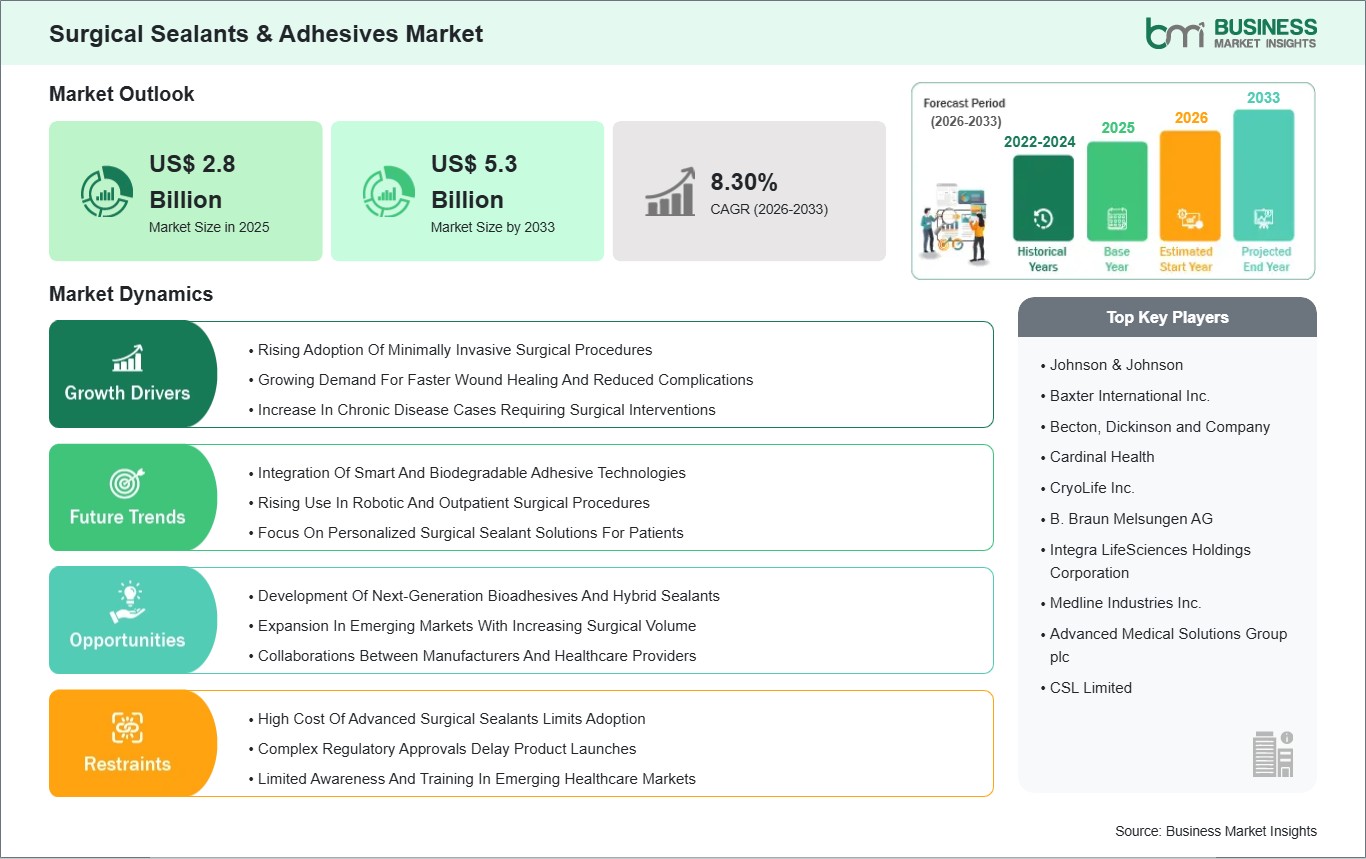

The Surgical Sealants & Adhesives Market size is expected to reach US$ 5.3 billion by 2033 from US$ 2.8 billion in 2025. The market is estimated to record a CAGR of 8.30% from 2026 to 2033.

