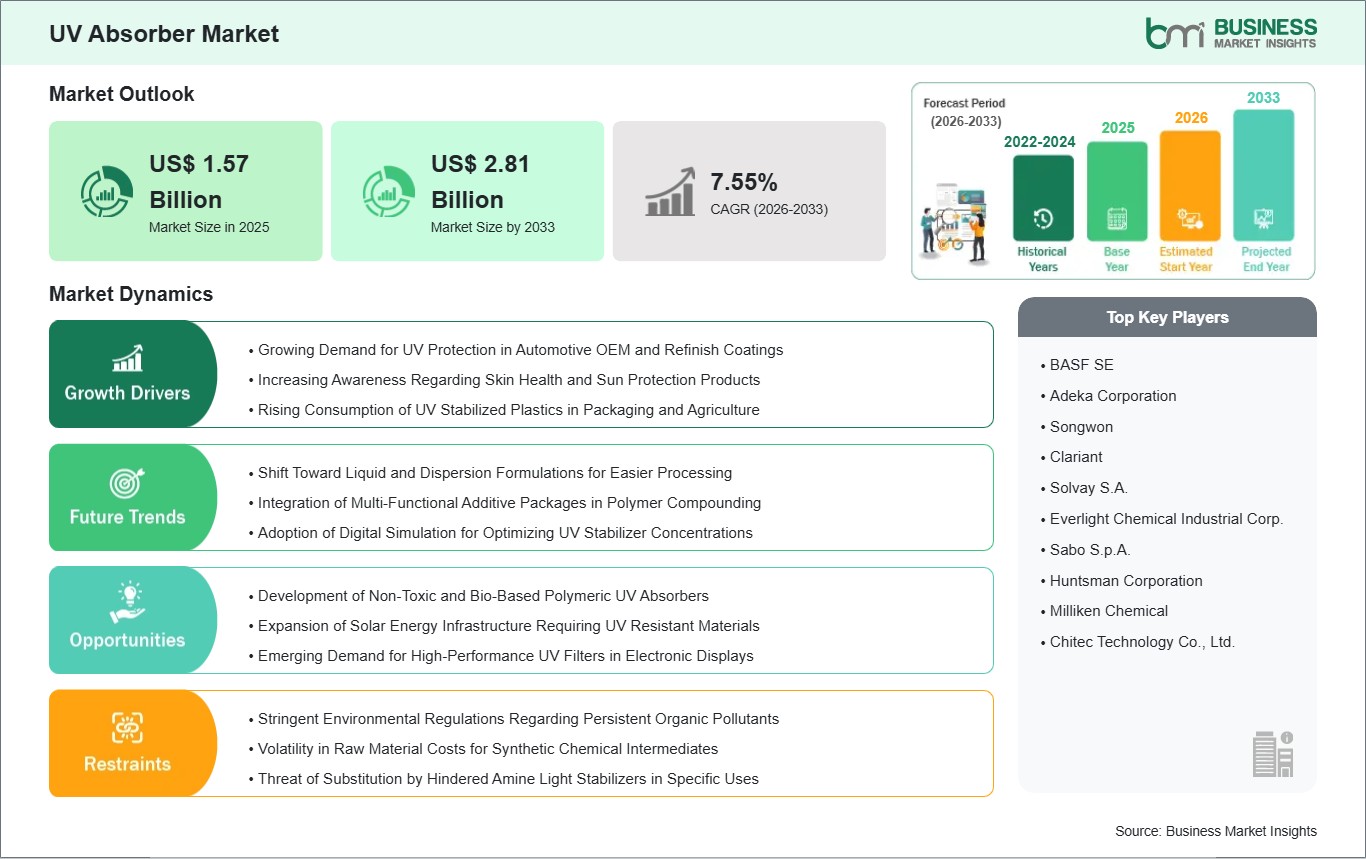

The UV Absorber Market size is expected to reach US$ 2.81 billion by 2033 from US$ 1.57 billion in 2025. The market is estimated to record a CAGR of 7.55% from 2026 to 2033.

