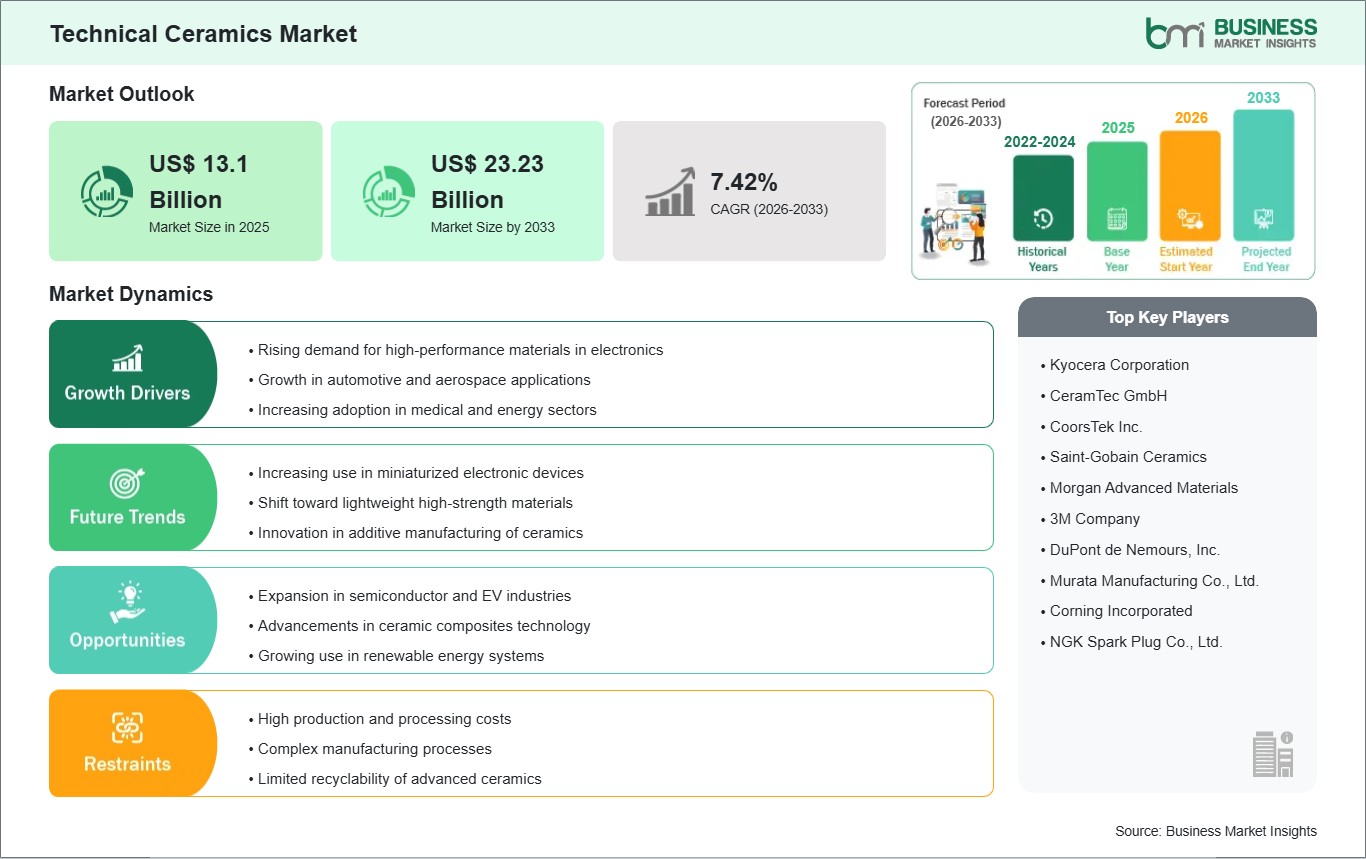

The Technical Ceramics Market size is expected to reach US$ 23.23 billion by 2033 from US$ 13.1 billion in 2025. The market is estimated to record a CAGR of 7.42% from 2026 to 2033.

