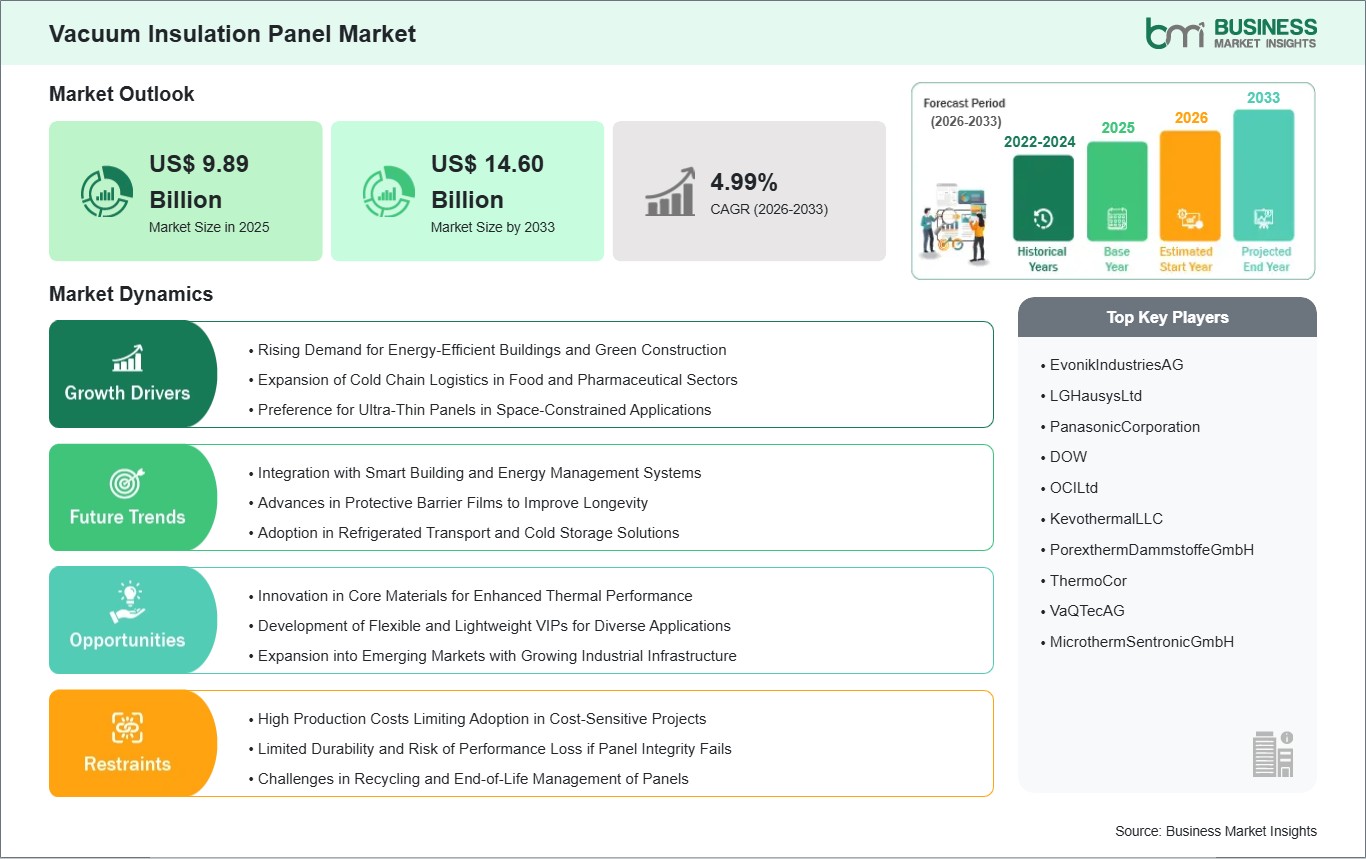

The Vacuum Insulation Panel Market size is expected to reach US$ 14.6 billion by 2033 from US$ 9.89 billion in 2025. The market is estimated to record a CAGR of 4.99% from 2026 to 2033.

