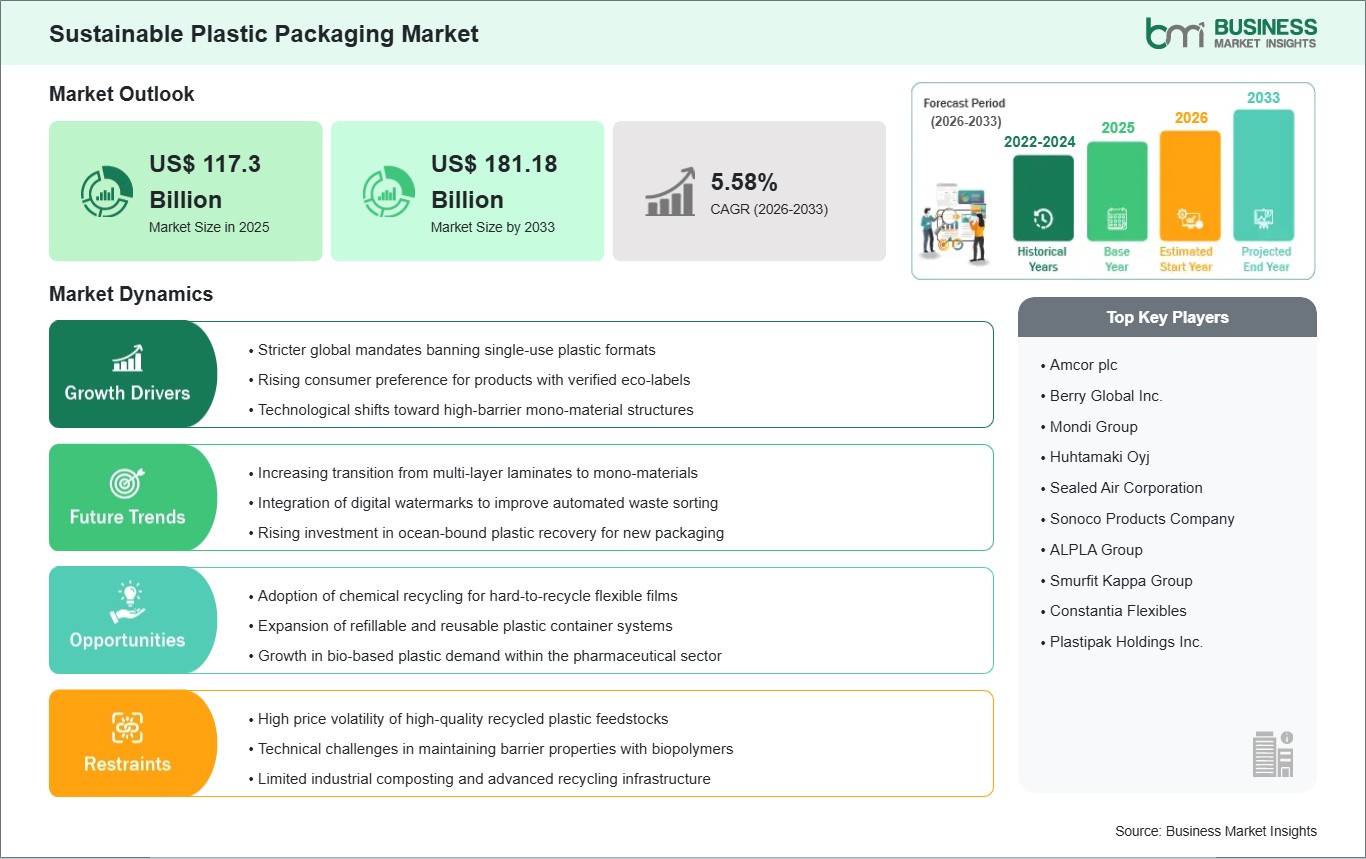

The Sustainable Plastic Packaging Market size is expected to reach US$ 181.18 billion by 2033 from US$ 117.3 billion in 2025. The market is estimated to record a CAGR of 5.58% from 2026 to 2033.

Executive Summary and Global Market Analysis:

The sustainable plastic packaging market is a central pillar of the global transition toward a circular economy, addressing the critical environmental impact of traditional petroleum-based polymers. This market focuses on the development and deployment of materials that are recyclable, reusable, or compostable, aiming to keep plastic waste out of landfills and oceans. Currently, the landscape is led by rigid packaging formats and recyclable processes, as these utilize existing waste management infrastructures more effectively than newer alternatives. The food and beverage sector remains the primary volume driver, as consumer goods companies face intense pressure to eliminate virgin plastics and adopt post-consumer recycled content to meet both regulatory mandates and public expectations.