Executive Summary and Global Market Analysis:

The technical ceramics market is witnessing a steady increase in market growth, and this is attributed to the rising need for high-performance materials in industries such as electronics, automotive, and healthcare. These materials possess excellent properties such as thermal resistance, mechanical strength, and electrical insulation, among others, and this makes them very suitable for high-end industries. Alumina is leading in the material segment of technical ceramics owing to its cost-effectiveness and versatility, while monolithic is leading in the product segment of technical ceramics owing to its reliability and durability.

The electrical and electronics segment is the largest end-user segment for technical ceramics and is driven by the rapid technological advancements in the manufacturing of semiconductor devices and electronics. Although the end-user segment faces challenges such as high production costs and complex processing techniques, the market for technical ceramics is expanding due to the constant technological innovations in the field. Moreover, the research and development activities aimed at improving the properties of the materials and reducing the production costs are increasing the competitiveness of the market for technical ceramics. Thus, the market for technical ceramics is expected to grow steadily with the increasing end-user applications and the need for the materials.

Technical Ceramics Market - Strategic Insights:

Get more information on this report

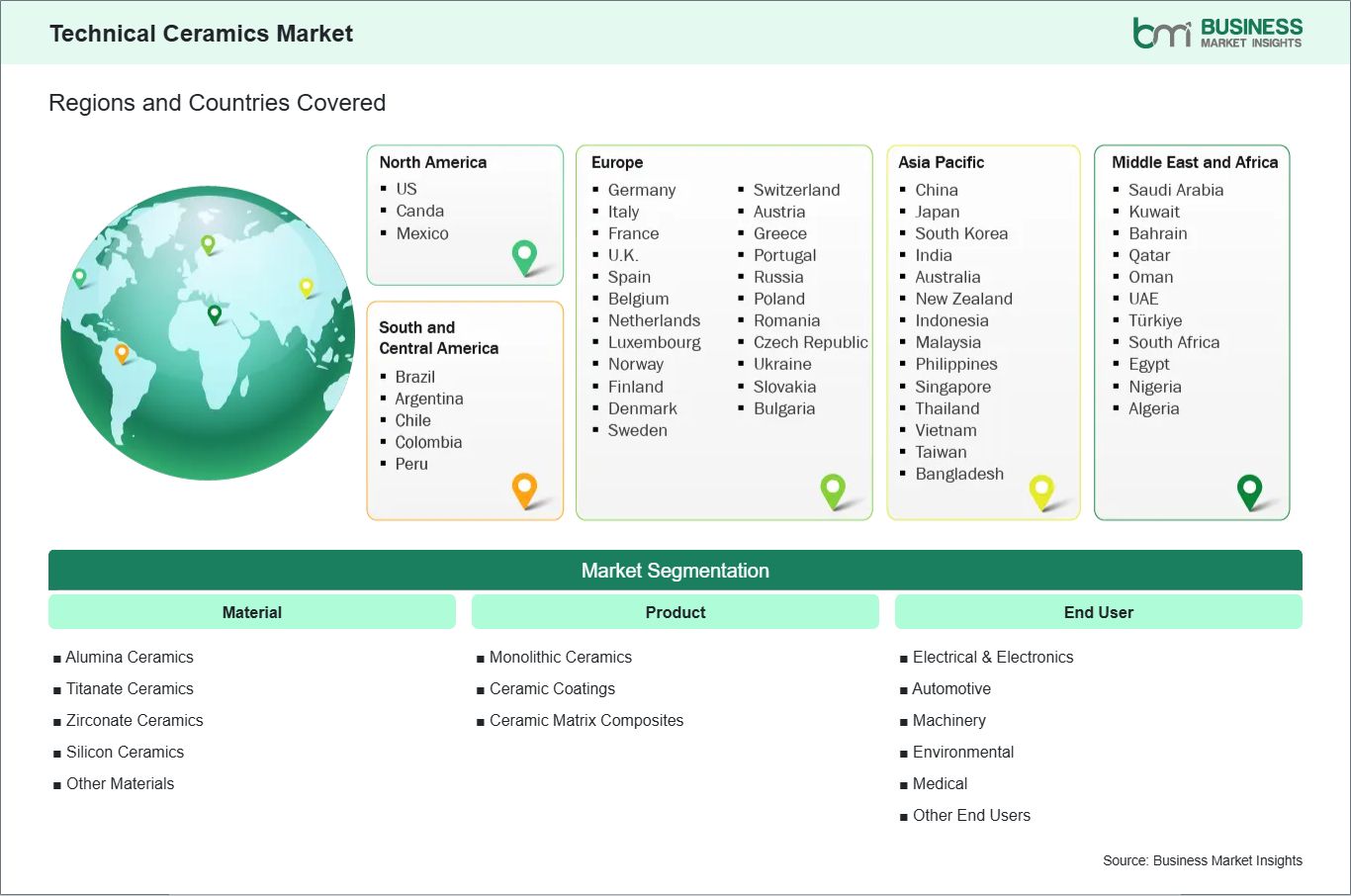

Technical Ceramics Market Segmentation Analysis:

Key segments that contributed to the derivation of the Technical Ceramics market analysis are material, product, and end user.

By material, the technical ceramics market is segmented into Alumina Ceramics, Titanate Ceramics, Zirconate Ceramics, Silicon Ceramics, and Others. The Alumina Ceramics segment dominated the market in 2025.

By product, the technical ceramics market is segmented into Monolithic Ceramics, Ceramic Coatings, and Ceramic Matrix Composites. The Monolithic Ceramics segment dominated the market in 2025.

By end user, the technical ceramics market is segmented into Electrical & Electronics, Automotive, Machinery, Environmental, Medical, and Others. The Electrical & Electronics segment dominated the market in 2025.

Technical Ceramics Market Drivers and Opportunities:

Rising demand for high-performance materials in electronics

The electronics industry is increasingly relying on high-performance materials, driving significant growth in the technical ceramics market. Technical ceramics are valued for their exceptional electrical insulation, high thermal stability, and superior mechanical strength, making them indispensable in the production of substrates, insulators, capacitors, and semiconductor devices. As electronic products continue to evolve toward smaller, faster, and more efficient designs, the need for materials that can maintain stability under extreme thermal and electrical conditions has become critical. This demand spans across advanced applications worldwide, from consumer electronics to industrial systems.

