01

Market Summery

Executive Summary and Global Market Analysis

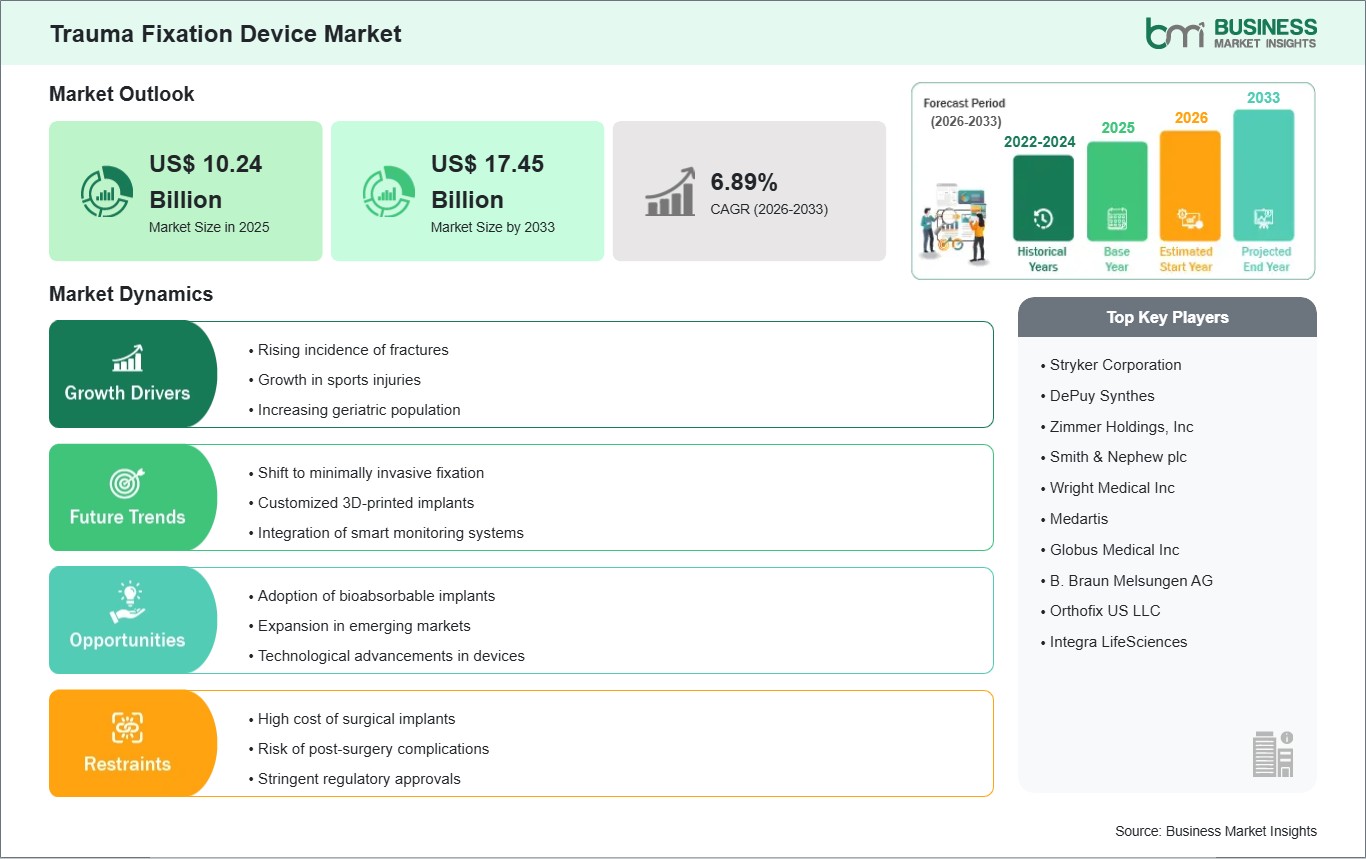

Trauma fixation devices are critical components in modern orthopedic care, designed to stabilize fractures and support natural bone healing. These devices include internal fixators such as plates, screws, and nails, as well as external fixators for complex injuries. The market's growth is fueled by rising global trauma cases, particularly road traffic accidents, sports injuries, and industrial mishaps, alongside an aging population increasingly vulnerable to osteoporotic fractures. These factors underscore the indispensable role of fixation devices in restoring mobility and reducing long-term disability.

