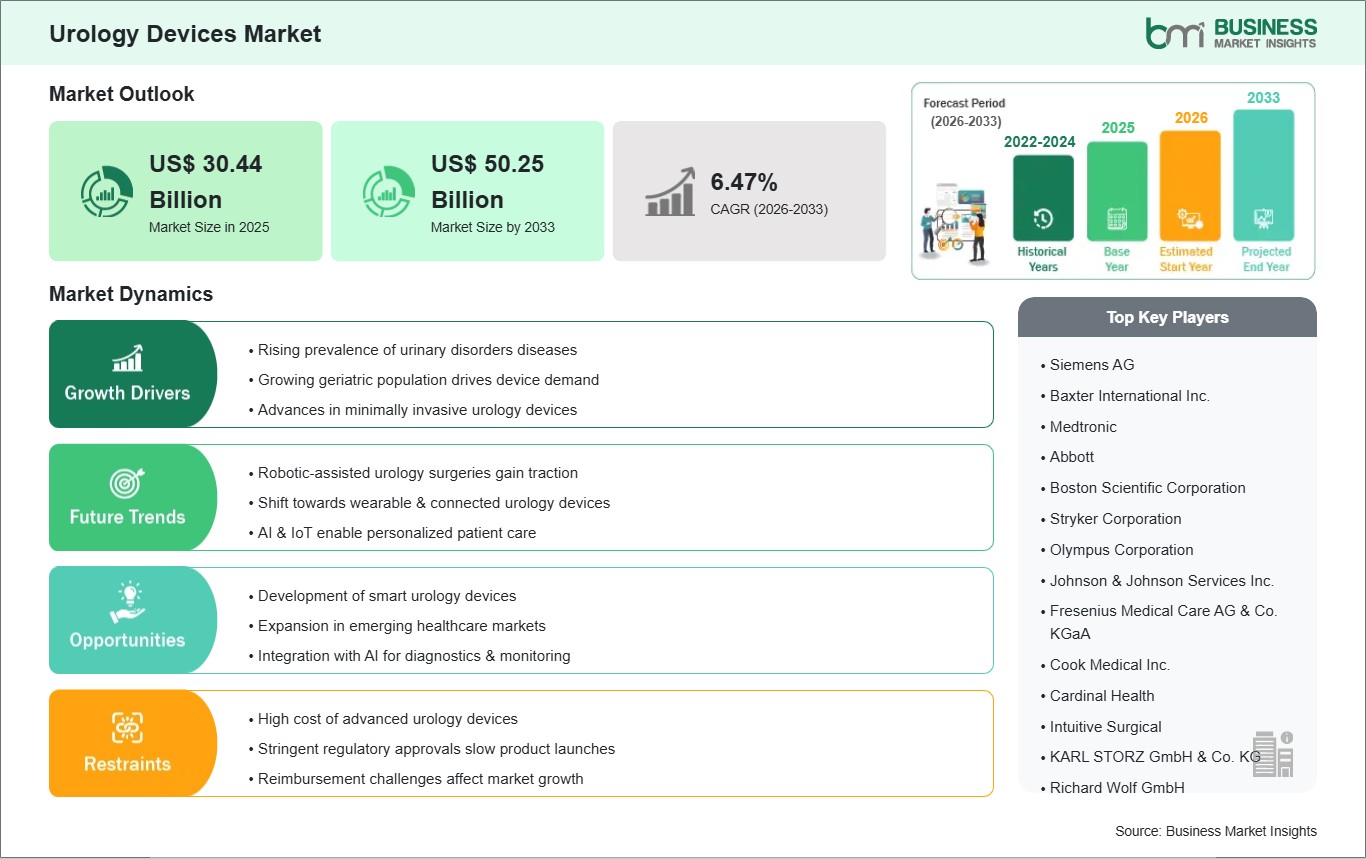

The Urology Devices Market size is expected to reach US$ 85.55 Billion by 2033 from US$ 51.25 Billion in 2025. The market is estimated to record a CAGR of 6.61% from 2026 to 2033.