Executive Summary and Global Market Analysis:

The global vacuum insulation panel (VIP) market has become strategically important because industrial sectors require modern thermal insulation materials that are better than traditional insulation products, which include fiberglass, polyurethane foam and polystyrene. Vacuum insulation panels function as advanced thermal protection systems that use core materials sealed inside gas-proof containers to create airtight spaces. The low-pressure interior design results in a significant reduction of heat transfer, which enables better insulation performance with thinner material requirements. The combination of space-saving features and efficient thermal performance makes VIPs an appealing solution for industries that need energy-saving capabilities, compact designs and dependable insulation systems.

The global VIP market experiences growth because building design professionals and construction organizations increasingly recognize the importance of energy-saving measures and environmentally friendly construction practices in all types of building projects. The development of building codes that require net-zero performance has driven regions to select advanced insulation solutions that maintain architectural aesthetics while decreasing energy needs for heating and cooling. VIPs serve multiple purposes in the construction industry, which requires space optimization and thermal efficiency for specialized equipment, including refrigerated display cases, energy-efficient refrigerated containers and ultra-thin wall systems used in cold chain logistics and refrigerated transport. The rising need for cold chain solutions, which support pharmaceutical and food processing and logistics operations, serves as another catalyst for growth. VIPs provide a dependable method for maintaining exact temperature requirements because their system uses less energy to control temperature in response to increasing global trade and rising demand for temperature-controlled shipping. Their use in refrigerated trucks, intermodal containers and cryogenic storage systems improves system efficiency while optimizing freight capacity.

The market experiences several significant obstacles that limit its potential. The high production cost and specialized manufacturing process for VIPs remain barriers to widespread adoption, which especially affects cost-sensitive construction projects and traditional insulation products where price competition dominates. Users prefer traditional materials for certain applications because insulation efficiency decreases when vacuum seals fail, and insulation materials lose their protective functions. VIP technologies are being developed through ongoing research, which focuses on creating new encapsulation systems, core materials and protective barrier films.

The industry is adopting better performance and sustainable solutions through product development work that improves durability and recyclability and simplifies product handling. VIPs will become crucial components of next-generation insulation technologies, which will be developed as various countries increase their infrastructure spending and energy efficiency requirements.

