01

Market Summery

Executive Summary and Global Market Analysis

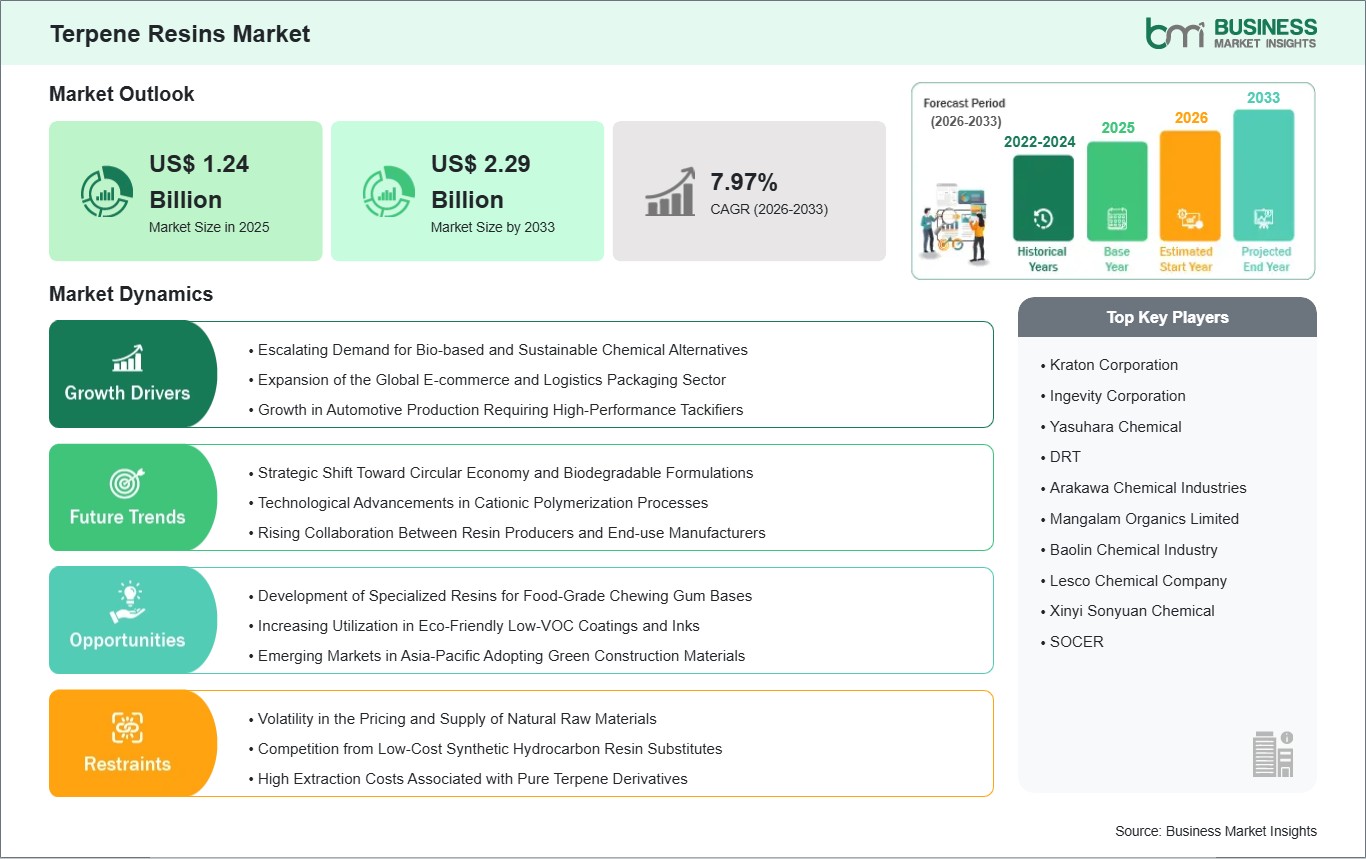

Terpene resin's global market is currently undergoing changes that stem from industrial performance needs versus the requirement for sustainability. These are bio-based polymers that were created for their unique tackifier characteristics as well as their thermal qualities, and thus are valuable in adhesives, coatings, and rubber industries. The change in the marketplace is heavily impacted by materials being sourced from renewable sources instead of using fossil fuels, and terpenes are an alternative material to those fossil fuels, as terpenes are made from waste in the forest and agricultural industries. The adhesives and sealant segment of this industry are still by far the largest contributor of revenue to this industry due to the continued increase in high-strength bonding of products being shipped and assembled in the automotive industry.

