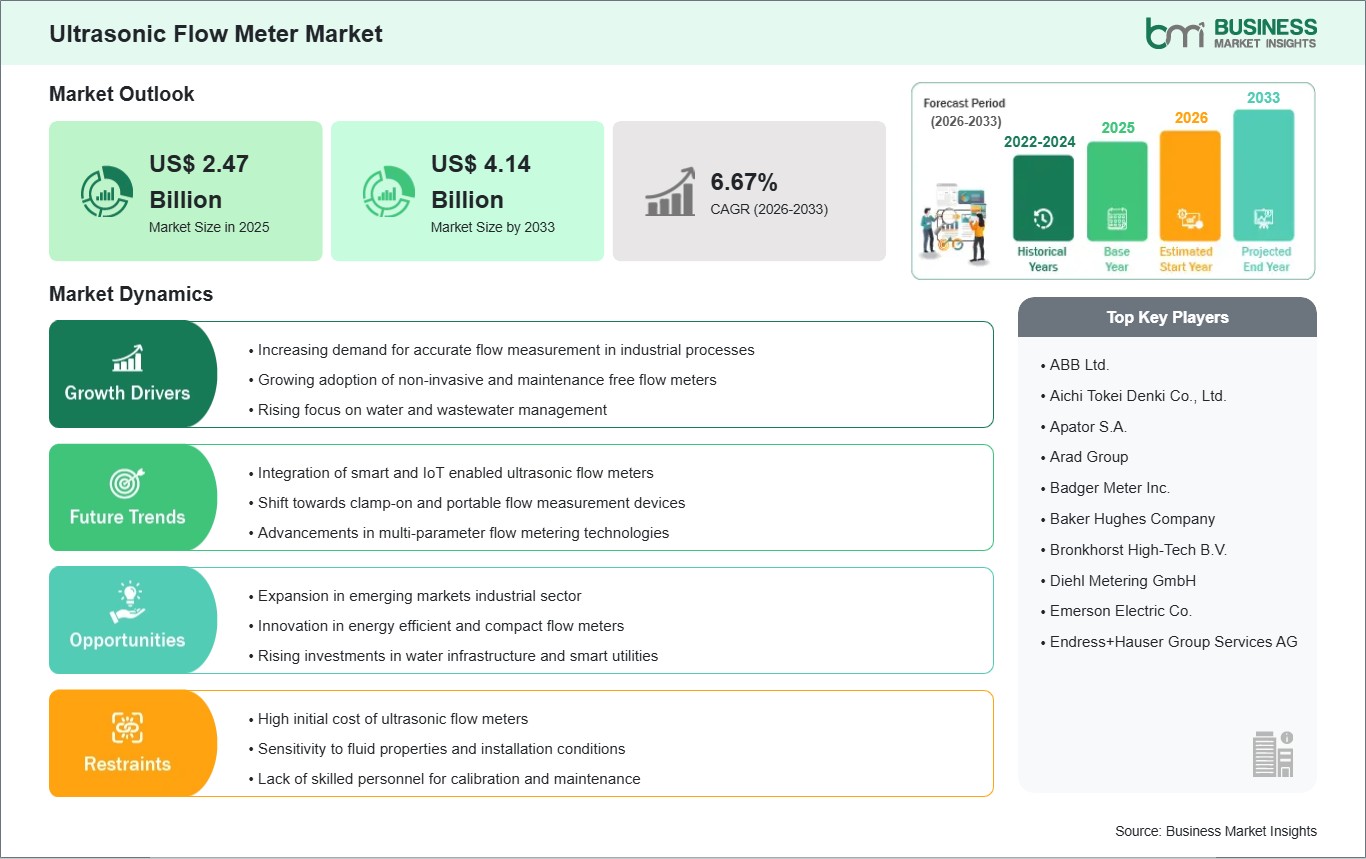

The Ultrasonic Flow Meter Market size is expected to reach US$ 4.14 billion by 2033 from US$ 2.47 billion in 2025. The market is estimated to record a CAGR of 6.67% from 2026 to 2033.

Executive Summary and Global Market Analysis:

Ultrasonic flow meters represent a sophisticated category of inferential measurement devices that utilize high-frequency acoustic waves to determine the volumetric flow rate of liquids and gases. By measuring either the transit-time difference of signals traveling with and against the flow or the frequency shift caused by the Doppler effect, these sensors provide highly accurate, non-intrusive data essential for modern process control and custody transfer. Unlike traditional mechanical meters, ultrasonic variants feature no moving parts, which eliminates pressure drops, reduces long-term maintenance overhead, and ensures high reliability in corrosive or abrasive environments. These components are fundamental in the transition toward digitalized industrial ecosystems, underpinning the precision required in oil and gas pipelines, chemical processing, and smart water management systems.