In the realm of innovation in material science, there is a tremendous focus on the development of mono-material technologies and bio-based plastics like PLA and PHA. The market is currently faced with many challenges, such as the high cost of recycled materials and the need for better sorting technologies; nevertheless, the trend is clearly pointing towards a healthy growth rate. The promises of multinational corporations with regard to sustainable development have become a catalyst for the development of sophisticated recycling and refill technologies. As the market progresses into the future, the inclusion of digital technologies and the development of chemical recycling technologies will become the key to the success of the recycling loop. The market is now shifting from the traditional approach of reducing waste towards the development of a sustainable ecosystem for the regeneration of the environment.

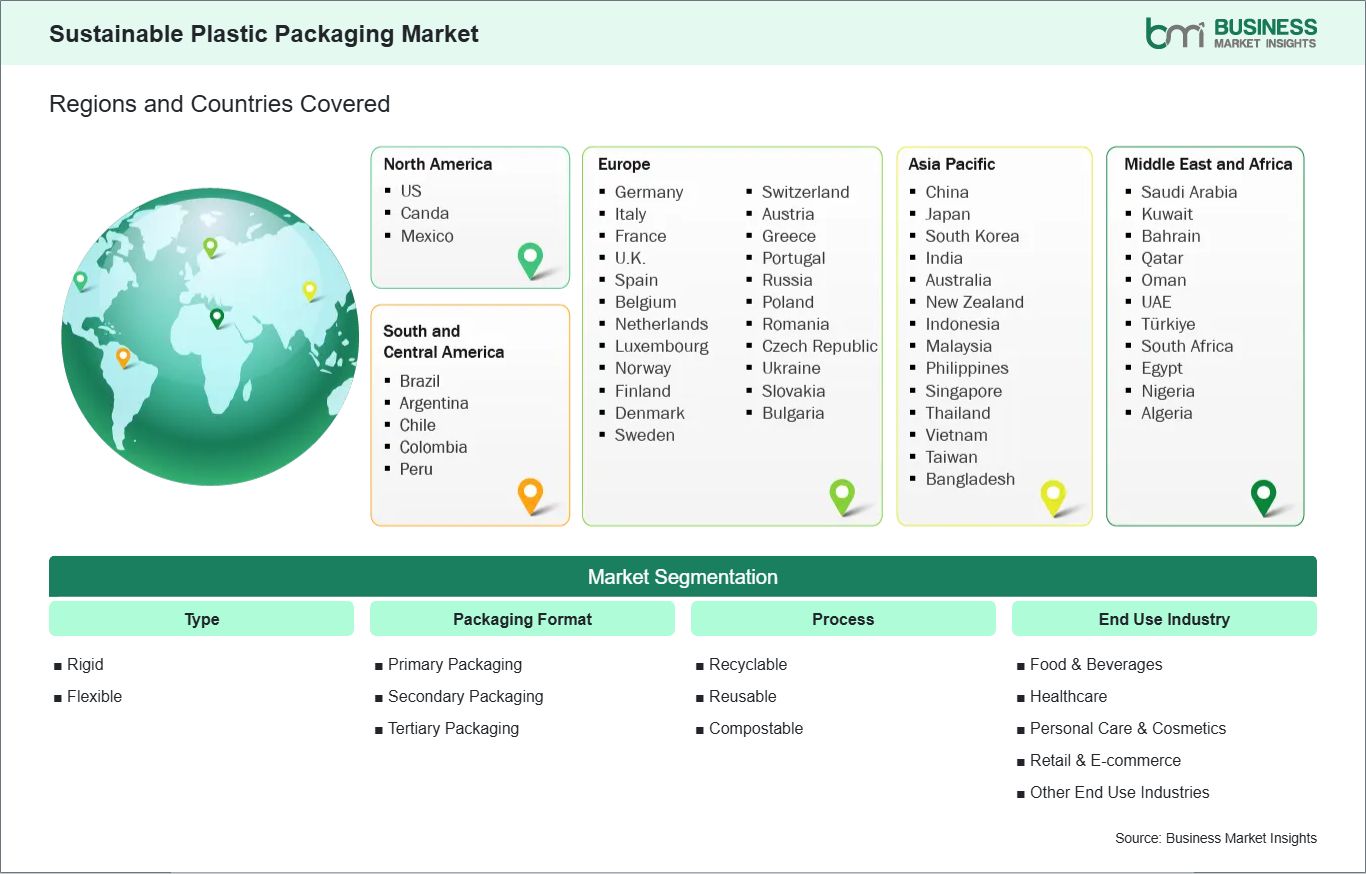

Key segments that contributed to the derivation of the Sustainable Plastic Packaging market analysis are type, packaging format, process, and end use industry.