Executive Summary and Global Market Analysis:

The global market for UV absorbers is a significant segment of the specialty chemicals industry, offering crucial protection for exposed materials against the damaging effects of sunlight. These chemicals act by absorbing damaging ultraviolet rays and dissipating them as harmless heat, thus protecting materials from degradation. Currently, the market is driven by the strong growth rate of the automotive, construction, and personal care industries, where product durability and appearance are major performance drivers. Benzotriazoles continue to be the dominant chemistry type owing to their excellent protective properties, and coatings is currently the biggest market segment, driven by the requirement for long-lasting exterior coatings.

Technological advancements are steering the market toward more specialized and sustainable solutions. The integration of high-performance triazines is increasing in the engineering plastics and premium coatings sectors due to their exceptional thermal stability. Simultaneously, the industry is responding to environmental concerns by developing low-migration and bio-based absorbers. While challenges such as raw material price volatility and strict regulatory oversight persist, the market's outlook remains positive. The expansion of renewable energy infrastructure and the increasing adoption of UV-stabilized plastics in emerging economies provide significant avenues for future growth. Strategic focus on innovation and environmental compliance will be the primary differentiators for market leaders in the coming years.

UV Absorber Market - Strategic Insights:

Get more information on this report

UV Absorber Market Segmentation Analysis:

Key segments that contributed to the derivation of the UV Absorber market analysis are type and application.

