01

Market Summery

Executive Summary and Global Market Analysis

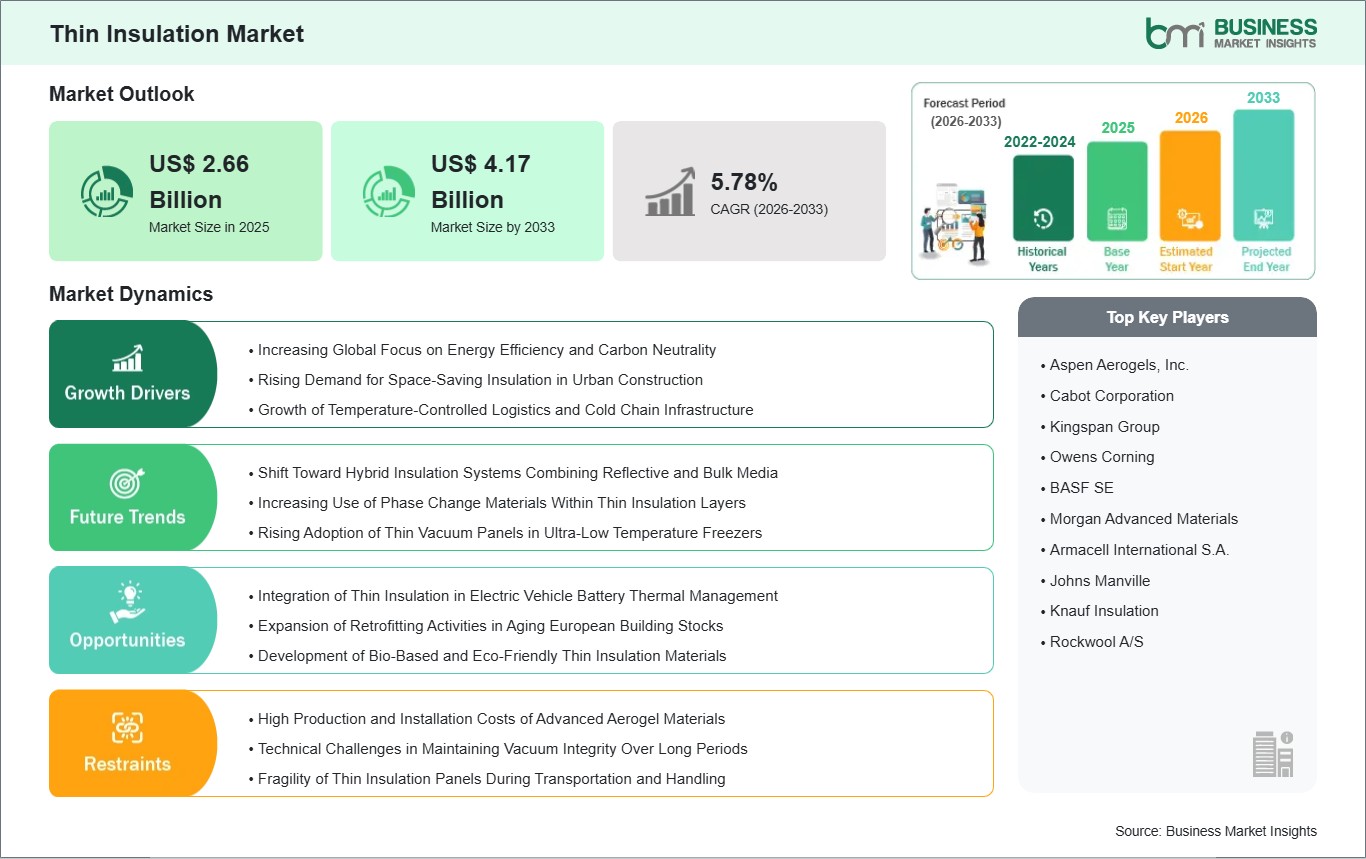

The global thin insulation market is at the forefront of a thermal management revolution. This is due to the fact that there is an unprecedented need for sustainability and space optimization. As industries aim to reach net-zero targets, there is an increased need for materials with high thermal resistance without the added thickness of traditional fiberglass and mineral wool. This market is distinguished by its use of cutting-edge material science, especially with regards to aerogels and vacuum insulation panels. These materials have industry-leading thermal performance in thin profiles and are being adopted at an unprecedented rate in high-growth industries like electric vehicles, space exploration, and high-performance building construction.