By type, the sustainable plastic packaging market is segmented into Rigid and Flexible. The Rigid segment dominated the market in 2025.

By packaging format, the sustainable plastic packaging market is segmented into Primary Packaging, Secondary Packaging, and Tertiary Packaging. The Primary Packaging segment dominated the market in 2025.

By process, the sustainable plastic packaging market is segmented into Recyclable, Reusable, and Compostable. The Recyclable segment dominated the market in 2025.

By end use industry, the sustainable plastic packaging market is segmented into Food & Beverages, Healthcare, Personal Care & Cosmetics, Retail & E-commerce, and Others. The Food & Beverages segment dominated the market in 2025.

Sustainable Plastic Packaging Market Drivers and Opportunities:

Stricter global mandates banning single-use plastic formats

The biggest driver behind the growth of the sustainable plastic packaging industry are the numerous aggressive laws being established by many countries to help limit plastic waste throughout our environment. Each of those governments has moved past just having general recommendations for limiting plastic waste, and have added in legally-required restrictions against certain types of single-use products. These restrictions specifically target products like straws, plastic cutlery, and thin-film plastic bags, and now require that manufacturers provide an adequate amount of recycled content when producing new plastic products. Laws specifically requiring manufacturers to eliminate their use of non-recyclable materials will also create certainty and predictability, which will help to encourage companies to invest in long-term sustainable material science and processing technology.

Additionally, extended producer responsibility schemes are being expanded to hold brand owners financially accountable for the end-of-life management of their packaging. This shift shifts the economic burden of waste collection and processing onto the producers, incentivizing the design of packaging that is easier and cheaper to recycle. As these regulations harmonize across international borders, companies are adopting global sustainability standards to simplify their supply chains. This legislative push ensures that the transition to sustainable plastics is not merely a voluntary marketing trend but a core requirement for maintaining market access and avoiding heavy non-compliance penalties in a rapidly tightening global trade landscape.

Adoption of chemical recycling for hard-to-recycle flexible films

The commercialization and expansion of chemical recycling (also known as advanced recycling), especially for complex flexible plastic waste, presents a significant opportunity for growth. Mechanical recycling generally does not work well with multi-layer films and contaminated plastics; therefore, mechanically recycled plastics are not able to be used in making food-grade products because mechanically recycled plastics are of lower-quality than virgin-grade plastics. The use of chemical recycling allows plastic to be broken down into its original molecular building blocks, producing virgin-quality polymer resins from feedstock materials that can create circular flexible packaging formats that had previously been considered non-recyclable. It opens up a new large source of high-value feedstock for the packaging industry.

As major chemical companies and packaging converters form strategic partnerships to build large-scale advanced recycling facilities, the availability of chemically recycled resins is expected to surge. This development is particularly crucial for the food and healthcare industries, where strict hygiene and safety standards demand the highest material purity. By utilizing these advanced resins, brands can meet their 100 percent recyclability pledges without compromising on the barrier properties or shelf-life extension provided by traditional plastics. The ability to process mixed plastic waste into high-performing packaging materials represents a frontier that can significantly decouple plastic production from fossil fuel extraction while addressing the persistent challenge of flexible plastic pollution.

Sustainable Plastic Packaging Market Size and Share Analysis:

The global Sustainable Plastic Packaging market is experiencing steady growth, with market size and share analysis reflecting evolving treatment preferences and competitive dynamics among key players. The report evaluates important subsegments categorized within type, packaging format, process, and end use industry, highlighting their respective contributions to overall market performance.

By type, the Rigid subsegment dominated the market in 2025 due to its superior structural integrity and high protection levels for liquid products, allowing for a higher integration of post-consumer recycled resins while maintaining the durability required for heavy-duty applications.

By packaging format, the Primary Packaging subsegment dominated the market in 2025 due to its direct contact with products, where the urgency to replace virgin plastics with food-grade recycled materials or bioplastics is highest to meet safety standards.

By process, the Recyclable subsegment dominated the market in 2025 as it leverages well-established global collection and sorting infrastructures, making it the most scalable and cost-effective pathway for brands to achieve immediate circularity goals compared to emerging composting systems.

By end use industry, the Food & Beverages subsegment dominated the market in 2025 because of the massive scale of daily consumer goods consumption and the intense regulatory pressure to eliminate single-use plastics in favor of sustainable alternatives like rPET bottles.