The role of technological innovation as a driver of market evolution is not changing, and manufacturers are instead focusing their efforts on improving their polymerization processes to increase the color, odor, and compatibility characteristics of the terpene resins. Despite the fact that the terpene resin market is facing various challenges, including raw material cost volatility and increased competition from lower-cost synthetic resins, the outlook for the market is positive due to the increasing regulations regarding environmental protection worldwide. The terpene resin market is also benefiting from the increasing trend towards the circular economy, and terpene resins will continue to play a vital role in the specialty chemicals chain.

03

Segment Analysis

Terpene Resins Market Segmentation

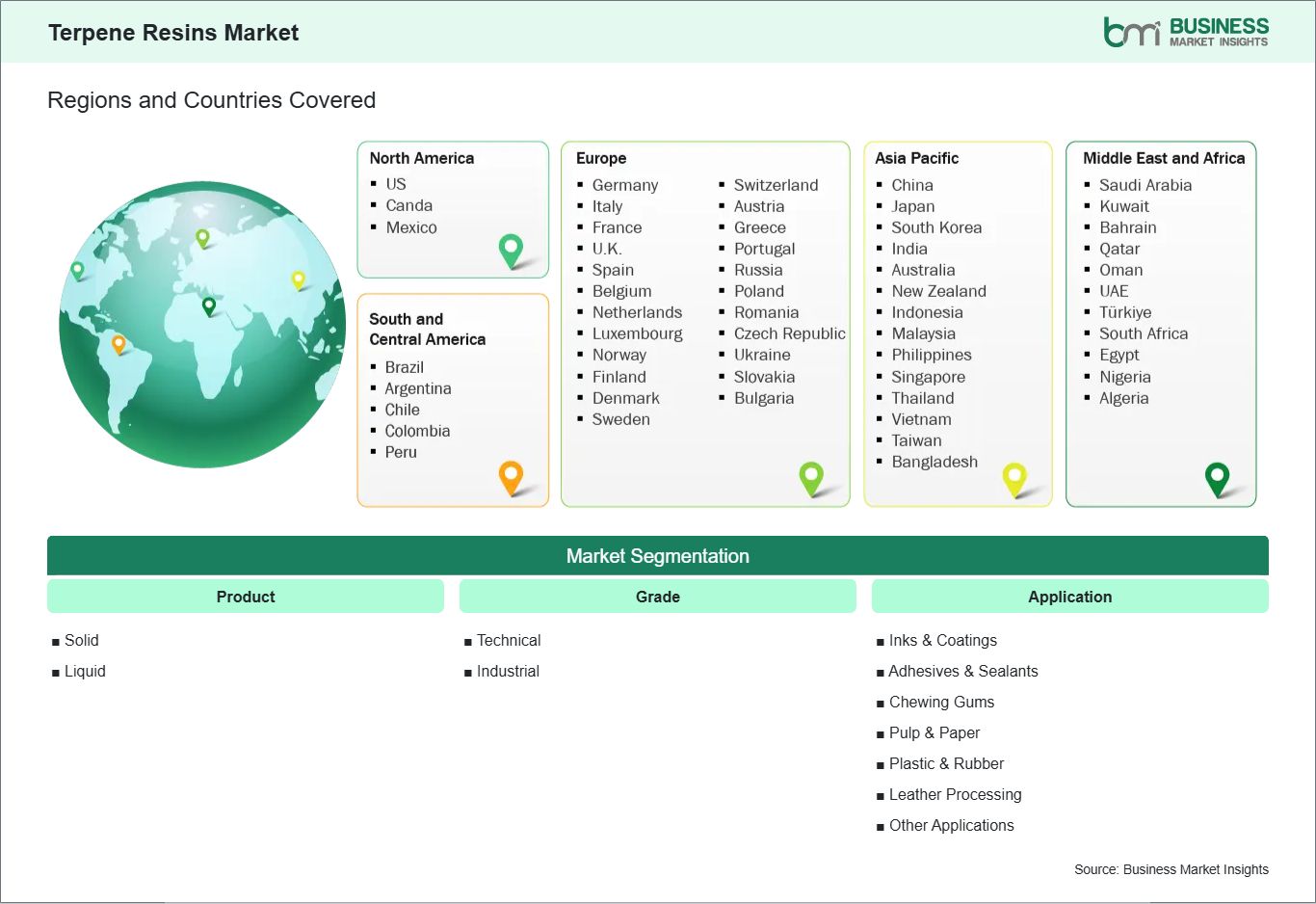

Key segments that contributed to the derivation of the Terpene Resins market analysis are product, grade, and application.

- By product, the terpene resins market is segmented into Solid and Liquid. The Solid segment dominated the market in 2025.

- By grade, the terpene resins market is segmented into Technical and Industrial. The Industrial segment dominated the market in 2025.

- By application, the terpene resins market is segmented into Inks & Coatings, Adhesives & Sealants, Chewing Gums, Pulp & Paper, Plastic & Rubber, Leather Processing, and Others. The Adhesives & Sealants segment dominated the market in 2025.

04

Market Forces

Terpene Resins Market Drivers and Opportunities

Escalating Demand for Bio-based and Sustainable Chemical Alternatives

With the growing trend toward environment-related responsibility worldwide, terpene resin products have become a more attractive alternative to the traditional petroleum-based tackifiers. Terpene resins are derived from renewable raw materials like pine wood and citrus fruit peel and have a much lower carbon footprint than their petroleum counterparts, supporting the aggressive ESG goals set by large corporations. Industries face mounting pressure from regulators and consumers to stop using synthetic chemicals that will ultimately damage the environment. Terpene resins present a natural alternative, providing all of the mechanical performance and chemical stability of conventional additives while being an important part of the current transition to "green" chemistry.

