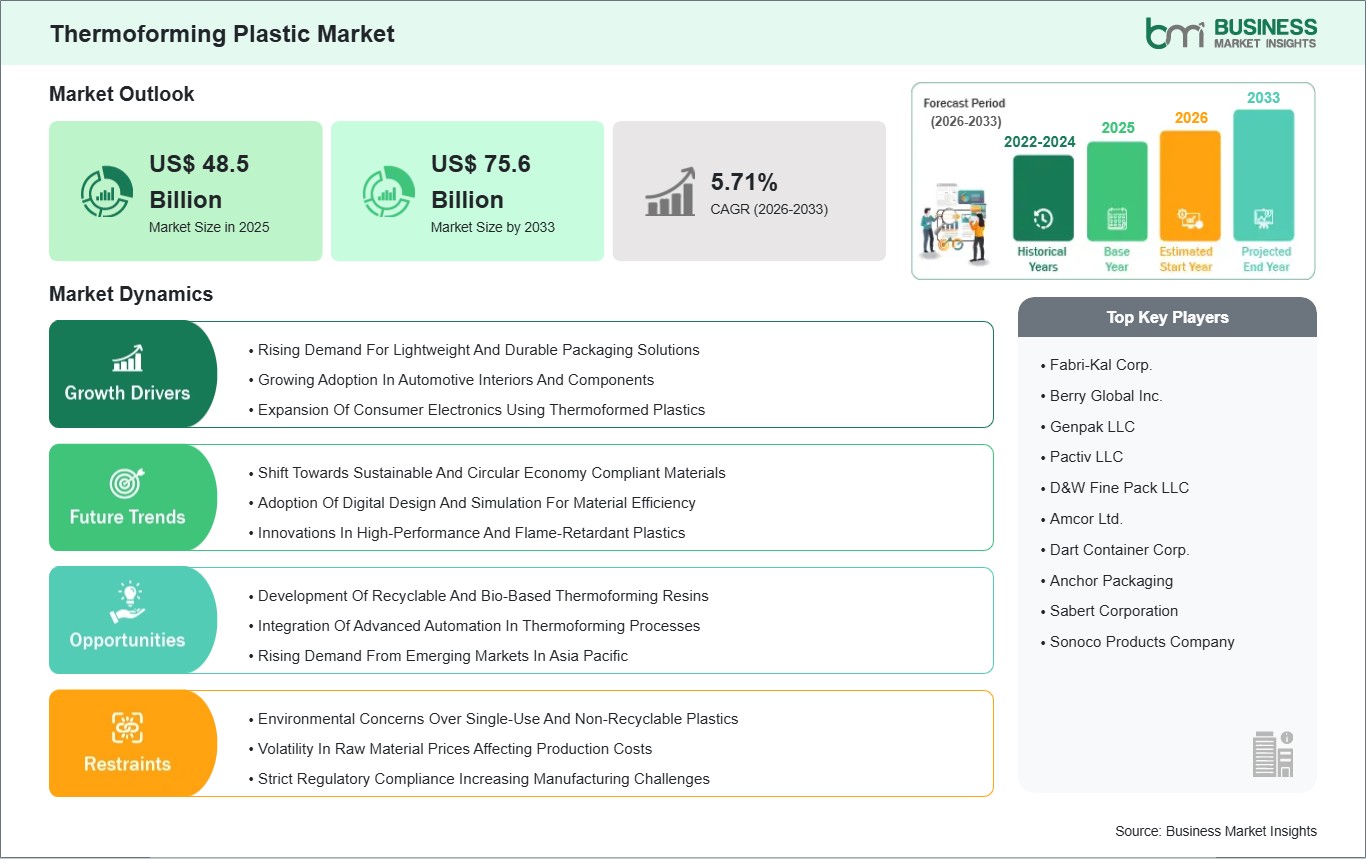

The Thermoforming Plastic Market size is expected to reach US$ 75.6 billion by 2033 from US$ 48.5 billion in 2025. The market is estimated to record a CAGR of 5.71% from 2026 to 2033.

