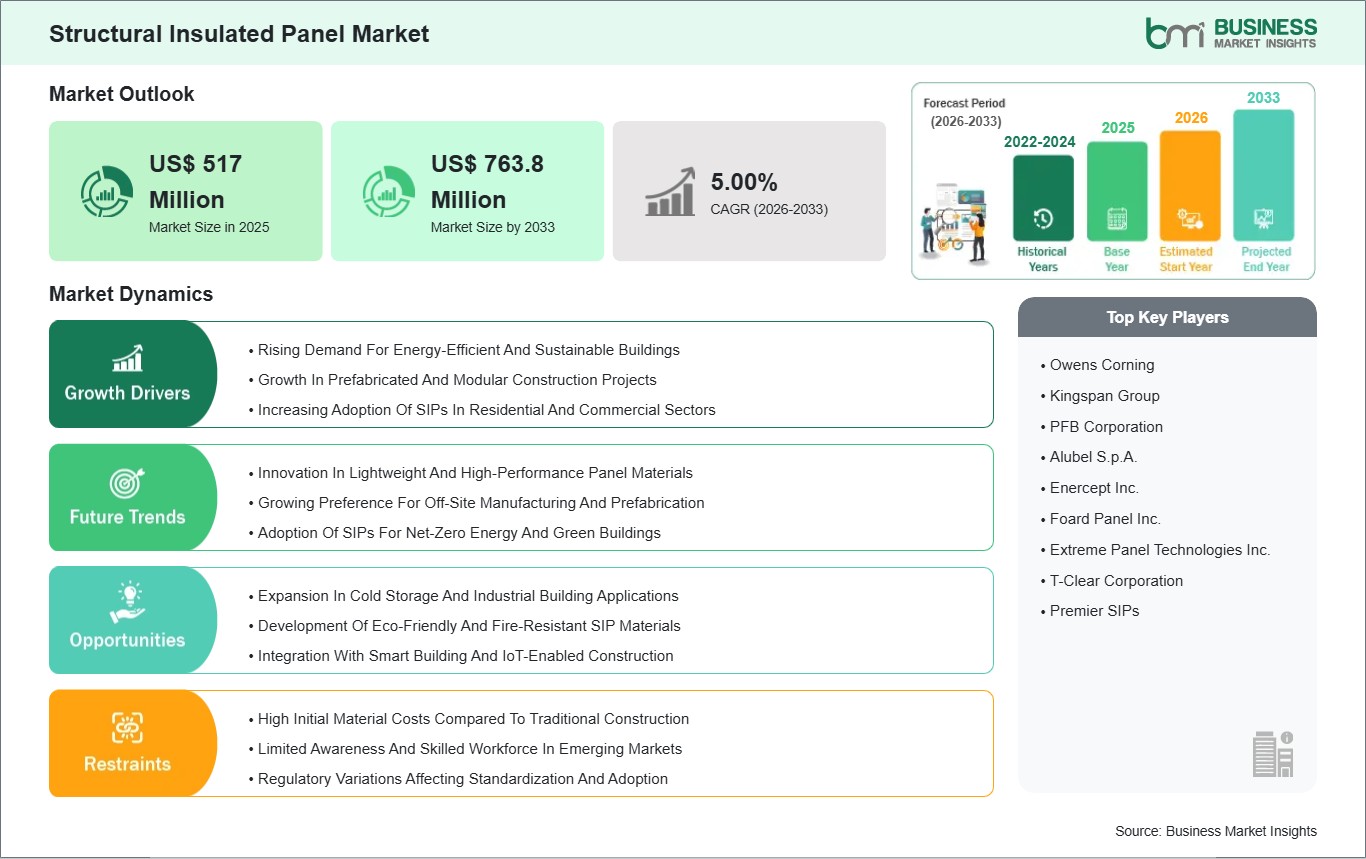

The Structural Insulated Panel Market size is expected to reach US$ 763.8 million by 2033 from US$ 517. million in 2025. The market is estimated to record a CAGR of 5.00% from 2026 to 2033.

Executive Summary and Global Market Analysis:

The global structural insulated panel (SIP) market is expanding as the construction industry increasingly prioritizes energy efficiency, sustainability, and faster project delivery. The building components known as structural insulated panels consist of an insulating foam core, which construction workers install between two structural facings that typically use oriented strand board (OSB) and metal and cementitious panels. The panels provide excellent thermal insulation and structural durability, which enable developers to construct residential, commercial and industrial projects at reduced labor costs and construction time. The market sees primary growth because customers demand building envelopes that provide both energy efficiency and high performance. The combination of rising energy expenses with stricter building regulations worldwide has led developers, architects and builders to select materials that improve thermal insulation together with materials that decrease energy needs for building operations.