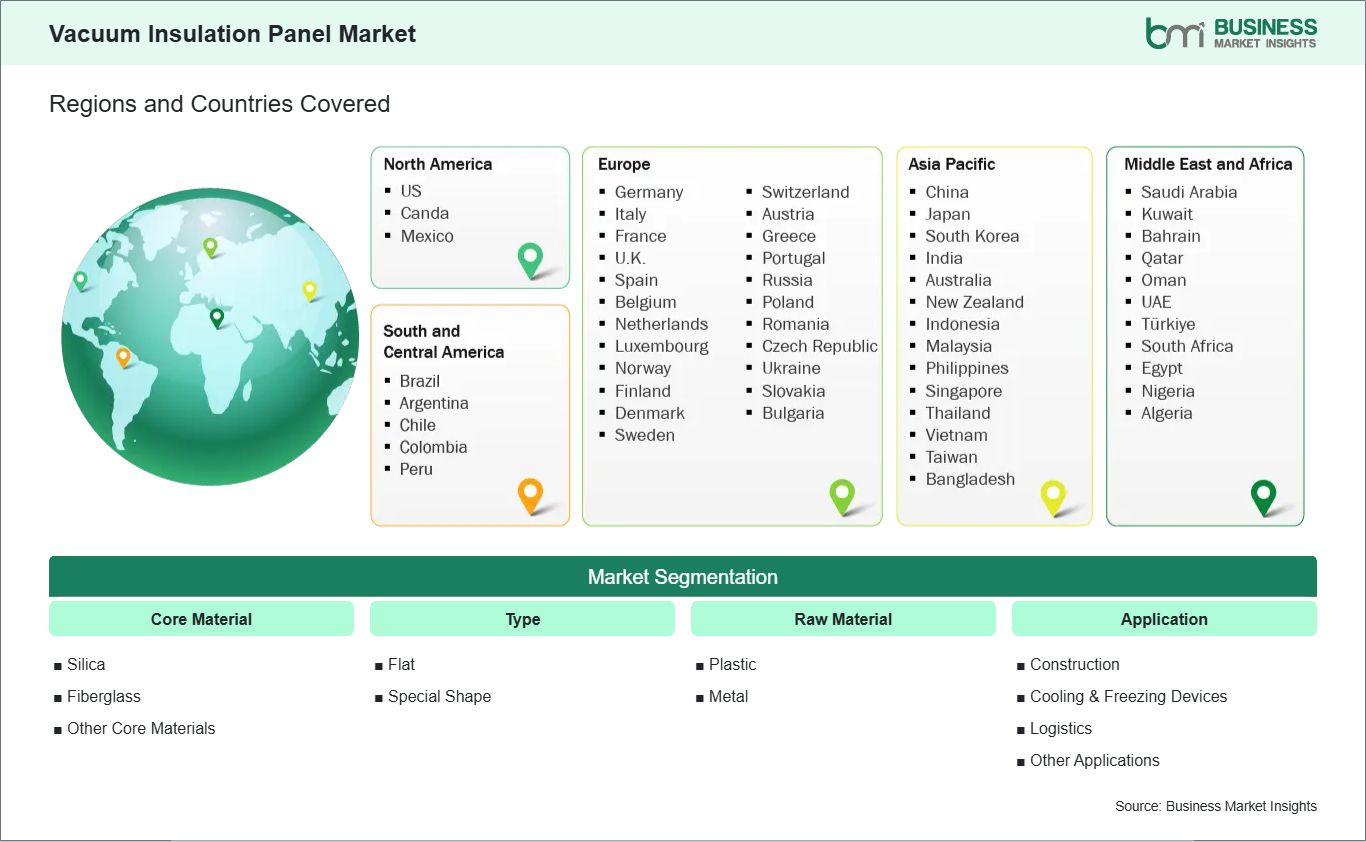

Key segments that contributed to the derivation of the vacuum insulation panel market analysis are core material, type, raw material, and application.

By core material, the vacuum insulation panel market is segmented into silica, fiberglass, other core materials. The silica segment dominated the market in 2025.

Based on type, the vacuum insulation panel market is categorized into flat, special shape. The flat segment dominated the market in 2025.

On the basis of raw material, the vacuum insulation panel market is segmented into plastic, metal. The metal segment dominated the market in 2025.

In terms of application, the vacuum insulation panel market is categorized into construction, cooling & freezing devices, logistics, other applications. The construction segment dominated the market in 2025.

Vacuum Insulation Panel Market Drivers and Opportunities:

Rising Demand for Energy-Efficient Buildings and Green Construction

The global push for energy-efficient buildings is a key driver for the vacuum insulation panel market. Architects, builders, and developers are increasingly specifying materials that reduce energy consumption while meeting sustainability certifications such as LEED and BREEAM. VIPs provide superior thermal insulation compared to conventional materials, enabling ultra-thin wall and floor systems without compromising interior space. This is particularly critical in urban areas where real estate costs are high, and every square meter of usable space is valuable. High-end residential, commercial, and institutional construction projects are leveraging VIPs to meet strict thermal performance standards, reduce operational costs, and achieve long-term energy savings.

Cold chain and refrigerated storage applications further highlight VIPs’ relevance in energy-efficient construction. Warehouses, pharmaceutical storage facilities, and refrigerated transport units require insulation that minimizes thermal losses while optimizing space. By maintaining consistent temperatures with minimal energy input, VIPs support energy conservation goals and reduce greenhouse gas emissions across these sectors. North America and Europe are leading in adoption, with building codes increasingly mandating high-performance insulation, while Asia Pacific is witnessing rapid growth due to urbanization and sustainability-focused construction projects.