Technological developments in the form of the deployment of 5G technology, the development of AI, and the widespread use of IoT devices are increasingly promoting the use of advanced electronic parts. Technical ceramics are playing a vital role in improving thermal dissipation, reliability, and performance in miniaturized designs. Moreover, the development of semiconductor processes and the increasing global demand for consumer electronics are also promoting the use of technical ceramics. With industries increasingly looking to provide durable, efficient, and innovative products, the use of advanced materials like technical ceramics is likely to increase steadily. This shows that technical ceramics are going to be the key to future electronics in terms of technological development and market development.

Expansion in semiconductor and EV industries

As the semiconductor and EV markets continue to experience explosive growth, there are tremendous opportunities for the technical ceramics industry. The semiconductor and EV industries both rely upon high-performance materials that provide thermal resistance, electrical insulation and mechanical strength so that they maintain reliable performance in harsh environments. Technical ceramics provide all of these characteristics and therefore make excellent candidates for next generation applications which require high efficiency, safety and dependable performance over the long term.

Technical ceramics are a major material class used in semiconductor manufacturing. They are the basis of many wafer processing equipment, insulating components, and high-temperature systems requiring precision and stability. Like in semiconductor manufacturing, technical ceramics are being employed in EVs for battery systems, sensors, power electronics, etc., mainly because these materials are lightweight and can tolerate high heat. The worldwide movement toward electrification and digitalization is the main reason behind investments in both sectors, which led to an increased demand for high-performance materials. While manufacturers increase production and technology advances further, experts forecast that technical ceramics will be the cornerstone of innovation, help sustainability and reliability without a hitch. Wholesale fences this extension makes the market outlook stronger, but at the same time it places technical ceramics as the main driver of future industrial and technological progress

Technical Ceramics Market Size and Share Analysis:

The global Technical Ceramics market is experiencing steady growth, with market size and share analysis reflecting evolving treatment preferences and competitive dynamics among key players. The report evaluates important subsegments categorized within material, product, and end user, highlighting their respective contributions to overall market performance.

By material, the Alumina Ceramics subsegment dominated the market in 2025 due to its excellent electrical insulation, high thermal stability, corrosion resistance, and cost-effectiveness, making it widely used across electronics, automotive, and industrial machinery applications requiring durable and reliable material performance.