SIPs provide consistent insulation with minimal thermal bridging, which enables structures to meet stringent energy performance requirements and obtain certifications such as LEED and Passive House. The prefabricated design of these products enables construction teams to complete building projects more quickly while generating less waste on construction sites, which matches the construction industries move toward modular construction methods and sustainable building methods.

The market experiences its current condition because green building projects, urban infrastructure programs and renovation projects in established and developing nations experience rapid expansion. SIPs are increasingly used in school buildings, healthcare facilities, cold storage warehouses, and multi‑family housing due to their durability, fire resistance, and acoustic performance. The market operates under multiple existing obstacles. The construction industry needs to overcome two main problems because people think about building material prices, and they do not understand new building methods. The integration of SIPs faces two main obstacles because different regional standards exist, and some areas lack qualified installers. The structural insulated panel market will continue its global growth because panel materials will undergo new innovations, supply chain operations will improve, and construction methods will focus more on low‑carbon practices.

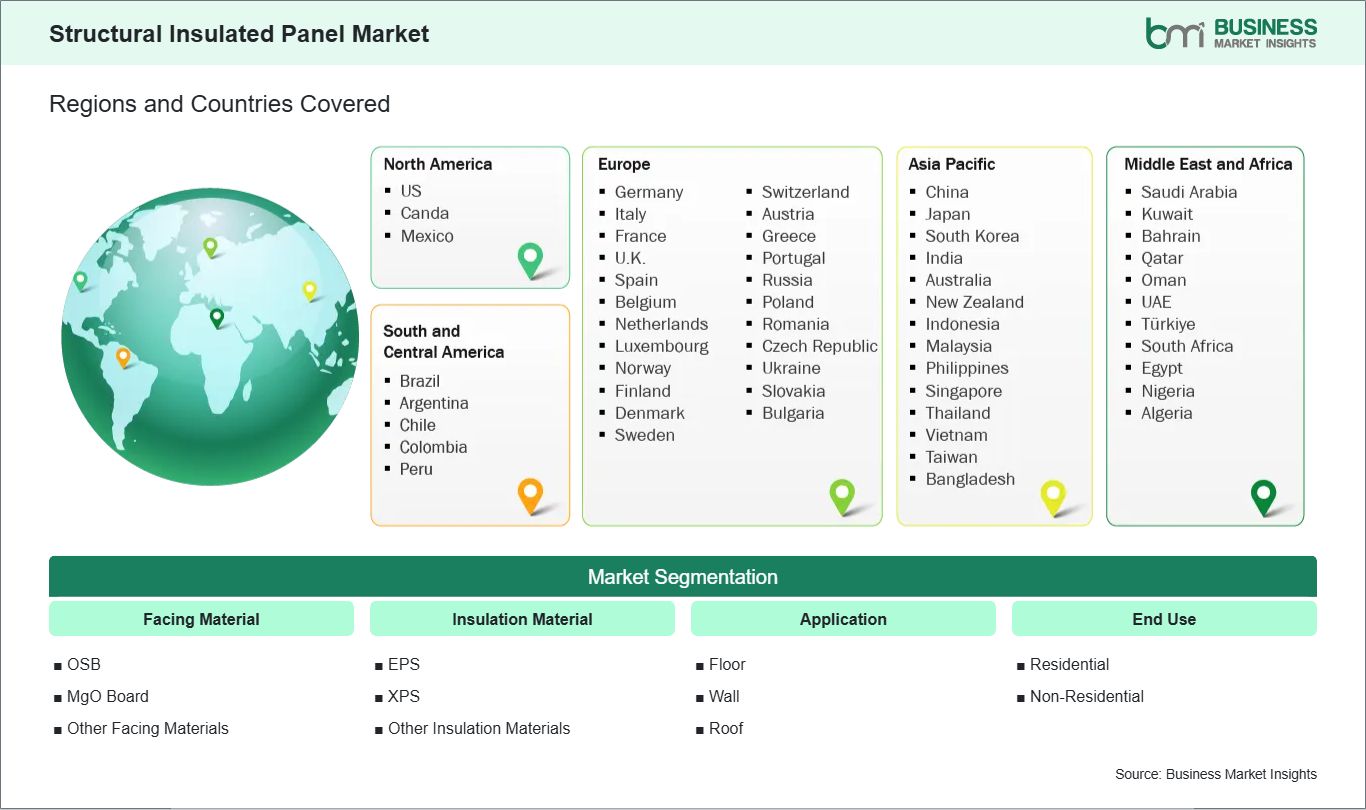

Key segments that contributed to the derivation of the structural insulated panel market analysis are facing material, insulation material, application, and end use.