Executive Summary and Global Market Analysis:

The global thermoforming plastic market comprises polymer sheets or films that reach their pliable forming temperature through heating and then undergo shaping into specific designs that result in usable parts or packaging through a molding process followed by trimming. The design flexibility of thermoforming plastics, together with their affordable tooling requirements, lightweight properties and their ability to support production in large quantities, makes them a valuable material. The materials are used for packaging through the production of blister packs, clamshells and trays, while their application extends to automotive interior parts and consumer products, medical equipment, signage and construction profiles. Thermoforming processes enable manufacturers to create product prototypes at high speed while reducing their production time and increasing their ability to modify products, which makes these processes popular in both industrial and consumer product manufacturing.

North America holds a dominant position due to its mature manufacturing base, robust automotive and packaging industries, and significant investments in durable and flexible plastics for industrial applications. The United States and Canada maintain established supply chains that provide polymer resins and advanced thermoforming equipment, while both countries prioritize compliance with rigorous product quality and safety requirements.

North American consumers and industries increasingly demand lightweight, durable, and recyclable plastic solutions, which leads to greater use of thermal plastics for applications ranging from food packaging to automotive interiors. The major forces that drive international markets include three factors: people who live in cities needing more packaged goods, the current demand for lightweight transportation materials and the new polymer technologies which enhance the strength, thermal resistance and sustainable features of thermoforming plastics.

The market experiences limitations because of two factors, which include environmental objections to single-use plastics and government requirements that demand either recycling or bioplastic use and the unpredictable expenses of raw materials, which result from changes in feedstock prices. Manufacturers are investing in recyclable and biopolymer-based thermoforming resins while they choose to implement better forming machines, which will help them decrease both material waste and energy requirements.

The global movement towards sustainable polymers, together with circular economy objectives, represents a major industry development. Companies use post-consumer recycled materials together with recycling-compatible adhesives to create new products. Companies that operate in regions with strict environmental regulations, such as the EU, now include recyclability requirements and decreasing virgin plastic usage in their product design process. Organizations around the world continue to adopt thermoforming plastics because these materials offer environmental advantages, economical benefits, and design versatility.