However, the market faces notable challenges, including the high initial capital expenditure associated with multi-path high-precision systems and the technical complexity of processing signals in heterogeneous fluids with high aeration or suspended solids. Furthermore, the specialized expertise required for the installation and calibration of inline variants can act as a deterrent for smaller industrial operators facing budgetary constraints.

Despite these hurdles, the market holds significant opportunities driven by the global push for Industry 4.0 and the integration of the Industrial Internet of Things (IIoT). The move toward autonomous "smart factories" is creating a demand for intelligent meters equipped with AI-driven self-diagnostics and remote verification capabilities. Additionally, the expansion of hydrogen infrastructure and the demand for energy-efficient "green" manufacturing frameworks are expected to open lucrative new avenues for ultrasonic technology as industries seek auditable, high-fidelity data to meet stringent environmental and regulatory mandates.

Ultrasonic Flow Meter Market - Strategic Insights:

Get more information on this report

Ultrasonic Flow Meter Market Segmentation Analysis:

Key segments that contributed to the derivation of the Ultrasonic Flow Meter market analysis are implementation type, measurement technology, and end-user industry.

By Implementation Type, the market is segmented into Clamp-On, Inline, and Others.

By Measurement Technology, the market is divided into Transit-Time, Doppler, and Hybrid.

By End-User Industry, the market is categorized into Oil and Gas, Power Generation, Water and Wastewater, and Others.

Ultrasonic Flow Meter Market Drivers and Opportunities:

Accelerated Transition to Smart Industrial Automation and Industry 4.0

The global acceleration toward fully automated industrial ecosystems serves as a foundational driver for the ultrasonic flow meter market. As manufacturing facilities and utilities transition into "Smart Factories," there is an escalating requirement for high-fidelity, real-time data to feed into centralized control systems. Unlike traditional mechanical meters that provide static or delayed readings, ultrasonic flow meters offer instantaneous digital output and advanced signal processing capabilities. This transition is particularly evident in the water and wastewater sector, where municipalities are replacing aging infrastructure with intelligent ultrasonic networks to combat non-revenue water losses. These meters facilitate precise leak detection and consumption monitoring without the need for periodic manual intervention.

Furthermore, the non-intrusive nature of clamp-on ultrasonic technology allows industrial operators to modernize their facilities without the costly downtime associated with cutting pipes or halting production lines. This inherent flexibility, combined with the ability to maintain consistent accuracy over long operational lifespans due to the absence of moving parts, makes ultrasonic technology the preferred choice for sectors prioritizing operational continuity. As global industries increasingly rely on data-driven decision-making, the demand for these sophisticated, communication-ready measurement tools continues to intensify.

Emergence of the Hydrogen Economy and Decarbonization Infrastructure

The global shift toward sustainable energy sources, specifically the rapid development of hydrogen production and distribution infrastructure, presents a transformative growth opportunity for the ultrasonic flow meter market. Hydrogen, characterized by its low density and high flow velocities, poses significant measurement challenges for legacy differential-pressure or turbine meters. Ultrasonic meters are uniquely suited for this application because they offer a wide turndown ratio and a completely unobstructed flow path, which minimizes pressure drops and prevents potential energy loss within the supply chain.

As governments implement aggressive decarbonization targets, massive investments are being funneled into green hydrogen electrolyzers and carbon capture systems, all of which require precise flow control to safeguard equipment and ensure commercial viability. Beyond simple measurement, the integration of these meters into digital twin frameworks allows operators to simulate various flow scenarios and optimize the performance of hydrogen blending in existing natural gas grids. This creates a lucrative avenue for manufacturers to develop specialized, "hydrogen-ready" ultrasonic sensors that can withstand the unique chemical properties of the gas. This strategic alignment with the global energy transition ensures that ultrasonic technology will remain a critical component in the next generation of clean energy infrastructure.

Ultrasonic Flow Meter Market Size and Share Analysis:

The Ultrasonic Flow Meter market demonstrates steady growth, with size and share analysis revealing evolving trends and competitive positioning among key players. The report further examines subsegments categorized within implementation type, measurement technology, and end-user industry, offering insights into their contribution to overall market performance.

In the implementation type, the Clamp-On sub-segment is gaining substantial share due to its non-intrusive nature, which allows for installation without interrupting process flow.

Regarding measurement technology, the Transit-Time sub-segment remains the most widely adopted for its superior accuracy in clean liquids and gases, which are prevalent in power and water management.