However, the industry faces notable challenges. Premium titanium implants, while offering superior biocompatibility and durability, remain cost-prohibitive for many healthcare systems. Regulatory frameworks like the EU MDR impose stringent approval timelines, delaying product launches and increasing compliance costs. Clinical risks such as surgical site infections and metal hypersensitivity further complicate adoption, particularly in resource-limited settings. These barriers demand strategic innovation and cost optimization from manufacturers.

Despite these constraints, the market presents compelling opportunities. Advances in 3D printing are enabling patient-specific implants that improve anatomical precision and reduce surgical time. Bio-absorbable materials are gaining traction, eliminating the need for secondary removal surgeries and enhancing patient outcomes. Additionally, the integration of smart implants equipped with biosensors is redefining post-operative care by enabling real-time monitoring of bone healing. Coupled with the global shift toward minimally invasive procedures and modernization of trauma care units in emerging economies, these trends position the market for sustained growth and technological evolution.

03

Segment Analysis

Trauma Fixation Device Market Segmentation

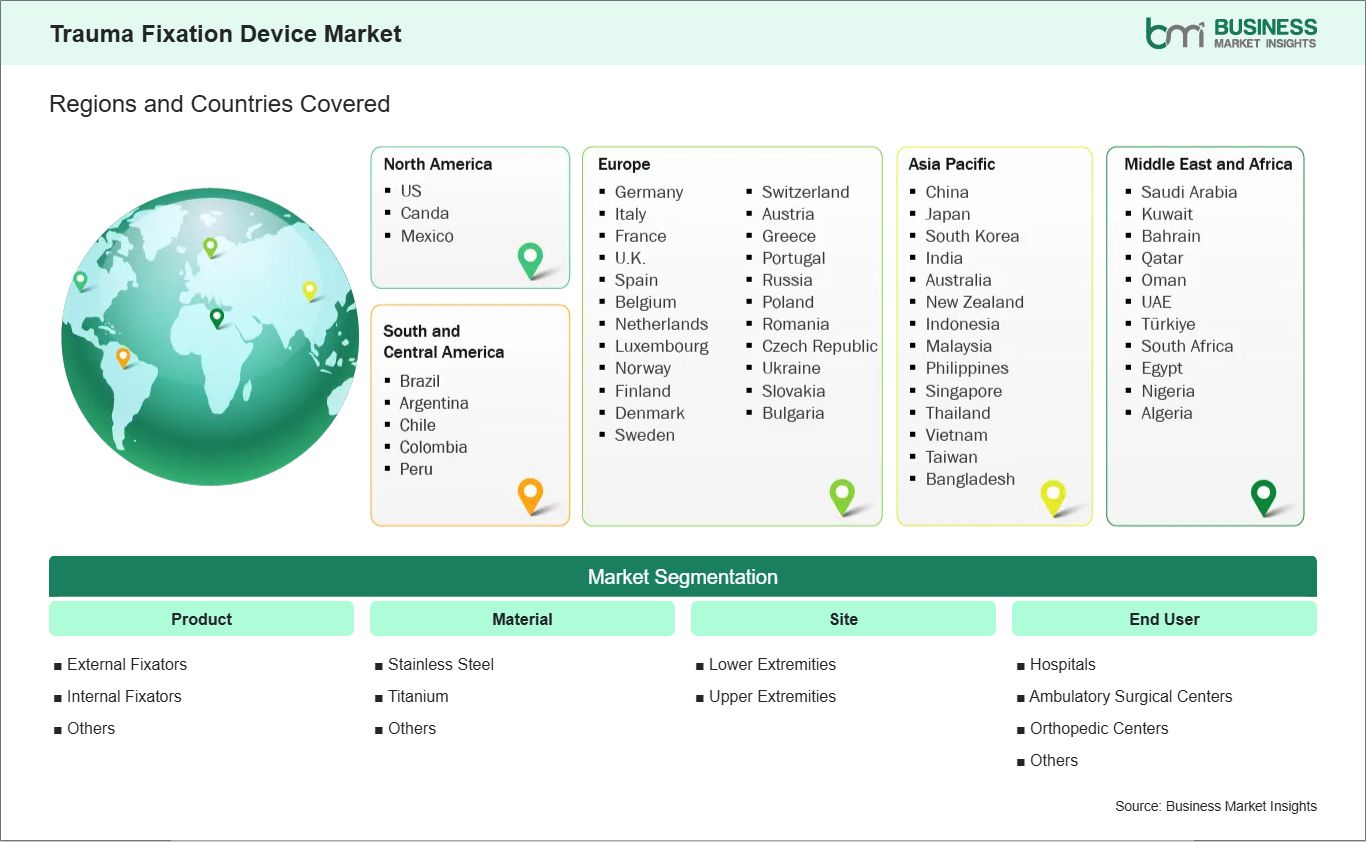

Key segments that contributed to the derivation of the Trauma Fixation Device market analysis are product, material, site, and end user.

- By Product, the market is segmented into External Fixators (Unilateral and Bilateral, Circular, and Hybrid), Internal Fixators (Plates, Screws, and Nails), and Others.

- By Material, the market is segmented into Stainless Steel, Titanium, and Others.

- By Site, the market is segmented into Lower Extremities (Hip And Pelvic, Lower Leg, Knee, Foot & Ankle, and Thigh) and Upper Extremities (Hand & Wrist, Shoulder, Elbow, and Arm).

- By End User, the market is segmented into Hospitals, Ambulatory Surgical Centers, Orthopedic Centers, and Others.

04

Market Forces

Trauma Fixation Device Market Drivers and Opportunities

Surge in Global Trauma Cases and Road Accidents