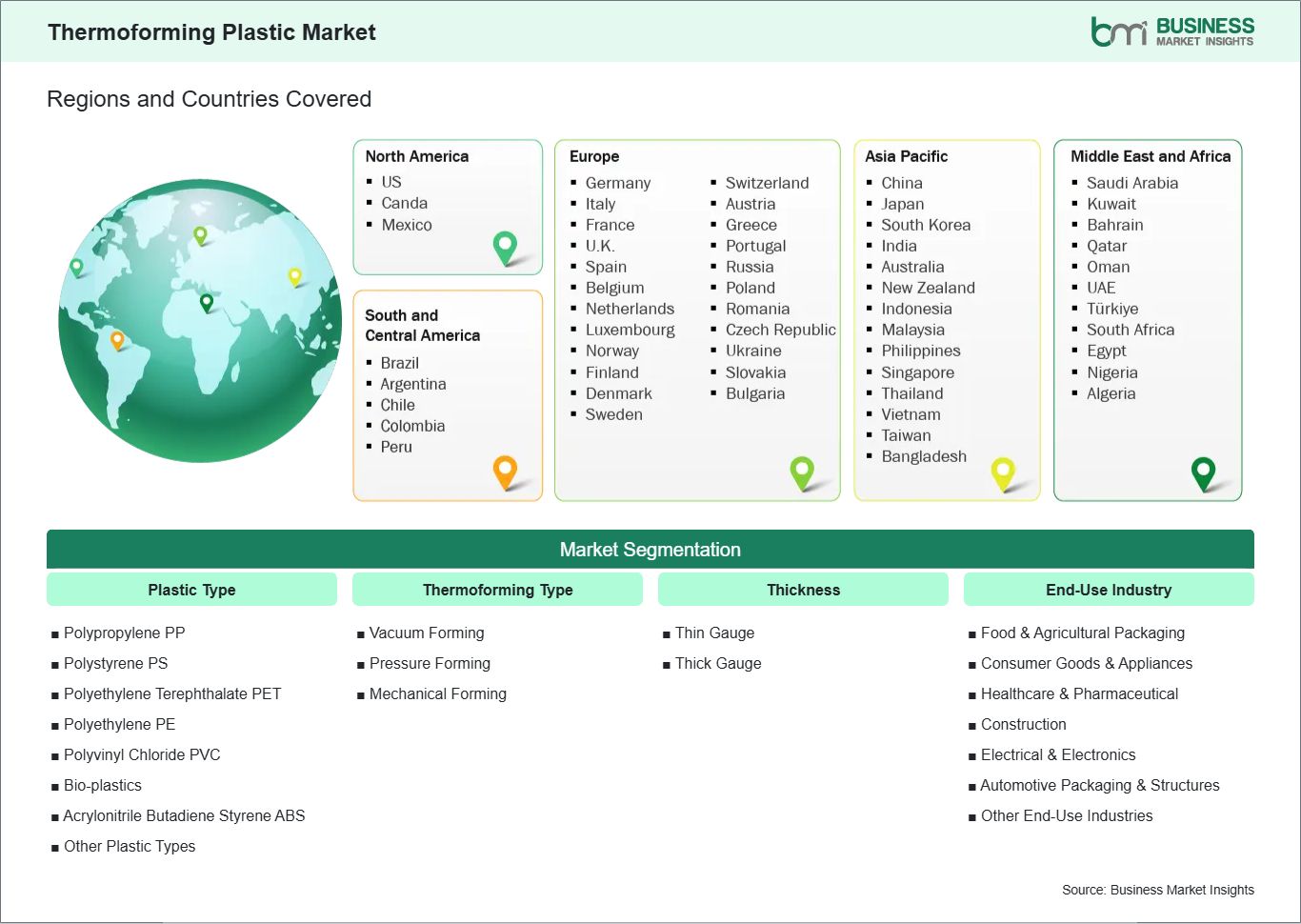

Key segments that contributed to the derivation of the thermoforming plastic market analysis are plastic type, thermoforming type, thickness, and end‑use industry.

By plastic type, the thermoforming plastic market is segmented into polypropylene (PP), polystyrene (PS), polyethylene terephthalate (PET), polyethylene (PE), polyvinyl chloride (PVC), bio‑plastics, acrylonitrile butadiene styrene (ABS), other plastic types. The polypropylene (PP) segment dominated the market in 2025.

Based on thermoforming type, the market is categorized into vacuum forming, pressure forming, mechanical forming. The vacuum forming segment dominated the market in 2025.

On the basis of thickness, the market is categorized into thin gauge, thick gauge. The thin gauge segment dominated the market in 2025.

In terms of end‑use industry, the market is categorized into food & agricultural packaging, consumer goods & appliances, healthcare & pharmaceutical, construction, electrical & electronics, automotive packaging & structures, other end‑use industries. The food & agricultural packaging segment dominated the market in 2025.

Thermoforming Plastic Market Drivers and Opportunities:

Rising Demand For Lightweight And Durable Packaging Solutions

The global rise in lightweight and durable packaging solutions is one of the primary growth drivers for the thermoforming plastic market. Across consumer goods, food & beverage, and healthcare sectors, manufacturers increasingly prefer thermoformed plastics such as PET, PP, and PS over heavier alternatives like metal and glass. These materials deliver the dual benefit of reducing transportation weights and increasing package resilience, which aligns with supply chain efficiency goals and consumer expectations for convenience and product safety. In Europe and North America, strict food safety and containment standards support the adoption of thermoforming packaging that delivers clarity, barrier properties, and mechanical protection.

In Asia Pacific, rapid growth in retail markets and expanding e‑commerce operations have fueled demand for thermoformed trays, clamshells, and custom packaging that protects fragile items while minimizing waste. Countries such as China, India, and Japan are investing heavily in upgrading packaging infrastructure, and local manufacturers are integrating advanced thermoforming resins to meet performance and aesthetic requirements in consumer electronics and fast moving consumer goods markets.