By product, the Monolithic Ceramics subsegment dominated the market in 2025 due to their superior mechanical strength, wear resistance, and structural integrity, enabling extensive use in demanding environments such as aerospace, automotive engines, and industrial components requiring high durability and long operational life.

By end user, the Electrical & Electronics subsegment dominated the market in 2025 due to increasing demand for semiconductors, electronic devices, and components requiring materials with high dielectric strength, thermal resistance, and reliability, supporting widespread adoption of technical ceramics in advanced electronic applications.

Australia, China, India, Japan, South Korea, Indonesia, Malaysia, Philippines, Singapore, Thailand, Vietnam, Bangladesh, New Zealand, Taiwan

South and Central America

Brazil, Argentina, Peru, Chile, Colombia

Middle East and Africa

Bahrain, Kuwait, Oman, Qatar, Saudi Arabia, United Arab Emirates, Turkiye, South Africa, Egypt, Algeria, Nigeria

Market leaders and key company profiles

Kyocera Corporation

CeramTec GmbH

CoorsTek Inc.

Saint-Gobain Ceramics

Morgan Advanced Materials

3M Company

DuPont de Nemours, Inc.

Murata Manufacturing Co., Ltd.

Corning Incorporated

NGK Spark Plug Co., Ltd.

Get more information on this report

Technical Ceramics Market Report Coverage and Deliverables:

The "Technical Ceramics Market Size and Forecast (2022 - 2033)" report provides a detailed analysis of the market covering below areas:

Technical Ceramics market size and forecast at the regional and country levels for segments covered under the scope

Technical Ceramics market trends, as well as drivers, restraints, and opportunities

Technical Ceramics market analysis covering key trends, regional framework, major players, regulations, and recent developments

Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments for the Technical Ceramics market

Detailed company profiles, including SWOT analysis

Technical Ceramics Market Geographic Insights:

The geographical scope of the Technical Ceramics market report is divided into: North America, Asia Pacific, Europe, Middle East & Africa, and South & Central America. North America held the largest share in 2025.

North America dominates the technical ceramics market due to strong demand from industries such as electronics, aerospace, automotive, and healthcare. The region benefits from advanced manufacturing infrastructure and significant investment in research and development, enabling the production of high-performance ceramic materials. The presence of leading technology companies and semiconductor manufacturers further drives demand for technical ceramics in electronic components and devices.

Additionally, the growing adoption of electric vehicles and renewable energy technologies is contributing to increased utilization of advanced ceramics in the region. Regulatory standards promoting high-quality and durable materials also support market growth. Continuous innovation and technological advancements are enhancing product capabilities and expanding application areas. The increasing focus on lightweight, energy-efficient, and high-strength materials across industries is further driving demand. Overall, North America maintains its leading position due to strong industrial base, technological leadership, and continuous advancements in material science.

Get more information on this report

Technical Ceramics Market Research Report Guidance:

The report includes qualitative and quantitative data in the Technical Ceramics market across material, product, end user, and geography.

The report starts with the key takeaways (chapter 2), highlighting the key trends and outlook of the Technical Ceramics market.

Chapter 3 focuses on the research methodology of the study.

Chapter 4 includes ecosystem analysis.

Chapter 5 highlights the major industry dynamics in the Technical Ceramics market, including factors that are driving the market, prevailing deterrents, potential opportunities, as well as future trends. Impact analysis of these drivers and restraints is also covered in this section.

Chapter 6 discusses the Technical Ceramics market scenario, in terms of historical market revenues, and forecast till the year 2033.

Chapters 7 to 10 cover the Technical Ceramics market segments by material, product, end user, and geography across North America, Europe, Asia Pacific, the Middle East and Africa, and South and Central America. They cover the market revenue, forecast, and factors driving the market.

Chapter 11 describes the competitive analysis along with the heat map analysis for the key players operating in the market.

Chapter 12 describes the industry landscape analysis. It provides detailed descriptions of business activities such as market initiatives, new developments, mergers, and joint ventures globally, along with a competitive landscape.

