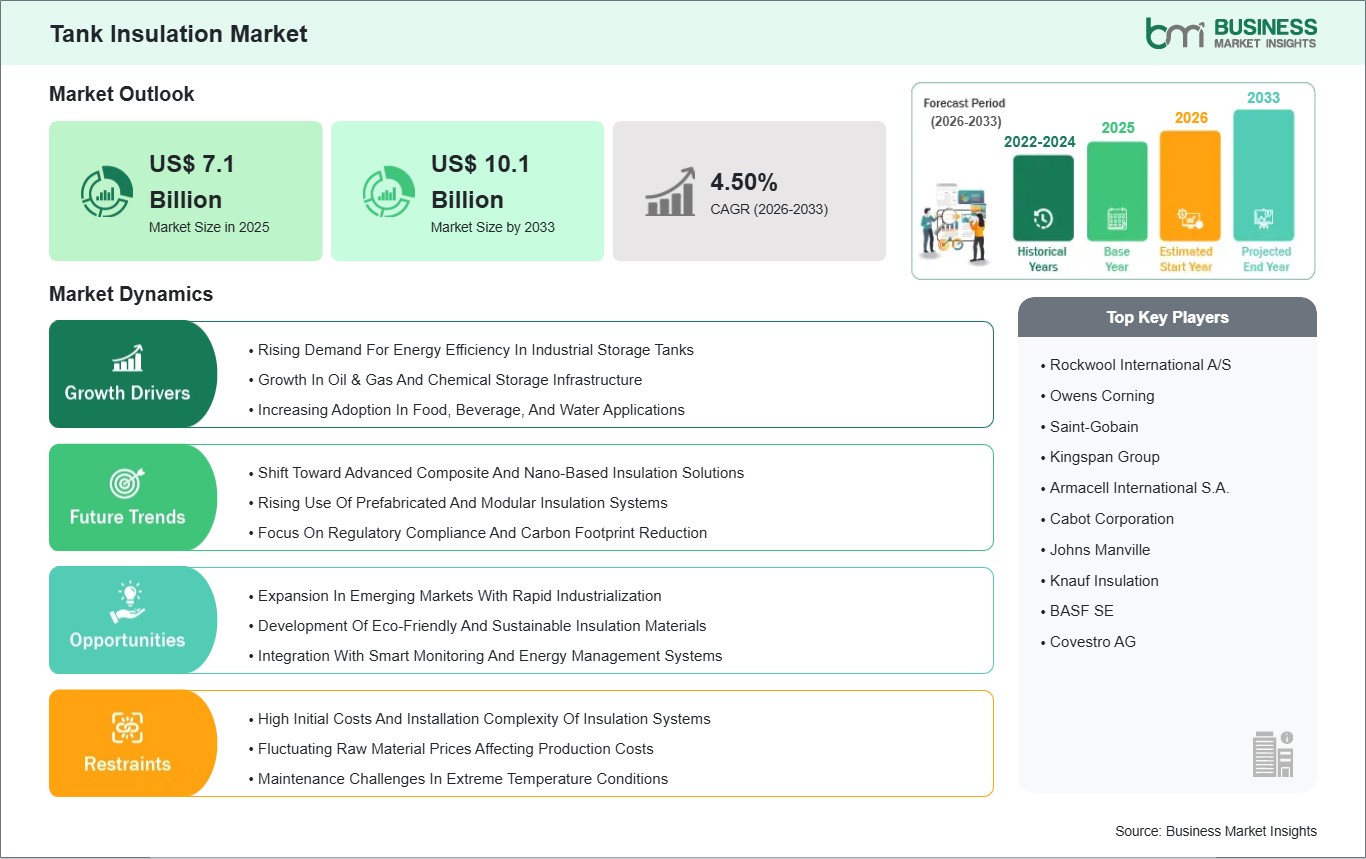

The Tank Insulation Market size is expected to reach US$ 10.1 billion by 2033 from US$ 7.1 billion in 2025. The market is estimated to record a CAGR of 4.50% from 2026 to 2033.

