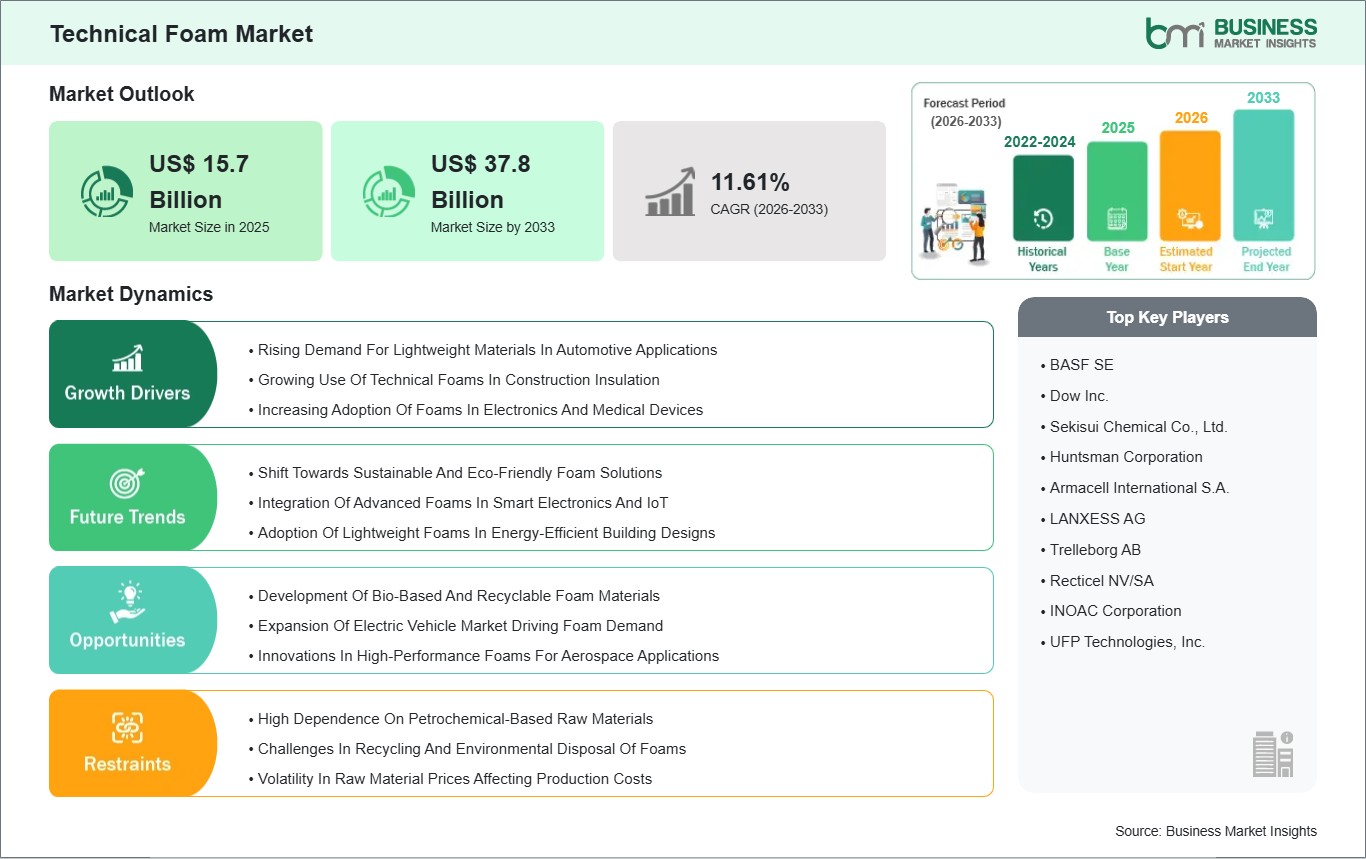

The Technical Foam Market size is expected to reach US$ 37.8 billion by 2033 from US$ 15.7 billion in 2025. The market is estimated to record a CAGR of 11.61% from 2026 to 2033.