Executive Summary and Global Market Analysis:

The worldwide market for surgical sealants and adhesives is experiencing fast growth because healthcare systems across different countries now focus on achieving better surgical results and protecting patients while improving the efficiency of their medical procedures. Surgical sealants and adhesives are specialized biomaterials used to close wounds and prevent blood or fluid leaks while they support tissue repair and eliminate the need for standard sutures and staples. The materials, which include synthetic glues and biologic sealants and fibrin‑based products and cyanoacrylate adhesives have essential functions in various surgical procedures, which include cardiovascular, orthopedic, general and plastic and minimally invasive surgeries. The medical community uses these technologies because of their rising surgical demands and their progress in robotic and minimally invasive techniques, which enable quicker patient recovery while minimizing infection danger.

The market experiences its main growth driver because hospitals require advanced sealing technologies, which provide both effective performance and tissue-safe solutions for their need to treat more patients through minimally invasive surgical methods. The use of synthetic adhesives or combination sealant systems in laparoscopic, endoscopic and robotic surgeries leads to better surgical results because these systems enable surgeons to perform their tasks with more accuracy while decreasing both blood loss and postoperative complications. Patients and clinicians are looking for solutions that enable patients to recover faster while needing fewer medical appointments especially in outpatient and day-care surgical facilities.

The increasing number of people with chronic conditions such as diabetes and vascular diseases has resulted in more complex surgical procedures, which create a greater need for dependable technologies that handle tissue closure and fluid management. The market has established constraints that restrict its operation. The high costs of products together with difficulties in obtaining reimbursement create barriers that prevent adoption in resource-limited environments where healthcare funding faces restrictions and existing closure techniques remain dominant. The regulatory process for new biological products and combination products requires multiple steps, which consume significant time to complete resulting in product launch delays that affect specific markets. Surgeon training and their ability to use advanced adhesive technologies create differences in hospitals and surgical centers regarding their rates of technology adoption.

The field faces obstacles; however, new technologies create clinical applications that include next-generation bioadhesives and hybrid sealant systems and smart materials that have better biocompatibility. Medical device companies, material scientists and surgical practitioners work together to speed up product development while they work on developing application protocols. Surgical sealants and adhesives will become essential components of contemporary surgical procedures throughout the world as healthcare delivery systems shift to value-based care that prioritizes better patient outcomes.