Moreover, the non-toxic nature of terpene-based chemistry is driving its adoption in sensitive sectors such as food packaging and personal care. Unlike many synthetic alternatives, these resins do not leach harmful volatile organic compounds, ensuring safety for end-consumers. This shift is not merely a trend but a structural change in material sourcing strategies. As global supply chains prioritize sustainability, the demand for terpene resins continues to rise, supported by a growing infrastructure for bio-refining. The ability of these resins to offer high compatibility with various polymers while remaining ecologically responsible ensures their long-term viability in a carbon-conscious market.

Development of Specialized Resins for Food-Grade Chewing Gum Bases

The food and beverage sector is a high-value market segment for terpene resin suppliers, and this is particularly evident in the chewing gum market, where terpene resin is required as an essential base component that dictates the texture, elasticity, and flavor profile of chewing gum products. As consumer trends change towards cleaner label formats, there is a clear migration from synthetic rubbers towards more natural resin-based solutions, and this is where highly specialized and food-grade terpene derivatives are required to pass strict international safety and purity criteria.

This is a specialized application with high profit potential, especially in relation to general grades of industrial resin. The production of resins with a consistent chew, while also providing resistance to moisture and oxidation, is a technical feat that requires innovative production capabilities to solve. Additionally, the antimicrobial qualities of certain terpenes offer a secondary benefit, which could potentially increase the shelf life of foodstuffs naturally. As emerging countries begin to increase their level of disposable income and, in turn, their level of confectionery consumption, this market is expected to increase exponentially. This presents a unique opportunity for companies to diversify their portfolios and move into a stable and profitable market of food additives.

05

Size and Share Analysis

Terpene Resins Market Size and Share Analysis

The global Terpene Resins market is experiencing steady growth, with market size and share analysis reflecting evolving treatment preferences and competitive dynamics among key players. The report evaluates important subsegments categorized within product, grade, and application, highlighting their respective contributions to overall market performance.