Despite high adoption, market expansion faces challenges such as elevated production costs and limited awareness among mid-tier construction players. Incorporating VIPs into conventional building materials also requires skilled installation and careful integration into design plans. However, as manufacturers develop more cost-effective solutions and educational efforts increase, VIPs are expected to become mainstream in global energy-efficient construction, particularly in regions prioritizing sustainability and space optimization, solidifying their role as a high-performance insulation solution worldwide.

Innovation in Core Materials for Enhanced Thermal Performance

The global vacuum insulation panel market experiences growth because core materials undergo ongoing innovative development. VIPs that use traditional fumed silica or fiberglass cores achieve excellent insulation performance yet face risks of becoming brittle and sustaining mechanical failures. Researchers develop new materials which include aerogels, polymer foams and composite cores to enhance thermal performance while improving mechanical strength and durability. The new VIP innovations enable products to keep their low thermal conductivity properties throughout extended periods of time and across various environmental conditions, which enables their use in industrial, commercial and residential applications.

Advanced core materials improve panel performance by enabling the creation of thinner and lighter panels, which builders need to retrofit existing buildings, construct high-rise buildings and design vehicles that need refrigeration. The construction industry in Europe and North America has used these advanced panels for high-end projects and specialized industrial applications, while businesses in the Asia Pacific now use them for cold storage and logistics and infrastructure development. VIPs use upgraded core materials to function effectively in extreme climate conditions that exist in Middle East high-temperature locations and northern North America frigid zones that conventional insulation systems cannot handle.

Sustainability and recyclability represent additional innovation goals that enhance product performance. Researchers are exploring bio-based and recyclable cores to reduce environmental impact while maintaining insulation efficiency. The enhanced durability of VIPs reduces maintenance expenses and extends their operational lifespan, which leads to better economic outcomes for major projects. The development of material technology, along with declining production costs, will enable VIPs that use their advanced cores to enter fresh market segments and new applications, which will establish their status as a top insulation solution for environmentally friendly building projects that require efficient use of space.

Vacuum Insulation Panel Market Size and Share Analysis:

The vacuum insulation panel market demonstrates steady growth, with size and share analysis highlighting evolving trends and competitive dynamics among key players. The report examines subsegments categorized within core material, type, raw material, and application, offering insights into their contribution to overall market performance.

By core material, the silica subsegment dominated the market in 2025, driven by its superior thermal insulation performance and long service life in vacuum insulation panels.

Based on type, the flat subsegment dominated the market in 2025, driven by its ease of manufacturing, installation, and integration into a wide range of applications.

By raw material, the metal subsegment dominated the market in 2025, driven by its excellent barrier properties, durability, and ability to enhance thermal performance.

In terms of application, the construction subsegment dominated the market in 2025, driven by the growing demand for energy-efficient insulation in buildings and infrastructure projects.

Australia, China, India, Japan, South Korea, Indonesia, Malaysia, Philippines, Singapore, Thailand, Vietnam, Bangladesh, New Zealand, Taiwan

South and Central America

Brazil, Argentina, Peru, Chile, Colombia

Middle East and Africa

Bahrain, Kuwait, Oman, Qatar, Saudi Arabia, United Arab Emirates, Turkiye, South Africa, Egypt, Algeria, Nigeria

Market leaders and key company profiles

EvonikIndustriesAG

LGHausysLtd

PanasonicCorporation

DOW

OCILtd

KevothermalLLC

PorexthermDammstoffeGmbH

ThermoCor

VaQTecAG

MicrothermSentronicGmbH

Get more information on this report

Vacuum Insulation Panel Market Report Coverage and Deliverables:

The "Vacuum Insulation Panel Market Size and Forecast (2022 - 2033)" report provides a detailed analysis of the market covering below areas:

Vacuum Insulation Panel Market size and forecast at global, regional, and country levels for all the key market segments covered under the scope

Vacuum Insulation Panel Market trends, as well as drivers, restraints, and opportunities

Vacuum Insulation Panel Market analysis covering key trends, global and regional framework, major players, regulations, and recent developments

Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments for the Vacuum Insulation Panel Market

Detailed company profiles, including SWOT analysis

The geographical scope of the Vacuum Insulation Panel Market report is divided into North America, Asia Pacific, Europe, Middle East & Africa, and South & Central America. North America held the largest share in 2025.