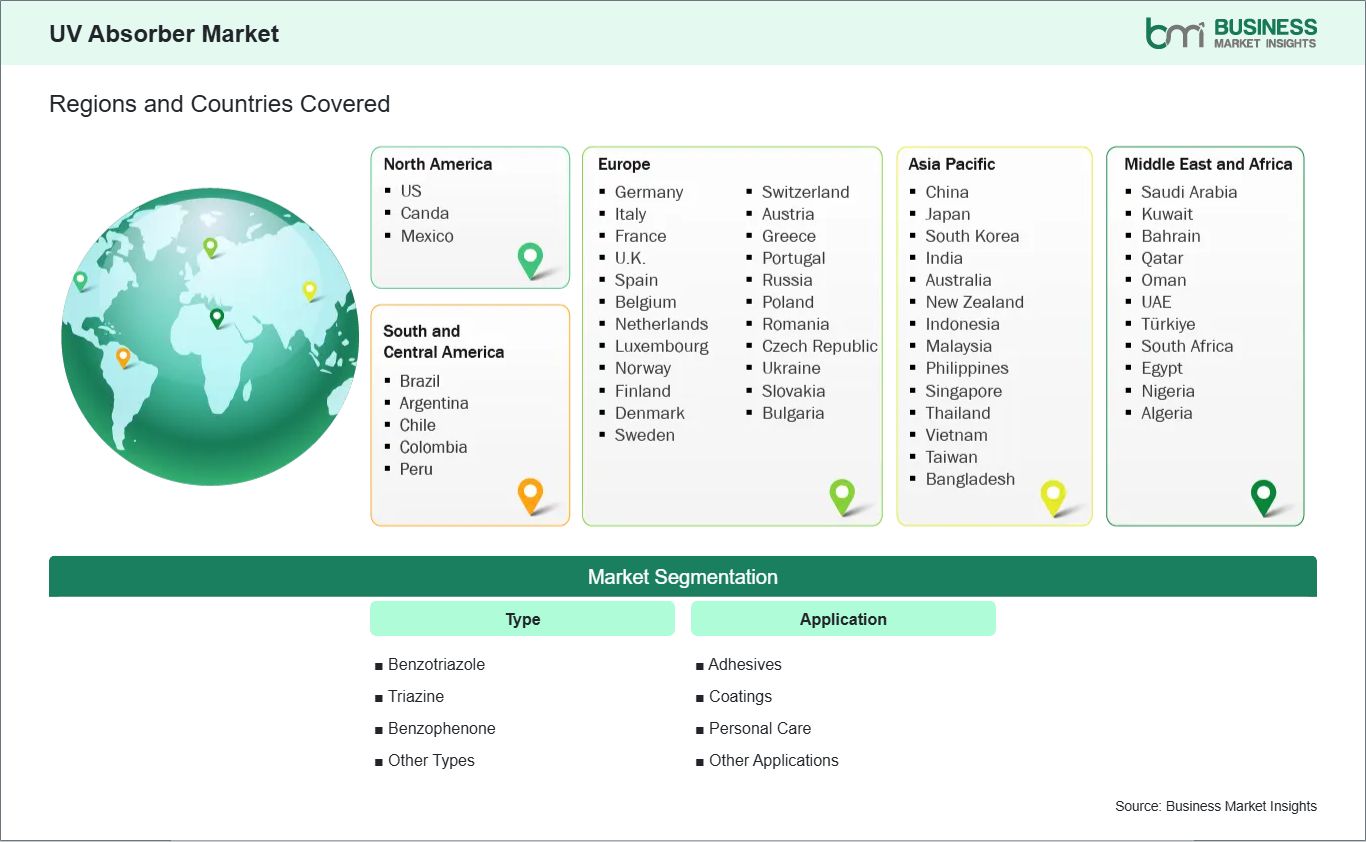

By type, the UV Absorber market is segmented into Benzotriazole, Triazine, Benzophenone, and Other The Benzotriazole segment dominated the market in 2025.

By application, the UV Absorber market is segmented into Adhesives, Coatings, Personal Care, and Other The Coatings segment dominated the market in 2025.

UV Absorber Market Drivers and Opportunities:

Growing Demand for UV Protection in Automotive OEM and Refinish Coatings

The automotive industry relies heavily on ultraviolet absorbers to maintain the aesthetic appeal and structural integrity of vehicle exteriors. Modern automotive coatings are complex multi-layered systems where the topmost clear coat must act as a primary shield against solar radiation. UV absorbers are integrated into these formulations to capture harmful radiation and dissipate it as harmless heat before it can reach the underlying pigment layers. This process is vital for preventing common degradation issues such as delamination, chalking, and the yellowing of white finishes. As vehicle manufacturers extend warranty periods for paint durability, the loading levels and quality of these stabilizers have become a focal point of material engineering.

Furthermore, the rise of electric vehicles and the use of lightweight composite body panels have introduced new challenges for thermal and UV management. Plastics and composites are inherently more sensitive to photodegradation than traditional steel, necessitating more robust stabilization strategies. In the refinish sector, the demand for high-quality repair paints that match the UV resistance of factory finishes ensures a steady consumption of these additives. The global expansion of the automotive fleet, particularly in regions with high solar intensity, sustains a continuous requirement for advanced benzotriazole and triazine chemistries that can withstand the rigors of various climates while meeting evolving environmental standards.

Development of Non-Toxic and Bio-Based Polymeric UV Absorbers

Environmental sustainability and human safety are increasingly dictating the innovation trajectory of the chemical additives market. Traditional UV absorbers, while effective, have faced scrutiny due to concerns over their potential for bioaccumulation and aquatic toxicity. This regulatory pressure has opened a significant opportunity for the development of polymeric UV absorbers and bio-derived alternatives. These next-generation materials are designed with higher molecular weights to prevent migration and leaching from the host matrix, thereby reducing the risk of environmental contamination and human exposure. By anchoring the UV-absorbing functional groups to a polymer chain, manufacturers can achieve long-lasting protection that remains effective throughout the entire lifecycle of the product.

In addition to safety benefits, bio-based UV absorbers utilize renewable feedstocks such as lignin or plant-derived phenolic compounds. This shift aligns with the broader goal of reducing the carbon footprint of the chemical industry and appeals to brands in the personal care and packaging sectors looking to market green products. The technical challenge lies in matching the high absorption efficiency and thermal stability of conventional synthetic absorbers. However, ongoing research into nanotechnology and molecular design is narrowing this performance gap. Companies that successfully commercialize high-performance, eco-friendly stabilizers are positioned to capture a premium market segment as global regulations move toward more restrictive chemical management frameworks.

UV Absorber Market Size and Share Analysis:

The global UV Absorber market is experiencing steady growth, with market size and share analysis reflecting evolving treatment preferences and competitive dynamics among key players. The report evaluates important subsegments categorized within type and application highlighting their respective contributions to overall market performance.