Executive Summary and Global Market Analysis:

The global technical foam market has developed into a vital part of advanced materials because multiple industries require materials that can deliver both lightweight characteristics and mechanical strength, insulation, and durability. Technical foams are increasingly replacing traditional materials across industries due to their ability to enhance performance while reducing overall system weight and energy consumption. Their application spans automotive components, construction insulation, medical cushioning, packaging protection, and electronic device stabilization, making them integral to both industrial and consumer-driven sectors. North America holds the top position in global market shares because of its robust industrial base and its tendency to adopt new-engineered materials. The region maintains its leading position because of its advanced automotive manufacturing base, its expanding electric vehicle industry and its focus on developing high-performance construction materials.

The role of technical foams in electric mobility has grown more important because they serve crucial functions in battery insulation, thermal management and vibration control. The increasing requirement for energy-efficient buildings, together with strict insulation regulations leads to higher foam usage in both residential and commercial construction projects. The global market currently operates under three main driving forces, which include the transportation industry shift toward lightweighting, the public's increasing knowledge of building energy efficiency, and the rising need for protective materials that also provide comfort in both consumer and medical products. The ongoing growth of electronic devices and home appliances leads to constant market demand because foams serve dual functions of shock absorption and thermal management.

The market encounters two major obstacles, which include environmental issues that arise from foam waste disposal and recycling processes and the industry's reliance on petrochemical-derived materials for production. Manufacturers need to develop new bio-based and recyclable foam solutions because regulatory agencies require them to decrease carbon emissions and adopt sustainable practices. The market shows a positive future because the ongoing development of new materials and the wider use of existing applications will continue to drive growth.

Technical Foam Market - Strategic Insights:

Get more information on this report

Technical Foam Market Segmentation Analysis:

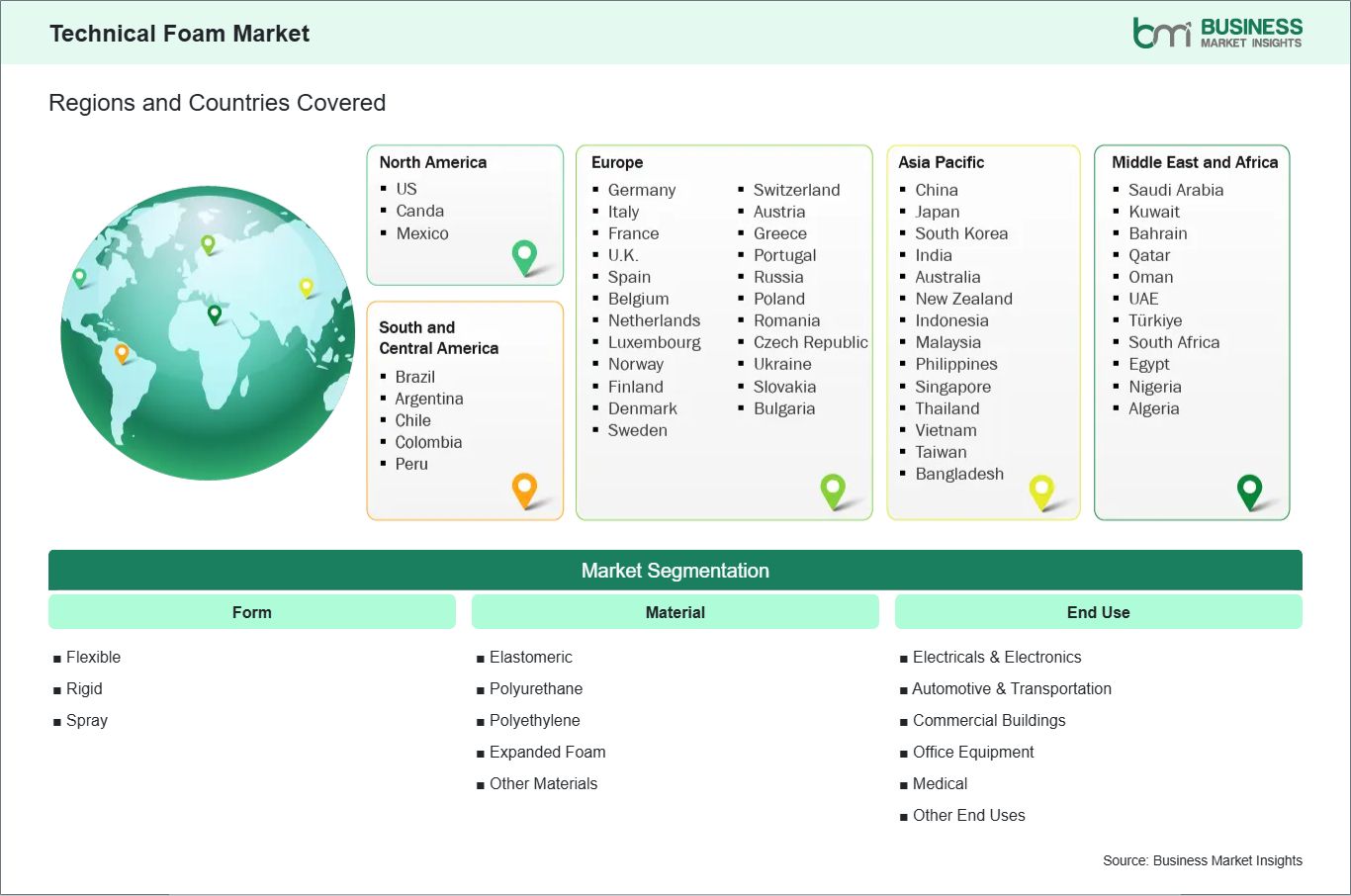

Key segments that contributed to the derivation of the technical foam market analysis are form, material and end use.

By form, the technical foam market is segmented into flexible, rigid, spray. The flexible segment dominated the market in 2025.

Based on material, the technical foam market is categorized into elastomeric, polyurethane, polyethylene, expanded foam, other materials. The polyurethane segment dominated the market in 2025.

In terms of end use, the technical foam market is categorized into electricals & electronics, automotive & transportation, commercial buildings, office equipment, medical, other end uses. The automotive & transportation segment dominated the market in 2025.

Technical Foam Market Drivers and Opportunities:

Rising Demand For Lightweight Materials In Automotive Applications

The global automotive industry is increasingly prioritizing lightweight materials to improve fuel efficiency, reduce emissions, and enhance vehicle performance. Technical foams have become a key solution, offering strength, thermal insulation, and vibration-dampening properties while significantly reducing component weight. From seating systems to interior panels and under-the-hood components, foams are being integrated across multiple automotive applications.

Electric vehicles (EVs) are further accelerating demand, as foams are critical for battery insulation, thermal management, and noise reduction. In Europe and North America, EV adoption is driving manufacturers to source specialized foam solutions that can withstand high temperatures and maintain structural integrity. Asia Pacific, with its rapidly growing automotive production in countries like China, India, and Japan, is also witnessing a surge in foam utilization to meet both conventional and EV requirements.

Moreover, lightweight technical foams contribute to overall sustainability initiatives by reducing energy consumption during transportation. Innovations such as high-density polyurethane foams, flexible elastomeric foams, and composite foam systems are enhancing automotive applications globally. As governments enforce stricter emissions and safety standards, the automotive sector’s reliance on advanced foams is expected to expand steadily, positioning the market for long-term growth and technological innovation.

Development Of Bio-Based And Recyclable Foam Materials

The technical foam market currently moves toward bio-based and recyclable alternatives because of environmental concerns and regulatory requirements. The carbon footprint and disposal problems of petrochemical-based traditional foams face scrutiny because of their environmental impact. Manufacturers across the globe currently direct their resources toward developing bio-polyurethane foams, plant-based polyols and recyclable elastomeric foams that meet performance requirements but decrease environmental harm.

The combination of regulatory frameworks and consumer awareness in Europe has led to the early adoption of sustainable foam materials. The North American market shows a tendency similar to Europe because the automotive, construction and packaging industries increasingly choose bio-based foams to achieve their environmental sustainability goals. The Asia Pacific region, especially China, Japan and South Korea has increased eco-friendly foam production to satisfy the rising demands of industrial and commercial sectors.

The foams provide both environmental benefits and technical advantages, which include durability, thermal resistance and flexibility that matches conventional foams. The circular economy movement drives market adoption through its support of recycling initiatives. With ongoing R&D focused on high-performance bio-based foams, manufacturers are creating solutions that balance environmental responsibility with application-specific demands, ensuring the global technical foam market evolves toward greener, more sustainable materials without compromising functionality.

Technical Foam Market Size and Share Analysis:

The technical foam market demonstrates steady growth, with size and share analysis highlighting evolving trends and competitive dynamics among key players. The report examines subsegments categorized within form, material and end use, offering insights into their contribution to overall market performance.