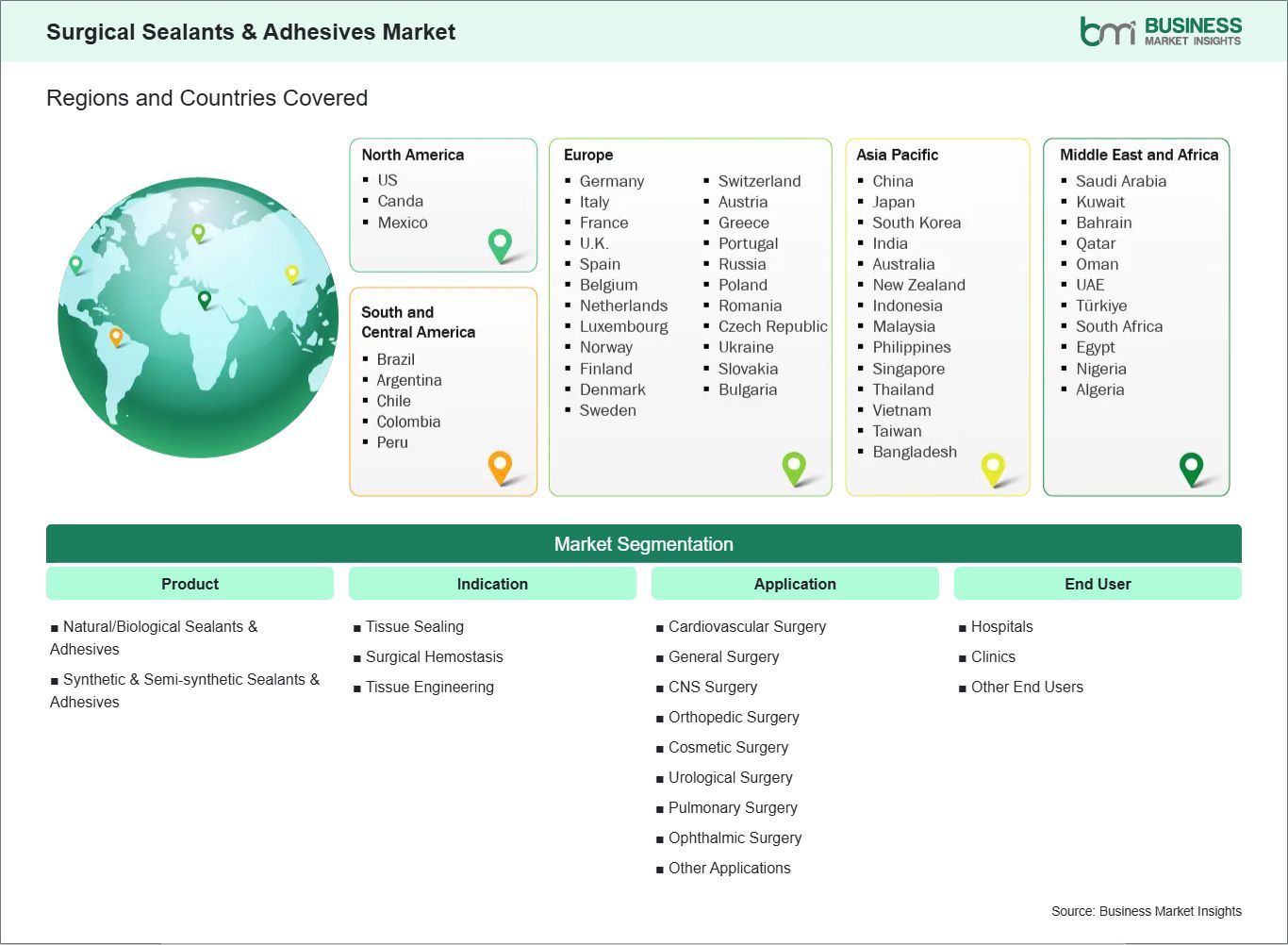

Key segments that contributed to the derivation of the surgical sealants & adhesives market analysis are product, indication, application, and end user.

By product, the surgical sealants & adhesives market is segmented into natural/biological sealants & adhesives, synthetic & semi‑synthetic sealants & adhesives. The synthetic & semi‑synthetic sealants & adhesives segment dominated the market in 2025.

Based on indication, the surgical sealants & adhesives market is categorized into tissue sealing, surgical hemostasis, tissue engineering. The surgical hemostasis segment dominated the market in 2025.

On the basis of application, the surgical sealants & adhesives market is categorized into cardiovascular surgery, general surgery, CNS surgery, orthopedic surgery, cosmetic surgery, urological surgery, pulmonary surgery, ophthalmic surgery, other applications. The general surgery segment dominated the market in 2025.

In terms of end user, the surgical sealants & adhesives market is categorized into hospitals, clinics, other end users. The hospitals segment dominated the market in 2025.

Surgical Sealants & Adhesives Market Drivers and Opportunities:

Rising Adoption Of Minimally Invasive Surgical Procedures

The global surgical sealants and adhesives market is significantly propelled by the rising adoption of minimally invasive surgical (MIS) procedures across healthcare systems worldwide. MIS techniques—such as laparoscopy, endoscopy, and robot‑assisted surgeries—are preferred due to reduced postoperative pain, quicker recovery, and shorter hospital stays compared with traditional open surgeries. These procedures often involve small incisions and complex internal maneuvers, creating a demand for advanced sealants and adhesives that can reliably close tissue gaps, control bleeding, and reinforce sutures in hard‑to‑access areas without extensive manipulation.

In cardiovascular surgery, for example, sealants are used to prevent blood leakage at arteriotomy sites during catheter‑based interventions. In gastrointestinal and bariatric procedures, adhesives assist in securing stapled tissue lines to minimize leakage and promote healing. The growing global focus on outpatient and day‑care surgical models further heightens the need for tissue closure solutions that support efficient workflows and reduce complication risks, especially where rapid sealing performance directly influences procedural success.