By type, the Benzotriazole subsegment dominated the market in 2025 due to its superior ability to absorb ultraviolet light across a wide spectrum. This chemistry provides exceptional protection for polymers and clear coatings, offering high thermal stability and compatibility with various resin systems used in demanding outdoor environments.

By application, the Coatings subsegment dominated the market in 2025 because of the critical need for surface protection in the automotive and construction sectors. UV absorbers are essential in clear coats and industrial paints to prevent gloss loss, cracking, and color fading caused by prolonged exposure to intense sunlight.

Australia, China, India, Japan, South Korea, Indonesia, Malaysia, Philippines, Singapore, Thailand, Vietnam, Bangladesh, New Zealand, Taiwan

South and Central America

Brazil, Argentina, Peru, Chile, Colombia

Middle East and Africa

Bahrain, Kuwait, Oman, Qatar, Saudi Arabia, United Arab Emirates, Turkiye, South Africa, Egypt, Algeria, Nigeria

Market leaders and key company profiles

BASF SE

Adeka Corporation

Songwon

Clariant

Solvay S.A.

Everlight Chemical Industrial Corp.

Sabo S.p.A.

Huntsman Corporation

Milliken Chemical

Chitec Technology Co., Ltd.

Get more information on this report

UV Absorber Market Report Coverage and Deliverables:

The "UV Absorber Market Size and Forecast (2022 - 2033)" report provides a detailed analysis of the market covering below areas:

UV Absorber market size and forecast at the regional and country levels for segments covered under the scope

UV Absorber market trends, as well as drivers, restraints, and opportunities

UV Absorber market analysis covering key trends, regional framework, major players, regulations, and recent developments

Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments for the UV Absorber market

Detailed company profiles, including SWOT analysis

UV Absorber Market Geographic Insights:

The geographical scope of the UV Absorber market report is divided into: North America, Asia Pacific, Europe, Middle East & Africa, and South & Central America. North America held the largest share in 2025.

North America stands as the leading region in the UV absorber market, characterized by its sophisticated manufacturing base and early adoption of advanced material technologies. The region's dominance is underpinned by a massive automotive industry and a robust construction sector that prioritizes the use of high-durability materials. Major global chemical producers headquartered in North America drive continuous innovation, focusing on high-purity and multi-functional additives that meet stringent local safety and performance standards. Additionally, the high consumer awareness regarding skin health and the detrimental effects of UV radiation has made the United States and Canada significant markets for UV absorbers in the personal care and cosmetics industries.

The region's lead is further supported by a strong regulatory environment that encourages the transition toward safer and more efficient chemical additives. Compliance with environmental standards has pushed North American manufacturers to be at the forefront of developing low-VOC and non-migratory UV stabilization systems. Furthermore, the rapid growth of the domestic solar energy sector and the increasing use of high-performance plastics in aerospace and electronics contribute to a steady demand for specialty UV absorbers. With a well-established supply chain and a focus on high-value applications, North America continues to set the global benchmark for technical standards and market trends in ultraviolet protection.

Get more information on this report

UV Absorber Market Research Report Guidance:

The report includes qualitative and quantitative data in the UV Absorber market across type, application, and geography.

The report starts with the key takeaways (chapter 2), highlighting the key trends and outlook of the UV Absorber market.

Chapter 3 focuses on the research methodology of the study.

Chapter 4 includes ecosystem analysis.

Chapter 5 highlights the major industry dynamics in the UV Absorber market, including factors that are driving the market, prevailing deterrents, potential opportunities, as well as future trends. Impact analysis of these drivers and restraints is also covered in this section.

Chapter 6 discusses the UV Absorber market scenario, in terms of historical market revenues, and forecast till the year 2033.

Chapters 7 to 9 cover the UV Absorber market segments by type, application, and geography across North America, Europe, Asia Pacific, the Middle East and Africa, and South and Central America. They cover the market revenue, forecast, and factors driving the market.

Chapter 10 describes the competitive analysis along with the heat map analysis for the key players operating in the market.