Executive Summary and Global Market Analysis:

The global tank insulation market functions as an essential component for industrial operations, commercial activities and residential buildings because it helps save energy while controlling temperatures and increasing safety and decreasing tank operating expenses, which are used to hold liquids and gases. Tank insulation systems are applied to storage tanks in industries like oil & gas, petrochemical, chemical processing, water treatment, food & beverage, and pharmaceuticals, where maintaining specific temperatures is essential for process integrity, product quality, and safety compliance. The systems use various materials, which include fiberglass, mineral wool, cellular glass, polyurethane foam and elastomeric materials, and they choose materials based on the required thermal resistance, environmental conditions and operational requirements.

Energy efficiency and sustainability have emerged as primary market drivers because organizations increasingly prioritize these two aspects. All industries must decrease their energy consumption and carbon emissions according to growing global demands, and tank insulation optimization provides an effective method to decrease heat loss while enhancing process efficiency for tanks that store both high-temperature fluids and cryogenic gases. Thermal insulation systems in oil and gas storage terminals maintain product temperatures while stopping evaporation losses, which leads to decreased operational expenses and better regulatory compliance. Tank insulation delivers temperature management for water treatment facilities and industrial processes, which is vital to the biological and chemical reaction processes. Industrial infrastructure development in emerging economies serves as one of the main factors driving industrial growth, which results in increased capacity for petrochemical operations, terminal operations and storage facility operations. The requirement for advanced insulation solutions that provide extreme temperature resistance and environmental protection increases as tank sizes grow and systems become more advanced.

The market contains various limitations that restrict its growth. Project costs and schedules will be impacted by advanced insulation material costs, which vary because of two factors: raw material price changes and supply chain interruptions. Existing facilities need insulation installation and maintenance, which requires extensive manpower and technical skills to execute, especially for large buildings that need specific insulation solutions. Cost-sensitive applications and locations without specialized installation skills face challenges because of these factors.

Tank Insulation Market - Strategic Insights:

Get more information on this report

Tank Insulation Market Segmentation Analysis:

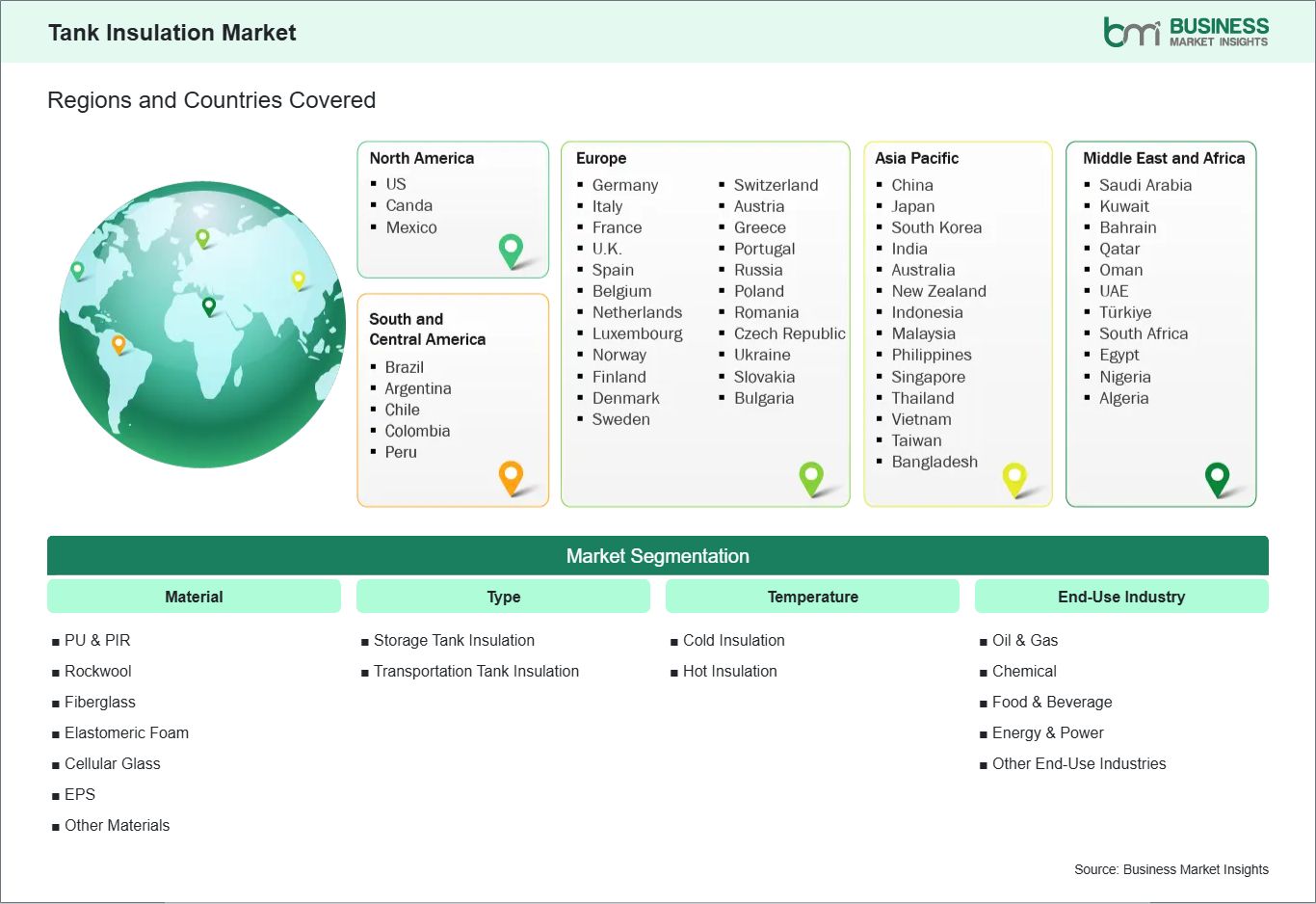

Key segments that contributed to the derivation of the tank insulation market analysis are material, type, temperature, and end‑use industry.

By material, the tank insulation market is segmented into PU & PIR, rockwool, fiberglass, elastomeric foam, cellular glass, EPS, other materials. The PU & PIR segment dominated the market in 2025.

Based on type, the tank insulation market is categorized into storage tank insulation, transportation tank insulation. The storage tank insulation segment dominated the market in 2025.

On the basis of temperature, the tank insulation market is categorized into cold insulation, hot insulation. The cold insulation segment dominated the market in 2025.

In terms of end‑use industry, the tank insulation market is categorized into oil & gas, chemical, food & beverage, energy & power, other end‑use industries. The oil & gas segment dominated the market in 2025.

Tank Insulation Market Drivers and Opportunities:

Rising Demand For Energy Efficiency In Industrial Storage Tanks

The global tank insulation market is increasingly driven by rising demand for energy efficiency in industrial storage tanks across multiple sectors, including oil & gas, chemical processing, power generation, and food & beverage. Industrial operations depend on insulated tanks because these tanks protect their stored materials from temperature changes, which lead to heat loss and higher energy costs. In refineries and petrochemical complexes, where large volumes of liquids must be heat‑managed 24/7, insulation helps reduce fuel consumption and improve process efficiency. This focus on operational cost savings and energy optimization has moved tank insulation from a "nice-to-have" to an essential component of sustainable industrial infrastructure.

The trend receives reinforcement from corporate sustainability commitments and energy policies, which European and North American countries enact. The regulatory frameworks in many mature markets now require facility owners to install advanced insulation systems or retrofit existing tanks because these systems deliver energy savings that meet environmental compliance standards. Insulation systems help facilities achieve efficiency targets while demonstrating lower carbon emissions, which supports their decarbonization efforts.