Among end-users, the Oil and Gas sub-segment continues to be the dominant contributor, utilizing high-path-count ultrasonic meters for precise custody transfer and pipeline leak detection.

Australia, China, India, Japan, South Korea, Indonesia, Malaysia, Philippines, Singapore, Thailand, Vietnam, Bangladesh, New Zealand, Taiwan

South and Central America

Brazil, Argentina, Peru, Chile, Colombia

Middle East and Africa

Bahrain, Kuwait, Oman, Qatar, Saudi Arabia, United Arab Emirates, Turkiye, South Africa, Egypt, Algeria, Nigeria

Market leaders and key company profiles

ABB Ltd.

AichiTokeiDenkiCo.,Ltd.

ApatorSA

AradGroup

BadgerMeterInc.

BakerHughesCompany

BronkhorstHigh-TechBV

DiehlMeteringGmbH

EmersonElectricCo.

Endress+HauserGroupServicesAG

Get more information on this report

Ultrasonic Flow Meter Market Report Coverage and Deliverables:

The "Ultrasonic Flow Meter Market Size and Forecast (2022–2033)" report provides a detailed analysis of the market covering below areas:

Ultrasonic Flow Meter market size and forecast at global, regional, and country levels for all the key market segments covered under the scope

Ultrasonic Flow Meter market trends, as well as market dynamics such as drivers, restraints, and key opportunities

Ultrasonic Flow Meter market analysis covering key market trends, global and regional framework, major players, regulations, and recent market developments

Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments for the Ultrasonic Flow Meter market

Detailed company profiles, including SWOT analysis

Ultrasonic Flow Meter Market Geographic Insights:

The geographical scope of the Ultrasonic Flow Meter market report is divided into five regions: North America, Asia Pacific, Europe, the Middle East & Africa, and South & Central America.

In North America, the market is anchored by the extensive modernization of aging municipal water systems and the rapid expansion of shale gas exploration, where high-precision measurement is critical for both operational efficiency and environmental reporting. Europe maintains a leading position in the technological transition toward the hydrogen economy, with regional activities focused on the deployment of "hydrogen-ready" ultrasonic meters and the integration of advanced sensors into green energy distribution grids to support decarbonization targets. The Asia-Pacific region serves as a primary hub for both high-volume manufacturing and massive infrastructure projects, where rapid urbanization and government-led smart city initiatives in major emerging economies are fueling the large-scale adoption of digital metering solutions.

In the Middle East & Africa, market expansion is largely propelled by high-capital investment in desalination plants and the continued modernization of the oil and gas midstream sector, requiring ruggedized equipment for harsh desert environments. Meanwhile, South & Central America are witnessing a steady rise in demand through the digital transformation of the mining and food processing industries, as regional operators increasingly adopt non-intrusive clamp-on technology to improve resource management and reduce process downtime.

Get more information on this report

Ultrasonic Flow Meter Market Research Report Guidance:

The report includes qualitative and quantitative data in the Ultrasonic Flow Meter market across implementation type, measurement technology, end-user industry, and geography.

The report starts with the key takeaways (chapter 2), highlighting the key trends and outlook of the Ultrasonic Flow Meter market.

Chapter 3 includes the research methodology of the study.

Chapter 4 further includes ecosystem analysis.

Chapter 5 highlights the major industry dynamics in the Ultrasonic Flow Meter market, including factors that are driving the market, prevailing deterrents, potential opportunities, as well as future trends. Impact analysis of these drivers and restraints is also covered in this section.

Chapter 6 discusses the Ultrasonic Flow Meter market scenario, in terms of historical market revenues, and forecast till the year 2033.

Chapters 7 to 10 cover Ultrasonic Flow Meter market segments by implementation type, measurement technology, end-user industry, and geography across North America, Europe, Asia Pacific, the Middle East and Africa, and South and Central America. They cover the market revenue, forecast, and factors driving the market.

Chapter 11 describes the competitive analysis along with the heat map analysis for the key players operating in the market.

Chapter 12 describes the industry landscape analysis. It provides detailed descriptions of business activities such as market initiatives, new developments, mergers, and joint ventures globally, along with a competitive landscape.

Chapter 13 provides detailed profiles of the major companies operating in the Ultrasonic Flow Meter market. Companies have been profiled on the basis of their key facts, business descriptions, products and services, financial overview, SWOT analysis, and key developments.

Chapter 14, i.e., the appendix, is inclusive of a brief overview of the company, a list of abbreviations, and a disclaimer.