By facing material, the structural insulated panel market is segmented into OSB, MgO board, other facing materials. The OSB segment dominated the market in 2025.

Based on insulation material, the structural insulated panel market is categorized into EPS, XPS, other insulation materials. The EPS segment dominated the market in 2025.

On the basis of application, the structural insulated panel market is categorized into floor, wall, roof. The wall segment dominated the market in 2025.

In terms of end use, the structural insulated panel market is categorized into residential, non‑residential. The residential segment dominated the market in 2025.

Structural Insulated Panel Market Drivers and Opportunities:

Rising Demand For Energy‑Efficient And Sustainable Buildings

The global structural insulated panel market is significantly propelled by the rising demand for energy‑efficient and sustainable buildings across residential, commercial, and institutional sectors. As governments and developers focus on reducing energy consumption and minimizing environmental impact, SIPs have emerged as a preferred solution due to their superior thermal performance and minimal thermal bridging. Unlike traditional construction methods that often struggle to meet stringent energy codes, SIP‑based structures deliver consistent insulation, helping buildings maintain occupant comfort while lowering operational energy costs over the long term. This energy focus resonates with global sustainability initiatives and green building certifications that prioritize low‑impact materials and systems.

Increasing awareness of lifecycle performance has pushed architects and builders to specify structural insulated panels in new constructions. In Europe and North America, for example, rigorous building codes and incentives for net‑zero energy certification have driven greater adoption of high‑performance building envelopes. These panels also support healthier indoor environments by reducing drafts and moisture infiltration, which aligns with occupant wellbeing priorities in modern design.

Additionally, the trend toward sustainable urbanization in rapidly developing regions is strengthening SIP demand. In Asia‑Pacific and Latin America, developers are incorporating energy‑efficient panels into high‑rise residential towers, institutional campuses, and mixed‑use developments to strike a balance between rapid growth and environmental stewardship. This convergence of regulatory pressure, consumer preference for green buildings, and the clear economic value of reduced energy use has positioned structural insulated panels as a cornerstone of energy‑efficient construction worldwide.

Expansion In Cold Storage And Industrial Building Applications

The expansion of cold storage and industrial building applications is another critical driver for the global structural insulated panel market. Cold storage facilities—used in food processing, pharmaceuticals, and logistics—demand high‑performance insulation to maintain strict temperature controls. SIPs provide a reliable, thermally robust solution that can withstand repeated temperature cycling while minimizing energy loss. As global supply chains become more complex and temperature‑controlled logistics gain importance, manufacturers and warehouse operators are increasingly turning to SIPs to enhance operational efficiency and reduce long‑term energy expenses.

Industrial buildings also benefit from SIP integration due to their structural strength, ease of installation, and ability to support large clear‑span designs. In manufacturing hubs across North America, Europe, and Asia‑Pacific, structural insulated panels are used in factories, distribution centers, and assembly plants that require durable building envelopes capable of supporting heavy equipment and environmental control systems. SIPs also contribute to faster build times, which is particularly valuable in regions where industrial expansion must keep pace with economic development and competitive pressures.

Moreover, emerging economies are recognizing the value of SIPs in industrial applications where climate conditions demand robust insulation. In the Middle East and Africa, for example, SIP‑based cold storage solutions are becoming more common as stakeholders in agribusiness and pharmaceuticals invest in facilities that ensure product integrity amid extreme temperature variations. This geographic diversification in end‑use demand reinforces the importance of structural insulated panels beyond traditional residential and commercial contexts, highlighting their versatility and value in specialized construction sectors.

Structural Insulated Panel Market Size and Share Analysis:

The structural insulated panel market demonstrates steady growth, with size and share analysis highlighting evolving trends and competitive dynamics among key players. The report examines subsegments categorized within facing material, insulation material, application, and end use, offering insights into their contribution to overall market performance.

By facing material, the OSB subsegment dominated the market in 2025, driven by its cost-effectiveness, high structural strength, and wide availability for use in structural insulated panels.

Based on insulation material, the EPS subsegment dominated the market in 2025, driven by its lightweight nature, excellent thermal insulation properties, and low production cost.