By form, the flexible subsegment dominated the market in 2025, driven by its widespread use in cushioning, insulation, and vibration damping applications across multiple industries.

Based on material, the polyurethane subsegment dominated the market in 2025, driven by its superior versatility, durability, and excellent thermal and mechanical properties.

In terms of end use, the automotive & transportation subsegment dominated the market in 2025, driven by increasing demand for lightweight, energy-efficient, and noise-reducing materials in vehicles.

Australia, China, India, Japan, South Korea, Indonesia, Malaysia, Philippines, Singapore, Thailand, Vietnam, Bangladesh, New Zealand, Taiwan

South and Central America

Brazil, Argentina, Peru, Chile, Colombia

Middle East and Africa

Bahrain, Kuwait, Oman, Qatar, Saudi Arabia, United Arab Emirates, Turkiye, South Africa, Egypt, Algeria, Nigeria

Market leaders and key company profiles

BASF SE

Dow Inc.

Sekisui Chemical Co., Ltd.

Huntsman Corporation

Armacell International S.A.

LANXESS AG

Trelleborg AB

Recticel NV/SA

INOAC Corporation

UFP Technologies, Inc.

Get more information on this report

Technical Foam Market Report Coverage and Deliverables:

The "Technical Foam Market Size and Forecast (2022 - 2033)" report provides a detailed analysis of the market covering below areas:

Technical Foam Market size and forecast at global, regional, and country levels for all the key market segments covered under the scope

Technical Foam Market trends, as well as drivers, restraints, and opportunities

Technical Foam Market analysis covering key trends, global and regional framework, major players, regulations, and recent developments

Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments for the Technical Foam Market

Detailed company profiles, including SWOT analysis

Technical Foam Market Geographic Insights:

The geographical scope of the Technical Foam Market report is divided into North America, Asia Pacific, Europe, Middle East & Africa, and South & Central America. North America held the largest share in 2025.

North America leads the global technical foam market because its automotive, aerospace and construction industries demand materials that provide high performance together with lightweight and durable insulation, cushioning and vibration control. The United States maintains its regional leadership through its electric vehicle innovations and energy-efficient building material developments, and its industrial applications, which use technical foams for thermal management and noise reduction and structural support. Europe developed into a mature market because of strong adoption in automotive manufacturing, aerospace and green construction projects. The UK, France and Germany pursue sustainable manufacturing through energy-efficient buildings which use bio-based and recyclable foams.

Asia Pacific experiences rapid growth because industrialization, urbanization and automotive production increase throughout China, Japan and India. The region needs foams for packaging and insulation and protective applications because its electronics, medical and transportation sectors continue to expand.

The Middle East & Africa market depends on infrastructure development and industrial expansion while people become more aware of comfort and insulation standards, which affect commercial and residential construction. The countries of UAE, Saudi Arabia and South Africa use technical foams for building insulation and HVAC system components and automotive applications while their adoption remains lower than North America and Europe.

The emerging market of South & Central America is being developed through rising demand from Brazil, Mexico and Argentina for lightweight automotive components, construction insulation and packaging solutions. The region faces challenges such as limited raw material availability and slower technological adoption, but offers growth potential due to rising industrialization and urban infrastructure projects.

The demand for sustainable recyclable technical foams with high performance characteristics has become a worldwide trend because regulatory requirements, energy efficiency targets and the need for lightweight multifunctional materials have driven various industries to adopt these materials, which North America leads while other regions expand at different speeds.

Get more information on this report

Technical Foam Market Research Report Guidance:

The report includes qualitative and quantitative data in the Technical Foam Market across form, material, end use and geography.

The report starts with the key takeaways (chapter 2), highlighting key trends and outlook of the Technical Foam Market.

Chapter 3 focuses on the research methodology of the study.

Chapter 4 includes ecosystem analysis.

Chapter 5 highlights the major industry dynamics in the Technical Foam Market, including factors that are driving the market, prevailing deterrents, potential opportunities, as well as future trends. Impact analysis of these drivers and restraints is also covered in this section.

Chapter 6 discusses the Technical Foam Market scenario, in terms of historical market revenues, and forecast till the year 2033.