Across industries, insurers and safety regulators increasingly encourage or mandate insulation to prevent thermal shock, condensation, and surface temperature extremes that can compromise structural integrity or worker safety. This multi‑layered demand—financial, environmental, and safety‑driven—continues to propel investment in high‑performance insulation materials and engineered systems globally, underscoring energy efficiency as a core driver of market growth.

Expansion In Emerging Markets With Rapid Industrialization

The tank insulation market is experiencing notable expansion in emerging markets characterized by rapid industrialization, infrastructural development, and rising manufacturing output. In Asia Pacific, countries such as China, India, Vietnam, and Indonesia are scaling up refinery capacity, petrochemical hubs, and heavy industry, all of which require temperature‑specific storage solutions. As these economies invest in new industrial parks and storage facilities to support domestic demand and global export chains, the adoption of tank insulation becomes integral to construction and operational planning. These regions are increasingly moving beyond basic insulation to advanced engineered systems tailored to climatic and process needs.

Similarly, in parts of Latin America and the Middle East, expanding energy, water treatment, and agro‑processing sectors are creating opportunities for insulation solutions. Brazil and Mexico, for instance, are investing in modern chemical and biofuel infrastructure where thermal insulation enhances energy conservation and process reliability. The Middle East`s ongoing diversification from pure hydrocarbon exportation into petrochemicals and industrial chemicals also demands robust insulation systems to ensure product quality across extreme temperature ranges.

Government initiatives that promote industrial modernization and energy efficiency, coupled with foreign direct investment in manufacturing zones, are accelerating infrastructure projects that include insulated tank installations. Local suppliers are increasingly partnering with global insulation material producers to deliver cost‑effective solutions, further embedding tank insulation into emerging markets’ industrial expansion strategies.

Tank Insulation Market Size and Share Analysis:

The tank insulation market demonstrates steady growth, with size and share analysis highlighting evolving trends and competitive dynamics among key players. The report examines subsegments categorized within material, type, temperature, and end‑use industry, offering insights into their contribution to overall market performance.

By material, the PU & PIR subsegment dominated the market in 2025, driven by its superior thermal insulation, lightweight nature, and energy‑saving properties in tank applications.

Based on type, the storage tank insulation subsegment dominated the market in 2025, driven by high demand from stationary tanks in industries like oil, gas, and chemicals.

In terms of temperature, the cold insulation subsegment dominated the market in 2025, driven by the need to maintain low temperatures in LNG, cryogenic, and refrigerated storage applications.

On the basis of end‑use industry, the oil & gas subsegment dominated the market in 2025, driven by extensive use of insulated tanks for storage and handling of crude oil, LNG, and other hydrocarbon products.

Australia, China, India, Japan, South Korea, Indonesia, Malaysia, Philippines, Singapore, Thailand, Vietnam, Bangladesh, New Zealand, Taiwan

South and Central America

Brazil, Argentina, Peru, Chile, Colombia

Middle East and Africa

Bahrain, Kuwait, Oman, Qatar, Saudi Arabia, United Arab Emirates, Turkiye, South Africa, Egypt, Algeria, Nigeria

Market leaders and key company profiles

Rockwool International A/S

Owens Corning

Saint-Gobain

Kingspan Group

Armacell International S.A.

Cabot Corporation

Johns Manville

Knauf Insulation

BASF SE

Covestro AG

Get more information on this report

Tank Insulation Market Report Coverage and Deliverables:

The "Tank Insulation Market Size and Forecast (2022 - 2033)" report provides a detailed analysis of the market covering below areas:

Tank Insulation Market size and forecast at global, regional, and country levels for all the key market segments covered under the scope

Tank Insulation Market trends, as well as drivers, restraints, and opportunities

Tank Insulation Market analysis covering key trends, global and regional framework, major players, regulations, and recent developments

Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments for the Tank Insulation Market

Detailed company profiles, including SWOT analysis

Tank Insulation Market Geographic Insights:

The geographical scope of the Tank Insulation Market report is divided into North America, Asia Pacific, Europe, Middle East & Africa, and South & Central America. North America held the largest share in 2025.

