threats. This is not limited to the traditional defense powers of the world but also the emerging economies that are heavily investing in their local defense systems.

As modern warfare transitions toward more mobile and technologically integrated operations, the requirements for armor are becoming more stringent. Defense agencies are no longer just looking for thick protection but are demanding smart, integrated systems that can be rapidly deployed across various terrains. This environment fosters long-term government contracts for material suppliers, ensuring a stable revenue stream for companies capable of meeting rigorous military specifications. The ongoing cycle of threat-and-response—where new projectiles drive the development of newer, stronger materials—ensures that defense-related demand remains the primary engine for innovation and growth within the armor sector.

Rising Adoption of Ultra-Lightweight Ceramic Tiles for Body Armor Systems

The weight of personal protective equipment has always been a significant burden for soldiers and law enforcement officers, affecting maneuverability and increasing fatigue. To combat this, the industry is seeing a massive shift toward the use of advanced ceramics, such as boron carbide and silicon carbide, in body armor inserts. These materials offer extreme hardness at a fraction of the weight of traditional steel plates. When a projectile hit a ceramic tile, the material shatters locally, absorbing and dissipating the kinetic energy effectively. This allows for the production of Level IV plates that are light enough for extended wear while still providing protection against high-velocity rifle rounds.

This trend is being accelerated by advancements in ceramic manufacturing processes, which have made these once-exotic materials more affordable for large-scale deployment. Manufacturers are now utilizing modular ceramic designs that enhance multi-hit capabilities, a historic weakness of ceramic armor. By nesting small, high-purity tiles within a composite backing, the armor can localize damage and maintain integrity across the rest of the plate. This evolution in material design is transforming soldier systems, enabling a new generation of "high-mobility" infantry that remains fully protected without the physical toll associated with legacy armor systems.

Vehicle Armor Materials Market Size and Share Analysis:

The global Vehicle Armor Materials market is experiencing steady growth, with market size and share analysis reflecting evolving treatment preferences and competitive dynamics among key players. The report evaluates important subsegments categorized within product type, application, and end user, highlighting their respective contributions to overall market performance.

By product type, the Metal and Alloy subsegment dominated the market in 2025 due to its long-standing history of proven ballistic effectiveness and relatively low manufacturing costs. High-hardness steel, aluminum, and titanium remain the primary choices for heavy structural armor in tanks and large naval vessels, where their structural integrity and multi-hit capabilities are essential for survival in high-intensity combat.

By application, the Vehicle Armor subsegment dominated the market in 2025 because of massive global procurement programs for armored personnel carriers and main battle tanks. The high surface area of these platforms requires significant volumes of material, making vehicle protection the largest consumer of both traditional metals and modern composite strike plates.

By end user, the Defense subsegment dominated the market in 2025 as a result of escalating geopolitical tensions and national military modernization initiatives. Defense agencies command the largest budgets for large-scale acquisitions, spanning from individual soldier gear to heavy-duty tactical vehicles and advanced naval shielding.

Australia, China, India, Japan, South Korea, Indonesia, Malaysia, Philippines, Singapore, Thailand, Vietnam, Bangladesh, New Zealand, Taiwan

South and Central America

Brazil, Argentina, Peru, Chile, Colombia

Middle East and Africa

Bahrain, Kuwait, Oman, Qatar, Saudi Arabia, United Arab Emirates, Turkiye, South Africa, Egypt, Algeria, Nigeria

Market leaders and key company profiles

DuPont de Nemours, Inc.

Honeywell International Inc.

3M Company

BAE Systems plc

Saab AB

Compagnie de Saint-Gobain S.A.

Teijin Aramid B.V.

Morgan Advanced Materials plc

Allegheny Technologies Inc. (ATI)

Tata Steel Limited

Get more information on this report

Vehicle Armor Materials Market Report Coverage and Deliverables:

The "Vehicle Armor Materials Market Size and Forecast (2022 - 2033)" report provides a detailed analysis of the market covering below areas:

Vehicle Armor Materials market size and forecast at the regional and country levels for segments covered under the scope

Vehicle Armor Materials market trends, as well as drivers, restraints, and opportunities

Vehicle Armor Materials market analysis covering key trends, regional framework, major players, regulations, and recent developments

Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments for the Vehicle Armor Materials market

Detailed company profiles, including SWOT analysis

The geographical scope of the Vehicle Armor Materials market report is divided into: North America, Asia Pacific, Europe, Middle East & Africa, and South & Central America. North America held the largest share in 2025.

North America maintains its status as the leading regional market for Vehicle Armor Materials, a position rooted in having the world’s largest defense budget and a highly advanced military-industrial complex. The United States is the primary driver of this dominance, with consistent funding for multi-year procurement programs such as the modernization of the Army’s vehicle fleet and the continuous upgrading of soldier protection systems. The region is home to industry-leading material science firms like DuPont and Honeywell, whose R&D efforts set the global benchmark for ballistic fibers and composite performance. This concentration of technical expertise and manufacturing capacity allows North America to remain at the forefront of the transition from legacy steel to advanced lightweight materials.

The region’s lead is further reinforced by a strong homeland security sector and a growing civil armor market, where law enforcement agencies and private security firms prioritize high-quality, certified protective gear.

Furthermore, the North American market benefits from a well-established regulatory framework, such as the NIJ standards, which ensure material consistency and build consumer trust. As the U.S. and Canada continue to invest in aerospace defense and naval modernization, the demand for specialized armor for aircraft cockpits and ship hulls remains high. While other regions are growing rapidly, North America’s combination of technological leadership, massive procurement scale, and strategic focus on soldier survivability ensures it will continue to dictate the global direction of the Vehicle Armor Materials industry.