Chapter 11 describes the industry landscape analysis. It provides detailed descriptions of business activities such as market initiatives, new developments, mergers, and joint ventures globally, along with a competitive landscape.

Chapter 12 provides detailed profiles of the major companies operating in the UV Absorber market. Companies have been profiled on the basis of their key facts, business descriptions, applications, financial overview, SWOT analysis, and key developments.

Chapter 13, i.e., the appendix, is inclusive of a brief overview of the company, list of abbreviations, and disclaimer.

UV Absorber Market News and Key Development:

The UV Absorber market is evaluated by gathering qualitative and quantitative data post primary and secondary research, which includes important corporate publications, association data, and databases. A few of the key developments in the UV Absorber market are:

In January 2024, BASF, announced the expansion of its UV stabilizer production capacity at its Ludwigshafen, Germany site to meet increasing demand from automotive, coatings, and plastics industries.

In October 2025, BASF, announced the launch of Uvinul® TS Hydro, a new water-soluble UVA absorber designed to improve UV protection performance and formulation flexibility in sun care and coating applications.

In 2024, SONGWON Industrial Co., Ltd., announced the introduction and showcase of advanced SONGSORB® UV absorber technologies and expanded additive portfolio at NPE 2024, targeting improved durability and performance in plastics and coatings.

Key Sources Referred:

American Chemistry Council (ACC)International Council of Chemical Associations (ICCA)European Chemical Industry Council (Cefic)China Petroleum and Chemical Industry Federation (CPCIF)Indian Chemical Council (ICC)Japan Chemical Industry Association (JCIA)Brazilian Chemical Industry Association (ABIQUIM)Company WebsitesCompany Annual ReportsCompany Investor Presentations

The List of Companies - UV Absorber Market

BASF SE

Adeka Corporation

Songwon

Clariant

Solvay S.A.

Everlight Chemical Industrial Corp.

Sabo S.p.A.

Huntsman Corporation

Milliken Chemical

Chitec Technology Co., Ltd.

Frequently Asked Questions

How big is the UV Absorber Market?

The UV Absorber Market is valued at US$ 1.57 Billion in 2025, it is projected to reach US$ 2.81 Billion by 2033.

What is the CAGR for UV Absorber Market by (2026 - 2033)?

As per our report UV Absorber Market, the market size is valued at US$ 1.57 Billion in 2025, projecting it to reach US$ 2.81 Billion by 2033. This translates to a CAGR of approximately 7.55% during the forecast period.

What segments are covered in this report?

The UV Absorber Market report typically cover these key segments-

Type (Benzotriazole, Triazine, Benzophenone, Other Types)

Application (Adhesives, Coatings, Personal Care, Other Applications)

What is the historic period, base year, and forecast period taken for UV Absorber Market?

The historic period, base year, and forecast period can vary slightly depending on the specific market research report. However, for the UV Absorber Market report:

Historic Period : 2022-2024

Base Year : 2025

Forecast Period : 2026-2033

Who are the major players in UV Absorber Market?

The UV Absorber Market is populated by several key players, each contributing to its growth and innovation. Some of the major players include:

BASF SE

Adeka Corporation

Songwon

Clariant

Solvay S.A.

Everlight Chemical Industrial Corp.

Sabo S.p.A.

Huntsman Corporation

Milliken Chemical

Chitec Technology Co., Ltd.

Who should buy this report?

The UV Absorber Market report is valuable for diverse stakeholders, including:

Investors: Provides insights for investment decisions pertaining to market growth, companies, or industry insights. Helps assess market attractiveness and potential returns.

Industry Players: Offers competitive intelligence, market sizing, and trend analysis to inform strategic planning, product development, and sales strategies.

Suppliers and Manufacturers: Helps understand market demand for components, materials, and services related to concerned industry.

Researchers and Consultants: Provides data and analysis for academic research, consulting projects, and market studies.

Financial Institutions: Helps assess risks and opportunities associated with financing or investing in the concerned market.

Essentially, anyone involved in or considering involvement in the UV Absorber Market value chain can benefit from the information contained in a comprehensive market report.

Get Free Sample For UV Absorber Market

Get Free Sample For UV Absorber Market