Technological advancements in the manufacturing process are also making it easier for the industry to adopt these high-tech materials by making them more durable and easier to install. Even though high initial costs are a factor, the long-term benefits of saving money on energy costs and the additional space that can be obtained with these products in the commercial real estate industry are a great incentive for investing in these products. The industry is also moving towards sustainable and recyclable forms of insulation products with corporate social responsibility for the environment being a major factor in procurement decisions. With North America and Europe being the forerunners in regulation and the Asia-Pacific region driving demand with massive growth in infrastructure development, the thin insulation industry is poised to play a major role in the development of a technologically advanced world that is also environmentally friendly.

03

Segment Analysis

Thin Insulation Market Segmentation

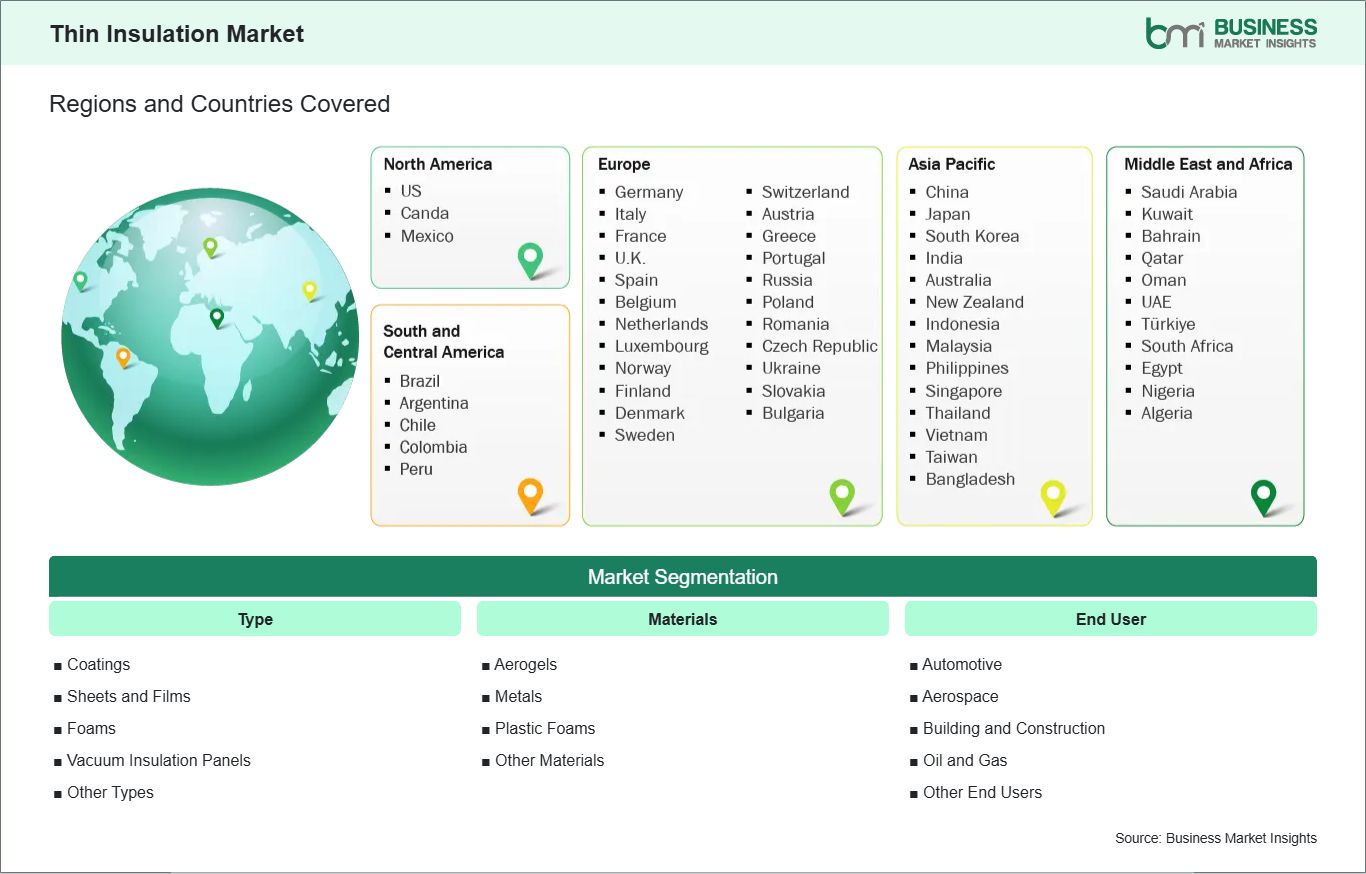

Key segments that contributed to the derivation of the Thin Insulation market analysis are type, materials, and end user.

- By type, the Thin Insulation market is segmented into Coatings, Sheets and Films, Foams, Vacuum Insulation Panels, and Other Types. The Vacuum Insulation Panels segment dominated the market in 2025.

- By materials, the Thin Insulation market is segmented into Aerogels, Metals, Plastic Foams, and Other Materials. The Aerogels segment dominated the market in 2025.

- By end user, the Thin Insulation market is segmented into Automotive, Aerospace, Building and Construction, Oil and Gas, and Other End Users. The Building and Construction segment dominated the market in 2025.

04

Market Forces

Thin Insulation Market Drivers and Opportunities

Increasing Global Focus on Energy Efficiency and Carbon Neutrality

The global move towards a low-carbon economy is the main driver of the thin insulation market. As governments around the world are enforcing stringent climate regulations and measures, the construction and industrial sectors are under tremendous pressure to reduce heat loss and improve their energy consumption. However, conventional insulation materials need to be of considerable thickness to attain high R-values. This is no longer compatible with contemporary architectural and industrial layouts. Vacuum insulation and aerogel materials offer a revolutionary alternative to conventional insulation materials by providing superior thermal insulation with significantly less thickness. This makes it possible to develop highly efficient insulation products with a significantly reduced carbon footprint.