The steady rise in global vehicular traffic, combined with the high incidence of industrial accidents and sports-related injuries, continues to be a major driver of demand within the orthopedic trauma market. With increasing urbanization, road congestion and motor-vehicle collisions have increased drastically, resulting in a greater number of road incidents leading to fractures and musculoskeletal injuries requiring immediate and effective intervention. Similarly, the expansion of manufacturing sectors and the growing popularity of high-impact sports have contributed to a higher frequency of trauma cases, underscoring the need for reliable stabilization solutions.

Global health statistics consistently show that orthopedic trauma remains one of the leading causes of long-term disability, significantly impacting mobility, productivity, and quality of life. This rising burden places considerable emphasis on the availability of high-performance fixation and stabilization devices capable of supporting proper bone healing and restoring function. As a result, hospitals and trauma centers are increasingly investing in advanced implants, plates, screws, and external fixation systems designed to deliver superior mechanical stability, faster recovery times, and improved patient outcomes.

Advancements in Material Science and 3D Printing

A significant growth opportunity within the market lies in the ongoing shift from traditional stainless-steel implants to advanced materials such as titanium and bio-absorbable polymers. Titanium has gained widespread preference due to its exceptional biocompatibility, corrosion resistance, and superior strength-to-weight ratio, making it particularly well-suited for managing complex fractures that require durable yet lightweight fixation. Its ability to integrate smoothly with bone tissue also reduces the risk of adverse reactions, promoting faster healing and long-term stability.

In parallel, bio-absorbable materials are emerging as an attractive alternative for select indications, offering the advantage of gradually degrading within the body and eliminating the need for secondary surgeries to remove implants. This not only improves patient comfort but also reduces healthcare costs and surgical risks.