Get more information on this report

Vehicle Armor Materials Market Research Report Guidance:

The report includes qualitative and quantitative data in the Vehicle Armor Materials market across product type, application, end user, and geography.

The report starts with the key takeaways (chapter 2), highlighting the key trends and outlook of the Vehicle Armor Materials market.

Chapter 3 focuses on the research methodology of the study.

Chapter 4 includes ecosystem analysis.

Chapter 5 highlights the major industry dynamics in the Vehicle Armor Materials market, including factors that are driving the market, prevailing deterrents, potential opportunities, as well as future trends. Impact analysis of these drivers and restraints is also covered in this section.

Chapter 6 discusses the Vehicle Armor Materials market scenario, in terms of historical market revenues, and forecast till the year 2033.

Chapters 7 to 10 cover the Vehicle Armor Materials market segments by product type, application, end user, and geography across North America, Europe, Asia Pacific, the Middle East and Africa, and South and Central America. They cover the market revenue, forecast, and factors driving the market.

Chapter 11 describes the competitive analysis along with the heat map analysis for the key players operating in the market.

Chapter 12 describes the industry landscape analysis. It provides detailed descriptions of business activities such as market initiatives, new developments, mergers, and joint ventures globally, along with a competitive landscape.

Chapter 13 provides detailed profiles of the major companies operating in the Vehicle Armor Materials market. Companies have been profiled on the basis of their key facts, business descriptions, products, financial overview, SWOT analysis, and key developments.

Chapter 14, i.e., the appendix, is inclusive of a brief overview of the company, list of abbreviations, and disclaimer.

Vehicle Armor Materials Market News and Key Development:

The Vehicle Armor Materials market is evaluated by gathering qualitative and quantitative data post primary and secondary research, which includes important corporate publications, association data, and databases. A few of the key developments in the Vehicle Armor Materials market are:

In March 2023, Iten Defense, announced the acquisition of Transparent Armor Solutions, strengthening its portfolio in advanced transparent armor materials used in military ground vehicles and protective systems.

In January 2024, DuPont, announced an exclusive agreement with Point Blank Enterprises to supply advanced Kevlar® aramid fiber solutions for protective applications, including vehicle armor systems for law enforcement and defense sectors.

In 2024, Saint-Gobain, continued expansion of its advanced ceramics portfolio (including ballistic-grade materials) to support lightweight armor solutions for military vehicles and aerospace applications, aligned with growing demand for high-performance protective materials.

Key Sources Referred:

American Chemistry Council (ACC)International Council of Chemical Associations (ICCA)European Chemical Industry Council (Cefic)China National Packaging Industry Association (CNPIA)Indian Institute of Packaging (IIP)Japan Packaging Institute (JPI)Gulf Petrochemicals and Chemicals Association (GPCA)Company WebsitesCompany Annual ReportsCompany Investor Presentations

The List of Companies - Vehicle Armor Materials Market

DuPont de Nemours, Inc.

Honeywell International Inc.

3M Company

BAE Systems plc

Saab AB

Compagnie de Saint-Gobain S.A.

Teijin Aramid B.V.

Morgan Advanced Materials plc

Allegheny Technologies Inc. (ATI)

Tata Steel Limited

Frequently Asked Questions

How big is the Vehicle Armor Materials Market?

The Vehicle Armor Materials Market is valued at US$ 7.18 Billion in 2025, it is projected to reach US$ 12.06 Billion by 2033.

What is the CAGR for Vehicle Armor Materials Market by (2026 - 2033)?

As per our report Vehicle Armor Materials Market, the market size is valued at US$ 7.18 Billion in 2025, projecting it to reach US$ 12.06 Billion by 2033. This translates to a CAGR of approximately 6.70% during the forecast period.

What segments are covered in this report?

The Vehicle Armor Materials Market report typically cover these key segments-

Product Type (Metal and Alloy, Ceramic and Composite, Para-aramid Fiber, Ultra-high-molecular-weight Polyethylene, Other Product Types)

End User (Defense, Homeland Security & LawâEnforcement, and Civil & Commercial)

What is the historic period, base year, and forecast period taken for Vehicle Armor Materials Market?

The historic period, base year, and forecast period can vary slightly depending on the specific market research report. However, for the Vehicle Armor Materials Market report:

Historic Period : 2022-2024

Base Year : 2025

Forecast Period : 2026-2033

Who are the major players in Vehicle Armor Materials Market?

The Vehicle Armor Materials Market is populated by several key players, each contributing to its growth and innovation. Some of the major players include:

DuPont de Nemours, Inc.

Honeywell International Inc.

3M Company

BAE Systems plc

Saab AB

Compagnie de Saint-Gobain S.A.

Teijin Aramid B.V.

Morgan Advanced Materials plc

Allegheny Technologies Inc. (ATI)

Tata Steel Limited

Who should buy this report?

The Vehicle Armor Materials Market report is valuable for diverse stakeholders, including:

Investors: Provides insights for investment decisions pertaining to market growth, companies, or industry insights. Helps assess market attractiveness and potential returns.

Industry Players: Offers competitive intelligence, market sizing, and trend analysis to inform strategic planning, product development, and sales strategies.

Suppliers and Manufacturers: Helps understand market demand for components, materials, and services related to concerned industry.

Researchers and Consultants: Provides data and analysis for academic research, consulting projects, and market studies.

Financial Institutions: Helps assess risks and opportunities associated with financing or investing in the concerned market.

Essentially, anyone involved in or considering involvement in the Vehicle Armor Materials Market value chain can benefit from the information contained in a comprehensive market report.

Get Free Sample For Vehicle Armor Materials Market

Get Free Sample For Vehicle Armor Materials Market