The global vacuum insulation panel market sees North America emerge as its leading region because the area possesses established construction networks, together with its developed cold chain systems and strict energy efficiency standards that businesses must follow.

The United States and Canada lead VIP adoption in high-performance building insulation, ultra-thin wall systems, energy-efficient appliances, and refrigerated storage solutions. The combination of strict building codes and energy-saving incentives, together with the rising need for space-saving insulation systems, creates business advantages for manufacturers who operate in both residential and commercial construction areas.

The European market shows substantial VIP usage, which reaches its highest levels in Germany, France and the UK, because construction companies concentrate on building energy-efficient structures while implementing retrofitting methods and using sustainable design techniques. European adoption is further supported by energy efficiency directives and the need for compact refrigeration in food processing and logistics sectors.

The Asia Pacific region develops into a fast-growing market, which China, Japan, India and South Korea lead because their industrialization, urbanization and growing cold chain logistics systems create a need for high-performance thermal insulation. The refrigerated transport system and commercial freezers, together with compact building applications, use VIPs while local manufacturers establish domestic facilities through advanced panel technology development to satisfy increasing consumer requirements.

The Middle East and Africa region displays low adoption rates but shows potential for growth because of three factors: infrastructure development, increasing industrial refrigeration demands, and ongoing construction projects in the United Arab Emirates, Saudi Arabia, and South Africa. VIP integration in South and Central America occurs mainly through Brazil and Mexico, which dominate the cold storage and refrigerated transport and premium construction sectors, while urban development and industrial facility modernization drive their growth.

The worldwide adoption of VIP technology advances through three factors: organizations develop new technologies, they work towards sustainability goals, and they meet energy efficiency standards, while North America establishes product performance requirements that determine how well products endure use and function across different industries.

Get more information on this report

Vacuum Insulation Panel Market Research Report Guidance:

The report includes qualitative and quantitative data in the Vacuum Insulation Panel Market across core material, type, raw material, application and geography.

The report starts with the key takeaways (chapter 2), highlighting key trends and outlook of the Vacuum Insulation Panel Market.

Chapter 3 focuses on the research methodology of the study.

Chapter 4 includes ecosystem analysis.

Chapter 5 highlights the major industry dynamics in the Vacuum Insulation Panel Market, including factors that are driving the market, prevailing deterrents, potential opportunities, as well as future trends. Impact analysis of these drivers and restraints is also covered in this section.

Chapter 6 discusses the Vacuum Insulation Panel Market scenario, in terms of historical market revenues, and forecast till the year 2033.

Chapters 7 to 11 cover Vacuum Insulation Panel Market segments by core material, type, raw material, application and geography across North America, Asia Pacific, Europe, Middle East & Africa, and South & Central America. They cover the market revenue forecast and factors driving the market.

Chapter 12 describes the competitive analysis along with the heat map analysis for the key players operating in the market.

Chapter 13 describes the industry landscape analysis. It provides detailed descriptions of business activities such as market initiatives, new developments, mergers, and joint ventures globally, along with a competitive landscape.

Chapter 14 provides detailed profiles of the major companies operating in the Vacuum Insulation Panel Market. Companies have been profiled on the basis of their key facts, business descriptions, products, financial overview, SWOT analysis, and key developments.

Chapter 15, i.e., the appendix, is inclusive of a brief overview of the company, a list of abbreviations, and a disclaimer.

