01

Market Summery

Executive Summary and Global Market Analysis

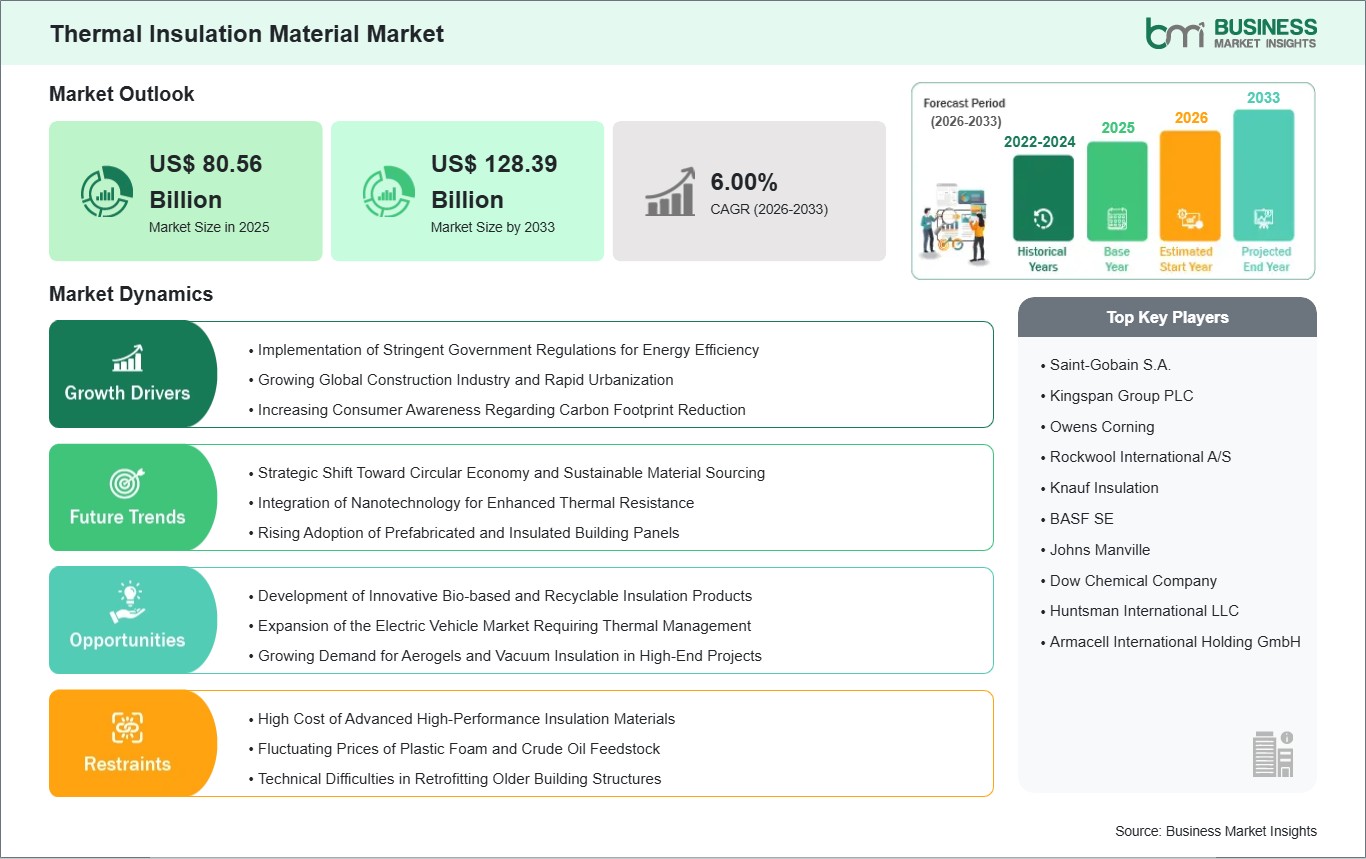

The global thermal insulation material market is undergoing rapid growth as energy price increases and stricter environmental policies push the industry. With decarbonization as the main agenda, insulation is no longer viewed as just a passive building element but rather a key technology in meeting net-zero energy objectives. The focus of the market has progressively been on products that combine improved thermal efficiency with environmentally friendly features. Although expanding polystyrene and glass wool are still the top choices for a majority due to their affordability, more and more people are turning to cutting-edge products like aerogels and vacuum insulation panels for highly specialized fields such as aerospace and high-tech manufacturing.