North America stands as the leading region in the Tank Insulation Market because of its developed industrial facilities, its strict energy efficiency standards and its various uses in oil and gas, chemical, water treatment and food and beverage sectors. Refineries, petrochemical plants and food processing facilities in the United States and Canada utilize advanced insulation solutions such as fiberglass and mineral wool, polyurethane foams and elastomeric materials to construct their large-scale storage tanks, which help them maintain temperature control and prevent heat loss and guarantee operational safety. The implementation of energy conservation initiatives combined with emissions reduction programs creates a need for high-performance insulation systems, which will be used in both new tank installations and retrofitted tank projects.

The European market exists as a crucial area for thermal insulation, which chemical and industrial storage tanks employ in Germany, France and the UK because industrial modernization, environmental regulations and sustainable building practices create demand for this technology although material costs and complex installation requirements create occasional challenges.

The Asia Pacific region is experiencing fast development because industrial infrastructure develops through industrial growth in China, India and Southeast Asian nations. The adoption of tank insulation is driven by increasing demand for petrochemical storage facilities and rising energy awareness and investments in food and beverage and water treatment sectors, which require eco-friendly and cost-effective materials that work well in tropical climates.

The Middle Eastern and African market depends on oil and gas storage and processing facilities, which exist throughout the region but especially impact Saudi Arabia and UAE, and South Africa, where thermal insulation protects hydrocarbon assets under extreme temperature conditions.

The South and Central American market represents a developing market with Brazil, Argentina and Chile developing industrial storage and water treatment and energy systems, although their progress remains restricted because they lack sufficient funds and advanced materials.

The North American market maintains its lead in technology adoption and regulatory support, yet other regions start to identify tank insulation advantages, which drive energy efficiency and safety and operational benefits, thus expanding the worldwide market growth.

Get more information on this report

Tank Insulation Market Research Report Guidance:

The report includes qualitative and quantitative data in the Tank Insulation Market across material, type, temperature, end‑use industry and geography.

The report starts with the key takeaways (chapter 2), highlighting key trends and outlook of the Tank Insulation Market.

Chapter 3 focuses on the research methodology of the study.

Chapter 4 includes ecosystem analysis.

Chapter 5 highlights the major industry dynamics in the Tank Insulation Market, including factors that are driving the market, prevailing deterrents, potential opportunities, as well as future trends. Impact analysis of these drivers and restraints is also covered in this section.

Chapter 6 discusses the Tank Insulation Market scenario, in terms of historical market revenues, and forecast till the year 2033.

Chapters 7 to 11 cover Tank Insulation Market segments by material, type, temperature, end‑use industry and geography across North America, Asia Pacific, Europe, Middle East & Africa, and South & Central America. They cover the market revenue forecast and factors driving the market.

Chapter 12 describes the competitive analysis along with the heat map analysis for the key players operating in the market.

Chapter 13 describes the industry landscape analysis. It provides detailed descriptions of business activities such as market initiatives, new developments, mergers, and joint ventures globally, along with a competitive landscape.

Chapter 14 provides detailed profiles of the major companies operating in the Tank Insulation Market. Companies have been profiled on the basis of their key facts, business descriptions, products, financial overview, SWOT analysis, and key developments.

Chapter 15, i.e., the appendix, is inclusive of a brief overview of the company, a list of abbreviations, and a disclaimer.