Emerging regions in South America and Africa are gradually increasing use of lightweight thermoformed packaging as logistics and manufacturing sectors modernize. The shift toward modern retail formats and increased emphasis on shelf appeal have encouraged adoption of thermoforming plastics, especially for branded consumer products. Across all regions, the combination of mechanical strength, design flexibility, cost efficiency, and environmental considerations continues to make lightweight, durable thermoformed packaging an important segment of the global plastic market.

Development Of Recyclable And Bio‑Based Thermoforming Resins

The growing global emphasis on sustainability has accelerated innovation in recyclable and bio‑based thermoforming resins. Traditional thermoforming plastics like PVC and non‑recycled PET face scrutiny due to environmental concerns associated with single‑use plastics and landfill accumulation. In response, material scientists and resin producers in North America and Europe are developing modified PET, PP, and PLA blends that support closed‑loop recycling and compatibility with existing recycling streams. These recyclable resins enable manufacturers to maintain thermoforming performance while reducing environmental footprint.

Bio‑based alternatives derived from renewable feedstocks such as sugarcane, corn, or cellulose are gaining traction, particularly in markets where regulatory frameworks incentivize reduced reliance on fossil‑based polymers. In Europe, stringent packaging waste directives and extended producer responsibility policies are pushing brands to incorporate bio‑based thermoforming materials into product lines. Companies in Scandinavia and Western Europe are pioneering hybrid materials that combine post‑consumer recycled content with bio‑derived polymers to meet eco‑label criteria and consumer sustainability expectations.

Asia Pacific manufacturers are also investing in recyclable and bio‑based thermoforming resins to serve export markets with high sustainability requirements. Initiatives in Japan, South Korea, and China focus on scaling production of high‑purity recyclable resins that deliver comparable strength, clarity, and formability to conventional plastics. Across global industries, recyclable and bio‑based thermoforming resins are emerging as strategic solutions that support circular economy goals while maintaining performance standards in packaging and component applications.

Thermoforming Plastic Market Size and Share Analysis:

The thermoforming plastic market demonstrates steady growth, with size and share analysis highlighting evolving trends and competitive dynamics among key players. The report examines subsegments categorized within plastic type, thermoforming type, thickness, and end‑use industry, offering insights into their contribution to overall market performance.

By plastic type, the polypropylene (PP) subsegment dominated the market in 2025, driven by its lightweight, chemical resistance, and cost-effectiveness, making it ideal for high-volume packaging applications.

Based on thermoforming type, the vacuum forming subsegment dominated the market in 2025, driven by its simplicity, cost-efficiency, and wide adoption in producing complex shapes in large volumes.

By thickness, the thin gauge subsegment dominated the market in 2025, driven by its extensive use in high-volume packaging, especially for food and consumer goods, where material efficiency is critical.

In terms of end‑use industry, the food & agricultural packaging subsegment dominated the market in 2025, driven by the rising demand for packaged foods and the need for protective, durable, and lightweight packaging solutions.

Australia, China, India, Japan, South Korea, Indonesia, Malaysia, Philippines, Singapore, Thailand, Vietnam, Bangladesh, New Zealand, Taiwan

South and Central America

Brazil, Argentina, Peru, Chile, Colombia

Middle East and Africa

Bahrain, Kuwait, Oman, Qatar, Saudi Arabia, United Arab Emirates, Turkiye, South Africa, Egypt, Algeria, Nigeria

Market leaders and key company profiles

Fabri-Kal Corp.

Berry Global Inc.

Genpak LLC

Pactiv LLC

D&W Fine Pack LLC

Amcor Ltd.

Dart Container Corp.