Executive Summary and Global Market Analysis:

The urology devices market is a vast one that includes all the necessary equipment for diagnosing, treating, and managing disorders of the urinary tract as well as the male reproductive system. These disorders include kidney stones, BPH, urinary incontinence, infections, and urological cancers. Such devices consist of, and are not limited to, endoscopes for visualization inside the body, catheters for urine drainage, stents to maintain patency, lithotripsy devices for stone fragmenting, lasers for tissue removal, urodynamic setups for function measurement, and surgical instruments. Hospitals and clinics are increasingly turning to minimally invasive and robotic-assisted technologies. The market continues to grow, driven by the aging population, the increase in the prevalence of urological problems, and a better understanding of the significance of early diagnosis. Besides, new technologies are also making the treatments more comfortable and effective. The latest advancements in the field cover the introduction of single-use devices that lower the risk of infection by their nature, the application of high-skilled imaging equipment that provides the clearest and real-time visuals for diagnosis, the execution of laser treatments that unerringly target and pound stones with almost no harm to adjacent tissue, and the installation of digital systems that grant instant measurement and monitoring of urinary function. These modifications are playing a key role in the improvement of the health of the patients.

Acute-care hospitals are the main sites of the use of the big majority of urology devices. However, the trend is shifting, and the ambulatory-care centers, as well as outpatient clinics, are increasingly utilizing the devices. This is due to the fact that they are financial friendly and help the patients to undergo a quicker recovery. Thus, the market comprises not only large multinational companies but also small manufacturers that have specific focuses. The legal environment, insurance reimbursement, and device costs together decide the speed of new products' adoption in the market. With the continuous improvement of healthcare systems in developing countries, the birth of new business opportunities comes along to fill the gaps in urological.

Urology Devices Market - Strategic Insights:

Get more information on this report

Urology Devices Market Segmentation Analysis:

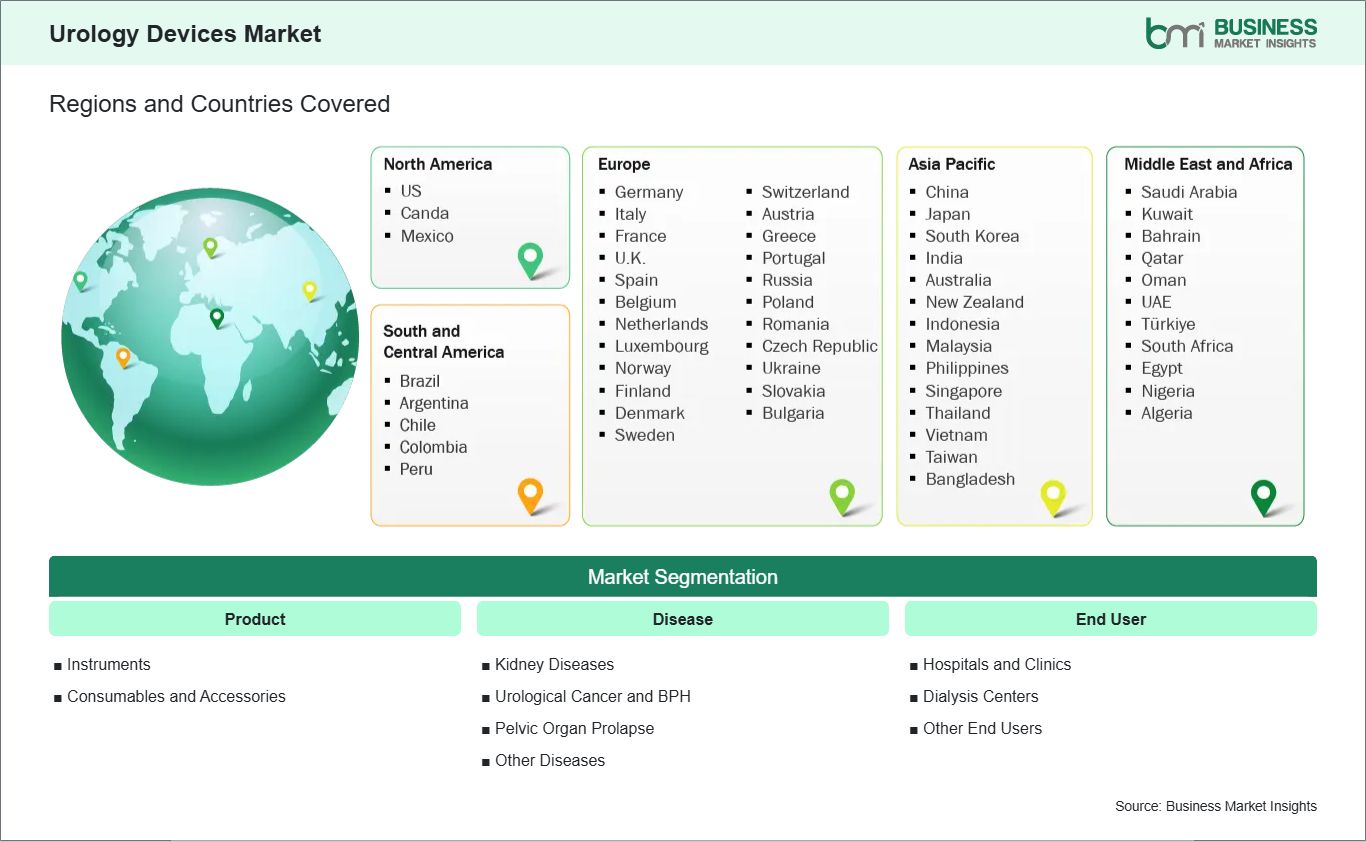

Key segments that contributed to the derivation of the urology devices market analysis are product, technology, disease, and end user.

By product, the urology devices market is bifurcated into instruments, consumables & accessories. The instruments segment dominated the market in 2025. The instruments is further bifurcated into dialysis devices, endoscopes & endovision systems, lasers & lithotripsy devices, robotic surgical systems, urodynamic systems, imaging & navigation devices, bladder management devices, other instruments. The consumables & accessories is further bifurcated into dialysis consumables, guidewires & urinary catheters, stents, biopsy devices, disposable ureteroscopes, continence care products, other consumables & accessories.

By technology, the market is bifurcated into minimally-invasive surgery devices, robotic urologic surgery systems, ai-enabled imaging & navigation, 3-D printed & patient-specific implants, other emerging technologies. The minimally-invasive surgery devices segment held the largest share of the market in 2025.

By disease, the market is bifurcated into kidney diseases, urological cancer & BPH, urinary stones (urolithiasis), pelvic organ prolapse, urinary incontinence, other diseases. The kidney diseases segment held the largest share of the market in 2025.

By end user, the market is segmented into hospitals & clinics, dialysis centres, ambulatory surgical centres, home-care settings, other end-users. The hospitals & clinics segment held the largest share of the market in 2025.

Urology Devices Market Drivers and Opportunities:

High Incidence Of Urologic Conditions

Market of urology devices are significantly impacted by the high prevalence of urological disorders and the continuous and increasing demand for products available in the diagnostic, therapeutic, and surgical categories. An aging population, changes in eating habits, and lifestyle diseases are all factors closely associated with urological diseases and are becoming increasingly common worldwide, particularly in rapidly developing and urbanizing areas. The most significant contributor to the demand for urology devices is kidney stones, as they affect around 40 million men in the United States alone, which is the primary reason for the existence of lithotripsy systems, ureteral stents, stone retrieval devices, and disposable ureteroscopes used in repeated interventions. The same can be said for benign prostatic hyperplasia (BPH), which can, at its worst, affect every other man; thus, the patient population has increased tremendously that is treatable by minimally invasive surgical technologies, laser therapies, and implantable solutions. Apart from that, urinary incontinence is another condition with a significant market share, as nearly 30 million adults are affected, thereby driving the demand for catheters, slings, artificial urinary sphincters, and advanced neuromodulation implants, which are designed to provide long-lasting symptom control. Most of all, a lot of urology diseases being chronic or recurrent in nature imply that their patients, rather than being treated once and for all, have to go through a cycle of monitoring, repeated procedures, or even use the same device for life. This ensures that manufacturers have a steady income and that, during difficult economic times, market performance remains stable, even in the case of restricted healthcare spending. Furthermore, awareness of the disease, earlier diagnosis, and accessibility to urologic care are all factors that contribute to the increase in the number of people being treated, thus leading to an increase in demand for devices.