In the industrial landscape, particularly within the oil and gas and power generation sectors, thin insulation is critical for maintaining process temperatures in complex piping networks. By reducing the volume of insulation required, companies can decrease the overall weight of offshore platforms and industrial skids, leading to substantial structural cost savings. Furthermore, the enhanced thermal performance directly correlates to reduced fuel consumption in heating and cooling systems. As international energy standards become more stringent, the shift toward these advanced, space-efficient materials is transitioning from a premium choice to a regulatory necessity for global infrastructure projects.

Integration of Thin Insulation in Electric Vehicle Battery Thermal Management

The rapid electrification of the automotive industry presents a significant opportunity for the thin insulation market. Battery packs in electric vehicles are highly sensitive to temperature fluctuations, requiring sophisticated thermal management systems to ensure safety, longevity, and optimal charging performance. Thin insulation materials are uniquely suited for this application because space within a vehicle chassis is at a premium. By utilizing aerogel blankets or thin reflective films between battery cells and modules, manufacturers can prevent thermal runaway and provide fire protection without adding excessive bulk or weight. This capability is essential for increasing energy density and extending the driving range of next-generation electric platforms.

Beyond safety, thin insulation contributes to the overall cabin efficiency of electric vehicles. Since these vehicles lack the waste heat from internal combustion engines to warm the interior, efficient cabin insulation becomes vital for reducing the energy load on the battery during cold weather. High-performance thin films and coatings applied to vehicle pillars and door panels help maintain interior temperatures more effectively than traditional materials. As automotive original equipment manufacturers compete to deliver vehicles with faster charging times and longer ranges, the integration of advanced, space-saving thermal barriers will become a standard feature in the design of high-performance battery enclosures and cabin interiors.

05

Size and Share Analysis

Thin Insulation Market Size and Share Analysis

The global Thin Insulation market is experiencing steady growth, with market size and share analysis reflecting evolving treatment preferences and competitive dynamics among key players. The report evaluates important subsegments categorized within type, materials, and end user highlighting their respective contributions to overall market performance.

