01

Market Summery

Executive Summary and Global Market Analysis

The global timber laminating adhesives market is indeed having a renaissance, driven by the marriage of modern advances in polymer chemistry and the global interest in "tall wood" construction as a sustainable solution. The market has clearly moved away from traditional materials and now focuses on the performance characteristics of polyurethane and emulsion polymer isocyanate adhesives, which can perform well under structural loads while meeting the world’s most stringent environmental requirements. The market is no longer simply a market for adhesives; it is a market to enable a fundamental change in the way the world builds its infrastructure.

The market environment is characterized by the rapidly advancing science of bio-based materials and the incorporation of Industry 4.0 automation. Although the market faces headwinds such as volatility of raw material pricing, the underlying market fundamentals of residential and commercial construction remain strong. Regionally, Europe leads in technical standards and early adoption, while North America and Asia-Pacific are the fastest-growing regions due to massive investments in sustainable housing and urban development. As building codes continue to modernize and the "green" premium becomes a standard requirement, the timber laminating adhesives market is positioned as an essential pillar of the future construction economy.

03

Segment Analysis

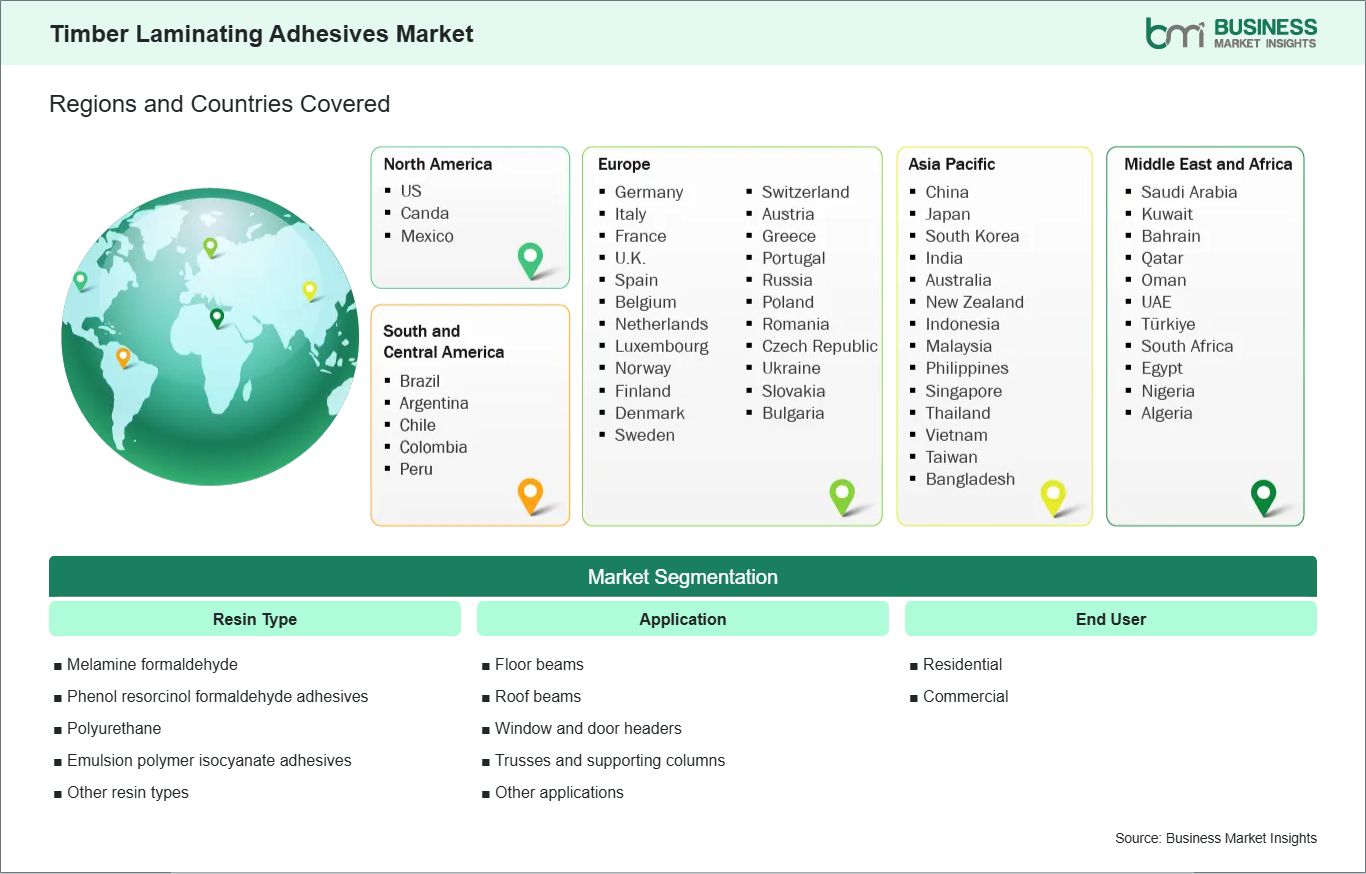

Timber Laminating Adhesives Market Segmentation

Key segments that contributed to the derivation of the Timber Laminating Adhesives market analysis are resin type, application, and end user.

- By resin type, the timber laminating adhesives market is segmented into Melamine formaldehyde, Phenol resorcinol formaldehyde adhesives, Polyurethane, Emulsion polymer isocyanate adhesives, and Other resin types. The Polyurethane segment dominated the market in 2025.

- By application, the timber laminating adhesives market is segmented into Floor beams, Roof beams, Window and door headers, Trusses and supporting columns, and Other applications. The Floor beams segment dominated the market in 2025.

- By end user, the timber laminating adhesives market is segmented into Residential and Commercial. The Residential segment dominated the market in 2025.

04

Market Forces

Timber Laminating Adhesives Market Drivers and Opportunities

Rising Global Adoption of Mass Timber for High-Rise Construction

The cityscape of modern cities is slowly changing as "plyscrapers," or high-rise buildings made of engineered wood, go from idea to reality. This is a huge boon to the timber laminating adhesives market as it uses the chemical bond of adhesives as the sole means of joining small wooden planks into massive CLT and glulam columns. Unlike traditional stick-framing, mass timber construction requires adhesives capable of handling extreme stress while meeting strict international code requirements for safety and longevity. This has led to a technological leap forward in adhesive chemistry, away from traditional rigid resins and toward flexible polymers capable of mimicking the natural expansion and contraction of wood.