Another transformative development is the rapid adoption of 3D printing technologies in trauma care. Additive manufacturing enables the design and production of patient-specific plates and fixation devices that conform precisely to an individual’s anatomy. This level of customization enhances the accuracy of fracture alignment, improves surgical outcomes, and can significantly reduce operative time for surgeons.

05

Size and Share Analysis

Trauma Fixation Device Market Size and Share Analysis

The Trauma Fixation Device market demonstrates steady growth, with size and share analysis revealing evolving trends and competitive positioning among key players. The report further examines subsegments categorized within product, material, site, and end user, offering insights into their contribution to overall market performance.

For instance, within the product segment, internal fixators, such as plates and screws, continue to lead due to their facilitation of early mobilization and reduced infection risk. In terms of material, titanium implants are gaining share in premium markets for their favorable strength-to-weight ratio and biocompatibility. In terms of site, fixation devices used in lower extremities (especially hip and knee) dominate, driven by high fracture incidence among older people. Finally, hospitals remain the main end-user, though ambulatory surgical centers are increasingly involved, reflecting a broader shift toward outpatient orthopedic care.

07

Report Coverage

Trauma Fixation Device Market Report Coverage and Deliverables

The Trauma Fixation Device Market Size and Forecast (2022–2033) report provides a detailed analysis of the market covering below areas:

- Trauma Fixation Device market size and forecast at global, regional, and country levels for all the key market segments covered under the scope

- Trauma Fixation Device market trends, as well as market dynamics such as drivers, restraints, and key opportunities

- Trauma Fixation Device market analysis covering key market trends, global and regional framework, major players, regulations, and recent market developments

- Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments for the Trauma Fixation Device market

- Detailed company profiles, including SWOT analysis

08

Geographic Insights

Trauma Fixation Device Market Geographic Insights

The geographical scope of the Trauma Fixation Device market report is divided into five regions: North America, Asia Pacific, Europe, the Middle East & Africa, and South & Central America.

North America benefits from advanced trauma care systems and strong adoption of innovative technologies. Europe prioritizes high-performance materials and compliance with rigorous safety standards, particularly in countries like Germany and France. Asia-Pacific is witnessing rapid growth driven by increasing road accident rates and expanding healthcare facilities in China and India. In the Middle East & Africa, investments in specialized orthopedic hospitals, especially within the GCC, are accelerating modernization. Meanwhile, South & Central America are gradually transitioning toward contemporary fixation practices, with urban centers in Brazil leading the shift.

10

Industry Activity

Recent Developments

The Trauma Fixation Device market is evaluated by gathering qualitative and quantitative data post primary and secondary research, which includes important corporate publications, association data, and databases. A few of the key developments in the Trauma Fixation Device market are:

- In October 2025, Zimmer launches 2 devices from $1.1B orthopedic takeover. The newly launched devices are the Gorilla Pilon Fusion Plating System and the Phantom TTC Trauma Nail. Paragon’s Gorilla system is used in the stabilization and fixation of a range of fractures.

- In September 2025, CurvaFix, Inc., a developer of medical devices to repair fractures in curved bones, today announced FDA 510(k) clearance for its next-generation CurvaFix® Low Profile System, a percutaneous solution for fixation of pelvic fractures. The CurvaFix Low Profile System is purpose-built to expand surgical options in challenging scenarios, including pathological bone, curved or narrow pelvic corridors, intersecting fixation pathways, and cases where indwelling or adjacent hardware is present.

11

Trust & Transparency

Research Methodology

The market analysis combines proprietary research with secondary data from government agencies, company disclosures, regulatory filings, industry databases and expert interviews. Market estimates are validated through data triangulation, cross-market benchmarking and analyst

review.

View Full Research Methodology

Key Sources Referred:

World Bank – Global Trade IndicatorsWorld Trade Organization (WTO)International Monetary Fund (IMF)International Trade Administration (ITA)Company WebsitesCompany Annual ReportsCompany Investor Presentations