By product, the Solid subsegment dominated because flaked or granular forms are significantly easier to transport, store, and handle in large-scale industrial processes. Their stable shelf life and compatibility with hot-melt extrusion methods make them the primary choice for global manufacturing chains.

By grade, the Industrial subsegment dominated due to its widespread utility in high-volume sectors like construction and packaging. Its cost-effectiveness and robust physical properties provide the necessary durability and wear resistance required for heavy-duty bonding and material reinforcement in commercial environments.

By application, the Adhesives & Sealants subsegment dominated as terpene resins are essential tackifiers that provide superior adhesion and thermal stability. The explosive growth of e-commerce packaging and automotive lightweighting relies heavily on these resins to ensure high-performance bonding under diverse environmental conditions.

07

Report Coverage

Terpene Resins Market Report Coverage and Deliverables

The "Terpene Resins Market Size and Forecast (2022 - 2033)" report provides a detailed analysis of the market covering below areas:

- Terpene Resins market size and forecast at the regional and country levels for segments covered under the scope

- Terpene Resins market trends, as well as drivers, restraints, and opportunities

- Terpene Resins market analysis covering key trends, regional framework, major players, regulations, and recent developments

- Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments for the Terpene Resins market

- Detailed company profiles, including SWOT analysis

08

Geographic Insights

Terpene Resins Market Geographic Insights

The geographical scope of the Terpene Resins market report is divided into: North America, Asia Pacific, Europe, Middle East & Africa, and South & Central America. North America held the largest share in 2025.

North America stands as the preeminent force in the terpene resins market, a position sustained by its extensive pine-chemical industry and advanced manufacturing infrastructure. The region benefits from a robust supply chain of raw materials, particularly crude tall oil and wood turpentine, which are essential precursors for resin production. This self-sufficiency in feedstock, combined with a highly developed adhesives and coatings sector, allows North American players to maintain a competitive edge in both quality and volume. Furthermore, the region`s stringent environmental policies have accelerated the adoption of bio-based resins, as companies seek to comply with federal and state-level mandates regarding sustainable material sourcing.

The dominance is also reinforced by the presence of major global market leaders and a high level of R&D investment focused on high-performance terpene derivatives. In the United States and Canada, the growth of the logistics and packaging industry, fueled by the world's most mature e-commerce market, creates a consistent and massive demand for terpene-based pressure-sensitive adhesives.

Additionally, the automotive sector in the region is increasingly utilizing these resins for interior bonding and tire manufacturing to meet lightweighting and sustainability targets. While Asia-Pacific is rapidly expanding, North America`s established technical expertise and integrated value chains ensure it remains the primary hub for innovation and high-value resin production.

10

Industry Activity

Recent Developments

The Terpene Resins market is evaluated by gathering qualitative and quantitative data post primary and secondary research, which includes important corporate publications, association data, and databases. A few of the key developments in the Terpene Resins market are:

- In October 2023, DRT (Les Dérivés Résiniques et Terpéniques) announced a significant expansion of its bio-based terpene resin production capacity in Europe to meet growing demand for sustainable adhesive and coating materials.

- In September 2023, Kraton Corporation announced the acquisition of Arkema`s downstream coating resins business, including terpene-based specialty resins, to strengthen its portfolio in performance materials and coatings.

- In March 2022, Yasuhara Chemical Co., Ltd. announced that it signed a long-term agreement with Leaf Resources to secure terpene feedstock supply for five years, reinforcing its terpene resins production capabilities.

11

Trust & Transparency

Research Methodology

The market analysis combines proprietary research with secondary data from government agencies, company disclosures, regulatory filings, industry databases and expert interviews. Market estimates are validated through data triangulation, cross-market benchmarking and analyst

review.

View Full Research Methodology

Key Sources Referred:

American Chemistry Council (ACC) International Council of Chemical Associations (ICCA) European Chemical Industry Council (Cefic) China Petroleum and Chemical Industry Federation (CPCIF) Indian Chemical Council (ICC) Japan Chemical Industry Association (JCIA) Brazilian Chemical Industry Association (ABIQUIM) Gulf Petrochemicals and Chemicals Association (GPCA) Company Websites Company Annual Reports Company Investor Presentations