Tank Insulation Market News and Key Development:

The Tank Insulation Market is evaluated by gathering qualitative and quantitative data post primary and secondary research, which includes important corporate publications, association data, and databases. A few of the key developments in the tank insulation market are:

In June 2025, Armacell announced that it opened a new aerogel insulation plant in India to manufacture its breakthrough ArmaGel XG product line, enhancing production capacity for advanced insulation materials used in industrial applications such as tank and vessel thermal protection.

In September 2025, Knauf Insulation, Inc. announced expanded investment in its Shelbyville, Indiana manufacturing facility, adding or upgrading production lines that support its pipe and tank insulation offerings as part of broader capacity enhancement and future‑ready manufacturing initiatives.

Key Sources Referred:

World Health Organization (WHO)Organisation for Economic Cooperation and Development (OECD)The World Bank GroupWorldometerThe LancetInternational Bar AssociationInternational Trade Administration

The List of Companies - Tank Insulation Market

Rockwool International A/S

Owens Corning

Saint-Gobain

Kingspan Group

Armacell International S.A.

Cabot Corporation

Johns Manville

Knauf Insulation

BASF SE

Covestro AG

About Author— Chemicals and Materials Research Team

Suraj Sajeev is a market research and consulting professional with nearly 10 years of experience across Life Sciences, Consumer Goods, Food & Beverages, Materials & Chemicals, and Automotive industries. Throughout his career, he has successfully managed and delivered custom market research and consulting engagements, enabling clients to make informed strategic decisions through actionable market intelligence.

Suraj has extensive expertise in end-to-end project management, including proposal development, market assessment, competitive intelligence, opportunity analysis, market sizing and forecasting, strategic recommendation..

Show More

Frequently Asked Questions

How big is the Tank Insulation Market?

The Tank Insulation Market is valued at US$ 7.1 Billion in 2025, it is projected to reach US$ 10.1 Billion by 2033.

What is the CAGR for Tank Insulation Market by (2026 - 2033)?

As per our report Tank Insulation Market, the market size is valued at US$ 7.1 Billion in 2025, projecting it to reach US$ 10.1 Billion by 2033. This translates to a CAGR of approximately 4.50% during the forecast period.

What segments are covered in this report?

The Tank Insulation Market report typically cover these key segments-

Material (PU & PIR, Rockwool, Fiberglass, Elastomeric Foam, Cellular Glass, EPS, Other Materials)

Type (Storage Tank Insulation, Transportation Tank Insulation)

Temperature (Cold Insulation, Hot Insulation)

End-Use Industry (Oil & Gas, Chemical, Food & Beverage, Energy & Power, Other End-Use Industries)

What is the historic period, base year, and forecast period taken for Tank Insulation Market?

The historic period, base year, and forecast period can vary slightly depending on the specific market research report. However, for the Tank Insulation Market report:

Historic Period : 2022-2024

Base Year : 2025

Forecast Period : 2026-2033

Who are the major players in Tank Insulation Market?

The Tank Insulation Market is populated by several key players, each contributing to its growth and innovation. Some of the major players include:

Rockwool International A/S

Owens Corning

Saint-Gobain

Kingspan Group

Armacell International S.A.

Cabot Corporation

Johns Manville

Knauf Insulation

BASF SE

Covestro AG

Who should buy this report?

The Tank Insulation Market report is valuable for diverse stakeholders, including:

Investors: Provides insights for investment decisions pertaining to market growth, companies, or industry insights. Helps assess market attractiveness and potential returns.

Industry Players: Offers competitive intelligence, market sizing, and trend analysis to inform strategic planning, product development, and sales strategies.

Suppliers and Manufacturers: Helps understand market demand for components, materials, and services related to concerned industry.

Researchers and Consultants: Provides data and analysis for academic research, consulting projects, and market studies.

Financial Institutions: Helps assess risks and opportunities associated with financing or investing in the concerned market.

Essentially, anyone involved in or considering involvement in the Tank Insulation Market value chain can benefit from the information contained in a comprehensive market report.

Get Free Sample For Tank Insulation Market

Get Free Sample For Tank Insulation Market