Overall, the high and ever-growing prevalence of urologic diseases ensures that there will always be a lasting clinical demand for new, effective, and patient-centered urology tools, thus making the occurrence of diseases one of the most persistent and powerful factors affecting the market's long-term development.

Collaboration with Research Institutions

The collaboration with research institutions not only means sharing resources. It also opens a door to a new urology device market. Manufacturers can innovate more, with less risk and stronger clinical credibility. Main players in the academic world include medical centers, universities, and specialized research institutes. They have been actively involved in developing urologic science for years. Their work covers biomaterials, robotics, imaging, and digital health. These areas make them valuable partners for the development of next-generation devices. Life sciences R&D partnerships within a multinational research company can significantly reduce the R&D struggles of smaller manufacturers. Early access to new ideas and technologies is one of the main advantages that device firms can get through these collaborations. Modern laser technologies, smart catheters with integrated sensors, bioresorbable implants, and AI-enabled diagnostic systems are just a few examples of the new technologies. The practice shortens the time required for lab discoveries to become commercial products. Moreover, the partnerships provide access to numerous patient groups and real-world clinical settings, which are essential for conducting robust clinical trials and collecting high-quality evidence during post-market studies that can be utilized in regulatory and reimbursement negotiations. Manufacturers, generally speaking, small and medium-sized ones, have an advantage when they join forces with research organizations. They can also acquire public financial assistance, grants, and shared infrastructure. Clinician-researchers ensure devices are stable, user-friendly, and compatible with the healthcare workflow. They achieve this by continually addressing clinical needs and healthcare standards. In this context, the healthcare training program and the excellence center can be integrated to expedite the process and facilitate skill transfer among urologists.

In an environment of fierce competition and strict regulations, collaborations matter. Co-authored articles, clinical endorsements, and long-term research partnerships all contribute to building brand credibility and differentiation. Partnership with companies in emerging markets leads to new, localized, and affordable products. This widens the company’s global market. For the urology devices business, the best option is to build research partnerships with reputable institutions. This enables continuous innovation, easier navigation of regulations, and market expansion.

Urology Devices Market Size and Share Analysis:

By product, the urology devices market is bifurcated into instruments, consumables & accessories. The instruments segment dominated the market in 2025. The share of urology instruments is the largest because they are used in all diagnostic and surgical procedures, so hospitals and clinics must replace them regularly due to the high volume of procedures.

By technology, the market is bifurcated into minimally-invasive surgery devices, robotic urologic surgery systems, ai-enabled imaging & navigation, 3-D printed & patient-specific implants, other emerging technologies. The minimally-invasive surgery devices segment held the largest share of the market in 2025. These devices are already dominating the market because doctors are opting for less invasive procedures that come with fewer risks, shorter hospital stays, and improved patient recovery in all major urologic conditions.

By disease, the market is segmented into kidney diseases, urological cancer & BPH, urinary stones (urolithiasis), pelvic organ prolapse, urinary incontinence, other diseases. The kidney diseases segment held the largest share of the market in 2025. Kidney diseases comprise the largest segment of applications due to the high incidence of kidney stones and chronic kidney disorders that necessitate repeated diagnostic and interventional procedures.

By end user, the market is segmented into hospitals & clinics, dialysis centres, ambulatory surgical centres, home-care settings, other end-users. The hospitals & clinics segment held the largest share of the market in 2025. The highest share belongs to hospitals and clinics due to their advanced infrastructure, high patient inflow, availability of skilled urologists, and concentration of complex urologic procedures.

