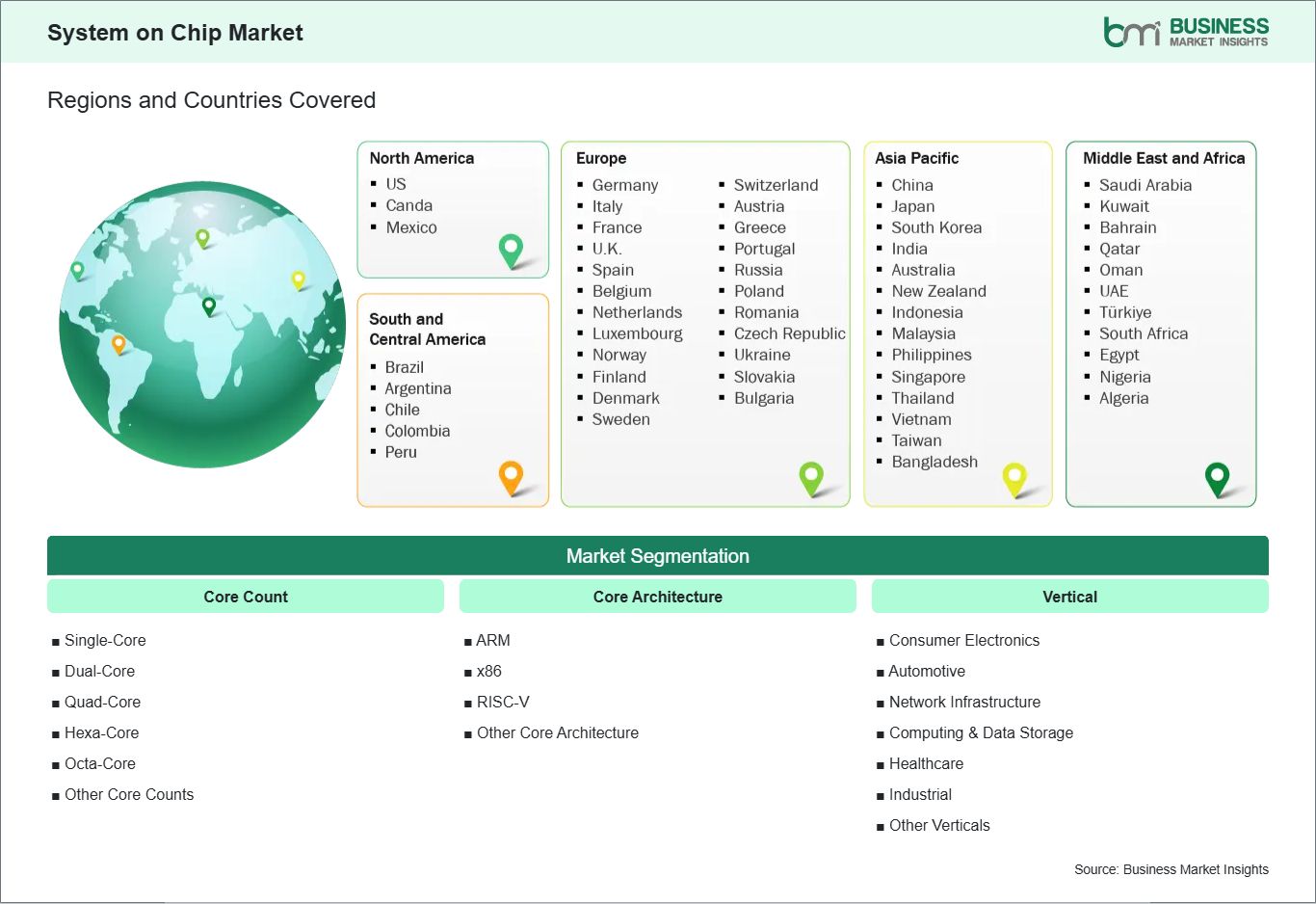

The geographical scope of the System‑on‑Chip Market report is divided into North America, Asia Pacific, Europe, Middle East & Africa, and South & Central America. North America held the largest share in 2025.

The global System‑on‑Chip market demonstrates distinct dynamics across regions, shaped by technological adoption, industrial priorities, and infrastructure development. North America leads in SoC design innovation, driven by strong R&D ecosystems, high adoption of AI and edge computing applications, and integration of SoCs into cloud infrastructure and autonomous systems.

Asia Pacific dominates production and manufacturing, with its robust electronics manufacturing ecosystem supporting mass deployment of mobile devices, IoT hardware, and telecommunication infrastructure, while rapid urbanization and digital transformation fuel demand for energy-efficient and multi-functional SoCs. Europe focuses on industrial automation, automotive electronics, and smart energy solutions, emphasizing functional safety, regulatory compliance, and domain-specific chip designs.

Middle East & Africa is emerging as a growth region for SoCs in telecommunications, smart city initiatives, and industrial monitoring, with rising investment in digital infrastructure creating new opportunities for low-power and cost-effective SoCs. South & Central America is witnessing gradual adoption of SoCs in automotive, consumer electronics, and industrial sectors, supported by localized manufacturing initiatives and increasing integration of connected devices.

Across all regions, the market is shaped by differing priorities: North America and Europe emphasize innovation and application-specific design, Asia Pacific leads in manufacturing scale, while Middle East, Africa, and South & Central America are focused on infrastructure-driven adoption, highlighting the global interdependence and strategic diversification within the SoC ecosystem.