Geographically, regions with strong adoption of MIS—such as North America and Europe—are leading demand for surgical sealants and adhesives. Meanwhile, emerging markets in Asia‑Pacific and Latin America are rapidly embracing minimally invasive platforms as investments in healthcare infrastructure increase. As surgeons and healthcare providers continue prioritizing less invasive techniques, the need for reliable sealing and adhesion technologies remains a key driver of market growth worldwide.

Development Of Next‑Generation Bioadhesives And Hybrid Sealants

Innovation in next‑generation bioadhesives and hybrid sealants is transforming the global surgical sealants and adhesives market by delivering enhanced performance, biocompatibility, and broader clinical applicability. Traditional products such as fibrin‑based sealants and cyanoacrylate adhesives have long served general tissue closure needs, but evolving surgical practices demand materials that offer stronger adhesion, reduced inflammatory response, and improved integration with living tissues. Bioadhesives developed from natural polymers and peptide‑based systems mimic biological adhesion mechanisms, enabling stronger bonds and reduced risk of adverse reactions.

Hybrid sealants that combine synthetic polymers with biologically derived components are also gaining traction. These products aim to deliver the mechanical strength of synthetic materials with the biocompatibility of natural compounds, making them suitable for complex surgical scenarios like vascular repair or nerve attachment. Researchers and manufacturers are also exploring stimuli‑responsive adhesives that activate upon exposure to body temperature or pH changes, improving handling and precision during surgery.

Collaborations between biomaterials scientists, surgical device developers, and academic institutions worldwide are accelerating commercialization of these advanced materials. North America and Europe remain innovation hubs, but Asia‑Pacific is rapidly scaling research initiatives in bioadhesive technologies. As clinical demand grows for versatile, strong, and patient‑friendly sealing solutions, next‑generation bioadhesives and hybrid systems are poised to redefine surgical closure practices globally.

Surgical Sealants & Adhesives Market Size and Share Analysis:

The surgical sealants & adhesives market demonstrates steady growth, with size and share analysis highlighting evolving trends and competitive dynamics among key players. The report examines subsegments categorized within product, indication, application, and end user, offering insights into their contribution to overall market performance.

By product, the synthetic & semi‑synthetic sealants & adhesives subsegment dominated the market in 2025, driven by their reproducible quality, broad compatibility, and strong performance across surgical procedures.

Based on indication, the surgical hemostasis subsegment dominated the market in 2025, driven by high clinical need to control bleeding effectively in a majority of surgical interventions.

In terms of application, the general surgery subsegment dominated the market in 2025, driven by the high volume of general surgical procedures worldwide that routinely use sealants and adhesives.

On the basis of end user, the hospitals subsegment dominated the market in 2025, driven by the concentration of complex and high-volume surgeries performed in hospital settings compared to clinics or other facilities.

Australia, China, India, Japan, South Korea, Indonesia, Malaysia, Philippines, Singapore, Thailand, Vietnam, Bangladesh, New Zealand, Taiwan

South and Central America

Brazil, Argentina, Peru, Chile, Colombia

Middle East and Africa

Bahrain, Kuwait, Oman, Qatar, Saudi Arabia, United Arab Emirates, Turkiye, South Africa, Egypt, Algeria, Nigeria

Market leaders and key company profiles

Johnson & Johnson

Baxter International Inc.

Becton, Dickinson and Company

Cardinal Health

CryoLife Inc.

B. Braun Melsungen AG

Integra LifeSciences Holdings Corporation

Medline Industries Inc.

Advanced Medical Solutions Group plc

CSL Limited

Get more information on this report

Surgical Sealants & Adhesives Market Report Coverage and Deliverables:

The "Surgical Sealants & Adhesives Market Size and Forecast (2022 - 2033)" report provides a detailed analysis of the market covering below areas:

Surgical Sealants & Adhesives Market size and forecast at global, regional, and country levels for all the key market segments covered under the scope

Surgical Sealants & Adhesives Market trends, as well as drivers, restraints, and opportunities

Surgical Sealants & Adhesives Market analysis covering key trends, global and regional framework, major players, regulations, and recent developments

Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments for the Surgical Sealants & Adhesives Market

Detailed company profiles, including SWOT analysis

The geographical scope of the Surgical Sealants & Adhesives Market report is divided into North America, Asia Pacific, Europe, Middle East & Africa, and South & Central America. North America held the largest share in 2025.