Ultrasonic Flow Meter Market News and Key Development:

The Ultrasonic Flow Meter market is evaluated by gathering qualitative and quantitative data post primary and secondary research, which includes important corporate publications, association data, and databases. A few of the key developments in the Ultrasonic Flow Meter market are:

In December 2025, KROHNE highlighted new advancements in Ultrasonic Flow Meter verification designed to improve accuracy and efficiency in custody transfer applications across the oil and gas sector. The company stated that integrating Ultrasonic Flow Meters with small volume provers remained a common yet technically demanding approach for optimizing custody transfer and lowering operational costs. Unlike mechanical meters, these ultrasonic systems featured no moving parts, which reduced maintenance needs and long-term wear while improving overall reliability.

In April 2025, global automation leader Emerson introduced the Flexim FLUXUS / PIOX 731 series, a new range of non-intrusive, clamp-on Ultrasonic Flow Meters designed to offer greater flexibility, convenience, and availability. The nine models in the 731 series featured high-performance volumetric and mass flow sensing technologies and a robust, functional design, which provided accurate and reliable measurements for both liquids and gases with no process media pressure limitations.

Key Sources Referred:

World Bank – Global Trade IndicatorsWorld Trade Organization (WTO)(International Monetary Fund )IMFInternational Trade Administration (ITA)Company websiteCompany annual reportsCompany investor presentations

The List of Companies - Ultrasonic Flow Meter Market

ABB Ltd.

AichiTokeiDenkiCo.,Ltd.

ApatorSA

AradGroup

BadgerMeterInc.

BakerHughesCompany

BronkhorstHigh-TechBV

DiehlMeteringGmbH

EmersonElectricCo.

Endress+HauserGroupServicesAG

About Author— Electronics and Semiconductor Research Team

Siddhika is an experienced market research professional with over five years of expertise in delivering actionable market intelligence and strategic insights to support business growth and decision-making. She has strong experience in designing and managing end-to-end research engagements, including research planning, data collection, and insight generation.

Proficient in research methodologies, Siddhika synthesizes diverse information sources to deliver accurate, high-quality insights and strategic recommendations. She excels at translating complex market information into strategic narratives that support executive decision-making..

Show More

Frequently Asked Questions

How big is the Ultrasonic Flow Meter Market?

The Ultrasonic Flow Meter Market is valued at US$ 2.47 Billion in 2025, it is projected to reach US$ 4.14 Billion by 2033.

What is the CAGR for Ultrasonic Flow Meter Market by (2026 - 2033)?

As per our report Ultrasonic Flow Meter Market, the market size is valued at US$ 2.47 Billion in 2025, projecting it to reach US$ 4.14 Billion by 2033. This translates to a CAGR of approximately 6.67% during the forecast period.

What segments are covered in this report?

The Ultrasonic Flow Meter Market report typically cover these key segments-

Implementation Type (Clamp-On, Inline, Other Implementations)

End-User Industry (Oil and Gas, Power Generation, Water and Wastewater, Other End-Users)

What is the historic period, base year, and forecast period taken for Ultrasonic Flow Meter Market?

The historic period, base year, and forecast period can vary slightly depending on the specific market research report. However, for the Ultrasonic Flow Meter Market report:

Historic Period : 2022-2024

Base Year : 2025

Forecast Period : 2026-2033

Who are the major players in Ultrasonic Flow Meter Market?

The Ultrasonic Flow Meter Market is populated by several key players, each contributing to its growth and innovation. Some of the major players include:

ABB Ltd.

AichiTokeiDenkiCo.,Ltd.

ApatorSA

AradGroup

BadgerMeterInc.

BakerHughesCompany

BronkhorstHigh-TechBV

DiehlMeteringGmbH

EmersonElectricCo.

Endress+HauserGroupServicesAG

Who should buy this report?

The Ultrasonic Flow Meter Market report is valuable for diverse stakeholders, including:

Investors: Provides insights for investment decisions pertaining to market growth, companies, or industry insights. Helps assess market attractiveness and potential returns.

Industry Players: Offers competitive intelligence, market sizing, and trend analysis to inform strategic planning, product development, and sales strategies.

Suppliers and Manufacturers: Helps understand market demand for components, materials, and services related to concerned industry.

Researchers and Consultants: Provides data and analysis for academic research, consulting projects, and market studies.

Financial Institutions: Helps assess risks and opportunities associated with financing or investing in the concerned market.

Essentially, anyone involved in or considering involvement in the Ultrasonic Flow Meter Market value chain can benefit from the information contained in a comprehensive market report.

Get Free Sample For Ultrasonic Flow Meter Market

Get Free Sample For Ultrasonic Flow Meter Market