In terms of application, the wall subsegment dominated the market in 2025, driven by high demand in building construction for energy-efficient and easy-to-install structural insulated panels.

On the basis of end use, the residential subsegment dominated the market in 2025, driven by rapid growth in housing construction and the increasing adoption of energy-efficient building materials.

Australia, China, India, Japan, South Korea, Indonesia, Malaysia, Philippines, Singapore, Thailand, Vietnam, Bangladesh, New Zealand, Taiwan

South and Central America

Brazil, Argentina, Peru, Chile, Colombia

Middle East and Africa

Bahrain, Kuwait, Oman, Qatar, Saudi Arabia, United Arab Emirates, Turkiye, South Africa, Egypt, Algeria, Nigeria

Market leaders and key company profiles

Owens Corning

Kingspan Group

PFB Corporation

Alubel S.p.A.

Enercept Inc.

Foard Panel Inc.

Extreme Panel Technologies Inc.

T-Clear Corporation

Premier SIPs

Get more information on this report

Structural Insulated Panel Market Report Coverage and Deliverables:

The "Structural Insulated Panel Market Size and Forecast (2022 - 2033)" report provides a detailed analysis of the market covering below areas:

Structural Insulated Panel Market size and forecast at global, regional, and country levels for all the key market segments covered under the scope

Structural Insulated Panel Market trends, as well as drivers, restraints, and opportunities

Structural Insulated Panel Market analysis covering key trends, global and regional framework, major players, regulations, and recent developments

Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments for the Structural Insulated Panel Market

Detailed company profiles, including SWOT analysis

The geographical scope of the Structural Insulated Panel Market report is divided into North America, Asia Pacific, Europe, Middle East & Africa, and South & Central America. North America held the largest share in 2025.

The global structural insulated panel market shows diverse regional adoption patterns, with North America leading because its construction industry has reached maturity, its building standards focus on energy efficiency and its prefabricated building system facilities. The region uses SIPs for various building types, which include residential spaces, commercial areas and industrial sectors that require quick building time and exceptional insulation capabilities. The region maintains its market leadership because established manufacturers and distributors and industry groups work together to ensure quality control while providing training for professional installers.

The Asia Pacific market shows rapid growth because urban areas expand, construction projects increase and sustainable energy-efficient building practices become more common in China India and Japan. SIPs have become the preferred building material for developers who design residential high-rises, commercial complexes and cold chain facilities because they want to use equipment that enables fast construction and excellent thermal performance.

The European building industry uses SIPs as a result of new regulations that require carbon reductions and energy performance improvements and building certifications, which particularly benefit Germany, France and Nordic countries that use green building practices to create new buildings and retrofit existing structures with prefabricated panels.

The Middle East and Africa region is slowly implementing SIP technology for their industrial and commercial and modular residential building projects, while the United Arab Emirates and South Africa develop sustainable construction solutions to address severe climate conditions and their fast infrastructure development.

The South and Central American market is currently developing because residential construction, cold storage, and commercial modular projects are growing through Brazil and Argentina where developers need energy-efficient building solutions that provide high performance.

The energy conservation knowledge of people through all regions, their need for fast construction work and their movement toward prefabricated and modular building techniques drive growth in all regions.

Get more information on this report

Structural Insulated Panel Market Research Report Guidance:

The report includes qualitative and quantitative data in the Structural Insulated Panel Market across facing material, insulation material, application, end use and geography.

The report starts with the key takeaways (chapter 2), highlighting key trends and outlook of the Structural Insulated Panel Market.

Chapter 3 focuses on the research methodology of the study.

Chapter 4 includes ecosystem analysis.

Chapter 5 highlights the major industry dynamics in the Structural Insulated Panel Market, including factors that are driving the market, prevailing deterrents, potential opportunities, as well as future trends. Impact analysis of these drivers and restraints is also covered in this section.

Chapter 6 discusses the Structural Insulated Panel Market scenario, in terms of historical market revenues, and forecast till the year 2033.

Chapters 7 to 11 cover Structural Insulated Panel Market segments by facing material, insulation material, application, end use and geography across North America, Asia Pacific, Europe, Middle East & Africa, and South & Central America. They cover the market revenue forecast and factors driving the market.

Chapter 12 describes the competitive analysis along with the heat map analysis for the key players operating in the market.

Chapter 13 describes the industry landscape analysis. It provides detailed descriptions of business activities such as market initiatives, new developments, mergers, and joint ventures globally, along with a competitive landscape.