Anchor Packaging

Sabert Corporation

Sonoco Products Company

Get more information on this report

Thermoforming Plastic Market Report Coverage and Deliverables:

The "Thermoforming Plastic Market Size and Forecast (2022 - 2033)" report provides a detailed analysis of the market covering below areas:

Thermoforming Plastic Market size and forecast at global, regional, and country levels for all the key market segments covered under the scope

Thermoforming Plastic Market trends, as well as drivers, restraints, and opportunities

Thermoforming Plastic Market analysis covering key trends, global and regional framework, major players, regulations, and recent developments

Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments for the Thermoforming Plastic Market

Detailed company profiles, including SWOT analysis

Thermoforming Plastic Market Geographic Insights:

The geographical scope of the Thermoforming Plastic Market report is divided into North America, Asia Pacific, Europe, Middle East & Africa, and South & Central America. North America held the largest share in 2025.

North America maintains its status as the leading market for thermoforming plastics because of its developed industrial ecosystem, its strong demand from both automotive and packaging industries and its extensive use of advanced plastic production methods. The United States and Canada use thermoforming technology for high-performance packaging, automotive interior parts, medical device enclosures and consumer products, which benefit from the use of lightweight, durable plastics that can be molded easily. The region's established supply chain, together with its research capabilities, allows for quick implementation of new thermoforming resins that meet strict product safety requirements, thus maintaining North America's leading market position. Europe operates as an established market that serves essential needs in food and pharmaceutical packaging, as well as consumer electronics and industrial equipment production. The strict environmental regulations and sustainability targets in Germany, France and Italy lead these countries to emphasize recyclable thermoforming plastics, which include bio-based materials. The European automotive industry creates demand for thermoformed parts, which feature enhanced mechanical strength and thermal resistance. The Asia Pacific region experiences rapid growth because it contains major production centers located in China, Japan, South Korea and India. The increasing adoption of thermoforming plastic materials for packaging, consumer electronics and vehicle interiors stems from urban population growth, the rise of retail and e-commerce and the growth of automotive manufacturing. The region experiences increased adoption of advanced polymers and automated thermoforming processes because infrastructure and industrial automation investments drive these technologies. The Middle East and Africa market shows growth potential, which depends on industrial fabrication and construction and automotive sector expansion, although adoption rates remain low because of differing economic development between countries. South and Central America are building their thermoforming plastics market, which Brazil, Mexico and Argentina drive by using plastics for packaging, consumer products and automotive parts. The global thermoforming plastic market develops through sustainable materials, lightweight design, and cost-efficient manufacturing practices, which North America uses to create performance and innovation standards.

Get more information on this report

Thermoforming Plastic Market Research Report Guidance:

The report includes qualitative and quantitative data in the Thermoforming Plastic Market across plastic type, thermoforming type, thickness, end‑use industry and geography.

The report starts with the key takeaways (chapter 2), highlighting key trends and outlook of the Thermoforming Plastic Market.

Chapter 3 focuses on the research methodology of the study.

Chapter 4 includes ecosystem analysis.

Chapter 5 highlights the major industry dynamics in the Thermoforming Plastic Market, including factors that are driving the market, prevailing deterrents, potential opportunities, as well as future trends. Impact analysis of these drivers and restraints is also covered in this section.

Chapter 6 discusses the Thermoforming Plastic Market scenario, in terms of historical market revenues, and forecast till the year 2033.

Chapters 7 to 11 cover Thermoforming Plastic Market segments by plastic type, thermoforming type, thickness, end‑use industry and geography across North America, Asia Pacific, Europe, Middle East & Africa, and South & Central America. They cover the market revenue forecast and factors driving the market.

Chapter 12 describes the competitive analysis along with the heat map analysis for the key players operating in the market.

Chapter 13 describes the industry landscape analysis. It provides detailed descriptions of business activities such as market initiatives, new developments, mergers, and joint ventures globally, along with a competitive landscape.

Chapter 14 provides detailed profiles of the major companies operating in the Thermoforming Plastic Market. Companies have been profiled on the basis of their key facts, business descriptions, products, financial overview, SWOT analysis, and key developments.

Chapter 15, i.e., the appendix, is inclusive of a brief overview of the company, a list of abbreviations, and a disclaimer.