Vacuum Insulation Panel Market News and Key Development:

The Vacuum Insulation Panel Market is evaluated by gathering qualitative and quantitative data post primary and secondary research, which includes important corporate publications, association data, and databases. A few of the key developments in the vacuum insulation panel market are:

In September 2024, va‑Q‑tec Thermal Solutions GmbH announced that it had strategically realigned its business to focus on five key growth areas including food logistics, pharmacy deliveries, appliances, construction, and mobility, with VIP production continuing at its Würzburg and Kölleda facilities and an exclusive agreement with Envirotainer for production and supply of highly insulating thermal boxes for the pharmaceutical industry.

In May 2025, Panasonic Corporation of North America announced that it would showcase its ADVANC‑R® Vacuum Insulation Panel at the AIA Conference on Architecture & Design 2025, highlighting a next‑generation VIP engineered for commercial buildings and low‑slope roofing systems that offers industry‑leading thermal performance in a thin profile.

Key Sources Referred:

World Health Organization (WHO)Organisation for Economic Cooperation and Development (OECD)The World Bank GroupWorldometerThe LancetInternational Bar AssociationInternational Trade Administration

The List of Companies - Vacuum Insulation Panel Market

EvonikIndustriesAG

LGHausysLtd

PanasonicCorporation

DOW

OCILtd

KevothermalLLC

PorexthermDammstoffeGmbH

ThermoCor

VaQTecAG

MicrothermSentronicGmbH

Frequently Asked Questions

How big is the Vacuum Insulation Panel Market?

The Vacuum Insulation Panel Market is valued at US$ 9.89 Billion in 2025, it is projected to reach US$ 14.60 Billion by 2033.

What is the CAGR for Vacuum Insulation Panel Market by (2026 - 2033)?

As per our report Vacuum Insulation Panel Market, the market size is valued at US$ 9.89 Billion in 2025, projecting it to reach US$ 14.60 Billion by 2033. This translates to a CAGR of approximately 4.99% during the forecast period.

What segments are covered in this report?

The Vacuum Insulation Panel Market report typically cover these key segments-

Core Material (Silica, Fiberglass, Other Core Materials)

Type (Flat, Special Shape)

Raw Material (Plastic, Metal)

Application (Construction, Cooling & Freezing Devices, Logistics, Other Applications)

What is the historic period, base year, and forecast period taken for Vacuum Insulation Panel Market?

The historic period, base year, and forecast period can vary slightly depending on the specific market research report. However, for the Vacuum Insulation Panel Market report:

Historic Period : 2022-2024

Base Year : 2025

Forecast Period : 2026-2033

Who are the major players in Vacuum Insulation Panel Market?

The Vacuum Insulation Panel Market is populated by several key players, each contributing to its growth and innovation. Some of the major players include:

EvonikIndustriesAG

LGHausysLtd

PanasonicCorporation

DOW

OCILtd

KevothermalLLC

PorexthermDammstoffeGmbH

ThermoCor

VaQTecAG

MicrothermSentronicGmbH

Who should buy this report?

The Vacuum Insulation Panel Market report is valuable for diverse stakeholders, including:

Investors: Provides insights for investment decisions pertaining to market growth, companies, or industry insights. Helps assess market attractiveness and potential returns.

Industry Players: Offers competitive intelligence, market sizing, and trend analysis to inform strategic planning, product development, and sales strategies.

Suppliers and Manufacturers: Helps understand market demand for components, materials, and services related to concerned industry.

Researchers and Consultants: Provides data and analysis for academic research, consulting projects, and market studies.

Financial Institutions: Helps assess risks and opportunities associated with financing or investing in the concerned market.

Essentially, anyone involved in or considering involvement in the Vacuum Insulation Panel Market value chain can benefit from the information contained in a comprehensive market report.

Get Free Sample For Vacuum Insulation Panel Market

Get Free Sample For Vacuum Insulation Panel Market