By type, the Vacuum Insulation Panels subsegment dominated the market in 2025 due to its unparalleled thermal resistance in extremely thin profiles, making it the primary choice for high-end refrigeration, temperature-controlled logistics, and space-constrained urban construction projects.

By materials, the Aerogels subsegment dominated the market in 2025 due to its ultra-low thermal conductivity and lightweight nature, providing superior fire resistance and energy efficiency for industrial piping and aerospace components where traditional thick insulation is impractical.

By end user, the Building and Construction subsegment dominated the market in 2025 due to rigorous green building codes and the global trend toward urban densification, which requires high-performance insulation materials that maximize internal floor space while meeting strict energy savings targets.

07

Report Coverage

Thin Insulation Market Report Coverage and Deliverables

The "Thin Insulation Market Size and Forecast (2022 - 2033)" report provides a detailed analysis of the market covering below areas:

- Thin Insulation market size and forecast at the regional and country levels for segments covered under the scope

- Thin Insulation market trends, as well as drivers, restraints, and opportunities

- Thin Insulation market analysis covering key trends, regional framework, major players, regulations, and recent developments

- Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments for the Thin Insulation market

- Detailed company profiles, including SWOT analysis

08

Geographic Insights

Thin Insulation Market Geographic Insights

The geographical scope of the Thin Insulation market report is divided into: North America, Asia Pacific, Europe, Middle East & Africa, and South & Central America. North America held the largest share in 2025.

North America maintains a leading position in the thin insulation market, supported by a robust industrial ecosystem and a high concentration of aerospace and defense players. The region's dominance is particularly evident in the adoption of high-performance thermal barriers for specialized applications, such as satellite components and cryogenic storage systems. In the United States, the Department of Energy’s focus on building weatherization and industrial efficiency has created a strong market pull for advanced aerogels and thin coatings. Furthermore, the North American automotive sector, led by the rapid transition to electric vehicle manufacturing, is a significant consumer of thin insulation for battery thermal management and cabin temperature control, ensuring a steady demand for innovative material solutions.

The dominance of the region is further reinforced by a strong regulatory framework and the presence of major global material innovators headquartered in the U.S. and Canada. Stringent fire safety codes and energy efficiency standards in the commercial construction sector have made North America a primary hub for vacuum insulation panel integration. Additionally, the region benefits from a mature oil and gas industry that increasingly utilizes thin insulation to protect subsea pipelines and refinery equipment in harsh environments. As the region continues to prioritize domestic manufacturing and the development of sustainable energy infrastructure, North America's leadership in the thin insulation market is expected to persist through a combination of high-value industrial demand and continuous technological research.

10

Industry Activity

Recent Developments

The Thin Insulation market is evaluated by gathering qualitative and quantitative data post primary and secondary research, which includes important corporate publications, association data, and databases. A few of the key developments in the Thin Insulation market are:

- In January 2026, 3M, announced the launch of a new line of advanced thin insulation materials optimized for electric vehicle (EV) battery thermal management and lightweight aerospace applications, designed to enhance heat resistance with reduced weight.

- In September 2025, Saint‑Gobain, announced the expansion of its thin high‑performance insulation product portfolio with new aerogel and composite insulation solutions aimed at building retrofits and industrial systems with limited space constraints.

- In June 2025, BASF SE, announced the introduction of a new thin insulation foam formulation for industrial and refrigeration applications that offers improved thermal efficiency with reduced thickness, responding to sustainable energy efficiency trends.

11

Trust & Transparency

Research Methodology

The market analysis combines proprietary research with secondary data from government agencies, company disclosures, regulatory filings, industry databases and expert interviews. Market estimates are validated through data triangulation, cross-market benchmarking and analyst

review.

View Full Research Methodology

Key Sources Referred:

American Chemistry Council (ACC)International Council of Chemical Associations (ICCA)European Chemical Industry Council (Cefic)North American Insulation Manufacturers Association (NAIMA)European Industrial Insulation Foundation (EiiF)Indian Thermal Insulation Manufacturers Association (ITIMA)China Thermal Insulation Materials Association (CTIMA)Japan Thermal Insulation Association (JTIA)Company WebsitesCompany Annual ReportsCompany Investor Presentations