Chapter 13 provides detailed profiles of the major companies operating in the Technical Ceramics market. Companies have been profiled on the basis of their key facts, business descriptions, products, financial overview, SWOT analysis, and key developments.

Chapter 14, i.e., the appendix, is inclusive of a brief overview of the company, list of abbreviations, and disclaimer.

Technical Ceramics Market News and Key Development:

The Technical Ceramics market is evaluated by gathering qualitative and quantitative data post primary and secondary research, which includes important corporate publications, association data, and databases. A few of the key developments in the Technical Ceramics market are:

In March 2026, Tethon 3D announced that it acquired a portfolio of intellectual property assets from Fortify to expand its advanced materials and technical ceramics capabilities, particularly for high-performance applications such as RF and microwave components.

In October 2023, IDEX Corporation announced that it entered into an agreement to acquire STC Material Solutions, a manufacturer of technical ceramics and hermetic sealing products, to strengthen its material science and engineered components portfolio.

In March 2025, H.C. Starck announced the acquisition of CeramTec, a global leader in advanced technical ceramics, to significantly expand its product portfolio and global market presence.

Key Sources Referred:

The American Ceramic Society (ACerS)

European Ceramic Society (ECerS)

International Ceramic Federation (ICF)

Ceramic Industry Association (CIA)

Japan Fine Ceramics Association (JFCA)

Indian Ceramic Society (ICS)

China Ceramic Industry Association (CCIA)

Korean Ceramic Society (KCS)

Company Websites

Company Annual Reports

Company Investor Presentations

The List of Companies - Technical Ceramics Market

Kyocera Corporation

CeramTec GmbH

CoorsTek Inc.

Saint-Gobain Ceramics

Morgan Advanced Materials

3M Company

DuPont de Nemours, Inc.

Murata Manufacturing Co., Ltd.

Corning Incorporated

NGK Spark Plug Co., Ltd.

Frequently Asked Questions

How big is the Technical Ceramics Market?

The Technical Ceramics Market is valued at US$ 13.1 Billion in 2025, it is projected to reach US$ 23.23 Billion by 2033.

What is the CAGR for Technical Ceramics Market by (2026 - 2033)?

As per our report Technical Ceramics Market, the market size is valued at US$ 13.1 Billion in 2025, projecting it to reach US$ 23.23 Billion by 2033. This translates to a CAGR of approximately 7.42% during the forecast period.

What segments are covered in this report?

The Technical Ceramics Market report typically cover these key segments-

Material (Alumina Ceramics, Titanate Ceramics, Zirconate Ceramics, Silicon Ceramics, Other Materials)

End User (Electrical & Electronics, Automotive, Machinery, Environmental, Medical, Other End Users)

What is the historic period, base year, and forecast period taken for Technical Ceramics Market?

The historic period, base year, and forecast period can vary slightly depending on the specific market research report. However, for the Technical Ceramics Market report:

Historic Period : 2022-2024

Base Year : 2025

Forecast Period : 2026-2033

Who are the major players in Technical Ceramics Market?

The Technical Ceramics Market is populated by several key players, each contributing to its growth and innovation. Some of the major players include:

Kyocera Corporation

CeramTec GmbH

CoorsTek Inc.

Saint-Gobain Ceramics

Morgan Advanced Materials

3M Company

DuPont de Nemours, Inc.

Murata Manufacturing Co., Ltd.

Corning Incorporated

NGK Spark Plug Co., Ltd.

Who should buy this report?

The Technical Ceramics Market report is valuable for diverse stakeholders, including:

Investors: Provides insights for investment decisions pertaining to market growth, companies, or industry insights. Helps assess market attractiveness and potential returns.

Industry Players: Offers competitive intelligence, market sizing, and trend analysis to inform strategic planning, product development, and sales strategies.

Suppliers and Manufacturers: Helps understand market demand for components, materials, and services related to concerned industry.

Researchers and Consultants: Provides data and analysis for academic research, consulting projects, and market studies.

Financial Institutions: Helps assess risks and opportunities associated with financing or investing in the concerned market.

Essentially, anyone involved in or considering involvement in the Technical Ceramics Market value chain can benefit from the information contained in a comprehensive market report.

Get Free Sample For Technical Ceramics Market

Get Free Sample For Technical Ceramics Market