Australia, China, India, Japan, South Korea, Indonesia, Malaysia, Philippines, Singapore, Thailand, Vietnam, Bangladesh, New Zealand, Taiwan

South and Central America

Brazil, Argentina, Peru, Chile, Colombia

Middle East and Africa

Bahrain, Kuwait, Oman, Qatar, Saudi Arabia, United Arab Emirates, Turkiye, South Africa, Egypt, Algeria, Nigeria

Market leaders and key company profiles

Amcor plc

Berry Global Inc.

Mondi Group

Huhtamaki Oyj

Sealed Air Corporation

Sonoco Products Company

ALPLA Group

Smurfit Kappa Group

Constantia Flexibles

Plastipak Holdings Inc.

Get more information on this report

Sustainable Plastic Packaging Market Report Coverage and Deliverables:

The "Sustainable Plastic Packaging Market Size and Forecast (2022 - 2033)" report provides a detailed analysis of the market covering below areas:

Sustainable Plastic Packaging market size and forecast at the regional and country levels for segments covered under the scope

Sustainable Plastic Packaging market trends, as well as drivers, restraints, and opportunities

Sustainable Plastic Packaging market analysis covering key trends, regional framework, major players, regulations, and recent developments

Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments for the Sustainable Plastic Packaging market

Detailed company profiles, including SWOT analysis

The geographical scope of the Sustainable Plastic Packaging market report is divided into: North America, Asia Pacific, Europe, Middle East & Africa, and South & Central America. North America held the largest share in 2025.

North America leads the sustainable plastic packaging market, a position established through its advanced manufacturing capabilities and the high concentration of major global consumer packaged goods companies. The region dominance is particularly strong in the United States, where a sophisticated retail landscape and mature e-commerce sector drive massive demand for innovative packaging solutions. Large-scale investments in recycling infrastructure and the early adoption of high-performance recycled resins have allowed North American manufacturers to set global benchmarks for sustainable design.

Furthermore, the presence of leading material science firms and a strong venture capital ecosystem facilitates the rapid commercialization of new bioplastics and chemical recycling technologies. The regional market is also characterized by a proactive shift among major brands to incorporate high levels of post-consumer recycled content in response to both state-level legislation and shifting consumer values. Initiatives like the U.S. Plastics Pact have unified various stakeholders across the value chain, creating a coordinated effort to improve recyclability and reduce plastic waste. While other regions are seeing rapid growth, North America remains the primary hub for high-value sustainable plastic applications, particularly in the healthcare and premium food segments.

The region emphasis on technological integration, such as smart labels for waste sorting and automated recovery systems, ensures it stays at the forefront of the global industry. As supply chains for renewable feedstocks continue to stabilize, North America is poised to maintain its market leadership through enhanced operational efficiency and technical innovation.

Get more information on this report

Sustainable Plastic Packaging Market Research Report Guidance:

The report includes qualitative and quantitative data in the Sustainable Plastic Packaging market across type, packaging format, process, end use industry, and geography.

The report starts with the key takeaways (chapter 2), highlighting the key trends and outlook of the Sustainable Plastic Packaging market.

Chapter 3 focuses on the research methodology of the study.

Chapter 4 includes ecosystem analysis.

Chapter 5 highlights the major industry dynamics in the Sustainable Plastic Packaging market, including factors that are driving the market, prevailing deterrents, potential opportunities, as well as future trends. Impact analysis of these drivers and restraints is also covered in this section.

Chapter 6 discusses the Sustainable Plastic Packaging market scenario, in terms of historical market revenues, and forecast till the year 2033.

Chapters 7 to 11 cover the Sustainable Plastic Packaging market segments by type, packaging format, process, end use industry, and geography across North America, Europe, Asia Pacific, the Middle East and Africa, and South and Central America. They cover the market revenue, forecast, and factors driving the market.

Chapter 12 describes the competitive analysis along with the heat map analysis for the key players operating in the market.

Chapter 13 describes the industry landscape analysis. It provides detailed descriptions of business activities such as market initiatives, new developments, mergers, and joint ventures globally, along with a competitive landscape.

Chapter 14 provides detailed profiles of the major companies operating in the Sustainable Plastic Packaging market. Companies have been profiled on the basis of their key facts, business descriptions, products, financial overview, SWOT analysis, and key developments.

Chapter 15, i.e., the appendix, is inclusive of a brief overview of the company, list of abbreviations, and disclaimer.