North America serves as the main center of the worldwide surgical sealants and adhesives market because its healthcare system operates at high standards, and it adopts new surgical technologies before other regions and conducts more surgical operations than any other area. The combination of established reimbursement systems and scientific evidence, which shows that surgical sealants and adhesives improve results for patients after cardiovascular orthopedic general and minimally invasive surgeries United States and Canada leads to their widespread application. Advanced adhesive systems together with combination sealant systems now form part of standard operating procedures that hospitals and surgical centers use to achieve quicker patient recovery results and decrease both surgical complications and hospital duration. The combination of leading medical device firms and their dedication to research and development funding creates a situation where product development continues, and new bioadhesives and hybrid sealant systems reach the market at a fast pace.

The adoption of surgical sealants in Asia Pacific countries such as China India, and Japan experiences growth through their rising surgical operations, developing healthcare infrastructure and their expanding healthcare spending. The growth of minimally invasive procedures together with higher understanding about postoperative surgical complications leads hospitals to adopt better tissue closure technologies, which they particularly use in urban hospitals and tertiary care facilities. The healthcare systems in Germany France, and the UK show high adoption because these countries possess both regulatory systems that support innovation and strong clinical research backing their public and private healthcare facilities.

European surgeons now choose bio-based adhesives for their cardiovascular and orthopedic work because these materials have received clinical validation for improved patient outcomes and operational efficiency.

The Middle East, Africa and South America are starting to adopt surgical sealants and adhesives because healthcare infrastructure development and new surgical centers and advanced surgical technology awareness are growing. The United Arab Emirates and Saudi Arabia are developing their surgical services to deliver high-quality care while implementing modern adhesive solutions for cardiovascular and cosmetic procedures. The growth of private hospitals in Brazil and Argentina enables the use of advanced adhesives for complex surgeries, which helps reduce complications and accelerate recovery.

Get more information on this report

Surgical Sealants & Adhesives Market Research Report Guidance:

The report includes qualitative and quantitative data in the Surgical Sealants & Adhesives Market across product, indication, application, end user and geography.

The report starts with the key takeaways (chapter 2), highlighting key trends and outlook of the Surgical Sealants & Adhesives Market.

Chapter 3 focuses on the research methodology of the study.

Chapter 4 includes ecosystem analysis.

Chapter 5 highlights the major industry dynamics in the Surgical Sealants & Adhesives Market, including factors that are driving the market, prevailing deterrents, potential opportunities, as well as future trends. Impact analysis of these drivers and restraints is also covered in this section.

Chapter 6 discusses the Surgical Sealants & Adhesives Market scenario, in terms of historical market revenues, and forecast till the year 2033.

Chapters 7 to 11 cover Surgical Sealants & Adhesives Market segments by product, indication, application, end user and geography across North America, Asia Pacific, Europe, Middle East & Africa, and South & Central America. They cover the market revenue forecast and factors driving the market.

Chapter 12 describes the competitive analysis along with the heat map analysis for the key players operating in the market.

Chapter 13 describes the industry landscape analysis. It provides detailed descriptions of business activities such as market initiatives, new developments, mergers, and joint ventures globally, along with a competitive landscape.

Chapter 14 provides detailed profiles of the major companies operating in the Surgical Sealants & Adhesives Market. Companies have been profiled on the basis of their key facts, business descriptions, products, financial overview, SWOT analysis, and key developments.

Chapter 15, i.e., the appendix, is inclusive of a brief overview of the company, a list of abbreviations, and a disclaimer.