The environmental narrative also plays a crucial role here. As the construction industry seeks to reduce its massive carbon footprint, wood is being championed as a carbon-sequestering alternative to carbon-intensive steel and concrete. Adhesives are the "invisible" enabler of this transition; without high-strength laminating agents, the structural use of wood would be limited to small-scale residential projects. As municipal building codes in North America and Europe evolve to allow wood structures of up to 18 stories or more, the demand for certified, high-reliability structural adhesives is projected to see sustained, double-digit growth.

Shift Toward Prefabricated and Modular Building Techniques

Efficiency is the new currency in the construction world, leading to a significant push toward off-site prefabrication and modular assembly. Timber laminating adhesives are perfectly suited for this industrial shift because they allow for the rapid production of standardized building components in a controlled factory environment. In a pre-fab setup, adhesives with fast curing times and clean application profiles, such as one-component polyurethanes, allow manufacturers to significantly increase throughput compared to traditional mechanical fastening. This speed is essential for developers looking to shorten project timelines and reduce on-site labor costs in an increasingly tight market.

Prefabrication also ensures a higher level of quality control, which is vital for the long-term performance of laminated timber. Factory-applied adhesives are subject to precise temperature and pressure controls that are nearly impossible to replicate on a construction site. This leads to more consistent bonding and higher resistance to moisture and delamination over time. As the housing crisis in many regions drives a need for rapid, high-quality residential solutions, the synergy between advanced timber adhesives and modular construction is becoming a primary catalyst for market expansion. This "manufacturing" approach to building ensures that the adhesive becomes a value-added component rather than just a secondary raw material.

05

Size and Share Analysis

Timber Laminating Adhesives Market Size and Share Analysis

The global Timber Laminating Adhesives market is experiencing steady growth, with market size and share analysis reflecting evolving treatment preferences and competitive dynamics among key players. The report evaluates important subsegments categorized within resin type, application, and end user highlighting their respective contributions to overall market performance.