Geographically, the Asia Pacific region is the fastest-growing hub, fueled by massive infrastructure development and urbanization in China and India. Meanwhile, North America and Europe remain the leaders in terms of technical innovation and the adoption of high-value, sustainable materials. The competitive landscape is becoming more integrated, with major players investing heavily in research to develop thinner, more efficient materials that do not compromise on durability. Despite challenges related to raw material price volatility, the long-term outlook for the market remains highly positive, supported by a global commitment to improving building resilience and industrial energy efficiency.

03

Segment Analysis

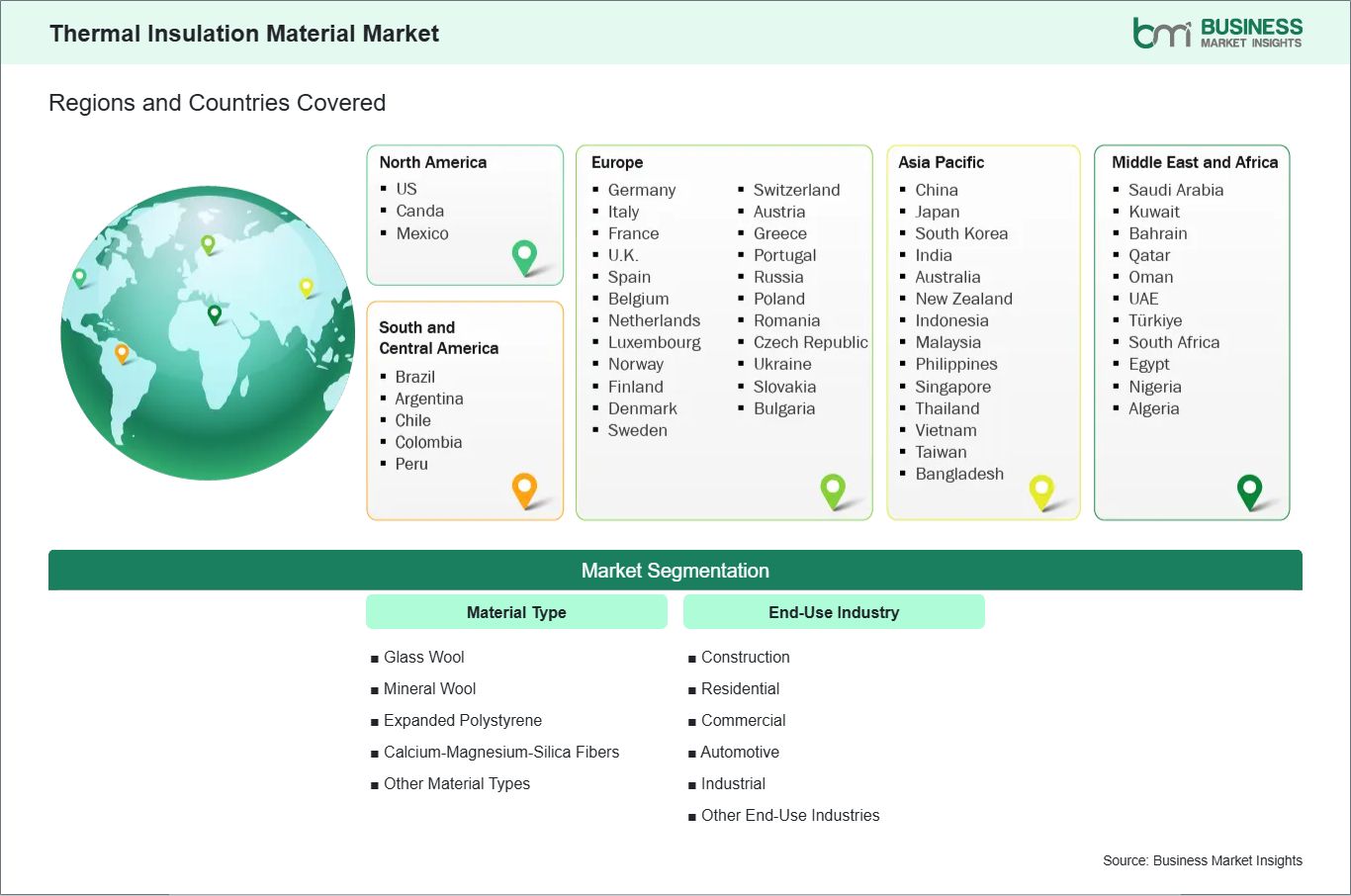

Thermal Insulation Material Market Segmentation

Key segments that contributed to the derivation of the Thermal Insulation Material market analysis are material type and end use industry.

- By material type, the thermal insulation material market is segmented into Glass Wool, Mineral Wool, Expanded Polystyrene, Calcium-Magnesium-Silica Fibers, and Others. The Expanded Polystyrene segment dominated the market in 2025.

- By end-use industry, the thermal insulation material market is segmented into Construction, Residential, Commercial, Automotive, Industrial, and Others. The Construction segment dominated the market in 2025.

04

Market Forces

Thermal Insulation Material Market Drivers and Opportunities

Implementation of Stringent Government Regulations for Energy Efficiency

Global regulatory frameworks have become a primary catalyst for the thermal insulation material market as nations strive to meet ambitious climate targets. Governments in Europe and North America have introduced building energy codes that mandate specific R-values for new constructions, making high-quality insulation a legal necessity rather than a choice. These regulations are designed to lower the carbon emissions associated with heating and cooling, which account for a significant portion of total building energy use. By providing tax incentives and rebates for homeowners who upgrade their insulation, authorities are effectively subsidizing market growth and accelerating the phase-out of inefficient building practices.