Thermoforming Plastic Market News and Key Development:

The Thermoforming Plastic Market is evaluated by gathering qualitative and quantitative data post primary and secondary research, which includes important corporate publications, association data, and databases. A few of the key developments in the thermoforming plastic market are:

In September 2025, PolyFlex Products LLC, part of the Nefab Group, announced that it is expanding its thermoforming and plastics packaging manufacturing presence in McMinnville, Tennessee, with a new 137,000‑square‑foot facility that enhances heavy‑gauge thermoforming capabilities and integrates closed‑loop recycling for sustainable plastics production.

In September 2024, C&K Plastics announced that it acquired the Thermoforming Division of Gregstrom Corporation, strengthening its precision thermoforming capabilities and expanding production capacity in key sectors such as medical, communications, and energy.

Key Sources Referred:

World Health Organization (WHO)Organisation for Economic Cooperation and Development (OECD)The World Bank GroupWorldometerThe LancetInternational Bar AssociationInternational Trade Administration

The List of Companies - Thermoforming Plastic Market

Fabri-Kal Corp.

Berry Global Inc.

Genpak LLC

Pactiv LLC

D&W Fine Pack LLC

Amcor Ltd.

Dart Container Corp.

Anchor Packaging

Sabert Corporation

Sonoco Products Company

About Author— Chemicals and Materials Research Team

Suraj Sajeev is a market research and consulting professional with nearly 10 years of experience across Life Sciences, Consumer Goods, Food & Beverages, Materials & Chemicals, and Automotive industries. Throughout his career, he has successfully managed and delivered custom market research and consulting engagements, enabling clients to make informed strategic decisions through actionable market intelligence.

Suraj has extensive expertise in end-to-end project management, including proposal development, market assessment, competitive intelligence, opportunity analysis, market sizing and forecasting, strategic recommendation..

Frequently Asked Questions

How big is the Thermoforming Plastic Market?

The Thermoforming Plastic Market is valued at US$ 48.5 Billion in 2025, it is projected to reach US$ 75.6 Billion by 2033.

What is the CAGR for Thermoforming Plastic Market by (2026 - 2033)?

As per our report Thermoforming Plastic Market, the market size is valued at US$ 48.5 Billion in 2025, projecting it to reach US$ 75.6 Billion by 2033. This translates to a CAGR of approximately 5.71% during the forecast period.

What segments are covered in this report?

The Thermoforming Plastic Market report typically cover these key segments-

What is the historic period, base year, and forecast period taken for Thermoforming Plastic Market?

The historic period, base year, and forecast period can vary slightly depending on the specific market research report. However, for the Thermoforming Plastic Market report:

Historic Period : 2022-2024

Base Year : 2025

Forecast Period : 2026-2033

Who are the major players in Thermoforming Plastic Market?

The Thermoforming Plastic Market is populated by several key players, each contributing to its growth and innovation. Some of the major players include:

Fabri-Kal Corp.

Berry Global Inc.

Genpak LLC

Pactiv LLC

D&W Fine Pack LLC

Amcor Ltd.

Dart Container Corp.

Anchor Packaging

Sabert Corporation

Sonoco Products Company

Who should buy this report?

The Thermoforming Plastic Market report is valuable for diverse stakeholders, including:

Investors: Provides insights for investment decisions pertaining to market growth, companies, or industry insights. Helps assess market attractiveness and potential returns.

Industry Players: Offers competitive intelligence, market sizing, and trend analysis to inform strategic planning, product development, and sales strategies.

Suppliers and Manufacturers: Helps understand market demand for components, materials, and services related to concerned industry.

Researchers and Consultants: Provides data and analysis for academic research, consulting projects, and market studies.

Financial Institutions: Helps assess risks and opportunities associated with financing or investing in the concerned market.

Essentially, anyone involved in or considering involvement in the Thermoforming Plastic Market value chain can benefit from the information contained in a comprehensive market report.

Get Free Sample For Thermoforming Plastic Market

Get Free Sample For Thermoforming Plastic Market