Surgical Sealants & Adhesives Market News and Key Development:

The Surgical Sealants & Adhesives Market is evaluated by gathering qualitative and quantitative data post primary and secondary research, which includes important corporate publications, association data, and databases. A few of the key developments in the surgical sealants & adhesives market are:

In November 2023, Ethicon, a Johnson & Johnson MedTech company, announced that it received CE Mark approval for its new ETHIZIA™ Hemostatic Sealing Patch, an advanced adjunctive hemostat designed to control difficult‑to‑stop bleeding in internal surgeries. The ETHIZIA™ patch, developed with unique synthetic polymer technology, can be molded, trimmed, and applied in both open and minimally invasive procedures, and the company indicated planned roll‑outs in key markets including EMEA, North America, Asia Pacific, and Latin America following regulatory clearances.

In May 2023, Advanced Medical Solutions Group announced continued global adoption and regulatory progress for its LiquiBand® and TissuGlu® adhesive technologies, highlighting their increasing use in surgical wound closure and internal tissue bonding applications across multiple regions.

Key Sources Referred:

World Health Organization (WHO)Organisation for Economic Cooperation and Development (OECD)The World Bank GroupWorldometerThe LancetInternational Bar AssociationInternational Trade Administration

The List of Companies - Surgical Sealants & Adhesives Market

Johnson & Johnson

Baxter International Inc.

Becton, Dickinson and Company

Cardinal Health

CryoLife Inc.

B. Braun Melsungen AG

Integra LifeSciences Holdings Corporation

Medline Industries Inc.

Advanced Medical Solutions Group plc

CSL Limited

Frequently Asked Questions

How big is the Surgical Sealants & Adhesives Market?

The Surgical Sealants & Adhesives Market is valued at US$ 2.8 Billion in 2025, it is projected to reach US$ 5.3 Billion by 2033.

What is the CAGR for Surgical Sealants & Adhesives Market by (2026 - 2033)?

As per our report Surgical Sealants & Adhesives Market, the market size is valued at US$ 2.8 Billion in 2025, projecting it to reach US$ 5.3 Billion by 2033. This translates to a CAGR of approximately 8.30% during the forecast period.

What segments are covered in this report?

The Surgical Sealants & Adhesives Market report typically cover these key segments-

Application (Cardiovascular Surgery, General Surgery, CNS Surgery, Orthopedic Surgery, Cosmetic Surgery, Urological Surgery, Pulmonary Surgery, Ophthalmic Surgery, Other Applications)

End User (Hospitals, Clinics, Other End Users)

What is the historic period, base year, and forecast period taken for Surgical Sealants & Adhesives Market?

The historic period, base year, and forecast period can vary slightly depending on the specific market research report. However, for the Surgical Sealants & Adhesives Market report:

Historic Period : 2022-2024

Base Year : 2025

Forecast Period : 2026-2033

Who are the major players in Surgical Sealants & Adhesives Market?

The Surgical Sealants & Adhesives Market is populated by several key players, each contributing to its growth and innovation. Some of the major players include:

Johnson & Johnson

Baxter International Inc.

Becton, Dickinson and Company

Cardinal Health

CryoLife Inc.

B. Braun Melsungen AG

Integra LifeSciences Holdings Corporation

Medline Industries Inc.

Advanced Medical Solutions Group plc

CSL Limited

Who should buy this report?

The Surgical Sealants & Adhesives Market report is valuable for diverse stakeholders, including:

Investors: Provides insights for investment decisions pertaining to market growth, companies, or industry insights. Helps assess market attractiveness and potential returns.

Industry Players: Offers competitive intelligence, market sizing, and trend analysis to inform strategic planning, product development, and sales strategies.

Suppliers and Manufacturers: Helps understand market demand for components, materials, and services related to concerned industry.

Researchers and Consultants: Provides data and analysis for academic research, consulting projects, and market studies.

Financial Institutions: Helps assess risks and opportunities associated with financing or investing in the concerned market.

Essentially, anyone involved in or considering involvement in the Surgical Sealants & Adhesives Market value chain can benefit from the information contained in a comprehensive market report.

Get Free Sample For Surgical Sealants & Adhesives Market

Get Free Sample For Surgical Sealants & Adhesives Market