Chapters 7 to 10 cover Technical Foam Market segments by form, material, end use and geography across North America, Asia Pacific, Europe, Middle East & Africa, and South & Central America. They cover the market revenue forecast and factors driving the market.

Chapter 11 describes the competitive analysis along with the heat map analysis for the key players operating in the market.

Chapter 12 describes the industry landscape analysis. It provides detailed descriptions of business activities such as market initiatives, new developments, mergers, and joint ventures globally, along with a competitive landscape.

Chapter 13 provides detailed profiles of the major companies operating in the Technical Foam Market. Companies have been profiled on the basis of their key facts, business descriptions, products, financial overview, SWOT analysis, and key developments.

Chapter 14, i.e., the appendix, is inclusive of a brief overview of the company, a list of abbreviations, and a disclaimer.

Technical Foam Market News and Key Development:

The Technical Foam Market is evaluated by gathering qualitative and quantitative data post primary and secondary research, which includes important corporate publications, association data, and databases. A few of the key developments in the technical foam market are:

In September 2024, L&L Products announced that it launched its new InsituCore™ foaming materials for composite manufacturing, expanding its portfolio of technical foam solutions for lightweight components across automotive, aerospace, sporting goods, and other industries.

In June 2025, Armacell announced that it opened a new aerogel insulation manufacturing facility in Pune, India, aimed at producing its advanced ArmaGel® XG product line for global markets. This plant expansion increases production capacity for next‑generation technical foam materials with ultra‑low thermal conductivity, supporting broader adoption in energy‑efficient insulation applications worldwide.

Key Sources Referred:

World Health Organization (WHO)Organisation for Economic Cooperation and Development (OECD)The World Bank GroupWorldometerThe LancetInternational Bar AssociationInternational Trade Administration

The List of Companies - Technical Foam Market

BASF SE

Dow Inc.

Sekisui Chemical Co., Ltd.

Huntsman Corporation

Armacell International S.A.

LANXESS AG

Trelleborg AB

Recticel NV/SA

INOAC Corporation

UFP Technologies, Inc.

Frequently Asked Questions

How big is the Technical Foam Market?

The Technical Foam Market is valued at US$ 15.7 Billion in 2025, it is projected to reach US$ 37.8 Billion by 2033.

What is the CAGR for Technical Foam Market by (2026 - 2033)?

As per our report Technical Foam Market, the market size is valued at US$ 15.7 Billion in 2025, projecting it to reach US$ 37.8 Billion by 2033. This translates to a CAGR of approximately 11.61% during the forecast period.

What segments are covered in this report?

The Technical Foam Market report typically cover these key segments-

Form (Flexible, Rigid, Spray)

Material (Elastomeric, Polyurethane, Polyethylene, Expanded Foam, Other Materials)

End Use (Electricals & Electronics, Automotive & Transportation, Commercial Buildings, Office Equipment, Medical, Other End Uses)

What is the historic period, base year, and forecast period taken for Technical Foam Market?

The historic period, base year, and forecast period can vary slightly depending on the specific market research report. However, for the Technical Foam Market report:

Historic Period : 2022-2024

Base Year : 2025

Forecast Period : 2026-2033

Who are the major players in Technical Foam Market?

The Technical Foam Market is populated by several key players, each contributing to its growth and innovation. Some of the major players include:

BASF SE

Dow Inc.

Sekisui Chemical Co., Ltd.

Huntsman Corporation

Armacell International S.A.

LANXESS AG

Trelleborg AB

Recticel NV/SA

INOAC Corporation

UFP Technologies, Inc.

Who should buy this report?

The Technical Foam Market report is valuable for diverse stakeholders, including:

Investors: Provides insights for investment decisions pertaining to market growth, companies, or industry insights. Helps assess market attractiveness and potential returns.

Industry Players: Offers competitive intelligence, market sizing, and trend analysis to inform strategic planning, product development, and sales strategies.

Suppliers and Manufacturers: Helps understand market demand for components, materials, and services related to concerned industry.

Researchers and Consultants: Provides data and analysis for academic research, consulting projects, and market studies.

Financial Institutions: Helps assess risks and opportunities associated with financing or investing in the concerned market.

Essentially, anyone involved in or considering involvement in the Technical Foam Market value chain can benefit from the information contained in a comprehensive market report.

Get Free Sample For Technical Foam Market

Get Free Sample For Technical Foam Market