Beyond residential codes, industrial standards are also tightening to ensure operational safety and energy conservation in manufacturing plants. Facilities are now required to insulate high-temperature process equipment to protect workers and prevent heat loss, which directly impacts their bottom line. This compliance-driven environment forces architects and engineers to prioritize insulation early in the design phase. As these mandates expand into emerging economies in Asia and Latin America, the global demand for standardized, certified insulation materials is projected to rise steadily, ensuring a stable revenue stream for established manufacturers.

Development of Innovative Bio-based and Recyclable Insulation Products

The move towards green building practices has led to a huge opportunity for bio-based insulation materials that are available in the market with a lower environmental impact compared to traditional synthetic insulation materials. Materials made from natural fibers such as hemp, wool, and cellulose are becoming more popular as they are non-toxic and have a lower carbon footprint compared to traditional materials. These materials are becoming attractive to a growing segment of green building developers and homeowners. The ability to create a sustainable material from agricultural byproducts can create a closed-loop system that can satisfy regional sustainability ratings such as LEED and BREEAM.

Moreover, technology is enhancing their fire resistance and durability, enabling them to compete with conventional glass wool and plastic foams. Advances in treatment processes have enabled bio-based materials to pass very strict safety standards while retaining their superior moisture-wicking capabilities. This is not only true for the materials but also extends to binders, where there is a clear shift towards plant-based resins. As the market aims to reduce its ecological footprint, the commercialization of such high-performance, bio-based insulators is a vital frontier for market diversification and sustainability.

05

Size and Share Analysis

Thermal Insulation Material Market Size and Share Analysis

The global Thermal Insulation Material market is experiencing steady growth, with market size and share analysis reflecting evolving treatment preferences and competitive dynamics among key players. The report evaluates important subsegments categorized within material type and end use industry highlighting their respective contributions to overall market performance.