Chapter 14 provides detailed profiles of the major companies operating in the Structural Insulated Panel Market. Companies have been profiled on the basis of their key facts, business descriptions, products, financial overview, SWOT analysis, and key developments.

Chapter 15, i.e., the appendix, is inclusive of a brief overview of the company, a list of abbreviations, and a disclaimer.

Structural Insulated Panel Market News and Key Development:

The Structural Insulated Panel Market is evaluated by gathering qualitative and quantitative data post primary and secondary research, which includes important corporate publications, association data, and databases. A few of the key developments in the structural insulated panel market are:

In April 2024, Metl‑Span, a Nucor company, announced that it had completed construction of a new insulated metal panel manufacturing facility in Brigham City, Utah, which will produce high‑performance insulated wall and roof panels to enhance construction efficiency and energy performance, illustrating expansion of insulated panel production capacity in North America.

In February 2024, Owens Corning announced that it initiated a review of strategic alternatives for its global glass reinforcements business, which is part of its broader building materials portfolio. While this strategic review focuses on glass reinforcement, it reflects the company`s broader effort to optimize its portfolio within building and construction materials — a space that includes insulation solutions often paired with structural insulated panels for energy‑efficient buildings.

Key Sources Referred:

World Health Organization (WHO)Organisation for Economic Cooperation and Development (OECD)The World Bank GroupWorldometerThe LancetInternational Bar AssociationInternational Trade Administration

The List of Companies - Structural Insulated Panel Market

Owens Corning

Kingspan Group

PFB Corporation

Alubel S.p.A.

Enercept Inc.

Foard Panel Inc.

Extreme Panel Technologies Inc.

T-Clear Corporation

Premier SIPs

About Author— Chemicals and Materials Research Team

Suraj Sajeev is a market research and consulting professional with nearly 10 years of experience across Life Sciences, Consumer Goods, Food & Beverages, Materials & Chemicals, and Automotive industries. Throughout his career, he has successfully managed and delivered custom market research and consulting engagements, enabling clients to make informed strategic decisions through actionable market intelligence.

Suraj has extensive expertise in end-to-end project management, including proposal development, market assessment, competitive intelligence, opportunity analysis, market sizing and forecasting, strategic recommendation..

Show More

Frequently Asked Questions

How big is the Structural Insulated Panel Market?

The Structural Insulated Panel Market is valued at US$ 517 Million in 2025, it is projected to reach US$ 763.8 Million by 2033.

What is the CAGR for Structural Insulated Panel Market by (2026 - 2033)?

As per our report Structural Insulated Panel Market, the market size is valued at US$ 517 Million in 2025, projecting it to reach US$ 763.8 Million by 2033. This translates to a CAGR of approximately 5.00% during the forecast period.

What segments are covered in this report?

The Structural Insulated Panel Market report typically cover these key segments-

Facing Material (OSB, MgO Board, Other Facing Materials)

Insulation Material (EPS, XPS, Other Insulation Materials)

Application (Floor, Wall, Roof)

End Use (Residential, Non-Residential)

What is the historic period, base year, and forecast period taken for Structural Insulated Panel Market?

The historic period, base year, and forecast period can vary slightly depending on the specific market research report. However, for the Structural Insulated Panel Market report:

Historic Period : 2022-2024

Base Year : 2025

Forecast Period : 2026-2033

Who are the major players in Structural Insulated Panel Market?

The Structural Insulated Panel Market is populated by several key players, each contributing to its growth and innovation. Some of the major players include:

Owens Corning

Kingspan Group

PFB Corporation

Alubel S.p.A.

Enercept Inc.

Foard Panel Inc.

Extreme Panel Technologies Inc.

T-Clear Corporation

Premier SIPs

Who should buy this report?

The Structural Insulated Panel Market report is valuable for diverse stakeholders, including:

Investors: Provides insights for investment decisions pertaining to market growth, companies, or industry insights. Helps assess market attractiveness and potential returns.

Industry Players: Offers competitive intelligence, market sizing, and trend analysis to inform strategic planning, product development, and sales strategies.

Suppliers and Manufacturers: Helps understand market demand for components, materials, and services related to concerned industry.

Researchers and Consultants: Provides data and analysis for academic research, consulting projects, and market studies.

Financial Institutions: Helps assess risks and opportunities associated with financing or investing in the concerned market.

Essentially, anyone involved in or considering involvement in the Structural Insulated Panel Market value chain can benefit from the information contained in a comprehensive market report.

Get Free Sample For Structural Insulated Panel Market

Get Free Sample For Structural Insulated Panel Market