Australia, China, India, Japan, South Korea, Indonesia, Malaysia, Philippines, Singapore, Thailand, Vietnam, Bangladesh, New Zealand, Taiwan

South and Central America

Brazil, Argentina, Peru, Chile, Colombia

Middle East and Africa

Bahrain, Kuwait, Oman, Qatar, Saudi Arabia, United Arab Emirates, Turkiye, South Africa, Egypt, Algeria, Nigeria

Market leaders and key company profiles

Baxter International Inc.

Boston Scientific Corporation

Becton, Dickinson and Company

Cook Medical Incorporated

Stryker Corporation

Fresenius Medical Care AG & Co. KGaA

Intuitive Surgical Inc.

KARL STORZ SE & Co. KG

Medtronic plc

Olympus Corporation

Get more information on this report

Urology Devices Market Report Coverage and Deliverables:

The Urology Devices Market Size and Forecast (2025-2033) report provides a detailed analysis of the market covering below areas:

Urology devices market size and forecast at global, regional, and country levels for all the key market segments covered under the scope

Urology devices market trends, as well as market dynamics such as drivers, restraints, and key opportunities

Urology devices market analysis covering key market trends, global and regional framework, major players, regulations, and recent market developments

Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments for the urology devices market

Detailed company profiles, including SWOT analysis

Urology Devices Market Geographic Insights:

The geographical scope of the urology devices market report is divided into five regions: North America, Asia Pacific, Europe, Middle East & Africa, and South & Central America. The Urology Devices market in Asia Pacific is expected to grow significantly during the forecast period.

The Asia-Pacific Urology Devices market is segmented into China, Japan, South Korea, India, Australia, New Zealand, Indonesia, Malaysia, the Philippines, Singapore, Thailand, Vietnam, Taiwan, Bangladesh, and the Rest of Asia. The Asia-Pacific region is expected to be the largest market area for urology devices, with the highest compound annual growth rate (CAGR). The Asia-Pacific urology devices market is growing rapidly, driven by rising healthcare spending and increased awareness of urological disorders. Besides, the main factors that significantly contribute to this market growth are population increase, improvement in healthcare infrastructure, and government initiatives to enhance access and quality of services. The leading markets are China, India, and Japan, where considerable investments are made by both local and foreign companies. For instance, Stryker and Teleflex have already begun their expansion in the area, thus raising competition and stimulating the innovation process. As the adoption of more modern urology devices increases, the market is projected to grow even faster, thereby making the Asia-Pacific region a major hub for future innovation.

Get more information on this report

Urology Devices Market Research Report Guidance:

The report includes qualitative and quantitative data in the Urology Devices market across product, technology, disease, end user, and geography.

The report starts with the key takeaways (chapter 2), highlighting the key trends and outlook of the urology devices market.

Chapter 3 includes the research methodology of the study.

Chapter 4 further includes ecosystem analysis.

Chapter 5 highlights the major industry dynamics in the urology devices market, including factors that are driving the market, prevailing deterrents, potential opportunities, as well as future trends. Impact analysis of these drivers and restraints is also covered in this section.

Chapter 6 discusses the urology devices market scenario, in terms of historical market revenues, and forecast till the year 2031.

Chapters 7 to 11 cover urology devices market segments by type, destination, and end user, and geography across North America, Europe, Asia Pacific, Middle East and Africa, and South and Central America. They cover the market volume revenue forecast and factors driving the market.

Chapter 12 describes the competitive analysis along with the heat map analysis for the key players operating in the market.

Chapter 13 describes the industry landscape analysis. It provides detailed descriptions of business activities such as market initiatives, new developments, mergers, and joint ventures globally, along with a competitive landscape.

Chapter 14 provides detailed profiles of the major companies operating in the urology devices market. Companies have been profiled on the basis of their key facts, business descriptions, products and services, financial overview, SWOT analysis, and key developments.

Chapter 15, i.e., the appendix is inclusive of a brief overview of the company, list of abbreviations, and disclaimer.

Urology Devices Market News and Key Development:

The Urology Devices market is evaluated by gathering qualitative and quantitative data post primary and secondary research, which includes important corporate publications, association data, and databases. A few of the key developments in the Urology Devices market are:

In November 2025, Boston Scientific (US) announced the launch of a new line of advanced urology devices designed to improve surgical outcomes and reduce recovery times. This strategic move underscores the company's commitment to innovation and positions it favorably in relation to its competitors. By focusing on advanced technology, Boston Scientific (US) aims to capture a larger market share and address the growing demand for effective urological solutions.