By resin type, the Polyurethane subsegment dominated the market in 2025 due to its superior curing speed, formaldehyde-free chemistry, and exceptional bonding strength in moisture-prone environments, making it the preferred choice for modern cross-laminated timber (CLT) production.

By application, the Floor beams subsegment dominated the market in 2025 due to the rising adoption of engineered wood floor systems in mid-rise urban developments, where high load-bearing capacity and long-span capabilities are critical for structural performance.

By end user, the Residential segment dominated the market in 2025 due to a global surge in single-family and multi-family wood-frame construction, coupled with homeowner preferences for the aesthetic and environmental benefits of exposed timber elements.

07

Report Coverage

Timber Laminating Adhesives Market Report Coverage and Deliverables

The "Timber Laminating Adhesives Market Size and Forecast (2022 - 2033)" report provides a detailed analysis of the market covering below areas:

- Timber Laminating Adhesives market size and forecast at the regional and country levels for segments covered under the scope

- Timber Laminating Adhesives market trends, as well as drivers, restraints, and opportunities

- Timber Laminating Adhesives market analysis covering key trends, regional framework, major players, regulations, and recent developments

- Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments for the Timber Laminating Adhesives market

- Detailed company profiles, including SWOT analysis

08

Geographic Insights

Timber Laminating Adhesives Market Geographic Insights

The geographical scope of the Timber Laminating Adhesives market report is divided into: North America, Asia Pacific, Europe, Middle East & Africa, and South & Central America. North America held the largest share in 2025.

North America currently stands as the most influential region in the timber laminating adhesives market, a position built on a vast forest resource base and a rapidly maturing mass timber ecosystem. The United States and Canada have seen a dramatic rise in the number of CLT and glulam manufacturing facilities over the last several years, driven by a regional push to revitalize the domestic timber industry and address the housing shortage. North American dominance is further supported by proactive updates to the International Building Code (IBC), which has cleared the path for large-scale timber structures in major urban centers. This regulatory clarity has given developers and investors the confidence to scale up wood-based projects, directly increasing the demand for certified, high-performance structural adhesives.

Beyond construction volume, North America is a hub for chemical innovation, housing several of the world’s leading adhesive manufacturers. These companies are working closely with regional forest product labs to develop adhesives specifically tailored for North American wood species, such as Douglas Fir and Southern Yellow Pine. The region's focus on high-efficiency, automated manufacturing also favors the adoption of advanced, fast-curing resins. Additionally, the increasing consumer demand for healthy indoor environments has made North America a leader in the transition toward formaldehyde-free and low-VOC adhesive solutions. With a robust pipeline of commercial and residential timber projects and a strong network of Tier-1 chemical suppliers, North America is poised to remain the global leader in high-value timber adhesive applications.

10

Industry Activity

Recent Developments

The Timber Laminating Adhesives market is evaluated by gathering qualitative and quantitative data post primary and secondary research, which includes important corporate publications, association data, and databases. A few of the key developments in the Timber Laminating Adhesives market are:

- In February 2024, Henkel AG & Co. KGaA announced the expansion of its LOCTITE and TECHNOMELT adhesive solutions portfolio for engineered wood and mass timber applications, focusing on sustainable, low-emission laminating adhesives for construction.

- In June 2023, Sika AG announced the launch of new polyurethane (PUR) structural adhesives designed specifically for cross-laminated timber (CLT) and glulam production, improving bonding strength and durability in load-bearing wooden structures.

- In September 2022, H.B. Fuller Company announced the expansion of its engineering adhesives portfolio for wood construction, including laminating adhesives for mass timber, with a focus on sustainability and compliance with green building standards.

11

Trust & Transparency

Research Methodology

The market analysis combines proprietary research with secondary data from government agencies, company disclosures, regulatory filings, industry databases and expert interviews. Market estimates are validated through data triangulation, cross-market benchmarking and analyst

review.

View Full Research Methodology

Key Sources Referred:

American Chemistry Council (ACC) International Council of Chemical Associations (ICCA) European Chemical Industry Council (Cefic) China National Forest Products Industry Association (CNFPIA) Indian Plywood Industries Research & Training Institute (IPIRTI) Japan Adhesive Industry Association (JAIA) Brazilian Association of Wood Panels and Adhesives (ABIPA) Gulf Petrochemicals and Chemicals Association (GPCA) Company Websites Company Annual Reports Company Investor Presentations