By material type, the Expanded Polystyrene subsegment dominated the market in 2025 because of its high thermal resistance, lightweight composition, and cost-effectiveness. It is widely preferred in large-scale building projects and cold storage logistics due to its durability and moisture resistance, making it the most economical choice for bulk insulation.

By end-use industry, the Construction subsegment dominated the market in 2025 as a result of rapid global urbanization and the implementation of strict energy-efficient building codes. The massive volume of new residential and commercial infrastructure projects necessitates advanced thermal barriers to reduce energy consumption and meet mandatory sustainability standards.

07

Report Coverage

Thermal Insulation Material Market Report Coverage and Deliverables

The "Thermal Insulation Market Size and Forecast (2022 - 2033)" report provides a detailed analysis of the market covering below areas:

- Thermal Insulation market size and forecast at the regional and country levels for segments covered under the scope

- Thermal Insulation market trends, as well as drivers, restraints, and opportunities

- Thermal Insulation market analysis covering key trends, regional framework, major players, regulations, and recent developments

- Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments for the Thermal Insulation market

- Detailed company profiles, including SWOT analysis

08

Geographic Insights

Thermal Insulation Material Market Geographic Insights

The geographical scope of the Thermal Insulation Material market report is divided into: North America, Asia Pacific, Europe, Middle East & Africa, and South & Central America. North America held the largest share in 2025.

North America is a leading player in the thermal insulation materials market, and this position has been achieved over time with established building codes and a highly advanced industrial base. The United States and Canada have put in place some of the toughest regulations in terms of energy efficiency, and this has meant that a high level of insulation is required in both new constructions and renovation projects. This is further aided by a highly advanced manufacturing and distribution sector, ensuring that a variety of insulation materials are available in the market. Additionally, the extreme climate fluctuations, from arctic conditions to scorching summers, make it a necessity to have high-quality thermal insulation materials to keep temperatures comfortable and costs in check.

The regional market is also characterized by a high rate of technological adoption, with North American companies leading the charge in developing smart insulation and high-R-value materials. The strong presence of the automotive and aerospace industries in the region further bolsters demand, as these sectors require specialized insulation for thermal management in engines and cabins. Additionally, a flourishing renovation market, driven by homeowners seeking to upgrade older properties to modern energy standards, provides a consistent secondary demand stream. While other regions are growing rapidly, North America's combination of technical expertise, large-scale industrial requirements, and proactive environmental policies ensures its continued leadership in the global landscape.

10

Industry Activity

Recent Developments

The Thermal Insulation Material market is evaluated by gathering qualitative and quantitative data post primary and secondary research, which includes important corporate publications, association data, and databases. A few of the key developments in the Thermal Insulation Material market are:

- In January 2023, Owens Corning, announced that it showcased its expanded insulation portfolio at the International Builders’ Show, including newly integrated spray foam insulation products following its acquisition of Natural Polymers, strengthening its position in high-performance thermal insulation solutions.

- In February 2024, ROCKWOOL, announced in its official annual report release that it is advancing toward its sustainability targets and committed to achieving net-zero greenhouse gas emissions by 2050, reinforcing its long-term strategy in sustainable stone wool insulation solutions.

- In July 2023, Kingspan Group, announced plans to acquire a majority stake in Steico SE, a wood fiber insulation manufacturer, to expand its presence in natural and bio-based thermal insulation materials.

11

Trust & Transparency

Research Methodology

The market analysis combines proprietary research with secondary data from government agencies, company disclosures, regulatory filings, industry databases and expert interviews. Market estimates are validated through data triangulation, cross-market benchmarking and analyst

review.

View Full Research Methodology

Key Sources Referred:

American Chemistry Council (ACC) European Chemical Industry Council (Cefic) International Council of Chemical Associations (ICCA) ASTM International International Organization for Standardization (ISO) North American Insulation Manufacturers Association (NAIMA) European Industrial Insulation Foundation (EiiF) Indian Thermal Insulation Manufacturers Association (ITIMA) China Thermal Insulation Materials Association (CTIMA) Japan Thermal Insulation Association (JTIA) Company Websites Company Annual Reports Company Investor Presentations