In October 2025, Medtronic (US) unveiled a partnership with a leading telehealth provider to integrate remote monitoring capabilities into its urology devices. This initiative reflects Medtronic's (US) focus on digital transformation and the increasing importance of telehealth in patient management. By enhancing connectivity and patient engagement, this strategy is likely to improve treatment adherence and outcomes, thereby solidifying Medtronic's (US) position in the market.

In January 2025, Boston Scientific Corporation entered into a definitive agreement to acquire Axonics, Inc. This acquisition would expand Boston Scientific Corporation's urology portfolio with differentiated technologies to treat urinary and bowel dysfunction.

Key Sources Referred:

World Bank – Global Trade IndicatorsEuropean Chemicals AgencyInternational Council of Chemical Associations(International Monetary Fund )IMFWorld Trade Organization (WTO)International Trade Administration (ITA)Company websiteCompany annual reportsCompany investor presentations

The List of Companies - Urology Devices Market

Baxter International Inc.

Boston Scientific Corporation

Becton, Dickinson and Company

Cook Medical Incorporated

Stryker Corporation

Fresenius Medical Care AG & Co. KGaA

Intuitive Surgical Inc.

KARL STORZ SE & Co. KG

Medtronic plc

Olympus Corporation

Frequently Asked Questions

How big is the Urology Devices Market?

The Urology Devices Market is valued at US$ 51.25 Billion in 2025, it is projected to reach US$ 85.55 Billion by 2033.

What is the CAGR for Urology Devices Market by (2026 - 2033)?

As per our report Urology Devices Market, the market size is valued at US$ 51.25 Billion in 2025, projecting it to reach US$ 85.55 Billion by 2033. This translates to a CAGR of approximately 6.61% during the forecast period.

What segments are covered in this report?

The Urology Devices Market report typically cover these key segments-

Product (Instruments, Consumables & Accessories)

Technology (Minimally-Invasive Surgery Devices, Robotic Urologic Surgery Systems, AI-enabled Imaging & Navigation, 3-D Printed & Patient-specific Implants, Other Emerging Technologies)

Disease (Kidney Diseases, Urological Cancer & BPH, Urinary Stones (Urolithiasis), Pelvic Organ Prolapse, Urinary Incontinence, Other Diseases)

What is the historic period, base year, and forecast period taken for Urology Devices Market?

The historic period, base year, and forecast period can vary slightly depending on the specific market research report. However, for the Urology Devices Market report:

Historic Period : 2022-2024

Base Year : 2025

Forecast Period : 2026-2033

Who are the major players in Urology Devices Market?

The Urology Devices Market is populated by several key players, each contributing to its growth and innovation. Some of the major players include:

Baxter International Inc.

Boston Scientific Corporation

Becton, Dickinson and Company

Cook Medical Incorporated

Stryker Corporation

Fresenius Medical Care AG & Co. KGaA

Intuitive Surgical Inc.

KARL STORZ SE & Co. KG

Medtronic plc

Olympus Corporation

Who should buy this report?

The Urology Devices Market report is valuable for diverse stakeholders, including:

Investors: Provides insights for investment decisions pertaining to market growth, companies, or industry insights. Helps assess market attractiveness and potential returns.

Industry Players: Offers competitive intelligence, market sizing, and trend analysis to inform strategic planning, product development, and sales strategies.

Suppliers and Manufacturers: Helps understand market demand for components, materials, and services related to concerned industry.

Researchers and Consultants: Provides data and analysis for academic research, consulting projects, and market studies.

Financial Institutions: Helps assess risks and opportunities associated with financing or investing in the concerned market.

Essentially, anyone involved in or considering involvement in the Urology Devices Market value chain can benefit from the information contained in a comprehensive market report.

Get Free Sample For Urology Devices Market

Get Free Sample For Urology Devices Market