Sustainable Plastic Packaging Market News and Key Development:

The Sustainable Plastic Packaging market is evaluated by gathering qualitative and quantitative data post primary and secondary research, which includes important corporate publications, association data, and databases. A few of the key developments in the Sustainable Plastic Packaging market are:

In November 2025, Amcor announced that it had expanded its sustainable plastic packaging portfolio by launching new high-barrier recyclable films for food and healthcare applications, designed to reduce carbon footprint while maintaining product safety.

In July 2024, Berry Global announced that it had introduced a new line of sustainable plastic packaging solutions incorporating post-consumer recycled (PCR) content, targeting e-commerce and fast-moving consumer goods markets.

In March 2023, Sealed Air announced that it had rolled out eco-friendly plastic packaging innovations under its SEE Sustainable Packaging program, focusing on lightweight recyclable films and reduced material usage.

Key Sources Referred:

WPO (World Packaging Organisation)SPC (Sustainable Packaging Coalition)FPA (Flexible Packaging Association)PMMI (The Association for Packaging and Processing Technologies)FEFCO (European Federation of Corrugated Board Manufacturers)AIPIA (Active & Intelligent Packaging Industry Association)IAPRI (International Association of Packaging Research Institutes)APR (Association of Plastic Recyclers)GPI (Glass Packaging Institute)Company WebsitesCompany Annual ReportsCompany Investor Presentations

The List of Companies - Sustainable Plastic Packaging Market

Amcor plc

Berry Global Inc.

Mondi Group

Huhtamaki Oyj

Sealed Air Corporation

Sonoco Products Company

ALPLA Group

Smurfit Kappa Group

Constantia Flexibles

Plastipak Holdings Inc.

About Author— Chemicals and Materials Research Team

Suraj Sajeev is a market research and consulting professional with nearly 10 years of experience across Life Sciences, Consumer Goods, Food & Beverages, Materials & Chemicals, and Automotive industries. Throughout his career, he has successfully managed and delivered custom market research and consulting engagements, enabling clients to make informed strategic decisions through actionable market intelligence.

Suraj has extensive expertise in end-to-end project management, including proposal development, market assessment, competitive intelligence, opportunity analysis, market sizing and forecasting, strategic recommendation..

Frequently Asked Questions

How big is the Sustainable Plastic Packaging Market?

The Sustainable Plastic Packaging Market is valued at US$ 117.3 Billion in 2025, it is projected to reach US$ 181.18 Billion by 2033.

What is the CAGR for Sustainable Plastic Packaging Market by (2026 - 2033)?

As per our report Sustainable Plastic Packaging Market, the market size is valued at US$ 117.3 Billion in 2025, projecting it to reach US$ 181.18 Billion by 2033. This translates to a CAGR of approximately 5.58% during the forecast period.

What segments are covered in this report?

The Sustainable Plastic Packaging Market report typically cover these key segments-

Type (Rigid, Flexible)

Packaging Format (Primary Packaging, Secondary Packaging, Tertiary Packaging)

Process (Recyclable, Reusable, Compostable)

End Use Industry (Food & Beverages, Healthcare, Personal Care & Cosmetics, Retail & E-commerce, Other End Use Industries)

What is the historic period, base year, and forecast period taken for Sustainable Plastic Packaging Market?

The historic period, base year, and forecast period can vary slightly depending on the specific market research report. However, for the Sustainable Plastic Packaging Market report:

Historic Period : 2022-2024

Base Year : 2025

Forecast Period : 2026-2033

Who are the major players in Sustainable Plastic Packaging Market?

The Sustainable Plastic Packaging Market is populated by several key players, each contributing to its growth and innovation. Some of the major players include:

Amcor plc

Berry Global Inc.

Mondi Group

Huhtamaki Oyj

Sealed Air Corporation

Sonoco Products Company

ALPLA Group

Smurfit Kappa Group

Constantia Flexibles

Plastipak Holdings Inc.

Who should buy this report?

The Sustainable Plastic Packaging Market report is valuable for diverse stakeholders, including:

Investors: Provides insights for investment decisions pertaining to market growth, companies, or industry insights. Helps assess market attractiveness and potential returns.

Industry Players: Offers competitive intelligence, market sizing, and trend analysis to inform strategic planning, product development, and sales strategies.

Suppliers and Manufacturers: Helps understand market demand for components, materials, and services related to concerned industry.

Researchers and Consultants: Provides data and analysis for academic research, consulting projects, and market studies.

Financial Institutions: Helps assess risks and opportunities associated with financing or investing in the concerned market.

Essentially, anyone involved in or considering involvement in the Sustainable Plastic Packaging Market value chain can benefit from the information contained in a comprehensive market report.

Get Free Sample For Sustainable Plastic Packaging Market

Get Free Sample For Sustainable Plastic Packaging Market